Foam Cushioning Market Report Size and Growth

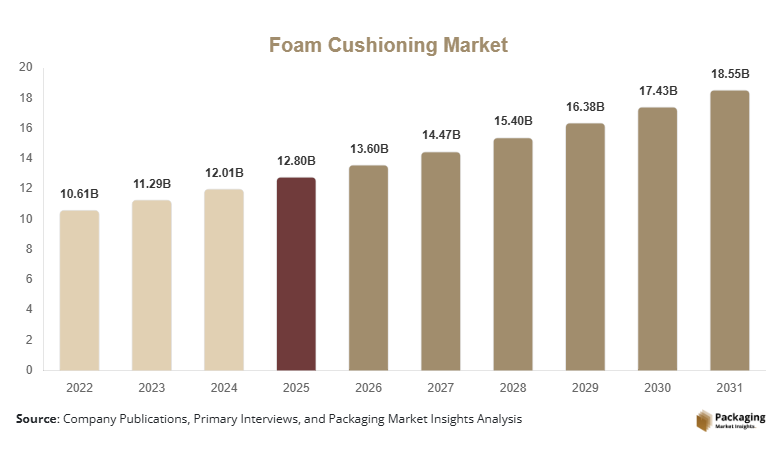

The Foam cushioning market was valued at USD 12.8 billion in 2025 and is projected to reach USD 18.7 billion by 2030, expanding at a compound annual growth rate (CAGR) of 6.4% during the forecast period (2025–2031). Foam cushioning materials are widely used in protective packaging, furniture, bedding, automotive interiors, and electronics packaging due to their ability to absorb shock, reduce vibration, and protect delicate products during transportation and storage. Increasing demand for lightweight protective materials across logistics and consumer goods sectors continues to influence the overall market size and growth trajectory.

A major global factor supporting the growth of the foam cushioning market is the rapid expansion of e-commerce and parcel delivery networks. As online retail continues to scale globally, the need for reliable protective packaging solutions has increased significantly. Foam cushioning materials such as polyethylene foam, polyurethane foam, and expanded polystyrene help prevent product damage during shipping, making them essential in modern supply chains. Companies are also focusing on sustainable and recyclable cushioning foam solutions to meet evolving regulatory requirements and environmental concerns.

The market analysis also reflects growing adoption across furniture and bedding industries, where foam cushioning enhances comfort and durability in mattresses, sofas, and seating products. Automotive manufacturers are increasingly integrating advanced foam materials into vehicle interiors to improve passenger comfort and noise insulation.

Key Highlights

- Asia Pacific held the dominant share of 38.6% of the foam cushioning market in 2025, while Latin America is expected to grow at the fastest CAGR of 7.3% during the forecast period.

- In the material segment, polyurethane foam was the leading subsegment, while polyethylene foam is projected to be the fastest-growing with a CAGR of 6.9%.

- Within end-use industries, packaging applications dominated the market, whereas automotive interiors are expected to register the fastest growth with a CAGR of 7.1%.

- China remained the dominant country market, valued at USD 2.3 billion in 2025 and estimated to reach USD 2.45 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Demand for Sustainable Cushioning Materials

Sustainability initiatives are influencing product development within the foam cushioning market. Manufacturers are gradually introducing recyclable, biodegradable, and bio-based foam materials to reduce environmental impact. Traditional petroleum-based foams have faced scrutiny due to recycling challenges and landfill accumulation. As a result, companies are investing in plant-based polyurethane foams and recyclable polyethylene foam alternatives.

In addition, regulatory frameworks encouraging circular economy models are prompting packaging companies to redesign cushioning materials for easier recycling and reuse. The development of molded pulp-foam hybrid cushioning products is another example of sustainable innovation shaping the industry outlook.

Increasing Integration of Foam Cushioning in Electronics Packaging

The global electronics sector has increased its reliance on precision protective packaging solutions. Foam cushioning is widely used to protect fragile electronic devices such as smartphones, laptops, televisions, and semiconductor components.

High-performance foams with anti-static properties are gaining traction because they protect sensitive electronic circuits from electrostatic discharge during shipping. Additionally, customized foam inserts designed through automated cutting technologies are becoming more common in consumer electronics packaging. This trend is expected to continue as global electronics shipments expand and product designs become more compact and fragile.

Market Drivers

Growth of the Global E-commerce Logistics Sector

The continuous expansion of online retail platforms has significantly increased demand for protective packaging materials. Foam cushioning materials help prevent product damage during long-distance shipping and last-mile delivery.

As logistics networks become more complex and shipment volumes increase, companies are prioritizing protective packaging solutions that minimize product returns and damage. Foam cushioning provides lightweight protection while maintaining packaging efficiency. This driver has contributed to consistent growth in the foam cushioning market across consumer electronics, home appliances, and personal care products.

Rising Demand from Furniture and Bedding Industries

The furniture and bedding industries represent another major growth driver for the foam cushioning market. Polyurethane foam and memory foam are commonly used in mattresses, sofas, office chairs, and seating systems due to their comfort, flexibility, and durability.

Consumers are increasingly seeking ergonomic furniture and high-comfort mattresses, which has encouraged manufacturers to develop advanced foam cushioning technologies. Growth in residential construction and home renovation activities also supports demand for foam-based cushioning materials used in furniture manufacturing.

Market Restraint

Environmental Concerns Related to Conventional Foam Materials

One of the primary challenges affecting the foam cushioning market is the environmental impact associated with petroleum-based foam materials. Traditional foams such as expanded polystyrene are difficult to recycle and may contribute to long-term environmental waste accumulation.

Several countries have introduced regulations limiting the use of certain plastic-based packaging materials. This has compelled manufacturers to reconsider product design and develop recyclable or biodegradable alternatives. Transitioning to sustainable foam solutions often requires additional research investment and changes in manufacturing infrastructure, which can increase operational costs.

Market Opportunities

Development of Bio-Based Foam Materials

The introduction of bio-based polyurethane and plant-derived cushioning foams presents a promising opportunity for industry participants. These materials use renewable raw materials such as soybean oil or plant-based polymers, reducing reliance on petroleum-based chemicals.

Companies investing in bio-based foam technologies may benefit from increasing demand for environmentally responsible packaging and furniture materials. This innovation also aligns with sustainability initiatives adopted by global consumer goods manufacturers.

Expansion of Automotive Interior Applications

Automotive manufacturers are continuously focusing on enhancing passenger comfort and acoustic insulation within vehicles. Foam cushioning materials are widely used in seating systems, headrests, armrests, and interior trim components.

The transition toward electric vehicles has further increased the need for lightweight interior materials that improve energy efficiency while maintaining passenger comfort. Foam cushioning solutions designed for vehicle interiors are expected to gain wider adoption as automotive manufacturers seek improved cabin ergonomics and noise reduction.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.8 Billion |

| Market Size in 2026 | USD 13.6 Billion |

| Market Size in 2031 | USD 18.6 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Polyurethane foam represented the largest material segment with approximately 41.2% share in 2024. This material is widely used due to its flexibility, durability, and excellent shock absorption properties. Polyurethane foam is commonly applied in furniture cushioning, bedding products, automotive seating, and packaging inserts.

Polyethylene foam is expected to be the fastest-growing material segment with a projected CAGR of 6.9% during the forecast period. This growth will be supported by its lightweight structure and strong protective characteristics, which make it suitable for packaging fragile electronics and industrial components. Its moisture resistance and recyclability will also encourage wider adoption across logistics and protective packaging applications.

By Type

Flexible foam dominated the type segment with a market share of 57.4% in 2024. Flexible foam materials are commonly used in mattresses, furniture cushions, and protective packaging due to their softness and adaptability. Their ability to absorb shocks and provide comfort has supported strong demand across multiple industries.

Rigid foam is anticipated to become the fastest-growing type segment with a CAGR of 6.6% during the forecast period. This growth will be influenced by increasing demand for rigid foam in structural packaging and protective product containers. Rigid foams provide higher strength and dimensional stability, which makes them suitable for heavy or fragile industrial products.

By Application

Packaging applications accounted for 45.8% of the foam cushioning market in 2024, making it the dominant application segment. Foam cushioning materials are widely used in protective packaging for electronics, appliances, and delicate consumer goods. Their shock-absorbing properties help prevent product damage during storage and transportation.

The automotive interiors segment will grow at the fastest CAGR of 7.1% during the forecast period. Foam cushioning materials will continue to be used in vehicle seating systems, door panels, and headrests. Automotive manufacturers are focusing on improving passenger comfort and reducing cabin noise, which will increase demand for specialized foam cushioning products.

By End-Use Industry

The consumer goods sector held the largest share of 39.6% in 2024 within the foam cushioning market. This dominance was driven by extensive use of cushioning materials in packaging consumer electronics, appliances, and household products.

The automotive industry will register the fastest growth with a CAGR of 7.0% during the forecast period. Increased production of electric vehicles and advancements in interior cabin design will create demand for lightweight foam cushioning materials that enhance passenger comfort and energy efficiency.

Foam Cushioning Market Segmentations

y Material

- Polyurethane Foam

- Polyethylene Foam

- Expanded Polystyrene

- Polypropylene Foam

- Others

By Type

- Flexible Foam

- Rigid Foam

By Application

- Packaging

- Furniture & Bedding

- Automotive Interiors

- Electronics Protection

- Industrial Applications

By End-Use Industry

- Consumer Goods

- Automotive

- Electronics

- Furniture Manufacturing

- Industrial Equipment

Regional Analysis

North America

North America accounted for 24.8% of the foam cushioning market share in 2025. The region’s market growth was supported by well-established packaging industries and strong demand from furniture and bedding manufacturers. During the forecast period, the regional market will grow at a CAGR of approximately 5.9% between 2025 and 2033 as companies continue to adopt advanced cushioning materials in logistics and consumer goods packaging.

The United States represented the dominant country market in North America. Growth in the U.S. foam cushioning market was influenced by the presence of large-scale e-commerce retailers and fulfillment centers that require efficient protective packaging solutions. In addition, the country’s furniture manufacturing sector continued to integrate advanced polyurethane foam technologies in mattresses and seating products, supporting long-term market expansion.

Europe

Europe held 21.5% of the foam cushioning market in 2025. The regional market was characterized by strong regulatory frameworks promoting sustainable packaging materials and recycling initiatives. Looking ahead, the European foam cushioning market will expand at a CAGR of 5.7% between 2025 and 2033 as manufacturers increasingly focus on recyclable cushioning products.

Germany emerged as the dominant country market in the region. The country’s growth was supported by its well-developed automotive manufacturing industry. Foam cushioning materials are widely used in automotive seating systems and interior components, providing comfort and structural support. Continuous advancements in vehicle interior design are expected to sustain demand for specialized foam cushioning products.

Asia Pacific

Asia Pacific represented the largest regional market with a 38.6% share in 2025. The region’s dominance was supported by expanding manufacturing industries, rising consumer goods production, and strong demand for packaging materials across logistics and electronics sectors. Over the forecast period, the Asia Pacific foam cushioning market will grow at a CAGR of 6.8% between 2025 and 2033.

China remained the largest national market in the region. The country’s extensive electronics manufacturing ecosystem created consistent demand for protective foam packaging materials used in the transportation of fragile devices. In addition, China’s furniture and bedding manufacturing sectors have continued to scale production, contributing to the growing consumption of polyurethane and polyethylene foam cushioning materials.

Middle East & Africa

The Middle East & Africa accounted for 7.2% of the foam cushioning market in 2025. Demand in the region was influenced by increasing industrialization and growth in packaging requirements for consumer goods and electronics imports. The regional market will grow at a CAGR of 6.2% during the forecast period through 2033.

Saudi Arabia represented the leading country within the region. Growth was supported by infrastructure development and rising demand for furniture and home furnishing products across residential and commercial sectors. Foam cushioning materials are increasingly used in furniture manufacturing to enhance product comfort and durability.

Latin America

Latin America captured 7.9% of the foam cushioning market share in 2025. The region has witnessed steady expansion in packaging demand driven by retail and consumer goods distribution networks. The Latin American foam cushioning market will expand at a CAGR of 7.3% between 2025 and 2033, making it one of the faster-growing regional markets.

Brazil dominated the regional market. Growth in the country was supported by increasing production of consumer electronics and appliances that require protective packaging materials during distribution. Additionally, Brazil’s furniture manufacturing industry continues to incorporate foam cushioning materials to enhance product quality and consumer comfort.

Competitive Landscape

The foam cushioning market is moderately fragmented, with global and regional manufacturers competing through product innovation, sustainability initiatives, and expansion of manufacturing capabilities. Companies are investing in advanced foam technologies to improve cushioning performance while reducing environmental impact.

BASF SE is considered one of the leading companies in the foam cushioning market due to its broad portfolio of polyurethane and specialty foam materials used across automotive, furniture, and packaging applications. The company has recently focused on developing recyclable foam technologies designed for sustainable packaging.

Other major players continue to expand production capacity and introduce new materials tailored for electronics packaging and automotive interiors. Strategic partnerships with packaging manufacturers and logistics companies are also becoming common to strengthen market presence

Key Players in the Foam Cushioning Market

- BASF SE

- Dow Inc.

- Huntsman Corporation

- Sealed Air Corporation

- Recticel NV

- Zotefoams plc

- Armacell International S.A.

- JSP Corporation

- Rogers Corporation

- Foamcraft Inc.

- UFP Technologies Inc.

- Woodbridge Foam Corporation

- FXI Holdings Inc.

- Pregis LLC

- Sekisui Chemical Co., Ltd.