Food And Beverage Metal Cans Market Size and Growth

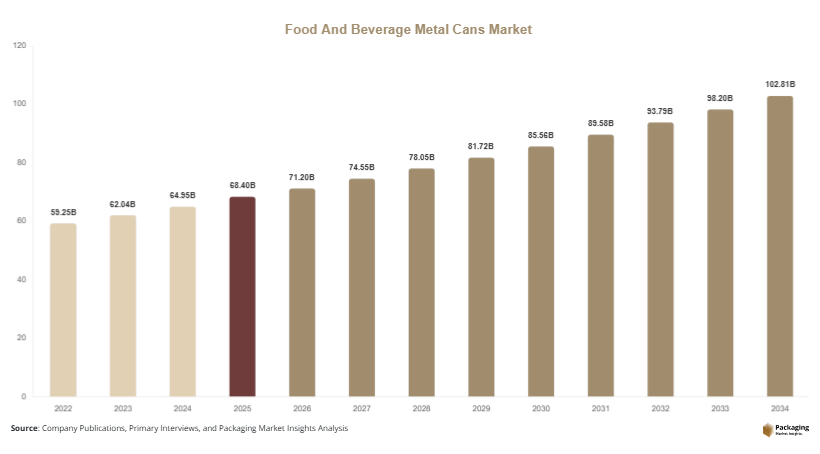

The global food and beverage metal cans market was valued at approximately USD 68.4 billion in 2025 and is estimated to reach USD 71.2 billion in 2026, progressing toward USD 102.5 billion by 2034, at a CAGR of 4.7% from 2025 to 2034. This growth is strongly influenced by rising consumption of ready-to-drink beverages, expanding urban populations, and the increasing need for extended shelf-life packaging. The food and beverage metal cans market is witnessing steady expansion due to the increasing demand for durable, sustainable, and cost-effective packaging solutions across the global food and beverage industry.

One of the major factors driving market growth is the shift toward environmentally sustainable materials. Metal cans, particularly aluminum, offer high recyclability and align with global sustainability targets. Additionally, technological advancements in can manufacturing, such as lightweight designs and enhanced coating solutions, are improving efficiency and reducing production costs. The demand for convenience packaging is also rising as consumers prefer portable and easy-to-store food and beverage products.

Key Highlights:

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 5.6%.

- Aluminum cans led the material segment with a 61.4% share, while steel cans are expected to grow at a CAGR of 4.9%.

- Beverage applications dominated with a 56.8% share, while food applications are forecasted to grow at a CAGR of 4.5%.

- Carbonated drinks led the application segment with 34.7% share, while energy drinks are expected to grow at a CAGR of 6.1%.

- China remained the dominant country with a market size of USD 12.4 billion in 2025 and USD 13.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing emphasis on sustainable and circular packaging solutions

The increasing focus on environmental sustainability is significantly shaping the food and beverage metal cans market. Governments and regulatory bodies across various regions are enforcing strict guidelines to reduce plastic waste, encouraging manufacturers to shift toward recyclable materials such as aluminum and steel. Metal cans are gaining traction due to their ability to be recycled multiple times without quality degradation. This characteristic supports the development of a circular economy, where materials are continuously reused. In addition, brands are incorporating sustainability messaging on packaging to attract environmentally conscious consumers. Investments in recycling infrastructure and closed-loop systems are further accelerating the adoption of metal cans across the food and beverage industry.

Increasing adoption of premium and customized packaging formats

The demand for visually appealing and differentiated packaging is growing across the beverage sector. Manufacturers are focusing on innovative can designs, including unique shapes, finishes, and high-quality printing technologies, to enhance brand recognition. Premium packaging formats such as matte finishes, embossed surfaces, and digitally printed cans are becoming more common. These features help brands stand out in competitive retail environments and improve consumer engagement. The rise of craft beverages, including specialty beers and functional drinks, is also contributing to this trend. Customized packaging not only enhances product appeal but also strengthens brand identity and consumer loyalty.

Market Drivers

Rising consumption of ready-to-drink beverages and convenience foods

The increasing demand for ready-to-drink beverages is a major factor contributing to the growth of the food and beverage metal cans market. Urbanization and busy lifestyles have led consumers to prefer convenient and portable food and beverage options. Metal cans are lightweight, easy to transport, and provide excellent protection, making them suitable for on-the-go consumption. The growth of energy drinks, carbonated beverages, and canned alcoholic drinks is further driving demand. In addition, metal cans help preserve flavor, carbonation, and nutritional value, ensuring product quality. This makes them a preferred packaging choice for manufacturers aiming to meet evolving consumer preferences.

Supportive regulatory environment promoting recyclable packaging

Government policies aimed at reducing environmental impact are encouraging the adoption of recyclable packaging materials. Many countries are implementing regulations that limit the use of single-use plastics and promote sustainable alternatives. Metal cans, being highly recyclable, are benefiting from these initiatives. Deposit return schemes and recycling mandates are increasing collection rates and improving material recovery. Companies are also aligning their operations with environmental, social, and governance goals by adopting sustainable packaging solutions. This regulatory support is playing a key role in strengthening the market for metal cans in the food and beverage industry.

Market Restraint

Volatility in raw material costs and supply chain disruptions

Fluctuating prices of raw materials such as aluminum and steel pose a significant challenge to the food and beverage metal cans market. These materials are subject to global supply-demand dynamics, geopolitical factors, and trade regulations, which can lead to price instability. Increased production costs directly impact profit margins for manufacturers and may result in higher prices for end consumers. Additionally, supply chain disruptions, including transportation delays and shortages of raw materials, can affect production efficiency. Smaller manufacturers often face difficulties in managing these challenges due to limited financial resources. This uncertainty can slow market growth and limit expansion opportunities in price-sensitive regions.

Market Opportunities

Expanding demand in emerging economies

Emerging markets present strong growth potential for the food and beverage metal cans market. Rapid urbanization, increasing disposable incomes, and changing consumption patterns are driving demand for packaged food and beverages in regions such as Asia Pacific, Latin America, and parts of Africa. The growth of modern retail infrastructure, including supermarkets and convenience stores, is improving product accessibility. Additionally, rising awareness regarding food safety and hygiene is encouraging consumers to choose packaged products. Metal cans offer durability and extended shelf life, making them suitable for these markets. This trend is expected to create new opportunities for manufacturers to expand their presence and increase market share.

Advancements in manufacturing and smart packaging technologies

Technological innovations are opening new avenues for growth in the food and beverage metal cans market. Developments such as lightweight can designs, improved internal coatings, and advanced printing technologies are enhancing product performance and reducing costs. Smart packaging solutions, including QR codes and interactive labels, are enabling brands to engage directly with consumers. Automation and digitalization in manufacturing processes are improving production efficiency and scalability. These advancements allow companies to offer customized and high-quality packaging solutions while maintaining cost-effectiveness. As a result, technological progress is expected to play a crucial role in shaping the future of the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 68.4 Billion |

| Market Size in 2026 | USD 71.2 Billion |

| Market Size in 2034 | USD 102.5 Billion |

| CAGR | 4.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Aluminum cans dominated the material segment with a market share of 61.4% in 2024, primarily due to their lightweight nature, high recyclability, and excellent barrier properties. Aluminum is widely preferred in beverage packaging because it effectively preserves taste, carbonation, and freshness. Additionally, its ability to be recycled multiple times without losing quality aligns with global sustainability initiatives. The increasing adoption of eco-friendly packaging solutions is further driving the demand for aluminum cans across the food and beverage industry.

Steel cans are expected to witness the fastest growth, registering a CAGR of 4.9% during the forecast period. Steel offers high durability and strength, making it suitable for packaging a wide range of food products such as vegetables, soups, and ready meals. Advancements in coating technologies are improving corrosion resistance and extending shelf life. The growing demand for long-lasting and safe food packaging is contributing to the increased use of steel cans.

By Application

Beverage applications accounted for the largest share of 56.8% in 2024, driven by the high consumption of soft drinks, energy drinks, and alcoholic beverages. Metal cans are widely used in the beverage sector due to their ability to maintain product quality and prevent contamination. The increasing demand for ready-to-drink beverages and convenience packaging is further supporting growth. Additionally, metal cans offer portability and ease of storage, making them a preferred choice among consumers.

Food applications are expected to grow steadily, with a CAGR of 4.5% during the forecast period. The rising demand for packaged and processed food products, including canned fruits, vegetables, and ready meals, is driving this segment. Metal cans provide superior protection against external factors such as light and oxygen, ensuring food safety and extended shelf life. The growing emphasis on hygiene and food preservation is further boosting the adoption of metal cans in food applications.

By End-Use

Carbonated drinks held the largest share of 34.7% in 2024, supported by their widespread global consumption. Metal cans are the preferred packaging format for carbonated beverages due to their ability to retain carbonation and prevent flavor loss. The availability of different can sizes and designs enhances consumer convenience. Increasing demand for flavored and low-sugar beverages is further contributing to the growth of this segment.

Energy drinks are expected to be the fastest-growing subsegment, with a CAGR of 6.1% during the forecast period. The rising popularity of energy drinks among young consumers and working professionals is driving demand. Metal cans provide durability and portability, making them suitable for this category. Additionally, innovative packaging designs and strong branding strategies are attracting consumers and supporting segment growth.

Food And Beverage Metal Cans Market Segmentations

By Material Type

- Aluminum

- Steel

By Application

- Beverages

- Food

By End-Use

- Carbonated Drinks

- Energy Drinks

- Alcoholic Beverages

- Ready-to-Eat Foods

Regional Analysis

North America

North America held a market share of approximately 24.6% in 2025 and is expected to grow at a CAGR of 4.3% during the forecast period. The region benefits from a well-established food and beverage industry and high consumption of canned products. The demand for ready-to-drink beverages, including energy drinks and canned coffee, continues to support market expansion. Additionally, advanced recycling infrastructure and strong environmental awareness among consumers are contributing to sustained growth.

The United States remains the dominant country in this region, supported by its large consumer base and developed retail sector. A key growth factor is the widespread implementation of deposit return systems, which encourage recycling and improve collection rates of used cans. This system supports sustainability initiatives and increases the adoption of metal cans across various applications in the country.

Europe

Europe accounted for around 22.8% of the global market share in 2025 and is projected to grow at a CAGR of 4.1%. The region’s focus on sustainability and strict environmental regulations are major drivers of market growth. Increasing demand for recyclable packaging and the popularity of canned beverages, including craft beer and sparkling drinks, are further supporting expansion. Technological advancements in packaging are also contributing to product innovation.

Germany leads the European market due to its strong industrial base and high recycling efficiency. A significant growth factor is the implementation of stringent packaging waste regulations, which promote the use of recyclable materials. These policies encourage manufacturers to shift toward metal cans, aligning with regional sustainability goals and supporting market development.

Asia Pacific

Asia Pacific dominated the global market with a share of 38.2% in 2025 and is expected to grow at a CAGR of 5.2%. Rapid urbanization, population growth, and increasing disposable incomes are driving demand for packaged food and beverages. The expansion of e-commerce platforms and retail networks is further boosting market growth. Additionally, the rising popularity of ready-to-drink beverages is increasing the adoption of metal cans.

China is the leading country in the region, supported by its large-scale manufacturing capabilities and growing consumer demand. A major growth factor is the rapid expansion of the beverage industry, particularly in energy drinks and functional beverages. This trend is creating substantial demand for metal cans and contributing to overall market growth in the region.

Middle East & Africa

The Middle East & Africa region accounted for a market share of 7.6% in 2025 and is expected to grow at a CAGR of 4.8%. Increasing urbanization and rising disposable incomes are driving demand for packaged food and beverages. The growth of tourism and hospitality industries is also contributing to higher consumption of canned beverages. Improvements in retail infrastructure are further supporting market expansion.

Saudi Arabia is the dominant country in this region, driven by its strong demand for packaged products. A key growth factor is the increasing investment in food processing and packaging industries. These investments are enhancing production capabilities and promoting the adoption of metal cans across various applications in the region.

Latin America

Latin America held a market share of 6.8% in 2025 and is projected to grow at the fastest CAGR of 5.6%. The region’s expanding middle-class population and increasing demand for convenient food and beverage products are key growth drivers. The development of retail channels and rising consumption of packaged beverages are further contributing to market expansion.

Brazil is the leading country in Latin America, supported by its large beverage industry. A unique growth factor is the growing popularity of canned alcoholic beverages, including beer and ready-to-drink cocktails. This trend is significantly increasing demand for metal cans and supporting the region’s market growth.

Competitive Landscape

The food and beverage metal cans market is characterized by a competitive environment with several global and regional players focusing on innovation, sustainability, and capacity expansion. Companies are investing in advanced manufacturing technologies and eco-friendly materials to enhance their market position and meet evolving consumer demands.

Ball Corporation is recognized as a leading player in the market, supported by its strong global presence and extensive product portfolio. The company has recently expanded its production capacity by establishing new facilities to address the growing demand for aluminum cans. Other key players are focusing on strategic collaborations, mergers, and acquisitions to strengthen their distribution networks and technological capabilities.

Manufacturers are increasingly adopting digital printing technologies and lightweight can designs to reduce material usage and improve product differentiation. Sustainability initiatives, including improving recycling rates and lowering carbon emissions, are also a central focus. These strategies are helping companies remain competitive and adapt to changing market dynamics.

Key Players List

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group

- CANPACK S.A.

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings Ltd.

- Orora Limited

- Kian Joo Can Factory Berhad

- CPMC Holdings Limited

- Nampak Ltd.

- BWAY Corporation

- Massilly Holding S.A.S

- Universal Can Corporation

- Kingcan Holdings Limited

- Envases Universales Group