Europe Flexible Packaging Market Size and Growth

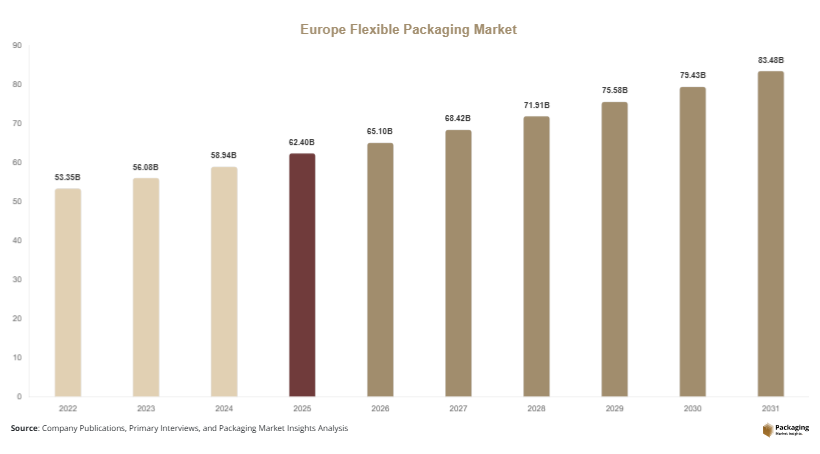

The Europe Flexible Packaging Market was valued at approximately USD 62.4 billion in 2025 and is projected to reach USD 83.7 billion by 2030, expanding at a CAGR of 5.1% during 2025–2031. The market reflects steady growth driven by increasing demand across food, pharmaceuticals, and personal care sectors, where lightweight, cost-effective, and sustainable packaging formats are gaining wider acceptance.

A key global factor supporting the growth of the Europe Flexible Packaging Market is the rising shift toward sustainable packaging solutions. Regulatory pressure across Europe, combined with consumer preference for recyclable and low-carbon packaging, has encouraged manufacturers to invest in biodegradable films, mono-material laminates, and advanced barrier technologies. This has reshaped product innovation and supply chain strategies across the industry.

Flexible packaging continues to outperform rigid alternatives due to its reduced material usage, improved shelf life, and transportation efficiency. Additionally, the growth of e-commerce and convenience food consumption has reinforced the demand for flexible formats such as pouches, sachets, and wraps.

Key Highlights:

- Europe accounted for a 28.6% share of the global flexible packaging market in 2025, while Asia Pacific is expected to grow at a CAGR of 6.8% through 2031.

- Plastic-based materials dominated with a 64.3% share, while biodegradable materials are projected to grow at a CAGR of 7.2%.

- Pouches led the product segment with a 39.5% share, whereas stand-up pouches are expected to grow at a CAGR of 6.5%.

- Germany, the dominant country, recorded USD 14.2 billion in 2025 and is estimated to reach USD 14.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Circular and Recyclable Packaging Solutions

The Europe Flexible Packaging Market is increasingly aligned with circular economy principles. Manufacturers are transitioning from multi-layer laminates to mono-material structures that are easier to recycle. Innovations in barrier coatings are enabling recyclable films to match the performance of traditional materials. This trend is reinforced by European Union regulations aimed at reducing packaging waste and improving recyclability rates. As a result, companies are redesigning packaging formats while investing in recycling infrastructure partnerships.

Digital Printing and Customization in Flexible Packaging

Digital printing technology is transforming production processes in the Europe Flexible Packaging Market. Brands are leveraging short-run, high-quality printing to enable product differentiation and faster time-to-market. This trend is particularly evident in food, beverage, and personal care industries where packaging aesthetics influence consumer purchasing decisions. Digital printing also supports versioning and personalization, allowing companies to adapt packaging for regional markets and promotional campaigns without increasing operational complexity.

Market Drivers

Growth in Convenience Food Consumption

The increasing demand for ready-to-eat and packaged food products has significantly contributed to the growth of the Europe Flexible Packaging Market. Urbanization, changing lifestyles, and rising disposable incomes have led consumers to prefer convenient, portable, and easy-to-store packaging formats. Flexible packaging provides extended shelf life and portion control, making it suitable for modern retail and on-the-go consumption patterns.

Cost Efficiency and Material Optimisation

Flexible packaging offers substantial cost advantages compared to rigid packaging alternatives. Reduced raw material usage, lower transportation costs, and improved storage efficiency have made it a preferred choice for manufacturers. In the Europe Flexible Packaging Market, companies are increasingly adopting lightweight packaging solutions to reduce logistics expenses and carbon footprint. This economic benefit, combined with sustainability goals, is driving widespread adoption across multiple industries.

Market Restraints

Recycling Complexity of Multi-Layer Materials

One of the major challenges in the Europe Flexible Packaging Market is the difficulty in recycling multi-layer flexible materials. These structures often combine different polymers and aluminum layers to achieve barrier properties, making separation and recycling technically complex and economically unviable. Despite advancements in recycling technologies, infrastructure limitations persist across several European countries.

This restraint impacts the sustainability goals of manufacturers and creates regulatory pressure to redesign packaging formats. Companies are required to invest in research and development to develop recyclable alternatives without compromising performance. However, the transition involves higher costs and operational adjustments, which can limit adoption among small and medium enterprises.

Market Opportunities

Expansion of Bio-Based and Compostable Packaging

The growing emphasis on sustainability presents significant opportunities for bio-based and compostable flexible packaging materials. In the Europe Flexible Packaging Market, manufacturers are investing in plant-based polymers and biodegradable films to meet regulatory requirements and consumer expectations. These materials offer a competitive advantage in environmentally conscious markets and open new revenue streams for innovative packaging solutions.

Growth of E-commerce Packaging Solutions

The expansion of e-commerce across Europe is creating new opportunities for flexible packaging formats. Lightweight and durable packaging solutions are essential for efficient shipping and product protection. Flexible packaging reduces shipping costs and enhances user experience through easy-to-open and resealable features. This trend is expected to drive demand for customized packaging solutions tailored to online retail requirements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 62.4 Billion |

| Market Size in 2026 | USD 65.1 Billion |

| Market Size in 2031 | USD 88.1 Billion |

| CAGR | 5.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Plastic materials dominated the Europe Flexible Packaging Market with a 64.3% share in 2024. Polyethylene and polypropylene were widely used due to their versatility, durability, and cost-effectiveness. These materials provided excellent barrier properties and flexibility, making them suitable for various applications including food packaging and industrial uses.

Biodegradable materials are expected to be the fastest-growing segment, with a projected CAGR of 7.2%. The growth is driven by increasing environmental regulations and consumer demand for sustainable packaging solutions. Innovations in bio-based polymers and compostable films will enhance adoption across multiple industries.

By Product Type

Pouches accounted for the largest share, contributing 39.5% in 2024. Their lightweight nature, ease of storage, and extended shelf life made them highly preferred across food and beverage applications. Stand-up pouches gained popularity due to their convenience and visual appeal.

Stand-up pouches are projected to grow at a CAGR of 6.5%, driven by their functionality and adaptability in retail environments. Their ability to incorporate resealable features and attractive designs will support continued growth.

By Application

Food and beverage applications dominated the market with a 52.7% share in 2024. Flexible packaging played a critical role in preserving freshness and extending shelf life of perishable products. The segment benefited from increasing consumption of packaged and processed foods.

Pharmaceutical applications are expected to grow at a CAGR of 6.2% due to rising healthcare demand and stringent packaging requirements. Flexible packaging offers tamper-evident and moisture-resistant properties, making it suitable for medical products.

By End-Use Industry

The food industry led with a 48.9% share in 2024, driven by high demand for packaged food products. Flexible packaging provided cost efficiency and improved logistics, supporting widespread adoption.

The personal care and cosmetics segment is expected to grow at a CAGR of 6.0%, supported by increasing demand for innovative packaging designs and sustainable materials. Flexible packaging enables convenient dispensing and enhances product appeal.

Europe Flexible Packaging Market Segmentations

By Material

- Plastic

- Paper

- Aluminum Foil

- Biodegradable Materials

By Product Type

- Pouches

- Bags

- Wraps

- Films

- Sachets

By Application

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial

- Others

By End-Use Industry

- Food Industry

- Healthcare

- Personal Care

- Retail

- Others

Regional Analysis

North America

North America accounted for approximately 24.1% of the global flexible packaging market share in 2025 and is expected to grow at a CAGR of 4.6% during 2025–2033. The region demonstrated steady demand driven by the food and pharmaceutical sectors. Regulatory frameworks supporting sustainable packaging and technological advancements in barrier materials contributed to market stability.

The United States remained the dominant country, supported by a strong packaged food industry and high consumer demand for convenience products. The presence of established packaging manufacturers and continuous innovation in recyclable materials strengthened the country’s market position.

Europe

Europe held a 28.6% share of the global flexible packaging market in 2025 and is projected to grow at a CAGR of 5.1% through 2033. The Europe Flexible Packaging Market benefited from strict environmental regulations and high consumer awareness regarding sustainable packaging. Investments in recycling infrastructure and adoption of eco-friendly materials drove market expansion.

Germany emerged as the dominant country due to its advanced manufacturing base and strong demand from food and pharmaceutical industries. The country’s focus on circular economy initiatives and technological innovation in packaging materials supported its leading position.

Asia Pacific

Asia Pacific captured around 32.8% of the global market share in 2025 and will grow at a CAGR of 6.8% during 2025–2033. Rapid urbanization, increasing disposable income, and expansion of the retail sector drove demand for flexible packaging. The region experienced significant growth in packaged food consumption and e-commerce activities.

China dominated the regional market due to its large population base and strong manufacturing capabilities. The country’s expanding middle class and growing demand for convenience products contributed to sustained market growth.

Middle East & Africa

The Middle East & Africa accounted for 7.3% of the global market share in 2025 and is expected to grow at a CAGR of 5.4% through 2033. The region experienced gradual growth supported by increasing investments in food processing and retail sectors. Flexible packaging adoption increased due to its cost efficiency and suitability for hot climates.

Saudi Arabia led the market, driven by government initiatives to diversify the economy and expand the food and beverage industry. The country’s focus on modern retail infrastructure supported demand for flexible packaging.

Latin America

Latin America held 7.2% of the global market share in 2025 and is projected to grow at a CAGR of 5.0% during 2025–2033. The region showed moderate growth due to rising urbanization and demand for packaged goods. Flexible packaging adoption increased in response to cost-effective packaging solutions.

Brazil dominated the regional market, supported by a strong agricultural base and expanding food processing industry. The country’s growing retail sector contributed to increased demand for flexible packaging solutions.

Competitive Landscape

The Europe Flexible Packaging Market is moderately consolidated, with several global and regional players competing on innovation, sustainability, and cost efficiency. Key companies are focusing on developing recyclable materials and expanding production capacities to meet evolving demand.

Amcor Plc is a leading player in the market, known for its strong portfolio of sustainable packaging solutions. The company has recently introduced advanced recyclable flexible packaging products aimed at reducing environmental impact. Other major players are investing in digital printing technologies and strategic partnerships to strengthen their market presence.

Competition is driven by product innovation, regulatory compliance, and the ability to offer customized packaging solutions. Companies are also focusing on mergers and acquisitions to expand their geographic footprint and enhance technological capabilities.

Key Players in the Europe Flexible Packaging Market

- Amcor Plc

- Mondi Group

- Sealed Air Corporation

- Huhtamaki Oyj

- Coveris Holdings S.A.

- Clondalkin Group

- Berry Global Inc.

- DS Smith Plc

- Uflex Ltd.

- Sonoco Products Company

- ProAmpac LLC

- Bischof + Klein SE & Co. KG

- Wipak Group

- Guala Pack S.p.A.