Europe Pharmaceutical Packaging Market Size and Growth

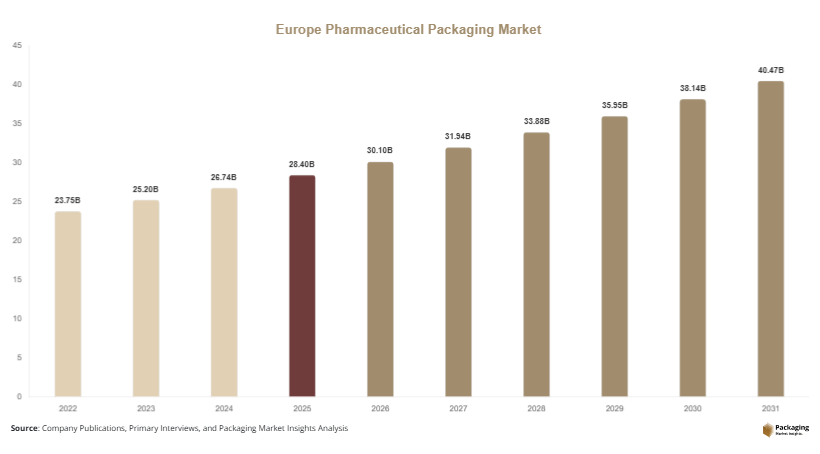

The Europe Pharmaceutical Packaging Market size was valued at approximately USD 28.4 billion in 2025 and is projected to reach USD 39.7 billion by 2030, expanding at a CAGR of 6.1% during 2025–2031. The market has been steadily evolving due to increasing pharmaceutical production, rising demand for biologics, and stricter regulatory requirements for drug safety and traceability.

A major global factor supporting the growth of the Europe Pharmaceutical Packaging Market is the expansion of the pharmaceutical manufacturing sector, driven by increasing healthcare spending and a growing aging population. This has led to higher consumption of prescription drugs, over-the-counter medications, and specialty biologics, thereby increasing the demand for advanced and compliant packaging solutions across the region.

Pharmaceutical packaging plays a crucial role in ensuring product integrity, patient safety, and regulatory compliance. Innovations such as smart packaging, anti-counterfeiting technologies, and sustainable materials are further transforming the market landscape. Additionally, the shift toward personalized medicine and home-based care has increased the need for flexible, user-friendly packaging formats.

Key Highlights:

- Europe accounted for 31.2% market share in 2025, while Asia Pacific is projected to grow at the fastest CAGR of 7.4%

- By product type, primary packaging dominated with 58.6% share, while flexible packaging is projected to grow at a CAGR of 7.1%

- By material, plastics led with 49.3% share, whereas biodegradable materials are expected to grow at 8.2% CAGR

- Germany remained the dominant country with a market size of USD 6.2 billion in 2025, expected to reach USD 6.6 billion in 2026

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Packaging Solutions

Sustainability has emerged as a defining trend in the Europe Pharmaceutical Packaging Market. Pharmaceutical companies are increasingly shifting toward recyclable, biodegradable, and low-carbon packaging materials to comply with environmental regulations and reduce their ecological footprint. Paper-based blister packs, recyclable polymers, and reduced-plastic packaging formats are gaining traction. This trend is further supported by European Union directives focused on circular economy practices, encouraging manufacturers to innovate in eco-friendly packaging design.

Integration of Smart and Anti-Counterfeiting Technologies

The integration of smart packaging technologies is reshaping the market. Features such as QR codes, RFID tags, and tamper-evident seals are being widely adopted to enhance traceability and ensure product authenticity. These technologies help combat counterfeit drugs, a growing concern across Europe. Additionally, digital labeling solutions improve patient engagement by providing dosage instructions and real-time product information, thereby improving compliance and safety.

Market Drivers

Rising Demand for Biologics and Specialty Drugs

The increasing production and consumption of biologics and specialty pharmaceuticals are significantly driving the Europe Pharmaceutical Packaging Market growth. These drugs require advanced packaging formats such as prefilled syringes, vials, and temperature-sensitive containers to maintain stability and efficacy. As biologics continue to gain prominence in treating chronic diseases, the demand for high-performance packaging solutions is expected to rise steadily.

Stringent Regulatory Framework in Europe

Strict regulatory requirements regarding drug safety, labeling, and traceability are another key growth driver. Regulations mandate tamper-evident packaging, serialization, and track-and-trace systems to ensure patient safety. Compliance with these standards compels pharmaceutical companies to invest in innovative packaging technologies, thereby boosting the market. The emphasis on child-resistant and senior-friendly packaging further supports demand for specialized solutions.

Market Restraint

High Cost of Advanced Packaging Solutions

One of the primary challenges in the Europe Pharmaceutical Packaging Market is the high cost associated with advanced packaging technologies. Smart packaging systems, sustainable materials, and compliance-driven innovations often require significant investment in research, development, and manufacturing processes.

Small and medium-sized pharmaceutical companies may face financial constraints in adopting these advanced solutions, limiting their market participation. Additionally, fluctuations in raw material prices, particularly for specialized polymers and biodegradable materials, further increase overall packaging costs. This can lead to pricing pressures and reduced profit margins for manufacturers.

Despite these challenges, companies are exploring cost optimization strategies such as automation and material substitution. However, the balance between cost efficiency and regulatory compliance remains a critical concern in the market.

Market Opportunities

Growth of Home Healthcare and Self-Administration

The increasing shift toward home healthcare and self-administration of drugs presents significant opportunities for the Europe Pharmaceutical Packaging Market. Patients prefer convenient and easy-to-use packaging formats such as prefilled syringes, autoinjectors, and blister packs. This trend is expected to drive demand for ergonomic and patient-friendly packaging designs.

Expansion of Contract Packaging Services

The rise of contract packaging organizations (CPOs) offers new growth avenues for the market. Pharmaceutical companies are increasingly outsourcing packaging operations to specialized service providers to reduce costs and improve efficiency. This trend enables packaging firms to expand their capabilities and adopt advanced technologies, thereby enhancing their market presence.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.4 Billion |

| Market Size in 2026 | USD 30.1 Billion |

| Market Size in 2031 | USD 42.1 Billion |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

Primary packaging dominated the Europe Pharmaceutical Packaging Market with a 58.6% share in 2024. This segment includes bottles, vials, ampoules, and blister packs that directly come into contact with the drug. The dominance is attributed to the critical role of primary packaging in maintaining drug stability and preventing contamination.

Flexible packaging is expected to be the fastest-growing subsegment, projected to grow at a CAGR of 7.1%. The growth is driven by its lightweight nature, cost efficiency, and increasing use in unit-dose packaging. Flexible formats also offer improved patient convenience and reduced material usage.

By Material

Plastic materials held the largest share of 49.3% in 2024, owing to their versatility, durability, and cost-effectiveness. Plastics are widely used in bottles, blister packs, and closures, making them a preferred choice for pharmaceutical packaging.

Biodegradable materials are projected to grow at a CAGR of 8.2%, driven by sustainability initiatives and regulatory pressure. These materials offer eco-friendly alternatives and are gaining acceptance among pharmaceutical companies aiming to reduce environmental impact.

By Packaging Type

Primary packaging remained dominant with a significant share due to its essential function in drug protection. Secondary packaging, including cartons and labels, also contributed notably to the market.

Tertiary packaging is expected to grow steadily, supported by increasing logistics and distribution requirements. The rise of e-commerce in pharmaceuticals is further driving demand for durable and efficient tertiary packaging solutions.

By Drug Delivery Mode

Oral drug delivery packaging dominated the market with a 45.7% share in 2024, driven by the widespread use of tablets and capsules. Blister packs and bottles are commonly used formats in this segment.

Injectable packaging is projected to grow at a CAGR of 7.6%, fueled by the increasing use of biologics and vaccines. The demand for prefilled syringes and advanced injectable packaging formats is expected to rise significantly.

By End User

Pharmaceutical manufacturing companies accounted for the largest share of 62.4% in 2024, as they require large-scale packaging solutions for drug production.

Contract packaging organizations are expected to grow at a CAGR of 7.3%, driven by outsourcing trends and the need for cost efficiency. These organizations provide specialized services, enabling pharmaceutical companies to focus on core operations.

Europe Pharmaceutical Packaging Market Segmentations

By Product Type

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

By Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

- Biodegradable Materials

- By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Drug Delivery Mode

- Oral

- Injectable

- Topical

- Inhalation

By End User

- Pharmaceutical Companies

- Contract Packaging Organizations

Regional Analysis

North America

North America accounted for approximately 27.8% of the Europe Pharmaceutical Packaging Market share in 2025 in terms of global comparison and is expected to grow at a CAGR of 5.8% during 2025–2033. The region's growth is attributed to high healthcare expenditure, advanced pharmaceutical manufacturing infrastructure, and strong adoption of innovative packaging technologies.

The United States dominated the region due to its well-established pharmaceutical industry and high demand for biologics. The presence of major pharmaceutical companies and continuous investment in research and development have driven the demand for advanced packaging solutions.

Europe

Europe held the largest share of 31.2% in 2025 and is projected to grow at a CAGR of 6.1% through 2033. The region benefits from a robust regulatory framework and strong pharmaceutical manufacturing base. Increasing demand for sustainable and compliant packaging solutions is driving market growth.

Germany emerged as the dominant country, driven by its strong pharmaceutical production capabilities and focus on innovation. The country's emphasis on high-quality packaging standards and export-oriented pharmaceutical industry has significantly contributed to market expansion.

Asia Pacific

Asia Pacific captured 24.5% market share in 2025 and is expected to grow at the fastest CAGR of 7.4% during 2025–2033. Rapid industrialization, expanding healthcare infrastructure, and increasing pharmaceutical production are key growth factors.

China led the region due to its large-scale pharmaceutical manufacturing and cost-effective production capabilities. The growing demand for generic drugs and increasing investments in healthcare infrastructure are further supporting market growth.

Middle East & Africa

The Middle East & Africa accounted for 8.6% share in 2025 and is anticipated to grow at a CAGR of 5.2%. The region's growth is driven by improving healthcare systems and increasing pharmaceutical imports.

Saudi Arabia dominated the region, supported by government initiatives to develop the healthcare sector and reduce dependency on imports. Investments in local pharmaceutical manufacturing have boosted demand for packaging solutions.

Latin America

Latin America held 7.9% market share in 2025 and is expected to grow at a CAGR of 5.5%. The region is witnessing steady growth due to rising healthcare awareness and pharmaceutical consumption.

Brazil emerged as the leading country, driven by its expanding pharmaceutical industry and increasing demand for affordable medicines. Government support for healthcare development is further contributing to market growth.

Competitive Landscape

The Europe Pharmaceutical Packaging Market is moderately fragmented, with the presence of several global and regional players focusing on innovation and sustainability. Companies are investing in advanced materials, smart packaging technologies, and strategic collaborations to strengthen their market position.

Amcor Plc is a leading player in the market, known for its extensive portfolio of sustainable packaging solutions. The company recently introduced recyclable pharmaceutical packaging formats to align with environmental regulations.

Other key players include Gerresheimer AG, Schott AG, West Pharmaceutical Services, and Berry Global Inc. These companies are actively expanding their production capacities and investing in research and development to meet evolving market demands.

Key Players in the Europe Pharmaceutical Packaging Market

- Amcor Plc

- Gerresheimer AG

- Schott AG

- West Pharmaceutical Services Inc.

- Berry Global Inc.

- AptarGroup Inc.

- Bormioli Pharma

- SGD Pharma

- Ardagh Group

- UFlex Ltd.

- Constantia Flexibles

- Nipro Corporation

- WestRock Company

- Mondi Group

- Sonoco Products Company