Flexible Polyurethane Foam Market Size and Growth

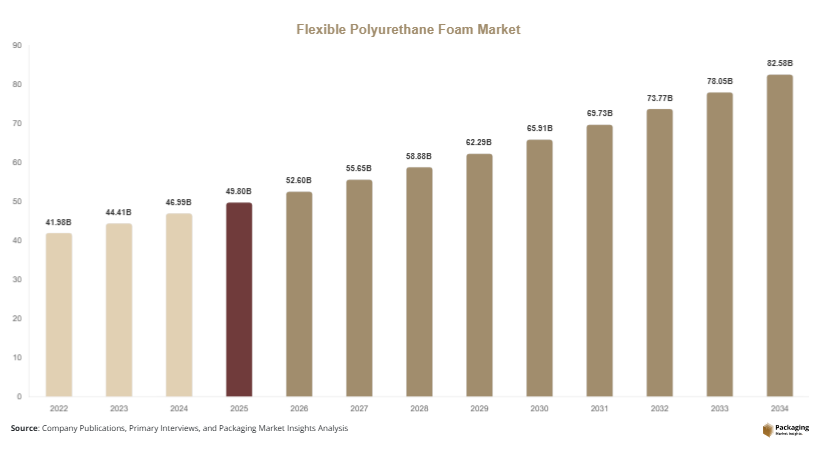

The global flexible polyurethane foam market size was valued at approximately USD 49.8 billion in 2025 and is projected to reach nearly USD 52.6 billion in 2026. By 2034, the market is forecasted to reach around USD 82.9 billion, expanding at a CAGR of 5.8% during 2025–2034. The growing automotive sector, increasing demand for lightweight materials, and expansion of the residential furniture industry continue to support long-term market growth. Flexible polyurethane foam is increasingly utilized in vehicle seating systems, mattresses, carpet underlays, sound insulation products, and protective packaging applications.

One of the primary growth factors is the rapid expansion of the furniture and bedding industries. Consumers are increasingly demanding premium mattresses and upholstered furniture products with enhanced comfort and durability. Another major factor is the growing automotive production sector, where lightweight polyurethane foam helps improve fuel efficiency and passenger comfort. Additionally, rising demand for thermal insulation materials in residential and commercial buildings is contributing to increased market adoption globally.

Key Highlights:

- Asia Pacific dominated the market with a 41.3% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Conventional flexible foam led the type segment with a 46.1% share.

- Petroleum-based polyols dominated the material segment with a 58.4% share

- Furniture and bedding applications led the end-use segment with 44.8% share.

- The US remained the dominant country with a market size of USD 9.7 billion in 2025 and USD 10.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Bio-Based and Low-Emission Foam Technologies

Sustainability is becoming a major trend influencing the flexible polyurethane foam market. Manufacturers are increasingly developing foam products using bio-based polyols derived from soy, castor oil, and other renewable materials. Low-emission and low-VOC polyurethane foams are gaining popularity across furniture and automotive industries due to growing environmental regulations and consumer awareness regarding indoor air quality. For example, mattress manufacturers are introducing eco-friendly foam products certified for reduced chemical emissions and improved recyclability. Automotive companies are also incorporating sustainable foam materials into seating systems to reduce vehicle carbon footprints. Future market expansion is expected to benefit from increasing investments in green chemistry and circular economy initiatives across global manufacturing industries.

Increasing Integration of Smart Manufacturing and Automation

The industry is witnessing growing integration of automation and smart manufacturing technologies in foam production operations. Companies are increasingly adopting computerized foam cutting systems, automated chemical mixing technologies, and AI-based quality control solutions to improve production efficiency and reduce material waste. For instance, large foam manufacturers are implementing robotic handling systems and digital monitoring technologies to optimize foam density consistency and processing speed. Smart manufacturing is also enabling customized foam production for automotive and bedding applications with improved precision and reduced operational costs. Future developments are expected to include real-time process monitoring and predictive maintenance systems capable of enhancing manufacturing efficiency and reducing downtime across production facilities.

Market Drivers

Expansion of Furniture and Bedding Industries

The rapid expansion of the furniture and bedding industries is one of the key drivers supporting growth of the flexible polyurethane foam market. Consumers are increasingly purchasing mattresses, sofas, recliners, and upholstered furniture products designed for enhanced comfort and durability. Flexible polyurethane foam provides cushioning performance, resilience, and lightweight properties that make it highly suitable for residential and commercial furniture applications. For example, premium mattress manufacturers are increasingly using memory foam and high-resilience polyurethane foam layers to improve sleep comfort and product lifespan. Rising urbanization and growth in residential construction activities are also increasing furniture demand globally. As disposable incomes continue rising in emerging economies, demand for high-quality furniture products is expected to support long-term market expansion.

Growing Demand for Lightweight Automotive Materials

The increasing use of lightweight materials in automotive manufacturing is another major factor driving the flexible polyurethane foam market. Automotive companies are focusing on reducing vehicle weight to improve fuel efficiency and comply with emission regulations. Flexible polyurethane foam is widely used in vehicle seats, door panels, headliners, and acoustic insulation systems due to its lightweight structure and sound absorption capability. For example, electric vehicle manufacturers are integrating advanced foam materials into interior components to improve passenger comfort while maximizing energy efficiency. Growth in electric vehicle production and rising global automobile sales are expected to further strengthen demand for flexible polyurethane foam products across the automotive industry.

Market Restraint

One of the major restraints affecting the flexible polyurethane foam market is the volatility in raw material prices and increasing environmental concerns associated with petrochemical-based foam production. Polyurethane foam manufacturing depends heavily on petroleum-derived chemicals such as polyols and isocyanates, which are subject to frequent price fluctuations due to changing crude oil prices and supply chain disruptions. Rising environmental regulations regarding chemical emissions and foam disposal are also creating operational challenges for manufacturers. For example, several countries are implementing stricter VOC emission standards and waste management regulations for polyurethane products. Smaller manufacturers may face difficulties investing in sustainable production technologies and regulatory compliance systems. These challenges could increase operational costs and limit market growth in certain regions during the forecast period.

Market Opportunities

Expansion of Bio-Based Polyurethane Foam Applications

The growing focus on sustainable manufacturing presents significant opportunities for bio-based flexible polyurethane foam products. Manufacturers are increasingly developing foam materials derived from renewable resources to reduce environmental impact and meet sustainability targets. Bio-based polyurethane foams are gaining popularity in furniture, automotive, and bedding applications due to lower emissions and improved environmental performance. For example, several furniture manufacturers are introducing mattresses and cushions made with partially plant-based foam formulations. Future growth opportunities are expected to emerge from increasing consumer demand for eco-friendly products and advancements in renewable chemical processing technologies. Expanding government support for green manufacturing initiatives is also likely to support market development.

Rising Demand for Advanced Acoustic and Insulation Solutions

The increasing need for acoustic insulation and thermal comfort solutions is creating new growth opportunities for the flexible polyurethane foam market. Flexible foam materials are widely used in automotive cabins, residential buildings, and industrial facilities to reduce noise levels and improve energy efficiency. For instance, construction companies are increasingly utilizing polyurethane foam insulation systems in commercial buildings to reduce heating and cooling energy consumption. Automotive manufacturers are also integrating advanced sound-absorbing foam materials into vehicle interiors to improve passenger comfort. Future market expansion is expected to benefit from growing infrastructure development, rising construction activities, and increasing adoption of energy-efficient building materials worldwide.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 49.8 Billion |

| Market Size in 2026 | USD 52.6 Billion |

| Market Size in 2034 | USD 82.9 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

Type Segment

Conventional flexible foam dominated the type segment with approximately 46.1% market share in 2024. This foam type is widely used across furniture, bedding, and packaging industries because of its affordability, cushioning performance, and versatility. Conventional polyurethane foam is commonly utilized in sofas, mattresses, carpet underlays, and protective packaging products due to its lightweight structure and cost efficiency. For example, residential furniture manufacturers continue to rely heavily on conventional foam materials for mass-market seating and mattress production. The segment’s dominance is also supported by widespread availability and compatibility with automated foam fabrication technologies. Rising urban housing demand and increasing furniture production across developing economies continue to strengthen consumption of conventional flexible polyurethane foam globally.

High-resilience foam is expected to witness the fastest CAGR of 6.7% during 2025–2034. Growth is being driven by rising demand for premium comfort products and advanced automotive seating systems. High-resilience polyurethane foam provides superior elasticity, durability, and pressure distribution compared to traditional foam products. For instance, premium mattress brands are increasingly using high-resilience foam layers to improve sleep quality and product longevity. Automotive manufacturers are also integrating these materials into vehicle seating applications for enhanced passenger comfort and vibration absorption. Future growth is expected to be supported by increasing consumer preference for luxury bedding products and rising adoption of ergonomic seating solutions across residential and commercial sectors.

Material Segment

Petroleum-based polyols dominated the material segment with approximately 58.4% share in 2024. These materials remain widely utilized because of their strong chemical performance, large-scale availability, and cost-effective manufacturing characteristics. Petroleum-based polyols are commonly used in furniture cushioning, automotive seating, insulation products, and industrial packaging applications. For example, large-scale foam manufacturers rely on petrochemical feedstocks for high-volume production of mattresses and upholstery foam materials. Their compatibility with existing manufacturing infrastructure and established supply chains continues to support market dominance. Additionally, petroleum-based polyols offer durability and flexibility characteristics that remain highly suitable for diverse industrial and consumer applications.

Bio-based polyols are projected to register the fastest CAGR of 7.1% during the forecast period. Growth is primarily driven by rising environmental concerns and increasing demand for sustainable foam production technologies. Manufacturers are increasingly developing bio-based polyurethane materials using renewable resources such as soybean oil and castor oil to reduce carbon emissions and dependence on fossil fuels. For instance, furniture companies are launching eco-friendly mattresses and seating systems containing partially renewable foam formulations. Future market expansion is expected to benefit from stricter sustainability regulations and growing consumer interest in environmentally responsible products. Advancements in renewable chemical processing technologies are also likely to improve commercial adoption across multiple industries.

End-Use Segment

Furniture and bedding applications dominated the end-use segment with approximately 44.8% market share in 2024. Flexible polyurethane foam is widely utilized in mattresses, sofas, cushions, recliners, and upholstered seating systems because of its comfort, resilience, and lightweight properties. Rising urbanization and increasing consumer spending on home furnishing products are driving substantial demand across residential and commercial sectors. For example, mattress manufacturers are increasingly producing memory foam and multi-layer polyurethane bedding products designed for pressure relief and ergonomic support. The dominance of this segment is also supported by rapid expansion of online furniture retail channels and growing hospitality infrastructure development globally.

Automotive applications are expected to witness the fastest CAGR of 6.5% through 2034. Growth is being driven by increasing vehicle production and rising adoption of lightweight interior materials. Flexible polyurethane foam is widely used in automotive seating, headrests, armrests, and sound insulation systems due to its cushioning performance and acoustic absorption capabilities. For example, electric vehicle manufacturers are increasingly integrating advanced foam materials into cabin interiors to improve passenger comfort while reducing overall vehicle weight. Future market growth is expected to benefit from rising electric vehicle production, stricter fuel efficiency regulations, and increasing investment in advanced automotive interior technologies worldwide.

Flexible Polyurethane Foam Market Segmentations

By Type

- Conventional Flexible Foam

- High-Resilience Foam

- Memory Foam

- Rebond Foam

- Specialty Flexible Foam

By Material

- Petroleum-Based Polyols

- Bio-Based Polyols

- Toluene Diisocyanate (TDI)

- Methylene Diphenyl Diisocyanate (MDI)

- Additives and Catalysts

By End-User

- Furniture & Bedding

- Automotive

- Packaging

- Construction

- Electronics & Appliances

Regional Analysis

North America

North America accounted for approximately 24.8% share of the flexible polyurethane foam market in 2025 and is projected to expand at a CAGR of 5.3% during 2025–2034. The region benefits from strong demand across furniture manufacturing, automotive production, and residential renovation activities. Rising consumer spending on premium bedding and upholstered furniture products continues to support market growth. The region also has a highly developed automotive sector that increasingly utilizes lightweight foam materials for seating and acoustic insulation applications. Growing investment in sustainable polyurethane technologies and low-emission manufacturing systems is further contributing to regional market expansion.

The United States dominates the North American market due to its large furniture industry and advanced automotive manufacturing base. A major growth driver is the increasing demand for premium mattresses and ergonomic furniture products among residential consumers. For example, bedding manufacturers are expanding production of memory foam mattresses with enhanced comfort and cooling technologies. Canada is also witnessing growing demand for polyurethane insulation materials in energy-efficient residential construction projects. Future regional growth is expected to benefit from increasing adoption of recyclable foam technologies and expansion of electric vehicle manufacturing facilities.

Europe

Europe represented approximately 22.6% market share in 2025 and is expected to grow at a CAGR of 5.5% during the forecast period. The region is characterized by strong automotive manufacturing activity, strict environmental regulations, and rising adoption of sustainable foam materials. Demand for flexible polyurethane foam is increasing across furniture, automotive, and construction industries due to rising interest in lightweight and recyclable materials. Manufacturers are increasingly investing in low-VOC foam technologies and renewable polyol production systems to comply with regional sustainability requirements. The growing use of acoustic insulation materials in residential and commercial construction is also supporting market growth.

Germany dominates the European market because of its advanced automotive industry and strong industrial manufacturing infrastructure. A unique growth driver is the increasing use of lightweight polyurethane components in electric vehicle interiors and seating systems. For example, German automobile manufacturers are integrating advanced foam materials to improve cabin comfort while reducing overall vehicle weight. France and Italy are also contributing significantly to regional demand due to expansion of furniture exports and premium mattress production. Future market growth is expected to be supported by circular economy initiatives and increasing investment in sustainable chemical manufacturing.

Asia Pacific

Asia Pacific dominated the flexible polyurethane foam market with approximately 41.3% share in 2025 and is projected to register the fastest CAGR of 6.3% during 2025–2034. Rapid urbanization, expanding middle-class populations, and growing industrialization are major factors driving regional market growth. The region has become a global manufacturing hub for furniture, mattresses, automotive components, and consumer goods utilizing polyurethane foam materials. Rising housing construction activities and increasing consumer spending on home furnishing products are also contributing significantly to demand. Expansion of packaging and electronics industries is further strengthening regional market opportunities.

China remains the dominant country in Asia Pacific due to its extensive furniture manufacturing industry and large-scale industrial production capacity. A major growth driver is the rapid growth of domestic residential housing and commercial construction activities. For example, Chinese furniture manufacturers are increasingly investing in automated foam production technologies to meet rising export demand. India is emerging as another important market because of increasing urbanization and growing automotive production. Japan continues to play a key role in advanced foam material innovation and automotive interior manufacturing. Future regional growth is expected to benefit from rising disposable income and industrial expansion.

Middle East & Africa

The Middle East & Africa region accounted for approximately 5.1% market share in 2025 and is expected to grow at a CAGR of 5.9% during the forecast period. Growth is being supported by expanding construction activities, rising furniture imports, and increasing demand for insulation materials in commercial infrastructure projects. Flexible polyurethane foam is increasingly used in mattresses, seating products, and thermal insulation systems across residential and hospitality sectors. Countries within the Gulf region are investing heavily in real estate development and hotel infrastructure, creating additional demand for cushioning and insulation materials.

Saudi Arabia dominates the regional market due to rising investments in residential housing and commercial development projects. A unique growth driver is the expansion of hospitality and tourism infrastructure requiring high volumes of furniture, mattresses, and interior cushioning products. For example, hotel development projects in Riyadh and Jeddah are increasing demand for premium polyurethane foam bedding systems. South Africa is also witnessing growth due to rising consumer demand for household furniture products and automotive seating applications. Future regional growth is expected to be supported by industrial diversification initiatives and increasing infrastructure investment.

Latin America

Latin America held approximately 6.2% market share in 2025 and is projected to expand at a CAGR of 6.4% during 2025–2034. The region is benefiting from rising residential construction activities, increasing automotive production, and growing furniture manufacturing operations. Flexible polyurethane foam demand is increasing across bedding, upholstered furniture, and packaging industries due to improving consumer purchasing power and retail expansion. Regional manufacturers are increasingly adopting modern foam processing technologies to improve product quality and production efficiency. The growing use of insulation materials in commercial construction projects is also supporting market growth.

Brazil dominates the Latin American market due to its large furniture manufacturing industry and expanding automotive sector. A key growth driver is the increasing domestic demand for mattresses and home furnishing products among middle-income consumers. For example, Brazilian furniture manufacturers are expanding production of premium upholstered seating systems utilizing high-resilience polyurethane foam. Mexico is also emerging as an important market because of growth in automotive component manufacturing and export-oriented production activities. Future regional growth is expected to be supported by urban development and increasing industrial investments across the region.

Competitive Landscape

The flexible polyurethane foam market is highly competitive, with manufacturers focusing on sustainable raw materials, advanced foam technologies, and production efficiency improvements to strengthen market position. Companies are increasingly investing in bio-based polyurethane formulations, low-emission manufacturing systems, and customized foam solutions for furniture and automotive applications.

BASF SE remains one of the leading companies due to its extensive polyurethane product portfolio and strong global manufacturing network. The company continues expanding sustainable foam technologies and renewable polyol development initiatives. Covestro AG is focusing on circular economy strategies and recyclable polyurethane solutions designed for automotive and furniture industries. Huntsman Corporation is strengthening its market presence through advanced comfort foam technologies and strategic partnerships with bedding manufacturers.

Other major companies are emphasizing regional expansion, capacity enhancement, and innovation in lightweight foam applications. Increasing investment in electric vehicle interior materials and eco-friendly furniture products is expected to shape future competition across the industry. Smart manufacturing and automation technologies are also becoming important strategic priorities for large-scale foam producers.

Key Players List

- BASF SE

- Covestro AG

- Huntsman Corporation

- Dow Inc.

- Recticel NV/SA

- Carpenter Co.

- Foamcraft Inc.

- Rogers Corporation

- Future Foam Inc.

- INOAC Corporation

- Mitsui Chemicals Inc.

- Sekisui Chemical Co., Ltd.

- UFP Technologies Inc.

- Vita Group

- Woodbridge Foam Corporation