Fast Food Containers Market Size and Growth

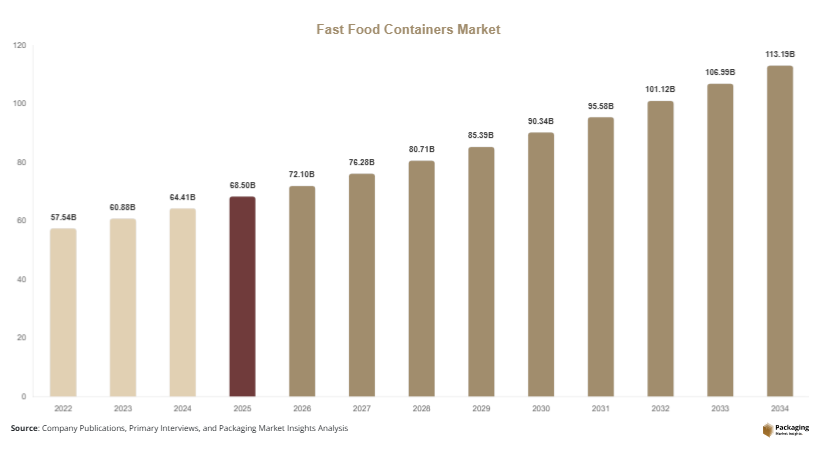

The fast food containers market size reached approximately USD 68.5 billion in 2025 and is estimated to grow to USD 72.1 billion in 2026. Over the forecast period from 2025 to 2034, the market is projected to expand at a CAGR of 5.8%, ultimately reaching USD 119.3 billion by 2034. This growth reflects a combination of demographic shifts, urban lifestyles, and the increasing reliance on packaged food solutions across both developed and emerging economies. The fast food containers market is experiencing steady growth due to rising consumption of convenience food and the rapid expansion of food delivery ecosystems worldwide.

One of the primary growth factors is the expansion of quick-service restaurant chains and online food delivery platforms. Consumers are increasingly opting for takeaway and ready-to-eat meals, which require efficient packaging solutions that preserve food quality during transit. Another important factor is the rising awareness of hygiene and food safety, which is encouraging the use of secure and contamination-resistant containers. Additionally, the growing focus on sustainability is pushing manufacturers to develop eco-friendly alternatives such as biodegradable and recyclable materials, further influencing market dynamics.

Key Highlights:

- Asia Pacific dominated the market with a 38.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.4%.

- Plastic-based containers led the material segment with a 49.7% share, while biodegradable containers are expected to grow at a CAGR of 6.8%.

- Clamshell containers dominated with a 34.5% share, while flexible packaging is forecasted to grow at a CAGR of 6.1%.

- Quick-service restaurants led the end-use segment with 45.2% share, while cloud kitchens are expected to grow at a CAGR of 7.0%.

- The United States remained the dominant country with a market size of USD 14.6 billion in 2025 and USD 15.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Packaging Solutions

The fast food containers market is witnessing a strong transition toward sustainable packaging materials driven by environmental concerns and evolving regulatory frameworks. Governments across multiple regions are implementing restrictions on single-use plastics, which is compelling manufacturers to adopt biodegradable and compostable materials such as paperboard, molded fiber, and plant-based polymers. Consumers are also becoming more environmentally conscious and prefer brands that demonstrate responsible packaging practices. This shift is encouraging food service providers to redesign their packaging strategies and align with sustainability goals. Companies are investing in research and development to create materials that maintain functionality while reducing environmental impact. This trend is expected to reshape product innovation and create long-term growth opportunities in the market.

Advancements in Functional and Smart Packaging

Technological innovation is transforming the design and functionality of fast food containers. Manufacturers are focusing on improving convenience, durability, and food preservation capabilities through advanced packaging solutions. Features such as heat retention layers, moisture control systems, and leak-proof designs are becoming standard requirements in the industry. Additionally, digital integration through QR codes and smart labels is enabling brands to enhance consumer interaction and provide detailed product information. These innovations not only improve user experience but also support operational efficiency for food delivery services. As competition intensifies, companies are increasingly leveraging advanced packaging technologies to differentiate their offerings and strengthen their market presence.

Market Drivers

Expansion of Food Delivery Ecosystems

The rapid growth of online food delivery platforms is significantly influencing the fast food containers market. With the increasing penetration of smartphones and digital payment systems, consumers are relying heavily on food delivery services for daily meals. This shift has created a strong demand for packaging solutions that ensure food safety, temperature control, and ease of handling during transportation. Restaurants and cloud kitchens require reliable containers that can maintain product quality over extended delivery times. As delivery volumes continue to rise, the need for standardized and efficient packaging solutions is expected to grow, supporting overall market expansion.

Rising Preference for Convenient Consumption Formats

Changing consumer lifestyles and busy schedules are driving the demand for convenient food consumption options. The increasing working population and urbanization are encouraging the adoption of takeaway meals and ready-to-eat food products. Fast food containers play a critical role in enabling portability and ease of use, making them essential for modern food consumption patterns. Manufacturers are focusing on developing lightweight, stackable, and easy-to-handle packaging solutions that enhance user convenience. This trend is particularly prominent among younger consumers who prioritize speed and accessibility in their food choices, thereby sustaining long-term demand for fast food containers.

Market Restraint

Regulatory Pressure on Plastic-Based Packaging

The fast food containers market faces challenges due to increasing regulatory restrictions on plastic usage. Governments across various regions are implementing strict policies to reduce environmental pollution caused by single-use plastics. These regulations include bans, taxes, and mandates for recyclable or biodegradable materials. While these measures promote sustainability, they also create challenges for manufacturers in terms of cost and production complexity. Transitioning to alternative materials often requires significant investment in new technologies and supply chains. For instance, replacing traditional plastic containers with biodegradable options can increase production costs and impact pricing strategies. Additionally, inconsistent regulations across regions complicate compliance for global companies, creating operational inefficiencies and limiting market growth potential.

Market Opportunities

Development of Eco-Friendly Material Innovations

The growing emphasis on sustainability presents significant opportunities for innovation in the fast food containers market. Manufacturers are exploring advanced materials such as biodegradable polymers, edible packaging, and reusable container systems to meet environmental standards. These innovations not only address regulatory requirements but also enhance brand image and customer loyalty. Companies that invest in sustainable solutions are likely to gain a competitive advantage and capture a larger market share. The increasing availability of cost-effective eco-friendly materials is further supporting their adoption across the food service industry.

Expansion in Emerging Economies

Emerging markets are offering substantial growth opportunities due to rapid urbanization and rising disposable incomes. Countries in Asia Pacific, Latin America, and Africa are experiencing increased demand for fast food and delivery services. The expansion of quick-service restaurants and digital food platforms in these regions is driving the need for efficient packaging solutions. Manufacturers can capitalize on these opportunities by establishing local production facilities and adapting their products to regional preferences. This approach not only reduces costs but also enhances market penetration and competitiveness in high-growth regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 68.5 Billion |

| Market Size in 2026 | USD 72.1 Billion |

| Market Size in 2034 | USD 119.3 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

Material Type

Plastic-based containers accounted for the largest share of the fast food containers market in 2024, contributing approximately 49.7% of total revenue. These containers are widely used due to their durability, cost efficiency, and ability to maintain food quality during transportation. Plastic materials offer excellent resistance to moisture and temperature changes, making them suitable for various food applications. Additionally, their lightweight nature reduces logistics costs and enhances operational efficiency for food service providers.

Biodegradable materials are emerging as the fastest-growing segment, expected to register a CAGR of 6.8% during the forecast period. Increasing environmental awareness and regulatory pressure are driving the adoption of sustainable alternatives. Manufacturers are investing in innovative materials such as plant-based polymers and compostable fibers to meet consumer expectations and compliance standards.

Product Type

Clamshell containers held the largest share in 2024, accounting for 34.5% of the total market. These containers are commonly used for packaging burgers, sandwiches, and other fast food items due to their secure closure and convenience. Their design helps maintain food integrity and prevents leakage during transportation, making them highly suitable for takeaway and delivery services.

Flexible packaging is expected to grow at the fastest rate, with a CAGR of 6.1% over the forecast period. The demand for lightweight and space-efficient packaging solutions is driving this segment. Flexible packaging offers advantages such as reduced material usage and improved storage efficiency, making it an attractive option for food delivery operations.

End-Use

Quick-service restaurants accounted for the largest share of the market in 2024, contributing 45.2% of total revenue. The high volume of takeaway orders and the need for standardized packaging solutions are key factors supporting this segment. QSR chains require packaging that ensures food safety and enhances brand visibility.

Cloud kitchens represent the fastest-growing segment, with a projected CAGR of 7.0%. The rise of online food delivery platforms and virtual restaurants is driving demand for efficient packaging solutions. These operations rely heavily on packaging to maintain food quality and customer satisfaction, creating significant growth opportunities for manufacturers.

Fast Food Containers Market Segmentations

By Material Type

- Plastic Containers

- Paper & Paperboard Containers

- Biodegradable & Compostable Containers

By Product Type

- Clamshell Containers

- Cups & Lids

- Trays & Bowls

- Flexible Packaging

By End-Use

- Quick-Service Restaurants

- Full-Service Restaurants

- Cloud Kitchens

- Catering Services

Regional Analysis

North America

North America accounted for a significant portion of the fast food containers market in 2025, holding approximately 28.6% of the global share. The region is projected to grow at a CAGR of 5.2% during the forecast period. Strong consumer demand for convenience food and the widespread presence of established quick-service restaurant chains contribute to steady market expansion. Technological advancements in packaging materials and increasing adoption of sustainable solutions are further supporting growth across the region.

The United States dominates the regional market due to its highly developed food service industry. A key growth factor is the increasing adoption of eco-friendly packaging by major restaurant chains. Companies are focusing on reducing environmental impact while maintaining packaging efficiency, which is driving innovation and market development in the country.

Europe

Europe held around 24.3% of the market share in 2025 and is expected to grow at a CAGR of 5.0% through 2034. The region is characterized by strict environmental regulations and strong consumer awareness regarding sustainability. These factors are encouraging the adoption of recyclable and biodegradable packaging materials across the food service industry.

Germany leads the European market, supported by its advanced manufacturing infrastructure and focus on environmental responsibility. Circular economy initiatives are playing a significant role in driving demand for sustainable packaging solutions, creating new opportunities for manufacturers in the region.

Asia Pacific

Asia Pacific emerged as the largest regional market, accounting for 38.1% of the global share in 2025. The region is expected to grow at a CAGR of 6.1% during the forecast period. Rapid urbanization, population growth, and increasing disposable incomes are key factors driving demand for fast food containers. The expansion of quick-service restaurant chains and food delivery platforms is further accelerating market growth.

China dominates the Asia Pacific market due to its large consumer base and rapidly growing food service sector. The widespread adoption of online food delivery services is a major growth factor, significantly increasing the demand for durable and efficient packaging solutions in urban areas.

Middle East & Africa

The Middle East & Africa region accounted for approximately 5.8% of the market share in 2025 and is projected to grow at a CAGR of 5.5%. Increasing urbanization and changing consumer preferences are driving demand for fast food and convenient packaging solutions. The expansion of international restaurant chains is also contributing to market growth.

The United Arab Emirates is the dominant country in the region, supported by a strong tourism sector and a growing hospitality industry. The demand for premium packaging solutions that enhance presentation and customer experience is a key factor driving market development.

Latin America

Latin America held a market share of around 3.2% in 2025 and is expected to grow at the fastest CAGR of 6.4% during the forecast period. The region is experiencing increased demand for fast food and delivery services due to urbanization and lifestyle changes. The growth of digital platforms is also supporting market expansion.

Brazil dominates the Latin American market due to its large population and expanding food service industry. Increasing investments in local manufacturing are improving supply chain efficiency and reducing costs, which is supporting the growth of the fast food containers market in the region.

Competitive Landscape

The fast food containers market is moderately fragmented, with a mix of global and regional players competing on innovation, pricing, and sustainability. Companies are focusing on expanding their product portfolios and adopting eco-friendly materials to align with changing consumer preferences. Strategic collaborations and capacity expansions are common strategies used to strengthen market position.

Amcor plc is recognized as a leading player in the market, driven by its strong focus on sustainable packaging solutions. The company has introduced recyclable and biodegradable container lines to address environmental concerns and regulatory requirements. Other key players are also investing in research and development to enhance product performance and reduce environmental impact, intensifying competition across the industry.

Key Players List

- Amcor plc

- Berry Global Inc.

- Dart Container Corporation

- Genpak LLC

- Huhtamaki Oyj

- Pactiv Evergreen Inc.

- Sabert Corporation

- Sonoco Products Company

- WestRock Company

- Novolex Holdings, Inc.

- Anchor Packaging LLC

- Detpak (Detmold Group)

- Vegware Ltd.

- Eco-Products, Inc.

- Reynolds Consumer Products