Foam Packaging Market Report Size and Growth

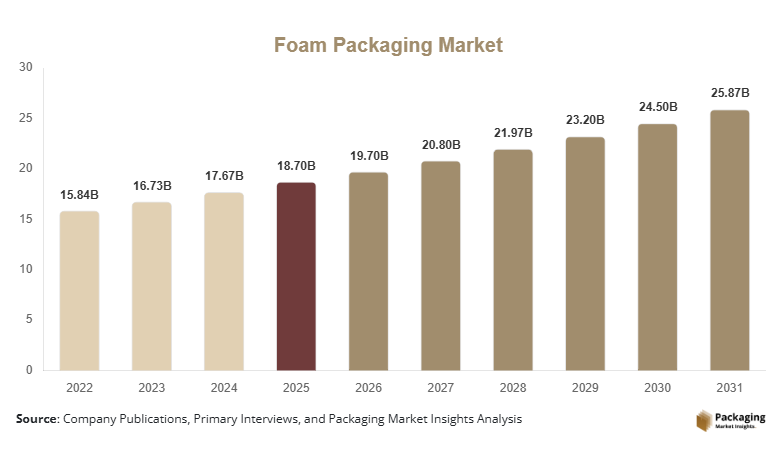

The Foam packaging marketsize was valued at USD 18.7 billion in 2025 and is projected to reach USD 25.9 billion by 2030, expanding at a compound annual growth rate (CAGR) of 5.6% during 2025–2031. Foam packaging has become an important component in protective packaging solutions due to its lightweight properties, cushioning capability, and cost efficiency. Industries such as electronics, food and beverages, healthcare, and e-commerce rely on foam packaging to prevent damage during storage and transportation.

One of the major global factors supporting the growth of the Foam packaging marketis the rapid expansion of the e-commerce and consumer electronics industries. The growth of online retail has increased the demand for protective packaging materials capable of minimizing damage during shipping. Foam packaging, particularly polyethylene and polyurethane foam solutions, offers high shock absorption and flexibility, making it suitable for packaging delicate products such as smartphones, laptops, and medical devices.

Additionally, manufacturers are introducing recyclable and bio-based foam packaging solutions to address environmental concerns associated with traditional plastic packaging. Advancements in manufacturing technologies have improved product performance while reducing material consumption, which supports cost optimization for manufacturers and logistics providers.

Key Highlights

- Dominant region: Asia Pacific accounted for 39.4% market share in 2025, while Latin America is projected to register the fastest CAGR of 6.8% during the forecast period.

- Leading subsegments:

- By Material: Polyethylene (PE) foam held the largest share.

- By Product Type: Foam sheets dominated the market.

- By End-Use Industry: Electronics packaging led the segment.

- Fastest-growing subsegments:

- Expanded polypropylene foam is expected to grow at 7.1% CAGR.

- Custom molded foam packaging is projected to grow at 6.9% CAGR.

- Dominant country: The United States Foam packaging marketwas valued at USD 3.6 billion in 2025 and increased to USD 3.8 billion in 2026 due to strong demand from logistics and consumer electronics sectors.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable Foam Packaging

Sustainability has emerged as a defining trend in the Foam Packaging Market. Governments and regulatory bodies worldwide are encouraging manufacturers to reduce plastic waste and improve recycling capabilities. As a result, packaging producers are developing recyclable polyethylene foams, biodegradable foam alternatives, and foam materials derived from renewable resources.

Companies are also investing in closed-loop recycling systems that allow used foam packaging to be collected and reprocessed into new products. This approach helps reduce landfill waste while lowering production costs over time. Sustainability initiatives have encouraged several packaging suppliers to replace traditional expanded polystyrene (EPS) with recyclable polyethylene and polypropylene foam materials.

Increasing Demand for Custom Protective Packaging

Another key trend shaping the Foam packaging marketgrowth is the increasing demand for customized packaging solutions. Manufacturers are using advanced cutting technologies, digital design tools, and automated molding processes to produce foam packaging tailored to specific product shapes.

Custom molded foam packaging is widely used in electronics, medical devices, and industrial equipment shipping. These solutions offer better product stability, reduced material waste, and improved protection compared with generic packaging materials. As supply chains become more complex and global shipments increase, customized foam packaging solutions are expected to become more common across industries.

Market Drivers

Expansion of the Global E-Commerce Industry

The rapid growth of e-commerce has significantly supported the Foam packaging marketgrowth. Online retailers rely on protective packaging solutions that minimize product damage during shipping and handling. Foam packaging materials provide excellent shock absorption and vibration resistance, making them suitable for packaging fragile consumer goods such as electronics, glassware, and appliances.

As global online retail continues to expand, logistics companies require packaging solutions that balance protection with cost efficiency. Foam packaging offers lightweight characteristics that reduce shipping costs while maintaining product safety. These advantages have strengthened the role of foam packaging in modern logistics operations.

Increasing Demand from Consumer Electronics Manufacturing

Consumer electronics manufacturing has grown steadily in recent years, creating strong demand for protective packaging materials. Devices such as smartphones, tablets, laptops, and wearable electronics require packaging that prevents physical damage during transportation.

Foam packaging materials provide effective cushioning and structural support, which helps maintain product integrity throughout the distribution process. With global electronics production increasing, especially in Asia Pacific, the demand for foam packaging solutions continues to rise across multiple supply chains.

Market Restraint

Environmental Concerns Related to Plastic Foam Waste

Despite its widespread use, environmental concerns associated with plastic foam packaging remain a major restraint for the Foam Packaging Market. Many foam materials, particularly expanded polystyrene, are difficult to recycle and often end up in landfills or oceans.

Several governments have implemented regulations limiting the use of certain foam materials in packaging applications. These restrictions are particularly evident in single-use food packaging segments. As sustainability regulations become stricter, packaging manufacturers must invest in alternative materials or recycling technologies.

In addition, consumer awareness regarding environmental sustainability has increased significantly. Many businesses are transitioning toward paper-based or biodegradable packaging solutions to align with corporate sustainability goals. This shift can limit the adoption of traditional foam packaging materials in certain industries.

However, ongoing research and development efforts focused on recyclable and biodegradable foam materials may help address these challenges in the long term.

Market Opportunities

Development of Bio-Based Foam Materials

Bio-based foam packaging represents a promising opportunity in the Foam Packaging Market. Manufacturers are exploring materials derived from renewable resources such as corn starch, sugarcane, and plant fibers to produce sustainable foam packaging alternatives.

These materials provide similar cushioning performance while reducing environmental impact. As sustainability regulations continue to evolve, bio-based foam packaging solutions are expected to gain broader acceptance across food packaging, consumer goods, and electronics industries.

Growth in Cold Chain Logistics

The expansion of cold chain logistics offers another growth opportunity for foam packaging manufacturers. Temperature-sensitive products such as pharmaceuticals, vaccines, and perishable food require insulation during transportation.

Foam packaging materials offer strong thermal insulation properties, making them suitable for cold chain applications. With global demand for temperature-controlled logistics increasing, foam packaging solutions designed for insulation and protective transport are expected to experience steady demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.7 Billion |

| Market Size in 2026 | USD 19.7 Billion |

| Market Size in 2031 | USD 25.9 Billion |

| CAGR | 5.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Polyethylene (PE) foam dominated the material segment and accounted for 34.8% of the Foam packaging marketshare in 2024. This material gained widespread adoption due to its durability, lightweight structure, and strong shock-absorbing properties. Polyethylene foam is commonly used for protective packaging of electronics, appliances, and industrial equipment. Its flexibility and chemical resistance make it suitable for various packaging applications across multiple industries.

Expanded polypropylene (EPP) foam is projected to grow at the fastest CAGR of 7.1% during the forecast period. The material provides strong structural integrity and excellent energy absorption, making it suitable for reusable packaging systems. Industries that require durable protective packaging, such as automotive and electronics manufacturing, are expected to adopt expanded polypropylene foam solutions more frequently in the coming years.

By Product Type

Foam sheets held the largest share in the Foam packaging marketin 2024, accounting for 31.6% of total revenue. Foam sheets are widely used in packaging applications due to their versatility and ease of customization. They can be cut into different shapes and sizes to provide cushioning for fragile products during transportation. Many electronics manufacturers use foam sheets as protective layers within packaging boxes.

Custom molded foam packaging is expected to grow at a CAGR of 6.9% during the forecast period. This segment is gaining popularity because it provides precise product fit and enhanced protection compared with traditional packaging materials. Manufacturers increasingly prefer molded foam inserts for packaging high-value products such as electronics, medical devices, and industrial components.

By End-Use Industry

The electronics industry accounted for the largest share of the Foam packaging marketin 2024, contributing 36.2% of global revenue. Electronics manufacturers rely heavily on foam packaging materials to protect delicate components and finished products during transportation. Foam packaging solutions provide cushioning that helps reduce the risk of product damage.

The healthcare industry is expected to register the fastest growth with a CAGR of 6.5% during the forecast period. Increasing demand for safe transportation of medical equipment, diagnostic devices, and temperature-sensitive products has created new opportunities for foam packaging solutions. Healthcare logistics providers require packaging materials that ensure product safety while maintaining temperature control during transportation.

Foam Packaging Market Segmentations

By Material

- Polyethylene (PE) Foam

- Polyurethane (PU) Foam

- Expanded Polystyrene (EPS)

- Expanded Polypropylene (EPP)

- Others

By Product Type

- Foam Sheets

- Foam Rolls

- Custom Molded Foam

- Foam Pouches

- Foam Inserts

By End-Use Industry

- Electronics

- Food & Beverages

- Healthcare

- Automotive

- Consumer Goods

- Industrial Equipment

Regional Analysis

North America

North America accounted for 27.6% of the global Foam packaging marketshare in 2025. The region’s market growth is supported by strong demand from e-commerce logistics, electronics manufacturing, and food distribution industries. The Foam packaging marketforecast for North America will expand at a CAGR of 5.1% during 2025–2033 due to increasing investments in packaging innovation and supply chain infrastructure.

The United States remained the dominant country within the regional market. A key growth factor in the country is the strong presence of advanced manufacturing industries that require protective packaging solutions. Electronics manufacturers and logistics companies widely adopt foam packaging to reduce shipping damage and improve supply chain efficiency. The increasing adoption of automated packaging systems has also supported demand for foam packaging products in the United States.

Europe

Europe represented 22.3% of the global Foam packaging marketsize in 2025. The region benefits from well-established packaging manufacturing industries and strong demand from automotive and electronics sectors. The European market is projected to grow at a CAGR of 4.8% during the forecast period as packaging companies invest in sustainable materials and recycling technologies.

Germany dominated the regional market due to its strong industrial and manufacturing base. The country’s automotive and electronics industries require protective packaging solutions for domestic distribution and international exports. Foam packaging materials are widely used to protect components during shipping and storage. In addition, Germany’s advanced manufacturing ecosystem supports innovation in packaging materials and production processes.

Asia Pacific

Asia Pacific held the largest share of 39.4% in the Foam packaging marketin 2025. The region has experienced rapid industrialization, increased manufacturing output, and expanding consumer markets. The Foam packaging marketin Asia Pacific will grow at a CAGR of 6.4% during 2025–2033 due to strong demand from electronics production, retail logistics, and food packaging industries.

China remained the dominant country within the region. The country’s electronics manufacturing sector is one of the largest globally, creating strong demand for protective packaging materials. Foam packaging solutions are widely used to protect electronic devices during export shipments. Additionally, China’s expanding e-commerce sector has increased demand for cost-efficient packaging materials that provide product protection during delivery.

Middle East & Africa

The Middle East & Africa accounted for 5.1% of the global Foam packaging marketshare in 2025. The region has experienced moderate growth due to increasing industrial activities and infrastructure development. The Foam packaging marketoutlook for the region will expand at a CAGR of 5.3% through 2033 as manufacturing sectors continue to develop.

The United Arab Emirates dominated the regional market. A major growth factor in the country is the expansion of logistics and re-export trade hubs. As a global trading center, the UAE requires protective packaging solutions to support the transportation of electronics, industrial goods, and consumer products. Foam packaging plays an important role in ensuring product safety during international shipments.

Latin America

Latin America held 5.6% of the global Foam packaging marketshare in 2025. The regional market has been influenced by growing consumer goods industries and expanding retail distribution networks. The Foam packaging marketin Latin America will grow at a CAGR of 6.8% during the forecast period, making it the fastest-growing region.

Brazil emerged as the dominant country in the region. The growth factor supporting the market in Brazil is the expansion of domestic manufacturing and retail sectors. The country’s consumer electronics and appliance industries require protective packaging solutions to maintain product quality during transportation across long distances. Foam packaging provides effective cushioning and cost efficiency, which supports its adoption among manufacturers and distributors.

Competitive Landscape

The Foam packaging marketis moderately fragmented, with several global and regional manufacturers competing through product innovation, manufacturing expansion, and strategic partnerships. Companies focus on developing sustainable foam packaging materials and customized protective packaging solutions.

Sealed Air Corporation remains a leading company in the market due to its extensive portfolio of protective packaging solutions and strong global distribution network. The company recently introduced recyclable foam packaging products designed to reduce environmental impact while maintaining protective performance.

Other key companies continue to expand production capacity and invest in advanced manufacturing technologies to meet rising demand from e-commerce, electronics, and industrial sectors. Strategic collaborations between packaging manufacturers and logistics providers have also supported market expansion.

Key Players in the Foam Packaging Market

- Sealed Air Corporation

- Sonoco Products Company

- Pregis LLC

- BASF SE

- JSP Corporation

- Zotefoams PLC

- Foamcraft Inc.

- Rogers Corporation

- Armacell International S.A.

- Recticel NV

- UFP Technologies Inc.

- Woodbridge Foam Corporation

- Kaneka Corporation

- DS Smith Plc

- ACH Foam Technologies