Feed Packaging Market Size And Growth

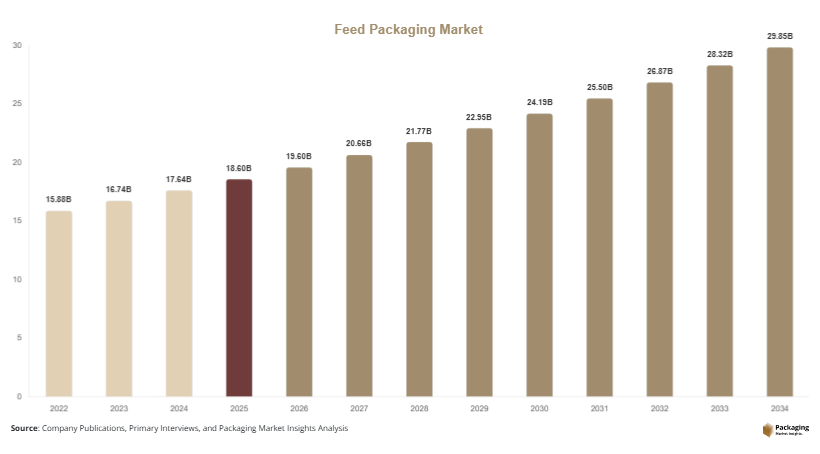

The Feed Packaging Market size was valued at approximately USD 18.6 billion in 2025 and is projected to reach USD 29.8 billion by 2034, expanding at a CAGR of 5.4% during the forecast period (2025–2034). The market growth is primarily supported by the steady expansion of the global livestock and aquaculture industries, which has increased demand for safe, durable, and contamination-resistant packaging solutions for feed products.

A major global factor driving the Feed Packaging Market is the rising need for efficient supply chain management in animal nutrition. As feed products are increasingly traded across regions, packaging plays a crucial role in preserving product quality, preventing spoilage, and ensuring regulatory compliance. Additionally, the growing awareness of feed hygiene and shelf-life stability is accelerating the adoption of advanced packaging formats.

Key Highlights:

- Asia Pacific dominated the market with a 38.2% share in 2025, while it is projected to grow at the fastest CAGR of 6.2% through 2034.

- Flexible packaging led the type segment with a 61.5% share, while biodegradable packaging materials are expected to grow at a CAGR of 6.8%.

- China, the dominant country, recorded a market value of USD 4.1 billion in 2025, projected to reach USD 4.4 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable Packaging Solutions

The feed packaging market is witnessing a gradual transition toward environmentally responsible materials. Manufacturers are adopting recyclable, compostable, and bio-based packaging solutions to align with regulatory expectations and sustainability goals. Paper-based sacks, biodegradable films, and reduced plastic content packaging are gaining traction, especially among large feed producers aiming to minimize environmental impact while maintaining durability and barrier performance.

Increasing Adoption of High-Barrier Flexible Packaging

High-barrier flexible packaging is emerging as a preferred solution for feed products due to its ability to protect against moisture, oxygen, and contaminants. Multi-layer films and laminated pouches are being increasingly used to extend shelf life and reduce product losses. These solutions also offer lightweight advantages, improving logistics efficiency and lowering transportation costs. The trend is particularly evident in aquafeed and specialty feed segments where product sensitivity is higher.

Market Drivers

Growth of Livestock and Aquaculture Production

The expansion of livestock farming and aquaculture industries is a major driver for the feed packaging market. Increasing demand for animal-based products such as meat, dairy, and seafood is fueling feed production, thereby boosting the need for reliable packaging solutions. Packaging ensures safe storage, handling, and transportation of feed, which is essential for maintaining nutritional value and quality.

Rising Demand for Feed Safety and Quality Assurance

The need to maintain feed quality and prevent contamination has intensified across global markets. Packaging solutions with improved sealing, moisture resistance, and durability are becoming essential to meet regulatory standards and ensure product integrity. This has led to increased adoption of advanced packaging technologies, including multi-layer films and tamper-resistant bags.

Market Restraint

Fluctuating Raw Material Prices

Volatility in the prices of packaging raw materials such as plastics, paper, and metals presents a significant challenge for the feed packaging market. Changes in crude oil prices directly impact plastic packaging costs, while variations in pulp prices affect paper-based packaging. These fluctuations can reduce profit margins for manufacturers and create pricing challenges for end users. Additionally, the cost pressure may limit the adoption of advanced or sustainable packaging solutions in price-sensitive markets.

Market Opportunities

Development of Smart Packaging Solutions

The integration of smart technologies into feed packaging offers new growth opportunities. Features such as QR codes, freshness indicators, and traceability systems can enhance supply chain transparency and improve product monitoring. These innovations are expected to gain traction in premium feed segments.

Expansion in Emerging Markets

Emerging economies in Asia, Africa, and Latin America present significant opportunities for the feed packaging market. Rapid urbanization, increasing livestock production, and growing awareness of feed quality are driving demand for packaged feed products. Local manufacturing and cost-effective packaging solutions are expected to support market growth in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.6 Billion |

| Market Size in 2034 | USD 29.8 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flexible packaging dominated the feed packaging market, accounting for 61.5% share in 2025 due to its lightweight nature and cost efficiency. It is widely used for bulk feed packaging and offers ease of transportation.

Rigid packaging is expected to grow at a CAGR of 5.9%, driven by its durability and suitability for premium feed products requiring enhanced protection.

By Material

Plastic materials held the largest share of 54.2% in 2025, supported by their versatility and barrier properties. Plastic packaging remains widely used across feed categories.

Biodegradable materials are projected to grow at a CAGR of 6.8%, driven by environmental concerns and regulatory pressures encouraging sustainable solutions.

By Livestock Type

Poultry feed packaging dominated with a 36.8% share in 2025, reflecting high poultry consumption globally.

Aquaculture feed packaging is expected to grow at a CAGR of 6.5%, supported by rising seafood demand and specialized feed requirements.

By Packaging Format

Bags and sacks accounted for 48.7% share in 2025, as they are widely used for bulk storage and transportation.

Pouches and small packs are projected to grow at a CAGR of 6.1%, driven by increasing demand for convenience and smaller packaging sizes.

Feed Packaging Market Segmentations

Type

- Flexible Packaging

- Rigid Packaging

Material

- Plastics

- Paper & Paperboard

- Metals

- Biodegradable Materials

Livestock Type

- Poultry

- Cattle

- Aquaculture

- Others

Packaging Format

- Bags & Sacks

- Pouches

- Containers

- Others

Regional Analysis

North America

North America accounted for 24.5% of the feed packaging market share in 2025 and is expected to grow at a CAGR of 4.8% during the forecast period. The region’s growth is supported by advanced feed production systems and well-established supply chains.

The United States dominated the regional market due to its large-scale livestock industry and emphasis on feed quality standards. The country’s adoption of technologically advanced packaging solutions has contributed to steady demand.

Europe

Europe held a 21.3% share in 2025 and will grow at a CAGR of 4.6% through 2034. The region benefits from strict regulatory frameworks governing feed safety and packaging materials.

Germany emerged as the dominant country, driven by its strong animal husbandry sector and focus on sustainable packaging practices. The shift toward recyclable materials is shaping regional demand.

Asia Pacific

Asia Pacific accounted for 38.2% of the feed packaging market in 2025 and will grow at a CAGR of 6.2%. Rapid industrialization and increasing demand for animal protein are key growth contributors.

China led the region, supported by its extensive feed production industry and growing exports. The country’s focus on improving feed quality has driven demand for advanced packaging solutions.

Middle East & Africa

The Middle East & Africa held a 9.1% share in 2025 and is projected to grow at a CAGR of 5.1%. Growth is driven by increasing investments in livestock farming and feed production.

South Africa dominated the region due to its organized agricultural sector and growing demand for packaged feed products.

Latin America

Latin America accounted for 6.9% of the market in 2025 and is expected to grow at a CAGR of 5.0%. The region’s growth is supported by expanding poultry and cattle industries.

Brazil led the market, benefiting from its strong agricultural base and increasing feed exports.

Competitive Landscape

The feed packaging market is moderately competitive, with several global and regional players focusing on product innovation and expansion strategies. Companies are investing in sustainable materials and advanced packaging technologies to strengthen their market presence.

Amcor plc is a key market leader, known for its extensive portfolio of flexible packaging solutions. The company recently introduced recyclable packaging options tailored for industrial applications, including feed products.

Other prominent players include Berry Global Inc., Mondi Group, Sonoco Products Company, and Smurfit Kappa Group. These companies are emphasizing strategic collaborations, product development, and regional expansion to enhance their market position.

Key Players List

- Amcor plc

- Berry Global Inc.

- Mondi Group

- Sonoco Products Company

- Smurfit Kappa Group

- Sealed Air Corporation

- Huhtamaki Oyj

- DS Smith plc

- Coveris Holdings S.A.

- Winpak Ltd.

- ProAmpac LLC

- LC Packaging International BV

- NNZ Group

- Uflex Ltd.

- Constantia Flexibles