Duplex Paper And Board For FMCG Market Size and Growth

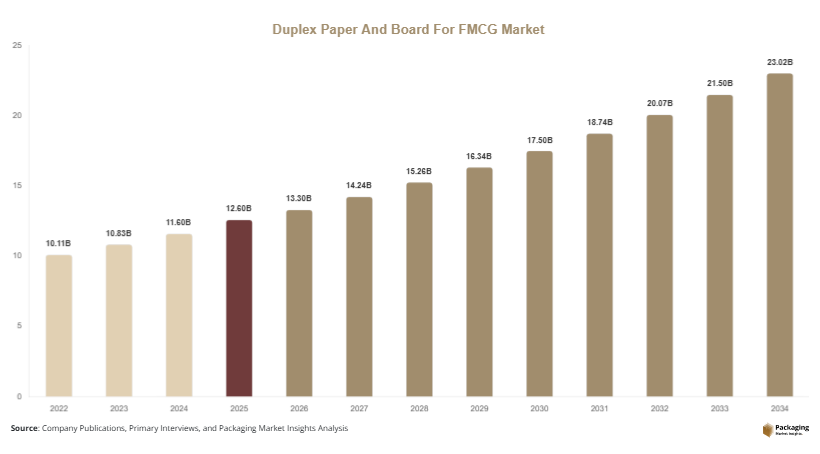

The global duplex paper and board for FMCG market size is estimated at USD 12.6 billion in 2025 and is projected to reach USD 13.3 billion in 2026. By 2034, the market is expected to attain USD 23.8 billion, registering a CAGR of 7.1% from 2025 to 2034. The duplex paper and board for FMCG market is witnessing steady expansion as FMCG manufacturers increasingly shift toward cost-efficient, printable, and recyclable packaging materials. Duplex paper and board are widely used for secondary packaging in food, personal care, household, and retail FMCG products due to their strength, smooth surface, and compatibility with high-quality printing.

One of the primary growth factors is the rising demand for sustainable packaging solutions across FMCG industries. Governments and regulatory bodies are pushing for reduced plastic usage, which is encouraging manufacturers to adopt paper-based alternatives such as duplex boards. Another key driver is the expansion of the FMCG sector, particularly in emerging economies, where urbanization and rising disposable incomes are increasing consumption of packaged goods. Additionally, advancements in coating and surface treatment technologies are improving the printability and barrier properties of duplex boards, making them more suitable for premium FMCG packaging applications.

Key Highlights

- Asia Pacific dominated the market with a 38.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.6%.

- Coated duplex boards led the type segment with a 52.4% share, while uncoated variants are expected to grow at a CAGR of 7.3%.

- Folding cartons dominated with a 55.6% share, while rigid packaging applications are forecasted to grow at a CAGR of 7.8%.

- Food & beverage applications led the segment with 44.2% share, while personal care packaging is expected to grow at a CAGR of 7.5%.

- China remained the dominant country with a market size of USD 3.4 billion in 2025 and USD 3.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing shift toward recyclable and fiber-based packaging materials

The duplex paper and board for FMCG market is strongly influenced by the global transition toward recyclable and fiber-based packaging solutions. FMCG brands are actively reducing their reliance on plastic packaging due to environmental concerns and regulatory pressures. Duplex paper and board offer a sustainable alternative that maintains structural integrity while supporting high-quality printing. Companies are redesigning packaging portfolios to align with circular economy principles, which is increasing demand for recycled fiber-based duplex boards. This trend is particularly strong in Europe and Asia Pacific, where governments are enforcing strict sustainability targets. The adoption of eco-friendly packaging is also driven by consumer preference for environmentally responsible brands, further reinforcing market growth.

Technological advancements in coating and printing capabilities

Another major trend shaping the duplex paper and board for FMCG market is the advancement in coating and printing technologies. Manufacturers are developing improved coating formulations that enhance moisture resistance, durability, and surface smoothness of duplex boards. These improvements enable better ink absorption and sharper printing quality, which is essential for FMCG branding and product differentiation. Digital and flexographic printing technologies are increasingly being integrated with duplex board applications to support short-run customized packaging. This trend is enabling FMCG companies to create visually appealing packaging designs while maintaining cost efficiency. As a result, demand for premium-grade duplex boards is rising across multiple FMCG segments.

Market Drivers

Expansion of FMCG industry and rising packaged goods consumption

The continuous expansion of the FMCG sector is a major driver of the duplex paper and board for FMCG market. Increasing urbanization, population growth, and rising disposable incomes are boosting demand for packaged food, beverages, personal care, and household products. As FMCG companies scale up production, the need for reliable and cost-effective packaging materials such as duplex board increases. Its ability to support high-volume manufacturing and efficient printing makes it suitable for mass-market FMCG applications. Additionally, the growth of organized retail and e-commerce platforms is further increasing demand for secondary packaging materials that ensure product safety during transportation and storage.

Regulatory push for sustainable and plastic-free packaging solutions

Government regulations aimed at reducing plastic waste are significantly driving the adoption of duplex paper and board in FMCG packaging. Many countries are implementing bans or restrictions on single-use plastics, encouraging manufacturers to adopt recyclable alternatives. Duplex board is widely accepted as a sustainable packaging material due to its recyclability and fiber-based composition. FMCG companies are increasingly shifting toward paper-based packaging to comply with environmental regulations and enhance brand reputation. This regulatory environment is accelerating the replacement of plastic packaging with duplex board solutions across multiple product categories.

Market Restraint

Volatility in raw material supply and pricing pressure

The duplex paper and board for FMCG market faces challenges due to fluctuations in raw material availability and pricing. The production of duplex boards depends heavily on paper pulp, which is influenced by forestry output, recycling rates, and global supply chain conditions. Any disruption in pulp supply can lead to price volatility, impacting manufacturing costs. For example, during periods of increased demand for recycled fiber, supply shortages can cause cost escalation for manufacturers. This price instability affects profit margins and creates challenges for FMCG companies that require consistent packaging costs. Additionally, competition for raw materials from other paper-based industries adds further pressure on supply stability.

Market Opportunities

Growth in premium FMCG packaging and brand differentiation strategies

The increasing focus on premium packaging presents significant opportunities for the duplex paper and board for FMCG market. FMCG brands are investing in visually appealing packaging to enhance shelf visibility and consumer engagement. Duplex boards provide a smooth surface suitable for high-resolution printing, embossing, and lamination, making them ideal for premium packaging applications. This is particularly relevant in cosmetics, personal care, and premium food segments, where packaging plays a critical role in brand perception. The demand for customized and aesthetically enhanced packaging is expected to support market expansion.

Expansion of e-commerce and demand for protective secondary packaging

The rapid growth of e-commerce is creating new opportunities for duplex paper and board manufacturers. Online retail requires durable and lightweight packaging materials that can protect products during shipping and handling. Duplex boards are increasingly used in secondary packaging formats such as cartons and boxes for FMCG products sold online. The rise in direct-to-consumer (D2C) brands is further increasing demand for customizable and cost-efficient packaging solutions. As e-commerce penetration continues to expand globally, the need for reliable packaging materials is expected to drive sustained growth in this market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.6 Billion |

| Market Size in 2026 | USD 13.3 Billion |

| Market Size in 2034 | USD 23.8 Billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Coated duplex boards dominated the market in 2024, accounting for approximately 52.4% of the share. These boards are widely used in FMCG packaging due to their superior surface finish, printability, and resistance to moisture. Coated variants are preferred for premium packaging applications, particularly in food, cosmetics, and personal care products. Their ability to support high-quality graphics makes them essential for brand-driven FMCG packaging strategies.

Uncoated duplex boards are expected to grow at the fastest CAGR of 7.3%. These boards are cost-effective and widely used in mass-market FMCG packaging applications. Increasing demand for economical packaging solutions in emerging markets is driving growth in this segment.

By Application

Folding cartons dominated the market in 2024, accounting for 55.6% of the share. These cartons are widely used in FMCG packaging due to their structural strength and versatility. They are extensively used for food, pharmaceuticals, and household products.

Rigid packaging applications are expected to grow at the fastest CAGR of 7.8%. The increasing demand for premium packaging and enhanced product protection is driving this segment.

By End-Use

Food & beverage applications dominated the market in 2024, accounting for 44.2% of the share. This segment relies heavily on duplex boards for packaging dry foods, frozen products, and beverages.

Personal care packaging is expected to grow at the fastest CAGR of 7.5%. Rising demand for branded cosmetics and hygiene products is driving this segment.

Duplex Paper And Board For FMCG Market Segmentations

By Type

- Coated Duplex Board

- Uncoated Duplex Board

By Application

- Folding Cartons

- Rigid Packaging

By End-User

- Food & Beverage

- Personal Care

- Household Products

- Pharmaceuticals

Regional Analysis

North America

North America accounted for a market share of 22.4% in 2025 and is projected to grow at a CAGR of 6.8%. The region benefits from a well-developed FMCG industry and strong demand for sustainable packaging solutions. Increasing environmental regulations are encouraging the adoption of recyclable paper-based materials across multiple product categories.

The United States dominates the regional market due to its large FMCG manufacturing base. A key growth factor is the increasing shift toward eco-friendly packaging in retail and food sectors.

Europe

Europe held a market share of 25.6% in 2025 and is expected to grow at a CAGR of 7.0%. The region has stringent sustainability regulations and strong consumer preference for environmentally friendly packaging.

Germany leads the European market due to its advanced packaging industry. A unique growth factor is the strong adoption of circular economy practices in packaging production.

Asia Pacific

Asia Pacific dominated the market with a 38.1% share in 2025 and is projected to grow at a CAGR of 7.6%. The region is driven by rapid FMCG industry expansion and increasing consumption of packaged goods.

China is the dominant country due to its large manufacturing and consumer base. A key growth factor is the expansion of domestic FMCG production and retail distribution networks.

Middle East & Africa

The Middle East & Africa region accounted for 6.2% of the market share in 2025 and is projected to grow at a CAGR of 7.2%. Growth is supported by increasing urbanization and retail sector expansion.

Saudi Arabia leads the region due to rising investments in packaged food industries. A unique growth factor is the development of modern retail infrastructure.

Latin America

Latin America held a market share of 7.7% in 2025 and is expected to grow at a CAGR of 7.6%. The region is witnessing rising demand for packaged FMCG products.

Brazil dominates the market due to its strong food and beverage industry. A key growth factor is increasing adoption of sustainable packaging in consumer goods.

Competitive Landscape

The duplex paper and board for FMCG market is moderately consolidated, with major players focusing on capacity expansion, sustainability initiatives, and product innovation. International Paper is recognized as a leading player due to its strong global presence and diversified product portfolio. The company continues to invest in sustainable fiber sourcing and advanced board manufacturing technologies.

Other key players include WestRock Company, Smurfit Kappa Group, Stora Enso, and Mondi Group. These companies are actively expanding production capacities and introducing recyclable and high-performance duplex board solutions. A recent development includes the launch of lightweight coated duplex boards designed to reduce material usage while maintaining strength and print quality. Competitive strategies in the market are increasingly focused on sustainability, cost efficiency, and innovation in packaging design.

Key Players List

- International Paper

- WestRock Company

- Smurfit Kappa Group

- Stora Enso Oyj

- Mondi Group

- UPM-Kymmene Corporation

- Nine Dragons Paper Holdings

- Oji Holdings Corporation

- Nippon Paper Industries

- Sappi Limited

- ITC Limited

- JK Paper Ltd.

- Georgia-Pacific LLC

- Lee & Man Paper Manufacturing

- Rengo Co. Ltd.