Duplex Paper For FMCG Market Size and Growth

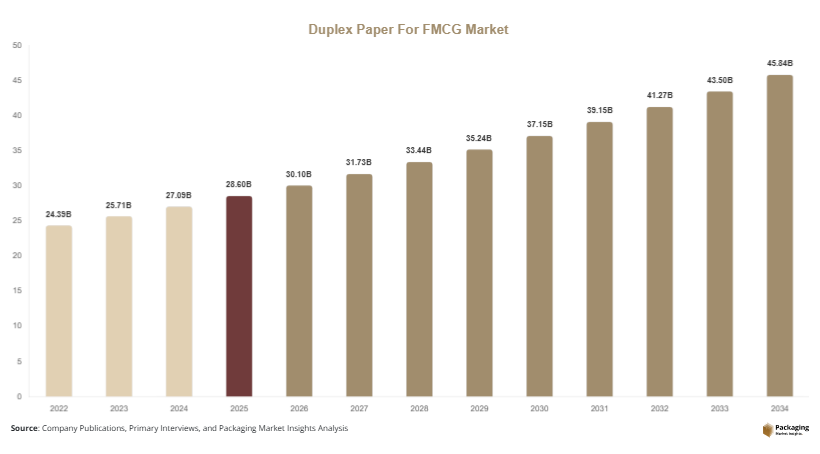

The global duplex paper for FMCG market size is estimated at USD 28.6 billion in 2025 and is expected to reach USD 30.1 billion in 2026. With continuous innovation and expanding application scope, the market is projected to grow to USD 45.7 billion by 2034, registering a CAGR of 5.4% during the forecast period (2025–2034). This growth reflects the ongoing transition from plastic-based packaging to recyclable paper-based alternatives. The duplex paper for FMCG market is experiencing steady expansion due to the increasing preference for sustainable, cost-efficient, and versatile packaging solutions across fast-moving consumer goods industries.

The rising demand for eco-friendly packaging materials remains a key factor driving market expansion. Duplex paper, composed of recycled fibers combined with a top layer of virgin pulp, offers a balance of durability, print quality, and affordability. This makes it highly suitable for packaging FMCG products such as food items, cosmetics, and household goods. In addition, the growth of organized retail and e-commerce sectors has significantly increased the need for protective and visually appealing packaging, further boosting the adoption of duplex paper.

Key Highlights:

- Asia Pacific dominated the market with a 38.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.4%.

- Coated duplex board led the type segment with a 46.7% share, while uncoated variants are expected to grow at a CAGR of 5.9%.

- Food packaging dominated with a 49.2% share, while personal care packaging is forecasted to grow at a CAGR of 6.1%.

- Carton packaging applications led with a 54.8% share, while flexible hybrid packaging is expected to grow at a CAGR of 6.3%.

- China remained the dominant country with a market size of USD 9.6 billion in 2025 and USD 10.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing shift toward sustainable and recyclable packaging

The demand for environmentally responsible packaging solutions is steadily influencing the duplex paper for FMCG market. Consumers are becoming more aware of the environmental impact of plastic waste, prompting FMCG brands to adopt recyclable and biodegradable materials. Duplex paper is widely preferred due to its high recyclability and reduced environmental footprint. Regulatory frameworks across multiple regions are supporting this transition by enforcing stricter guidelines on single-use plastics and promoting sustainable alternatives. In addition, companies are integrating eco-labeling and sustainability messaging into their packaging strategies, which enhances brand perception and drives demand for duplex paper products.

Advancements in coating and high-quality printing technologies

Technological improvements in coating and printing processes are transforming the usability and appeal of duplex paper in FMCG packaging. Modern coating techniques enhance the material’s resistance to moisture, grease, and external damage, allowing it to be used in a wider range of applications. At the same time, high-resolution printing capabilities enable manufacturers to create detailed and visually appealing packaging designs. This is particularly important in competitive retail environments, where packaging plays a crucial role in influencing consumer choices. The rise of digital printing is also enabling shorter production runs and customization, making duplex paper a flexible solution for diverse FMCG requirements.

Market Drivers

Expansion of FMCG consumption and organized retail networks

The growing consumption of FMCG products globally is significantly contributing to the demand for duplex paper packaging. Urbanization, rising disposable incomes, and changing lifestyles are increasing the consumption of packaged goods across food, personal care, and household segments. Organized retail formats such as supermarkets and hypermarkets are expanding rapidly, requiring efficient packaging solutions that ensure product safety and shelf appeal. Additionally, the growth of e-commerce platforms has increased the need for durable secondary packaging, further supporting the demand for duplex paper. This trend is expected to continue as retail infrastructure develops across emerging economies.

Cost-effective and versatile material for diverse packaging needs

Duplex paper offers a cost-efficient alternative to rigid plastics and premium paperboards, making it attractive for FMCG manufacturers seeking to optimize packaging costs. Its layered structure allows for efficient use of raw materials while maintaining strength and print quality. The material is suitable for a wide range of applications, including cartons, boxes, and display packaging. This versatility allows manufacturers to standardize packaging materials across multiple product lines, reducing operational complexity. As companies continue to focus on cost optimization and sustainability, duplex paper is expected to gain further traction in the market.

Market Restraint

Limitations in barrier properties for high-performance applications

One of the key challenges in the duplex paper for FMCG market is the relatively limited barrier performance compared to plastic-based materials. Certain FMCG products, particularly those requiring protection from moisture, oxygen, or grease, may not be adequately supported by standard duplex paper. To address this issue, manufacturers often apply additional coatings or laminations, which can increase production costs and reduce recyclability. This trade-off can limit the adoption of duplex paper in specific applications such as liquid packaging or high-moisture food products. As a result, some manufacturers continue to rely on alternative materials for high-performance packaging requirements.

Market Opportunities

Innovation in eco-friendly coatings and material enhancements

The development of advanced coatings and material technologies presents significant opportunities for the duplex paper for FMCG market. Manufacturers are focusing on creating bio-based and water-resistant coatings that enhance the functionality of duplex paper while maintaining its recyclability. These innovations enable the material to be used in applications that were previously dominated by plastic packaging. Companies investing in research and development can leverage these advancements to expand their product portfolios and capture new market segments. The increasing demand for sustainable packaging solutions is expected to drive continued innovation in this area.

Growth potential across emerging economies

Emerging markets offer strong growth opportunities due to increasing consumption of FMCG products and expanding retail infrastructure. Rapid urbanization and population growth in regions such as Asia Pacific, Latin America, and Africa are driving demand for affordable and efficient packaging solutions. Duplex paper is well-suited to these markets due to its cost-effectiveness and availability. Additionally, improvements in local manufacturing capabilities and supply chain networks are making duplex paper more accessible. Companies that establish a strong presence in these regions can benefit from rising demand and long-term market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.6 Billion |

| Market Size in 2026 | USD 30.1 Billion |

| Market Size in 2034 | USD 45.7 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Coated duplex board accounted for the largest share of 46.7% in 2024, driven by its superior surface quality and printability. This type of board is widely used in FMCG packaging due to its ability to support high-quality graphics and branding elements. The coated surface enhances durability and provides resistance to wear and moisture, making it suitable for packaging food and personal care products. Manufacturers prefer coated duplex board for its aesthetic appeal and functionality in competitive retail environments.

Uncoated duplex board is expected to register the fastest growth at a CAGR of 5.9% during the forecast period. This growth is supported by increasing demand for eco-friendly and cost-effective packaging materials. Uncoated boards are easier to recycle and require fewer chemical treatments, aligning with sustainability goals. Improvements in material processing are also enhancing their strength and usability across various applications.

By Application

Carton packaging dominated the application segment with a 54.8% share in 2024. Duplex paper cartons are widely used for packaging FMCG products due to their structural strength and ease of handling. These cartons provide effective protection during transportation and storage while offering ample space for branding and product information. The demand for carton packaging is further supported by the growth of retail and e-commerce sectors.

Flexible hybrid packaging is projected to grow at a CAGR of 6.3%, driven by the need for lightweight and versatile packaging solutions. This type of packaging combines duplex paper with flexible materials to enhance performance and reduce material usage. The increasing demand for convenience packaging and improved barrier properties is supporting the growth of this segment.

By End-Use

The food & beverage segment held the largest share of 49.2% in 2024, reflecting the high demand for packaging materials in the food industry. Duplex paper is widely used for packaging items such as cereals, snacks, and frozen foods due to its cost-effectiveness and recyclability. The growing demand for packaged and ready-to-eat foods is further driving the adoption of duplex paper in this segment.

The personal care segment is expected to grow at a CAGR of 6.1%, driven by the increasing demand for premium packaging solutions. Duplex paper offers excellent printability and design flexibility, allowing brands to create attractive packaging. The shift toward sustainable packaging in the personal care industry is also supporting the growth of this segment.

Duplex Paper For FMCG Market Segmentations

By Type

- Coated Duplex Board

- Uncoated Duplex Board

By Application

- Carton Packaging

- Flexible Hybrid Packaging

By End-Use

- Food & Beverage

- Personal Care

- Household Products

Regional Analysis

North America

North America held a significant share of the duplex paper for FMCG market, accounting for 21.6% in 2025 and expected to grow at a CAGR of 4.8% through 2034. The region benefits from well-established FMCG industries and a strong focus on sustainable packaging practices. Regulatory initiatives aimed at reducing plastic waste are encouraging manufacturers to adopt paper-based alternatives. Consumer awareness regarding environmental impact is also influencing purchasing behavior, which supports the adoption of duplex paper packaging.

The United States leads the regional market due to its advanced packaging sector and high consumption of FMCG products. A notable growth factor is the increasing adoption of circular economy principles, where companies focus on recycling and reusing materials. This approach is driving innovation in duplex paper manufacturing and enhancing its role in sustainable packaging solutions.

Europe

Europe accounted for 24.3% of the market share in 2025 and is projected to grow at a CAGR of 5.1%. The region is characterized by strict environmental regulations and a strong commitment to sustainability. Policies aimed at reducing single-use plastics are driving the demand for paper-based packaging solutions, including duplex paper. The presence of leading FMCG companies further supports steady market growth.

Germany dominates the European market due to its strong manufacturing base and focus on environmentally responsible practices. A unique growth factor is the integration of renewable energy in paper production processes, which reduces carbon emissions and enhances the sustainability profile of duplex paper products.

Asia Pacific

Asia Pacific emerged as the largest regional market, holding a 38.1% share in 2025 and projected to grow at a CAGR of 6.2%. Rapid urbanization, population growth, and increasing disposable incomes are driving demand for FMCG products and packaging materials. The expansion of e-commerce and retail sectors further supports market growth. The availability of raw materials and cost-efficient production capabilities also contribute to the region’s dominance.

China remains the leading country in the region due to its large manufacturing base and high consumption of packaged goods. Government initiatives to reduce plastic waste are encouraging the adoption of paper-based packaging, creating strong demand for duplex paper solutions.

Middle East & Africa

The Middle East & Africa region accounted for 7.8% of the market in 2025 and is expected to grow at a CAGR of 5.6%. Increasing urbanization and rising demand for packaged goods are driving market expansion. Governments are gradually introducing policies to promote sustainable packaging, which is supporting the adoption of duplex paper.

South Africa plays a key role in the regional market due to its developing retail sector. The expansion of local FMCG manufacturing is a significant growth factor, as it increases demand for cost-effective packaging materials such as duplex paper.

Latin America

Latin America held an 8.2% share in 2025 and is projected to grow at the fastest CAGR of 6.4%. The region’s growth is driven by rising consumer spending and expanding FMCG industries. The adoption of sustainable packaging solutions is gaining momentum as environmental awareness increases.

Brazil dominates the regional market due to its large population and strong FMCG sector. The growth of local recycling industries is a key factor supporting the production and adoption of duplex paper, making it more accessible and affordable for manufacturers.

Competitive Landscape

The duplex paper for FMCG market is characterized by moderate competition, with both global and regional players focusing on innovation and sustainability. Companies are investing in advanced manufacturing technologies and expanding their production capacities to meet rising demand. Strategic partnerships and product development initiatives are common strategies used to strengthen market presence.

International Paper Company remains a key market leader, leveraging its extensive distribution network and product portfolio. The company has recently focused on enhancing its sustainable packaging solutions, including duplex paper products, to align with evolving market requirements. Other players are also prioritizing eco-friendly innovations and cost optimization to remain competitive.

Key Players List

- International Paper Company

- WestRock Company

- Smurfit Kappa Group

- Stora Enso Oyj

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Mondi Group

- Nine Dragons Paper Holdings Limited

- Lee & Man Paper Manufacturing Ltd.

- Sappi Limited

- DS Smith Plc

- Packaging Corporation of America

- UPM-Kymmene Corporation

- Rengo Co., Ltd.

- JK Paper Ltd.