Electronic Packaging Market Size and Growth

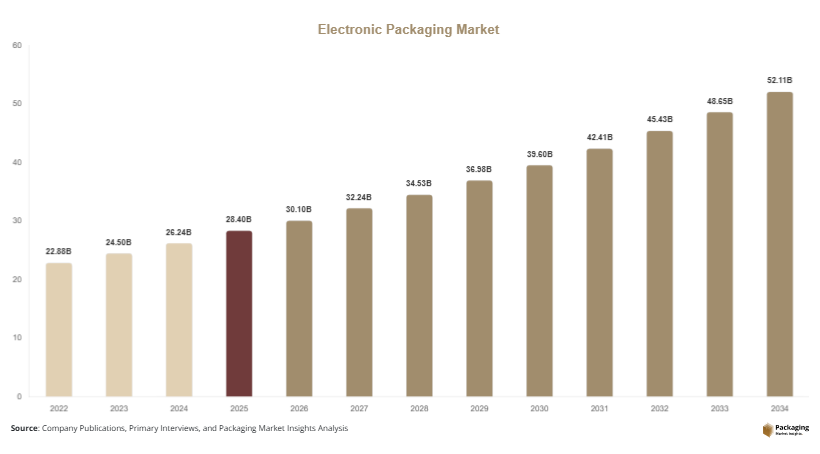

The global electronic packaging market size is estimated at USD 28.4 billion in 2025, and it is projected to reach USD 30.1 billion in 2026. By 2034, the market is expected to reach approximately USD 52.7 billion, registering a CAGR of 7.1% during 2025–2034. Growth is strongly driven by increasing demand for miniaturized electronic components, high-performance computing devices, and advanced packaging solutions that enhance thermal management and electrical performance. The electronic packaging market is witnessing steady expansion due to the rapid growth of semiconductor manufacturing, consumer electronics production, and advanced computing technologies.

One of the major growth factors is the expansion of semiconductor manufacturing capacity globally. Countries such as the United States, China, South Korea, and Taiwan are heavily investing in chip fabrication plants, increasing the demand for advanced packaging materials such as substrate-based packaging, wafer-level packaging, and system-in-package (SiP) technologies. Another key driver is the rapid adoption of consumer electronics including smartphones, laptops, wearables, and smart home devices. These products require compact, durable, and heat-resistant packaging solutions to ensure long-term reliability and performance.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Wafer-level packaging led the type segment with a 31.6% share.

- Plastic-based electronic packaging dominated with a 52.3% share.

- Consumer electronics led the application segment with 45.2% share.

- The US remained the dominant country with a market size of USD 6.2 billion in 2025 and USD 6.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Miniaturization and Advanced Semiconductor Packaging

A major trend shaping the electronic packaging market is the increasing miniaturization of semiconductor devices. As consumer electronics and computing devices become smaller yet more powerful, manufacturers are adopting advanced packaging technologies such as wafer-level packaging, chip-scale packaging, and system-in-package (SiP). These technologies allow multiple chips to be integrated into a single compact module, improving performance while reducing size. For example, smartphones now use highly integrated chips that combine processing, memory, and connectivity functions in one package. This trend is expected to accelerate further with the growth of wearable devices and IoT applications, where space constraints are critical.

Integration of High-Performance Thermal Management Solutions

Another key trend is the growing focus on thermal management in electronic packaging. As semiconductor devices become more powerful, heat dissipation has become a major challenge. Manufacturers are adopting advanced thermal interface materials, heat spreaders, and ceramic-based packaging solutions to improve heat control. For instance, high-performance computing systems used in AI data centers require advanced cooling solutions integrated into packaging structures. This trend is expected to play a critical role in enabling next-generation electronics, especially in AI, 5G infrastructure, and electric vehicles.

Market Drivers

Rapid Growth of Semiconductor Manufacturing

The expansion of semiconductor manufacturing facilities worldwide is a key driver of the electronic packaging market. Governments and private companies are investing heavily in chip production to reduce dependency on imports and strengthen supply chain resilience. This has led to increased demand for advanced packaging materials and technologies. For example, large-scale semiconductor fabs in the United States and Taiwan require sophisticated packaging solutions for high-performance chips used in computing and communication systems. As chip complexity increases, the need for advanced packaging continues to rise.

Rising Demand for Consumer Electronics and Smart Devices

The growing adoption of consumer electronics is another major driver. Devices such as smartphones, tablets, smartwatches, and smart home systems require compact and efficient electronic packaging solutions. These devices rely on miniaturized components that can deliver high performance in limited space. For instance, wearable fitness trackers use advanced packaging to integrate sensors, processors, and connectivity modules into small devices. This increasing demand for smart and connected devices continues to fuel market growth.

Market Restraint

High Cost of Advanced Packaging Technologies

One of the primary restraints in the electronic packaging market is the high cost associated with advanced packaging technologies. Techniques such as 3D packaging, wafer-level packaging, and heterogeneous integration require expensive materials and complex manufacturing processes. This increases production costs, making it challenging for smaller manufacturers to adopt these technologies. For example, advanced semiconductor packaging used in AI chips and high-performance computing systems requires significant investment in precision equipment and cleanroom environments. Additionally, supply chain disruptions and raw material price volatility further increase cost pressures, limiting widespread adoption in cost-sensitive applications.

Market Opportunities

Expansion of Electric Vehicle Electronics

The rapid growth of electric vehicles presents a significant opportunity for the electronic packaging market. EVs rely heavily on advanced electronic systems for battery management, power control, and autonomous driving features. These systems require high-performance packaging solutions that can withstand extreme temperatures and vibrations. For example, automotive semiconductor modules use robust packaging to ensure reliability in harsh driving conditions. As EV adoption increases globally, demand for advanced electronic packaging in automotive applications is expected to grow significantly.

Growth of AI and Data Center Infrastructure

The expansion of artificial intelligence and data center infrastructure is creating new opportunities for electronic packaging solutions. AI processors and high-performance computing systems require advanced packaging technologies to handle high data processing speeds and heat generation. For instance, data centers use specialized semiconductor packaging to improve energy efficiency and processing performance. As AI adoption accelerates across industries such as healthcare, finance, and manufacturing, demand for advanced packaging solutions is expected to increase substantially.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.4 Billion |

| Market Size in 2026 | USD 30.1 Billion |

| Market Size in 2034 | USD 52.7 Billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Wafer-level packaging dominated the market in 2024 with a 32.1% share due to its ability to enable compact, high-performance semiconductor integration. It is widely used in smartphones, processors, and advanced computing systems. This technology allows chips to be packaged at wafer scale, reducing size and improving efficiency. For example, high-end mobile processors use wafer-level packaging to integrate multiple functions into a single chip package.

3D packaging is the fastest-growing subsegment with a CAGR of 7.8%. It enables vertical stacking of semiconductor layers, improving performance and reducing latency. Growth is driven by AI, high-performance computing, and advanced data center applications. Future adoption is expected to increase as demand for high-density computing continues to rise.

By Material

Plastic-based packaging dominated with a 51.9% share in 2024 due to its cost efficiency and versatility in semiconductor protection. It is widely used in integrated circuits and consumer electronics.

Ceramic packaging is the fastest-growing segment with a CAGR of 6.4%, driven by its superior thermal stability and electrical insulation properties. It is increasingly used in high-power applications such as automotive electronics and aerospace systems.

By End-Use

Consumer electronics dominated the market in 2024 with a 45.2% share due to high demand for smartphones, laptops, and wearable devices. These products require compact and efficient packaging solutions.

Automotive electronics is the fastest-growing segment with a CAGR of 7.3%, driven by electric vehicles and autonomous driving systems requiring advanced semiconductor integration.

Electronic Packaging Market Segmentations

By Product Type

- Wafer-Level Packaging

- System-in-Package (SiP)

- 3D Packaging

- Chip-Scale Packaging

By Material

- Plastic Packaging

- Ceramic Packaging

- Metal Packaging

- Hybrid Materials

By Application / End-Use

- Consumer Electronics

- Automotive Electronics

- Industrial Electronics

- Telecommunications

Regional Analysis

North America

North America accounted for approximately 29.1% of the market share in 2025 and is projected to grow at a CAGR of 6.8%. The region benefits from strong semiconductor R&D capabilities and high adoption of advanced electronics. Growth is supported by investments in chip manufacturing and AI infrastructure development.

The United States dominates the region due to its leadership in semiconductor innovation. A key growth driver is the expansion of domestic chip fabrication plants aimed at strengthening supply chain independence and reducing reliance on imports.

Europe

Europe held a 23.4% share in 2025 and is expected to grow at a CAGR of 6.5%. The region is focused on automotive electronics and industrial automation. Demand for advanced packaging is increasing in electric mobility and smart manufacturing applications.

Germany leads the region due to its strong automotive industry. A key driver is the increasing integration of semiconductor systems in electric vehicles and autonomous driving technologies.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025 and is projected to grow at a CAGR of 7.6%. The region is a global hub for semiconductor manufacturing and consumer electronics production. Strong industrial ecosystems in China, Taiwan, South Korea, and Japan support market growth.

China is the dominant country due to its large electronics manufacturing base. A key driver is the expansion of semiconductor fabrication facilities supporting domestic chip production and export-oriented electronics manufacturing.

Middle East & Africa

The region accounted for 4.8% of the market in 2025 and is projected to grow at a CAGR of 6.3%. Growth is supported by increasing investments in digital infrastructure and telecommunications.

The UAE leads the region due to smart city development initiatives. A key driver is the adoption of advanced communication systems requiring semiconductor-based electronic packaging solutions.

Latin America

Latin America held a 5.3% share in 2025 and is expected to grow at the fastest CAGR of 7.0%. Growth is driven by increasing electronics imports and industrial digitalization.

Brazil dominates the region due to its growing consumer electronics market. A key driver is the expansion of telecom infrastructure and digital connectivity projects.

Competitive Landscape

The electronic packaging market is highly competitive, with major players focusing on miniaturization, thermal efficiency, and advanced semiconductor integration. Amkor Technology Inc. is a leading player due to its strong global semiconductor packaging capabilities. The company focuses on advanced system-in-package and wafer-level packaging technologies.

Other major players include ASE Technology Holding, Intel Corporation, Samsung Electronics, TSMC, and JCET Group. These companies are investing heavily in R&D to develop next-generation packaging technologies for AI, 5G, and automotive applications.

Key Players List

- Amkor Technology Inc.

- ASE Technology Holding Co. Ltd.

- Intel Corporation

- Samsung Electronics Co. Ltd.

- Taiwan Semiconductor Manufacturing Company (TSMC)

- JCET Group Co. Ltd.

- Infineon Technologies AG

- STMicroelectronics

- Texas Instruments Inc.

- Qualcomm Inc.

- Sony Semiconductor Solutions

- Renesas Electronics Corporation

- NXP Semiconductors

- Analog Devices Inc.

- Broadcom Inc.