Edible Oil Packaging Market Size and Growth

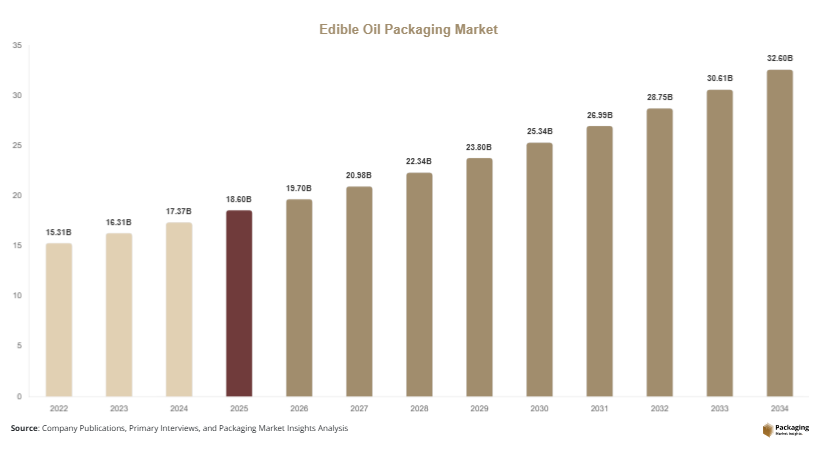

The edible oil packaging market size was valued at approximately USD 18.6 billion in 2025 and is projected to reach USD 19.7 billion in 2026. The market is forecasted to grow to nearly USD 34.8 billion by 2034, expanding at a CAGR of 6.5% during 2025–2034. Increasing household consumption of sunflower oil, soybean oil, olive oil, palm oil, and blended edible oils continues to support packaging demand worldwide. Growth in foodservice industries and ready-to-cook food products is also accelerating the adoption of advanced oil packaging solutions.

One of the major growth drivers is the rising shift toward packaged edible oils in urban markets. Consumers are increasingly preferring branded oils packaged in tamper-evident containers due to growing awareness regarding food hygiene and product authenticity. Another important factor is the expansion of modern retail infrastructure, including supermarkets, hypermarkets, and e-commerce grocery platforms, which require durable and visually appealing packaging formats. In addition, sustainability initiatives are encouraging manufacturers to introduce recyclable PET bottles, refill pouches, and lightweight packaging materials to reduce environmental impact.

Key Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.9%.

- PET bottles led the type segment with a 41.6% share.

- Plastic packaging materials dominated with a 57.4% share.

- Household cooking oil applications led the end-use segment with 48.3% share.

- The US remained the dominant country with a market size of USD 3.9 billion in 2025 and USD 4.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Lightweight Packaging

One of the major trends shaping the edible oil packaging market is the increasing shift toward sustainable and lightweight packaging materials. Packaging manufacturers are reducing the use of heavy plastic containers and introducing recyclable PET bottles, refill pouches, and bio-based packaging materials to reduce transportation costs and environmental impact. Edible oil producers are increasingly promoting refill pouch systems that allow consumers to reuse larger bottles at home. For example, several cooking oil brands in India and Southeast Asia are launching lightweight flexible pouch formats to improve affordability and reduce plastic usage. This trend is expected to strengthen further as governments introduce stricter packaging waste regulations and consumers increasingly prioritize environmentally responsible packaging solutions.

Growing Demand for Premium and Smart Packaging Solutions

Another important trend is the rising use of premium packaging designs and smart labeling technologies for edible oils. High-quality olive oil, avocado oil, and organic cooking oils are increasingly packaged in UV-protected glass bottles and aesthetically designed containers that improve shelf visibility and brand identity. Companies are also integrating QR codes and traceability labels that provide consumers with information regarding oil sourcing, production quality, and expiration tracking. For instance, premium olive oil producers in Europe are using dark glass packaging with digital authentication features to improve product differentiation and consumer trust. Future growth in smart packaging technologies is expected to improve transparency, product safety, and customer engagement across the edible oil sector.

Market Drivers

Increasing Consumption of Packaged Cooking Oils

The growing preference for packaged cooking oils is a major factor driving the edible oil packaging market. Consumers are increasingly choosing branded and sealed edible oils because of rising awareness regarding food hygiene, product purity, and adulteration risks. Urban households and commercial kitchens are shifting away from loose oil purchases and adopting packaged alternatives that offer better quality assurance and convenience. This trend is especially strong in developing economies where food safety awareness is expanding rapidly. For example, edible oil producers in India and China are increasing production of tamper-evident PET bottles and pouch packaging formats to meet growing retail demand. The increasing penetration of supermarkets and online grocery platforms is also supporting packaged oil consumption globally.

Expansion of Foodservice and Processed Food Industries

The expansion of restaurants, hotels, catering services, and processed food manufacturing is another major market driver. Commercial food operators require large-capacity and durable packaging solutions that improve storage, transportation, and dispensing efficiency. Bulk oil packaging formats such as drums, jerry cans, and industrial containers are witnessing strong demand from foodservice businesses and industrial food processors. In addition, growing consumption of fried and ready-to-cook foods is increasing edible oil usage across food manufacturing operations. Countries such as the United States, Brazil, and Indonesia are witnessing rising investments in food processing infrastructure, creating substantial opportunities for industrial edible oil packaging suppliers.

Market Restraint

Fluctuating Raw Material Prices and Recycling Challenges

One of the major restraints affecting the edible oil packaging market is the volatility in raw material prices and challenges associated with plastic recycling infrastructure. Packaging materials such as PET, HDPE, polypropylene, and aluminum are heavily influenced by fluctuations in petroleum and commodity markets. Rising material costs can increase overall packaging expenses for edible oil manufacturers and reduce profit margins. In addition, recycling systems for flexible multilayer pouches remain underdeveloped in several countries, limiting the sustainability potential of certain packaging formats. For example, many low-cost edible oil pouches used in developing markets are difficult to recycle due to mixed-material structures. Regulatory pressure regarding single-use plastics is also creating compliance challenges for packaging producers. Smaller manufacturers may struggle to adopt advanced recyclable packaging solutions because of higher production and investment costs. These factors may limit packaging innovation and affect market growth in price-sensitive regions.

Market Opportunities

Expansion of Refill Pouch Packaging in Emerging Economies

The growing popularity of refill pouch systems presents a major opportunity for the edible oil packaging market. Consumers in emerging economies increasingly prefer refill pouches because they are affordable, lightweight, and easy to transport. Refill systems also reduce plastic consumption and support sustainability initiatives. Packaging companies are developing durable multilayer flexible pouches with anti-leakage dispensing systems for household edible oil applications. Countries such as India, Indonesia, and the Philippines are witnessing rapid growth in refill pouch demand due to rising urbanization and middle-class expansion. Future opportunities are expected to emerge from recyclable pouch innovations and smart dispensing technologies designed for household and commercial oil usage.

Growth of Premium Organic and Specialty Oil Packaging

The increasing demand for organic and specialty oils is creating strong opportunities for premium packaging solutions. Consumers are purchasing olive oil, avocado oil, sesame oil, and cold-pressed oils packaged in glass bottles and high-end containers that enhance product presentation and quality perception. Packaging manufacturers are introducing UV-resistant coatings, decorative labeling, and anti-counterfeit packaging features for premium edible oil brands. In Europe and North America, organic oil producers are investing in sustainable glass and recyclable packaging formats to strengthen premium positioning. Rising consumer spending on health-focused cooking oils is expected to support long-term demand for advanced specialty oil packaging solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.7 Billion |

| Market Size in 2034 | USD 34.8 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

PET bottles dominated the market in 2024 with approximately 41.6% share due to their durability, lightweight structure, and cost efficiency. These bottles are widely used for sunflower oil, soybean oil, palm oil, and blended edible oils because they offer strong moisture resistance and convenient handling. Manufacturers increasingly prefer PET bottles because they support transparent product visibility and are compatible with automated filling systems. Retail edible oil brands in Asia Pacific and North America commonly use ergonomic PET bottles with anti-leakage caps and easy-pour dispensing systems. In addition, PET bottles are easier to transport than glass packaging, reducing logistics costs across large-scale retail distribution networks. Strong consumer familiarity and recyclability advantages continue to support segment dominance worldwide.

Flexible pouch packaging is expected to emerge as the fastest-growing type segment, registering a CAGR of 7.1% during the forecast period. Pouches are gaining popularity because they require less packaging material and significantly reduce transportation costs. Consumers in emerging economies increasingly prefer refill pouches for affordability and convenience. Edible oil manufacturers are introducing multilayer pouch packaging with improved puncture resistance and leak protection. Countries such as India, Indonesia, and Brazil are witnessing rapid adoption of stand-up and refill pouch systems for household cooking oils. In addition, advancements in recyclable flexible films are improving the sustainability profile of pouch packaging. Future demand is expected to remain strong due to increasing urbanization and growing preference for low-cost packaging formats.

By Material

Plastic packaging materials dominated the market in 2024 with a market share of approximately 57.4%. Materials such as PET, HDPE, and polypropylene are widely used because they offer durability, low production costs, and strong barrier protection against moisture and contamination. Plastic containers are commonly used for retail edible oil packaging due to their lightweight structure and compatibility with large-scale manufacturing operations. Packaging companies continue to improve plastic bottle designs through ergonomic handles, anti-slip surfaces, and advanced dispensing caps. In addition, plastic materials provide flexibility for various packaging sizes ranging from small household bottles to industrial bulk containers. Strong demand for affordable and efficient edible oil packaging continues to support segment leadership globally.

Recyclable paper-based packaging is projected to be the fastest-growing material segment with a CAGR of 6.8% during the forecast period. Sustainability regulations and consumer preference for environmentally responsible packaging are encouraging oil producers to explore fiber-based cartons and paper-integrated packaging formats. Packaging manufacturers are investing in moisture-resistant paper coatings and hybrid paper-plastic systems to improve durability for edible oil applications. European and North American brands are increasingly introducing paperboard outer packaging for premium oils and gift-oriented packaging formats. In addition, retailers are supporting sustainable packaging initiatives to reduce overall plastic waste. Continued innovation in barrier coating technologies is expected to improve the commercial viability of recyclable paper-based edible oil packaging.

By End-Use

Household cooking oil applications dominated the market in 2024 with approximately 48.3% share due to strong residential demand for packaged sunflower oil, soybean oil, olive oil, and blended oils. Consumers increasingly prefer branded cooking oils packaged in tamper-proof and easy-to-store containers. Retail supermarkets, convenience stores, and online grocery platforms are expanding sales of packaged household oils in both developed and emerging economies. Packaging manufacturers are developing ergonomic bottles, refill pouches, and leak-resistant closures that improve convenience for daily kitchen use. In countries such as India, China, and Brazil, rising urbanization and growing middle-class populations continue to drive packaged cooking oil demand. These factors are supporting strong long-term growth for household edible oil packaging applications.

Foodservice packaging is expected to register the fastest growth with a CAGR of 7.0% during the forecast period. Restaurants, hotels, catering businesses, and food processors require large-capacity oil packaging formats that improve handling efficiency and reduce operational waste. Industrial containers, jerry cans, and bulk packaging solutions are witnessing increasing demand across commercial food operations. Packaging companies are introducing durable high-capacity containers with controlled dispensing systems to reduce spillage and improve workplace safety. Rapid expansion of quick-service restaurants and cloud kitchens in Asia Pacific and the Middle East is also supporting segment growth. Continued growth in commercial food production and hospitality industries is expected to strengthen long-term demand for foodservice edible oil packaging solutions.

Edible Oil Packaging Market Segmentations

By Type

- PET Bottles

- Flexible Pouches

- Glass Bottles

- Metal Cans

- Bulk Containers

By Material

- Plastic Packaging

- Paper-Based Packaging

- Glass Packaging

- Metal Packaging

By End-User

- Household Cooking Oils

- Foodservice Packaging

- Industrial Food Processing

- Export Packaging

Regional Analysis

North America

North America accounted for approximately 24.8% of the global market share in 2025 and is expected to grow at a CAGR of 5.9% during the forecast period. The region benefits from strong packaged food demand, increasing health-conscious cooking habits, and rising consumption of premium edible oils such as olive oil and avocado oil. Consumers in the United States and Canada increasingly prefer branded cooking oils packaged in recyclable and tamper-proof containers. Retail chains and e-commerce grocery platforms are also encouraging manufacturers to adopt lightweight and sustainable packaging formats. Packaging companies across the region are investing in advanced dispensing systems, leak-resistant closures, and recyclable PET bottle technologies to improve convenience and sustainability.

The United States dominates the North American market due to its large packaged food industry and strong retail distribution network. A unique growth factor in the country is the rising demand for premium organic cooking oils packaged in glass bottles and eco-friendly containers. Consumers are increasingly purchasing specialty oils through online grocery channels and premium supermarkets. Foodservice operators are also adopting large-capacity oil packaging systems that improve storage efficiency and reduce operational waste. Growing investments in sustainable packaging technologies and smart labeling systems are expected to support future market growth across the country.

Europe

Europe represented approximately 21.7% market share in 2025 and is projected to expand at a CAGR of 5.7% through 2034. Strong sustainability regulations and rising consumer preference for premium edible oils are major factors supporting regional market growth. Consumers across Italy, Spain, Germany, and France are increasingly purchasing olive oil and organic oils packaged in recyclable glass bottles and paper-based cartons. Packaging manufacturers are developing lightweight containers and refill systems to reduce carbon emissions and material waste. In addition, strict European Union regulations regarding food packaging safety and recycling targets are accelerating innovation in recyclable and reusable edible oil packaging formats.

Italy remains the dominant country in the European market due to its strong olive oil production and export industry. A unique growth driver in Italy is the increasing use of premium packaging designs for extra virgin olive oil products. Producers are investing in dark glass bottles, embossed labels, and traceability technologies to improve export competitiveness and consumer trust. Premium packaging has become increasingly important for differentiating high-quality olive oils in international markets. Rising exports of specialty oils across Europe and North America are expected to strengthen demand for advanced edible oil packaging solutions in Italy.

Asia Pacific

Asia Pacific dominated the global edible oil packaging market with a 39.2% share in 2025 and is forecasted to register a CAGR of 7.0% during the forecast period. The region benefits from high edible oil consumption, rapid urbanization, and increasing adoption of packaged cooking oils in densely populated economies. Countries such as India, China, Indonesia, and Malaysia are witnessing strong demand for packaged sunflower oil, palm oil, soybean oil, and blended oils. Expansion of organized retail and online grocery platforms is increasing the need for durable, affordable, and lightweight packaging solutions. Flexible pouch packaging is particularly popular in Asia Pacific due to lower production costs and easier transportation.

India remains the dominant country in the Asia Pacific market because of its large population and significant edible oil consumption. A unique growth driver in India is the rapid expansion of affordable pouch packaging for household cooking oil applications. Domestic edible oil brands are introducing compact refill packs and value-oriented packaging solutions targeted at middle-income consumers. Government campaigns promoting food safety and packaged product standards are also encouraging the shift toward branded edible oils. In addition, rapid growth in supermarket chains and e-commerce grocery delivery services is increasing demand for secure and leak-resistant packaging formats.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.8% market share in 2025 and is projected to expand at a CAGR of 6.3% through 2034. Rising urban populations, increasing consumption of packaged food products, and expanding foodservice industries are driving edible oil packaging demand across the region. Consumers are increasingly purchasing packaged sunflower oil, palm oil, and blended oils through supermarkets and convenience stores. Packaging suppliers are focusing on durable and heat-resistant packaging formats suitable for hot climate conditions. Bulk edible oil packaging for restaurants, hotels, and catering operations is also witnessing increasing demand due to tourism sector expansion in Gulf countries.

Saudi Arabia dominates the regional market due to growing imports of packaged edible oils and increasing foodservice consumption. A unique growth factor in the country is the rapid expansion of quick-service restaurants and hospitality infrastructure. Foodservice operators require large-capacity packaging solutions that improve storage efficiency and minimize oil contamination risks. In addition, premium cooking oil brands are introducing advanced dispensing caps and ergonomic bottle designs targeted at urban consumers. Continued growth in tourism and hospitality activities is expected to support long-term packaging demand across Saudi Arabia and neighboring Gulf economies.

Latin America

Latin America held nearly 7.5% market share in 2025 and is projected to grow at the fastest CAGR of 6.9% during the forecast period. Increasing consumption of soybean oil, corn oil, and sunflower oil is supporting strong demand for household and industrial edible oil packaging across Brazil, Mexico, and Argentina. Retail expansion and rising packaged food consumption are encouraging edible oil producers to adopt lightweight and cost-effective packaging formats. Flexible pouches and PET bottles are gaining popularity due to affordability and improved transportation efficiency. Packaging manufacturers are also investing in sustainable plastic solutions to meet rising environmental concerns across regional markets.

Brazil remains the dominant country in the Latin American market because of its large soybean oil production and food processing industry. A unique growth driver in Brazil is the increasing export demand for packaged edible oils. Oil producers are adopting export-grade packaging formats with enhanced durability and labeling compliance to support international trade activities. In addition, domestic supermarkets are expanding sales of branded cooking oils packaged in ergonomic and recyclable containers. Rising investment in food processing infrastructure and retail modernization is expected to continue supporting market growth in Brazil.

Competitive Landscape

The global edible oil packaging market is moderately competitive, with leading companies focusing on lightweight packaging technologies, sustainable materials, and advanced dispensing solutions. Packaging manufacturers are investing heavily in recyclable PET bottles, flexible pouch innovations, and leak-resistant closures to improve product safety and operational efficiency. Companies are also expanding production capacities in emerging economies to support rising edible oil consumption and retail distribution growth.

Amcor plc remains one of the leading players in the market due to its extensive flexible and rigid packaging portfolio and strong global presence. Berry Global Inc., Greif Inc., Mondi Group, and Sonoco Products Company are also major participants focusing on sustainable packaging innovations and cost-efficient manufacturing strategies. Many companies are partnering with edible oil producers to develop customized packaging formats optimized for retail, foodservice, and export applications. Recent investments in recyclable flexible packaging and smart labeling technologies are expected to strengthen competitive positioning across the industry.

Key Players List

- Amcor plc

- Berry Global Inc.

- Mondi Group

- Greif Inc.

- Sonoco Products Company

- Silgan Holdings Inc.

- Smurfit Kappa Group

- Huhtamaki Oyj

- ProAmpac LLC

- DS Smith plc

- Constantia Flexibles

- CCL Industries Inc.

- AptarGroup Inc.

- Alpha Packaging

- Uflex Ltd.