FMCG Packaging Market Report Size and Growth

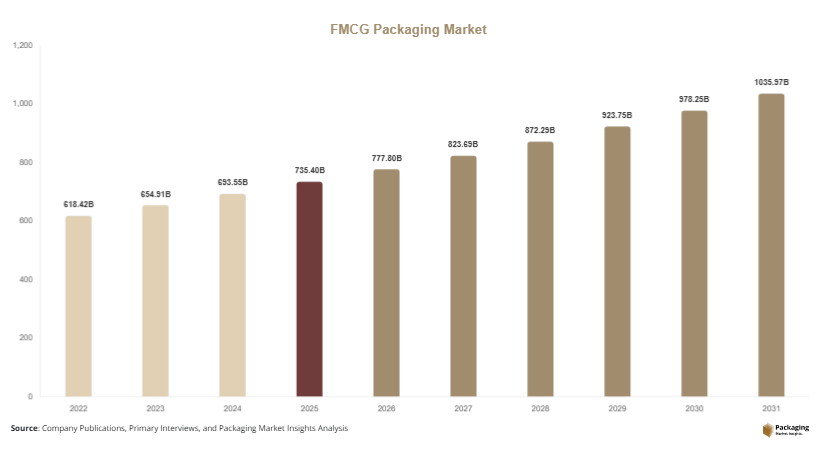

The FMCG Packaging Market was valued at approximately USD 735.4 billion in 2025 and is projected to reach USD 1,042.6 billion by 2030, expanding at a CAGR of 5.9% during 2025–2031. The market is witnessing steady expansion due to the growing consumption of fast-moving consumer goods across urban and rural economies. Rising demand for packaged food, beverages, personal care products, and household goods continues to drive packaging innovations across materials and formats.

A key global factor supporting the growth of the FMCG Packaging Market is the rapid expansion of organized retail and e-commerce channels. As consumers increasingly purchase daily-use goods through supermarkets and online platforms, packaging has become essential for product protection, shelf appeal, transportation efficiency, and brand differentiation. Companies are also investing in lightweight, recyclable, and flexible packaging to meet regulatory requirements and consumer sustainability expectations.

Technological advancements in packaging materials and printing technologies are further improving the functionality of FMCG packaging solutions. Smart packaging, improved barrier properties, and sustainable materials are enabling manufacturers to enhance product shelf life and logistics efficiency.

Key Highlights

- Asia Pacific dominated the FMCG Packaging Market with 38.6% share in 2025, while Latin America is expected to grow at the fastest CAGR of 6.7% during the forecast period.

- Plastic packaging led the material segment with 42.3% share, whereas biodegradable materials are projected to expand at a CAGR of 7.4%.

- Flexible packaging dominated the type segment with 47.8% share, while paper-based flexible formats are projected to grow at 6.9% CAGR.

- China represented the dominant country market, valued at USD 146.2 billion in 2025 and estimated to reach USD 154.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Sustainable and Recyclable Packaging Materials

Sustainability has become a major trend shaping the FMCG Packaging Market. Governments and environmental organizations are encouraging manufacturers to adopt recyclable, compostable, and reusable packaging materials. FMCG companies are redesigning packaging structures to reduce plastic content and improve recyclability.

Paper-based packaging, biodegradable polymers, and recycled plastics are gaining traction across food and personal care product categories. Many global FMCG brands are also committing to circular packaging strategies that include reusable containers and post-consumer recycled materials. These initiatives aim to reduce environmental impact while maintaining product safety and packaging performance.

Growth of Flexible Packaging Formats

Flexible packaging has emerged as one of the fastest evolving formats within the FMCG Packaging Market. Pouches, sachets, and flexible films provide lightweight, cost-effective, and space-efficient packaging solutions. These formats also support convenient features such as resealable closures and easy dispensing.

The rise of single-use consumer goods, particularly in emerging markets, is increasing demand for sachets and small packaging formats. Flexible packaging also reduces transportation costs and material consumption compared to rigid packaging solutions. As FMCG manufacturers seek efficiency and sustainability simultaneously, flexible packaging formats are becoming widely adopted across multiple product categories.

Market Drivers

Rising Demand for Packaged Food and Personal Care Products

The growing consumption of packaged food and personal care products is a key factor driving the FMCG Packaging Market. Urban lifestyles and changing dietary habits have increased reliance on ready-to-eat and convenience foods. This trend requires reliable packaging solutions that preserve freshness and ensure product safety.

Additionally, rising disposable incomes and increasing consumer awareness of hygiene are driving demand for packaged personal care items such as shampoos, soaps, and skincare products. Packaging plays a crucial role in maintaining product integrity, improving brand recognition, and ensuring safe distribution.

Expansion of Retail and E-Commerce Distribution Channels

The rapid expansion of modern retail infrastructure and online shopping platforms is accelerating the growth of the FMCG Packaging Market. Supermarkets, hypermarkets, and convenience stores require standardized packaging formats that support efficient shelf display and inventory management.

At the same time, e-commerce platforms demand durable and protective packaging to ensure safe product delivery. Packaging solutions designed for logistics efficiency, such as tamper-evident seals and protective secondary packaging, are gaining importance. These requirements are encouraging FMCG brands to invest in packaging innovations that support both retail and online distribution channels.

Market Restraint

Environmental Concerns Related to Plastic Waste

Environmental concerns associated with plastic packaging waste remain a major restraint affecting the FMCG Packaging Market. Plastic materials have long been widely used due to their durability, flexibility, and cost-effectiveness. However, improper disposal and limited recycling infrastructure have contributed to growing environmental challenges.

Governments across several regions are introducing regulations aimed at reducing single-use plastics and encouraging sustainable packaging alternatives. These policies are compelling FMCG companies to redesign packaging materials and invest in eco-friendly solutions, which may increase production costs in the short term.

Additionally, transitioning to biodegradable or recyclable materials can involve technological challenges, including maintaining barrier properties and product shelf life. Manufacturers must balance sustainability goals with packaging functionality, which can slow adoption in certain product categories.

Despite these constraints, companies continue to invest in research and development to develop environmentally responsible packaging materials. Over time, technological innovation and improved recycling infrastructure are expected to reduce the impact of this restraint on market expansion.

Market Opportunities

Growth of Smart and Interactive Packaging

Smart packaging technologies represent an emerging opportunity in the FMCG Packaging Market. Technologies such as QR codes, RFID tags, and temperature-sensitive indicators enable brands to provide additional product information and traceability.

These solutions allow consumers to access digital content related to product origin, usage instructions, and promotional campaigns. Smart packaging also helps manufacturers track product movement across supply chains and monitor storage conditions, improving quality assurance and reducing product loss.

Increasing Demand for Premium Packaging in Personal Care

Premium packaging solutions are gaining popularity in the personal care segment of the FMCG Packaging Market. Consumers increasingly associate high-quality packaging with product value and brand reliability. As a result, manufacturers are introducing innovative packaging designs featuring improved aesthetics, durability, and convenience.

Glass containers, high-quality plastic bottles, and decorative cartons are being used to enhance the visual appeal of skincare, cosmetics, and grooming products. Premium packaging also supports brand differentiation in competitive retail environments. With rising consumer spending on personal care products, this opportunity is expected to support continued innovation in packaging formats and materials.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 735.4 Billion |

| Market Size in 2026 | USD 777.8 Billion |

| Market Size in 2031 | USD 1,104.8 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Packaging Type

Flexible packaging dominated the FMCG Packaging Market in 2024, accounting for 47.8% of the total market share. Flexible packaging formats such as pouches, sachets, and films were widely used due to their lightweight structure and cost efficiency. These packaging solutions were commonly used for food products, snacks, and personal care items. The ability of flexible packaging to reduce material consumption and transportation costs supported its strong market adoption.

Rigid packaging represented the fastest-growing subsegment and will grow at a CAGR of 6.2% during the forecast period. Bottles, jars, and containers provide strong product protection and improved shelf stability. Rigid packaging formats will increasingly support premium packaging applications in the personal care and beverage industries. The growth of high-value FMCG products will drive demand for rigid packaging solutions with enhanced durability and aesthetic appeal.

By Material

Plastic materials dominated the FMCG Packaging Market in 2024 with a 42.3% market share. Plastic packaging solutions were widely used due to their durability, lightweight properties, and cost-effectiveness. Materials such as polyethylene, polypropylene, and PET supported the packaging of beverages, snacks, and household goods. Plastic packaging also enabled flexible packaging formats, which further strengthened its market presence.

Biodegradable materials will represent the fastest-growing material segment, projected to grow at a CAGR of 7.4%. Increasing environmental awareness and regulatory pressure will encourage FMCG manufacturers to adopt sustainable packaging materials. Biodegradable polymers and compostable materials will support eco-friendly packaging strategies across several FMCG product categories.

By Application

Food packaging dominated the FMCG Packaging Market in 2024 with 44.6% share. The packaging of packaged foods, snacks, dairy products, and ready-to-eat meals generated significant demand for both flexible and rigid packaging solutions. The large global consumption of food products supported the dominance of this segment.

Personal care packaging will grow at the fastest rate with a CAGR of 6.5% during the forecast period. The expanding skincare, cosmetics, and hygiene product industries will drive demand for innovative packaging solutions. Packaging designs featuring improved aesthetics and convenience features will play an important role in supporting growth in this segment.

By Distribution Channel

Retail distribution channels dominated the FMCG Packaging Market in 2024, accounting for 63.2% share. Supermarkets, hypermarkets, and convenience stores required packaging solutions that supported shelf display and product visibility. Standardized packaging formats enabled efficient product handling and storage across large retail networks.

E-commerce distribution will represent the fastest-growing subsegment and will grow at a CAGR of 7.1% during the forecast period. Online retail platforms will require durable packaging solutions that ensure safe transportation and product protection. Secondary packaging formats designed for logistics efficiency will gain importance as online sales of FMCG products continue to expand.

FMCG Packaging Market Segmentations

By Packaging Type

- Flexible Packaging

- Rigid Packaging

By Material

- Plastic

- Paper & Paperboard

- Glass

- Metal

- Biodegradable Materials

By Application

- Food

- Beverages

- Personal Care

- Household Products

By Distribution Channel

- Retail Stores

- E-Commerce Platforms

Regional Analysis

North America

North America accounted for 23.4% of the FMCG Packaging Market share in 2025. The region benefited from a mature consumer goods industry and strong demand for packaged food and personal care products. During the forecast period, the market will expand at a CAGR of 5.2% between 2025 and 2033. Technological advancements in packaging materials and the widespread presence of organized retail chains contributed to the region’s steady market performance.

The United States dominated the North American FMCG Packaging Market due to the country’s extensive FMCG manufacturing ecosystem. Large consumer goods companies operating in the U.S. continue to adopt packaging automation and advanced printing technologies to enhance packaging efficiency and product branding. Additionally, strong demand for packaged snacks, beverages, and household goods supported packaging consumption across multiple product categories.

Europe

Europe held 21.7% share of the FMCG Packaging Market in 2025. The region’s packaging industry has long been characterized by strong regulatory frameworks and advanced recycling systems. Over the forecast period, the market will grow at a CAGR of 5.1% between 2025 and 2033. European countries are increasingly promoting sustainable packaging materials and circular economy initiatives.

Germany represented the leading country in the European FMCG Packaging Market. The country’s well-established manufacturing sector and advanced packaging technologies have supported its market leadership. German packaging companies are investing in high-performance materials and efficient production systems that support large-scale FMCG production. Additionally, the presence of leading packaging equipment manufacturers has strengthened the country’s position within the regional packaging ecosystem.

Asia Pacific

Asia Pacific represented the largest share of the FMCG Packaging Market at 38.6% in 2025. Rapid urbanization, expanding middle-class populations, and rising consumption of packaged goods supported the region’s market dominance. The market will grow at a CAGR of 6.3% between 2025 and 2033, driven by strong demand across emerging economies.

China dominated the Asia Pacific FMCG Packaging Market due to its large consumer base and well-developed manufacturing infrastructure. The country’s extensive FMCG production capabilities and export-oriented packaging industry contributed to significant market demand. Increasing consumption of packaged food, beverages, and household goods supported steady growth in packaging production across the country.

Middle East & Africa

The Middle East & Africa accounted for 8.1% of the FMCG Packaging Market share in 2025. Growth in this region was supported by expanding retail infrastructure and increasing demand for packaged food products. The market will grow at a CAGR of 5.6% during 2025–2033 as urban populations continue to expand.

Saudi Arabia emerged as the dominant country in the regional market. The country’s rapidly developing retail sector and growing population have increased demand for packaged consumer goods. Government initiatives aimed at expanding domestic manufacturing capabilities are also encouraging investment in packaging production facilities.

Latin America

Latin America represented 8.2% of the FMCG Packaging Market in 2025. The region’s market was supported by rising consumption of packaged foods and beverages. Over the forecast period, the market will grow at the fastest CAGR of 6.7% between 2025 and 2033.

Brazil dominated the Latin American FMCG Packaging Market due to its large consumer goods industry and growing retail sector. The country’s food and beverage sector plays a significant role in driving packaging demand. Increasing urbanization and expanding supermarket chains have further strengthened the market for FMCG packaging solutions.

Competitive Landscape

The FMCG Packaging Market is characterized by the presence of several global packaging manufacturers and regional suppliers. Companies are focusing on expanding production capacity, introducing sustainable packaging materials, and investing in advanced packaging technologies.

Amcor plc represents one of the leading players in the FMCG packaging industry. The company continues to expand its sustainable packaging portfolio and invest in recyclable material technologies. Its global manufacturing network and partnerships with major FMCG brands support its market leadership.

Other companies operating in the market include Berry Global Group, Sealed Air Corporation, Mondi Group, and Sonoco Products Company. These companies are focusing on innovative packaging designs and material optimization strategies to meet evolving industry requirements.

Key Players in the FMCG Packaging Market

- Amcor plc

- Berry Global Group

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Smurfit Kappa Group

- DS Smith plc

- Ball Corporation

- Crown Holdings Inc.

- Huhtamaki Oyj

- Tetra Pak International

- WestRock Company

- Graphic Packaging International

- Constantia Flexibles

- AptarGroup Inc.