Flexible Packaging Market Size and Growth

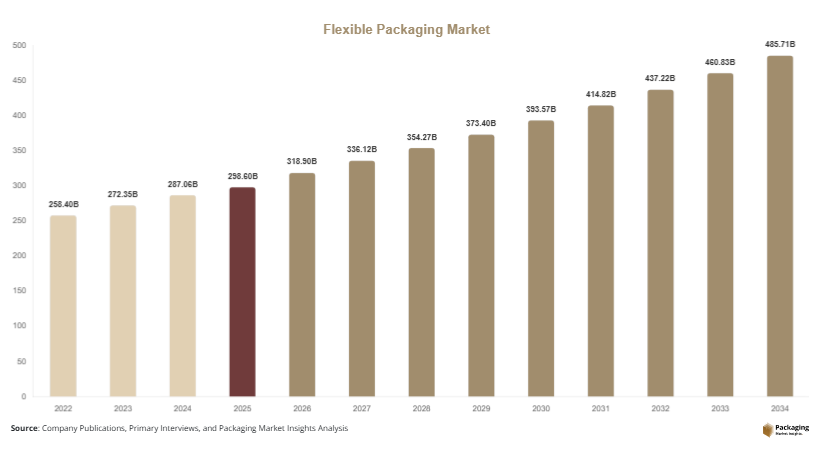

The global flexible packaging market size is estimated to reach USD 298.6 billion in 2025. With rising adoption across consumer goods sectors, the market is projected to grow to approximately USD 318.9 billion in 2026. Over the long-term forecast period, the market is expected to reach nearly USD 512.4 billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.4% between 2025 and 2034.

The flexible packaging market has experienced steady expansion over the past decade as manufacturers across industries shift toward lightweight, cost-efficient, and sustainable packaging formats. Flexible packaging refers to packaging solutions made from materials such as plastic films, aluminum foil, and paper that can easily change shape. These solutions are widely used in food and beverages, pharmaceuticals, personal care, and household products due to their versatility, extended shelf life capabilities, and reduced transportation costs.

Key Highlights

- Global flexible packaging market size estimated at USD 298.6 billion in 2025

- Market projected to reach USD 512.4 billion by 2034

- Expected CAGR of 5.4% from 2025 to 2034

- Increasing demand from food, beverage, and pharmaceutical industries

- Growing emphasis on lightweight and sustainable packaging solutions

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Recyclable Packaging Materials

Sustainability has become a central theme shaping the flexible packaging market. Governments, regulators, and consumers are increasingly demanding environmentally responsible packaging solutions that reduce waste and carbon emissions. As a result, manufacturers are investing in recyclable mono-material films, compostable packaging materials, and biodegradable polymers. These materials help address concerns regarding multi-layer plastic structures that are difficult to recycle.

Packaging producers are also collaborating with recycling technology providers to develop packaging formats that fit into existing recycling streams. Major consumer goods companies are introducing sustainability targets that prioritize recyclable or reusable packaging. Flexible packaging producers are responding by redesigning product structures to reduce material usage while maintaining barrier performance and durability. This shift toward sustainable packaging materials is expected to remain a key trend shaping innovation and investment across the market.

Expansion of Flexible Packaging in E-commerce and Retail Logistics

The rapid growth of e-commerce and digital retail channels is creating new opportunities for flexible packaging formats. Online retailers require packaging solutions that are lightweight, durable, and capable of protecting products during long transportation cycles. Flexible packaging addresses these requirements by reducing package weight and improving space efficiency during storage and shipping.

Many brands are adopting flexible pouches, mailer bags, and protective films for e-commerce shipments. These formats offer protective barriers while minimizing packaging volume. In addition, advancements in printing technology allow companies to customize packaging designs for online sales and limited-edition product launches. As global e-commerce continues to expand, flexible packaging solutions are becoming a preferred option for logistics optimization and brand presentation.

Market Drivers

Rising Demand for Packaged and Processed Food Products

The global food industry is undergoing significant transformation due to urbanization, changing dietary habits, and the growth of modern retail formats. Consumers increasingly prefer packaged foods that offer convenience, extended shelf life, and easy storage. Flexible packaging solutions such as pouches, sachets, and films provide excellent barrier properties that protect food from moisture, oxygen, and contamination.

These packaging formats are widely used for snacks, frozen foods, dairy products, and ready-to-eat meals. They also support portion control and resealability, which improves consumer convenience. As food companies expand their product portfolios and distribution networks, flexible packaging plays an important role in maintaining product quality during transportation and storage. This growing demand from the food industry remains a major driver supporting long-term growth in the flexible packaging market.

Cost Efficiency and Lightweight Advantages Over Rigid Packaging

Flexible packaging offers significant economic advantages compared with rigid packaging materials such as glass, metal, or rigid plastics. Flexible materials require less raw material during manufacturing, which reduces overall production costs. In addition, the lightweight nature of flexible packaging lowers transportation expenses and improves logistics efficiency.

Manufacturers and retailers benefit from reduced storage requirements because flexible packaging can be transported in flat or roll form before filling. This improves warehouse space utilization and lowers operational costs. The ability to produce flexible packaging in high volumes using advanced film extrusion and lamination technologies also supports cost-effective production. These economic benefits make flexible packaging an attractive option for companies seeking efficient packaging solutions.

Market Restraint

Environmental Concerns and Regulatory Pressure on Plastic Packaging

One of the primary restraints affecting the flexible packaging market is the increasing regulatory pressure related to plastic waste management. Many flexible packaging solutions rely on multi-layer plastic films that provide barrier protection but are difficult to recycle using conventional recycling systems. Governments around the world are introducing policies aimed at reducing single-use plastic waste and promoting circular economy practices.

These regulations include plastic taxes, extended producer responsibility programs, and restrictions on certain types of packaging materials. Compliance with these policies often requires packaging manufacturers to redesign products, invest in new materials, or modify production processes. Such changes can increase operational costs and create uncertainty for industry participants.

For example, several European countries have implemented packaging waste directives that encourage recyclable or reusable packaging formats. Companies operating in these markets must adapt their product structures to meet sustainability guidelines. Smaller packaging producers may face challenges in financing research and development activities needed to develop alternative materials.

However, these regulatory pressures are also driving innovation within the industry. Manufacturers are increasingly exploring recyclable mono-material films, bio-based polymers, and compostable packaging technologies. While environmental regulations present short-term challenges, they are expected to encourage long-term transformation in packaging design and material selection.

Market Opportunities

Growth of Bio-based and Compostable Packaging Materials

The development of bio-based and compostable materials presents a major opportunity within the flexible packaging market. As sustainability concerns continue to influence consumer purchasing decisions, companies are seeking packaging solutions that reduce environmental impact. Bio-based materials derived from renewable resources such as corn starch, sugarcane, and cellulose are gaining attention as potential alternatives to conventional plastic films.

Advancements in material science are improving the performance characteristics of these materials, enabling them to provide barrier protection and durability comparable to traditional plastics. Many packaging producers are forming partnerships with biotechnology companies to develop scalable production methods for biodegradable packaging films. As regulatory incentives and consumer awareness increase, bio-based flexible packaging is expected to become a significant growth segment within the industry.

Increasing Adoption in Pharmaceutical and Healthcare Packaging

The pharmaceutical and healthcare industries are increasingly adopting flexible packaging solutions due to their protective and cost-efficient properties. Flexible packaging formats such as blister films, medical pouches, and sterile barrier systems provide reliable protection against contamination and environmental exposure. These packaging solutions help maintain product integrity while ensuring compliance with regulatory requirements.

The growth of the global pharmaceutical sector, driven by aging populations and rising healthcare expenditures, is creating new demand for specialized packaging materials. Flexible packaging manufacturers are developing high-barrier films and tamper-evident packaging systems that meet strict quality standards. As pharmaceutical companies expand their global distribution networks, flexible packaging solutions will play an important role in ensuring product safety and logistics efficiency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 298.6 Billion |

| Market Size in 2026 | USD 318.9 Billion |

| Market Size in 2034 | USD 512.4 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Plastic materials dominated the flexible packaging market with approximately 62.5% share in 2024. Plastic films such as polyethylene, polypropylene, and polyethylene terephthalate are widely used because of their durability, flexibility, and strong barrier properties. These materials offer excellent protection against moisture and oxygen, making them suitable for food and beverage packaging. Plastic packaging also supports high-speed manufacturing processes and cost-efficient production. Many manufacturers continue to rely on multi-layer plastic film structures to achieve enhanced barrier performance for perishable products. As consumer demand for packaged foods continues to rise, plastic materials remain a central component of flexible packaging solutions across multiple industries.

Paper-based flexible packaging is expected to be the fastest-growing material segment, with a projected CAGR of around 6.1% through 2034. The growth of this segment is driven by increasing demand for environmentally friendly packaging solutions. Paper packaging materials are often recyclable and derived from renewable resources, which aligns with sustainability goals adopted by many consumer goods companies. Packaging manufacturers are investing in advanced coatings and lamination technologies to improve the moisture resistance and durability of paper-based packaging. These innovations allow paper packaging to replace plastic in certain applications such as dry foods, bakery products, and retail shopping bags.

By Packaging Type

Pouches accounted for the largest share of approximately 38.9% in 2024 within the flexible packaging market. Stand-up pouches and flat pouches are widely used across food, beverage, and personal care industries due to their versatility and convenience. These packaging formats offer features such as resealable closures, easy-tear openings, and lightweight construction. Stand-up pouches also provide strong shelf presence in retail environments, allowing brands to display products effectively. The combination of functional design and cost efficiency has made pouches a preferred packaging format for manufacturers seeking flexible and consumer-friendly packaging solutions.

The sachets and stick packs segment is expected to witness the fastest growth, with an estimated CAGR of 6.3% over the forecast period. This growth is largely driven by increasing demand for small-portion packaging formats in emerging markets. Sachets are commonly used for products such as instant coffee, condiments, shampoo, and single-serve beverages. These formats allow consumers to purchase products in affordable portions, which supports market penetration in price-sensitive regions. Additionally, companies use sachet packaging to introduce new products and expand distribution in rural areas where small-quantity purchases are common.

By End-Use Industry

The food and beverage industry represented the dominant end-use segment with approximately 54.6% share in 2024. Flexible packaging solutions are widely used for snacks, frozen foods, dairy products, beverages, and ready-to-eat meals. The strong barrier properties of flexible packaging help maintain product freshness while reducing spoilage. Additionally, flexible packaging supports convenient packaging formats such as resealable bags and single-serve portions. As global demand for packaged foods continues to rise, the food and beverage sector remains the primary consumer of flexible packaging materials.

The pharmaceutical and healthcare segment is projected to grow at the fastest CAGR of 6.0% through 2034. The growth of this segment is supported by increasing demand for safe and sterile packaging solutions. Flexible packaging formats such as medical pouches and blister films provide reliable protection against contamination and environmental exposure. Pharmaceutical companies also benefit from the lightweight and cost-efficient characteristics of flexible packaging during global product distribution.

Flexible Packaging Market Segmentations

Material

- Plastic

- Paper

- Aluminum Foil

- Bioplastics

Packaging Type

- Pouches

- Bags

- Sachets & Stick Packs

- Wraps & Films

End-Use Industry

- Food & Beverage

- Pharmaceutical & Healthcare

- Personal Care & Cosmetics

- Household Products

- Industrial Applications

Regional Analysis

North America

North America accounted for approximately 26.4% share of the global flexible packaging market in 2025. The region is expected to grow at a CAGR of 4.8% during the forecast period. Market growth is supported by the strong presence of packaged food manufacturers and well-established retail distribution networks. Flexible packaging is widely used in snack foods, frozen meals, and ready-to-drink beverages across the United States and Canada.

The United States represents the dominant country within the North American market. A key growth factor in the country is the increasing demand for sustainable packaging solutions from consumer goods companies. Major brands are introducing recyclable packaging targets, which encourages packaging manufacturers to develop eco-friendly flexible materials and advanced film technologies.

Europe

Europe held nearly 23.7% share of the global flexible packaging market in 2025. The region is expected to register a CAGR of around 4.6% through 2034. Growth is supported by strong environmental awareness and the adoption of advanced recycling infrastructure. Flexible packaging is widely used in the food, pharmaceutical, and personal care sectors across European countries.

Germany is the dominant market in the region. The country benefits from a strong manufacturing base and advanced packaging technology capabilities. One unique growth factor is the widespread adoption of circular economy initiatives, which encourage companies to develop recyclable and reusable packaging materials.

Asia Pacific

Asia Pacific represented the largest regional share at approximately 34.8% in 2025. The region is projected to grow at the fastest CAGR of 6.4% during the forecast period. Rapid urbanization, expanding middle-class populations, and growing retail industries are contributing to the rising demand for packaged consumer goods.

China leads the Asia Pacific market due to its large manufacturing sector and strong domestic demand for packaged foods and beverages. A key growth factor in the country is the rapid expansion of e-commerce platforms, which increases demand for lightweight and durable flexible packaging solutions.

Middle East & Africa

The Middle East & Africa region accounted for around 7.1% share of the global flexible packaging market in 2025. The market is expected to grow at a CAGR of 5.1% during the forecast period. Growth is supported by increasing investments in food processing industries and expanding retail infrastructure across several countries.

Saudi Arabia is one of the leading markets in the region. A major growth factor is the expansion of local food production and packaging industries as part of economic diversification initiatives. This has increased demand for cost-efficient packaging materials used in domestic food manufacturing.

Latin America

Latin America represented nearly 8.0% of the global flexible packaging market in 2025. The region is projected to expand at a CAGR of 5.0% between 2025 and 2034. Market growth is supported by the increasing demand for packaged consumer goods and improving retail distribution networks.

Brazil dominates the regional market due to its large food and beverage industry. A key growth factor is the rising popularity of flexible packaging for snack foods and convenience products. Local manufacturers are also investing in modern packaging technologies to improve product shelf life and logistics efficiency.

Competitive Landscape

The flexible packaging market is characterized by the presence of several global packaging companies that compete through product innovation, geographic expansion, and strategic partnerships. Market participants are focusing on developing recyclable and sustainable packaging materials in response to evolving regulatory requirements and consumer preferences.

Among the major companies operating in the industry, Amcor plc is widely recognized as a market leader due to its extensive global manufacturing network and strong research and development capabilities. The company continues to invest in advanced recyclable packaging solutions and sustainable material technologies.

Other prominent companies include Sealed Air Corporation, Berry Global Group, Mondi Group, and Huhtamaki Oyj. These companies are expanding their product portfolios by introducing high-barrier films, recyclable mono-material packaging structures, and lightweight flexible packaging formats.

In recent years, companies have also pursued mergers, acquisitions, and strategic partnerships to strengthen their market presence. For example, several packaging firms have partnered with material science companies to develop biodegradable film technologies. Continuous innovation and sustainability initiatives remain central strategies for maintaining competitiveness within the global flexible packaging market.

Key Players List

- Amcor plc

- Berry Global Group, Inc.

- Sealed Air Corporation

- Mondi Group

- Huhtamaki Oyj

- Sonoco Products Company

- Constantia Flexibles Group

- Coveris Holdings S.A.

- ProAmpac LLC

- Glenroy Inc.

- Uflex Ltd.

- Clondalkin Group

- Winpak Ltd.

- Transcontinental Inc.

- Bischof + Klein SE & Co. KG