Dna Packaging Systems Market Size and Growth

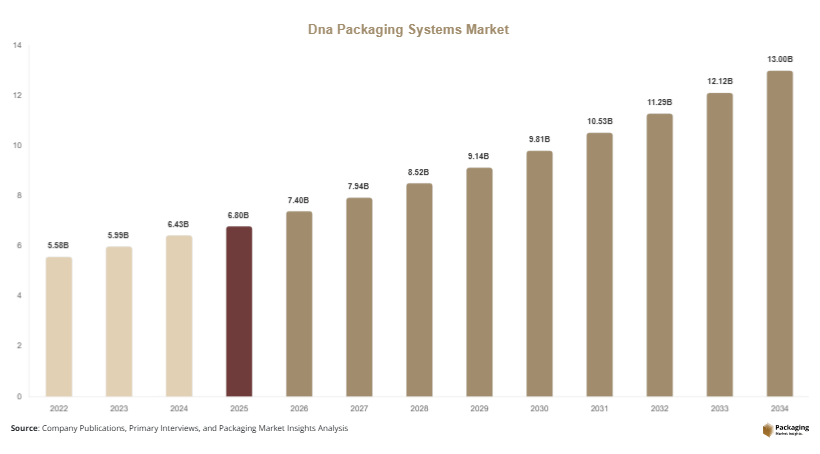

The global dna packaging systems market size was valued at USD 6.8 billion in 2025 and is projected to reach USD 7.4 billion in 2026. Over the forecast period, the market is expected to reach approximately USD 13.9 billion by 2034, expanding at a CAGR of 7.3% from 2025 to 2034. DNA packaging systems play a critical role in organizing and delivering genetic material within biological and synthetic systems, making them essential for applications in pharmaceuticals, diagnostics, and research. The dna packaging systems market is witnessing steady growth due to the increasing demand for advanced biotechnology solutions, gene therapy development, and precision medicine applications.

One of the primary growth factors is the rapid advancement in gene therapy and genetic engineering technologies. As research in genomics continues to expand, the need for efficient DNA packaging mechanisms that ensure stability, delivery accuracy, and controlled expression is increasing. This is particularly important in the development of targeted therapies and personalized medicine solutions.

Key Highlights:

- Asia Pacific dominated the market with a 35.6% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.6%.

- Viral vectors led the type segment with a 44.2% share, while non-viral vectors are expected to grow at a CAGR of 7.9%.

- Synthetic carriers dominated with a 51.3% share, while lipid-based carriers are forecasted to grow at a CAGR of 7.5%.

- Gene therapy applications led the segment with 46.7% share, while vaccine development is expected to grow at a CAGR of 7.4%.

- The United States remained the dominant country with a market size of USD 2.1 billion in 2025 and USD 2.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Integration of Nanotechnology in DNA Packaging

The integration of nanotechnology is transforming the dna packaging systems market by enabling the development of highly efficient and targeted delivery systems. Nanoparticles are being used to encapsulate and protect DNA molecules, ensuring stability and controlled release within biological systems. These technologies are particularly useful in gene therapy and drug delivery applications, where precision is critical. Researchers are focusing on designing nanoscale carriers that can overcome biological barriers and deliver genetic material to specific cells or tissues. This approach improves therapeutic outcomes and reduces side effects. The adoption of nanotechnology is expected to continue growing as it offers enhanced efficiency and scalability for DNA packaging systems.

Growing Adoption of Non-Viral Delivery Systems

There is a noticeable shift toward non-viral delivery systems in the dna packaging systems market due to concerns related to safety and immunogenicity associated with viral vectors. Non-viral systems, including lipid-based nanoparticles and polymer-based carriers, are gaining traction as they offer lower toxicity and greater flexibility. These systems are easier to manufacture and can be customized for specific applications. Pharmaceutical companies are increasingly investing in non-viral technologies to develop safer and more effective therapies. This trend is supported by ongoing research aimed at improving the efficiency and targeting capabilities of non-viral delivery systems.

Market Drivers

Expansion of Gene Therapy and Precision Medicine

The rapid growth of gene therapy and precision medicine is a major factor driving the dna packaging systems market. These therapies rely on efficient delivery of genetic material to achieve targeted treatment outcomes. DNA packaging systems play a crucial role in ensuring that genetic material is protected and delivered accurately. The increasing number of clinical trials and regulatory approvals for gene therapies is boosting demand for advanced packaging solutions. As healthcare systems shift toward personalized treatment approaches, the need for reliable DNA packaging technologies is expected to grow significantly.

Increasing Investment in Biotechnology Research

The rise in investment in biotechnology research and development is significantly contributing to market growth. Governments, academic institutions, and private companies are investing heavily in genomic research, drug discovery, and vaccine development. These activities require advanced DNA packaging systems to support experimentation and production processes. The availability of funding is enabling the development of innovative technologies and expanding the scope of applications. As research activities continue to increase, the demand for efficient DNA packaging systems is expected to rise.

Market Restraint

High Cost and Technical Complexity of DNA Packaging Systems

The dna packaging systems market faces challenges related to high costs and technical complexity. Developing and manufacturing advanced DNA packaging systems requires specialized equipment, skilled personnel, and extensive research. These factors contribute to high production costs, which can limit adoption, particularly among smaller organizations. Additionally, the complexity of designing efficient and safe delivery systems presents technical challenges. For example, optimizing the balance between stability and release efficiency in DNA carriers can be difficult. These challenges can slow down market growth and create barriers for new entrants.

Market Opportunities

Advancements in Synthetic Biology and Genomic Engineering

The growing field of synthetic biology presents significant opportunities for the dna packaging systems market. Researchers are developing engineered biological systems that require efficient DNA packaging mechanisms. These advancements are enabling new applications in medicine, agriculture, and industrial biotechnology. The ability to design and manipulate genetic material is creating demand for innovative packaging solutions that ensure stability and functionality. Companies that invest in synthetic biology technologies are likely to benefit from emerging opportunities in the market.

Expansion of Vaccine Development Programs

The increasing focus on vaccine development is creating new opportunities for DNA packaging systems. The need for rapid and effective vaccine production has highlighted the importance of efficient genetic material delivery systems. DNA-based vaccines require reliable packaging solutions to ensure stability and efficacy. The expansion of global vaccination programs and the development of new vaccine technologies are driving demand for advanced DNA packaging systems. This trend is expected to continue as healthcare systems prioritize disease prevention and preparedness.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.8 Billion |

| Market Size in 2026 | USD 7.4 Billion |

| Market Size in 2034 | USD 13.9 Billion |

| CAGR | 7.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Viral vectors accounted for the largest share of 44.2% in 2024, driven by their high efficiency in delivering genetic material into target cells. These vectors are widely used in gene therapy and vaccine development due to their ability to achieve stable gene expression. Their effectiveness in clinical applications has made them a preferred choice for researchers and pharmaceutical companies. Continuous advancements in viral vector design are improving safety and performance, supporting their dominance in the market.

Non-viral vectors are projected to grow at a CAGR of 7.9%, driven by their lower risk profile and flexibility. These systems include lipid-based nanoparticles and polymer-based carriers that offer safer alternatives to viral vectors. The increasing focus on reducing immunogenicity and improving scalability is driving the adoption of non-viral delivery systems. Ongoing research is enhancing their efficiency, making them a key growth segment.

By Material

Synthetic carriers dominated the market with a share of 51.3% in 2024 due to their versatility and ability to be customized for specific applications. These carriers are widely used in DNA packaging systems for their stability and compatibility with various formulations. The development of advanced synthetic materials is improving performance and expanding their use in different applications.

Lipid-based carriers are expected to grow at a CAGR of 7.5%, driven by their effectiveness in delivering genetic material. These carriers are widely used in non-viral delivery systems and offer advantages such as biocompatibility and low toxicity. The increasing adoption of lipid-based technologies in vaccine development is supporting segment growth.

By Application

Gene therapy applications accounted for the largest share of 46.7% in 2024, driven by the increasing development of targeted therapies. DNA packaging systems are essential for delivering genetic material in these applications, ensuring stability and efficiency. The growing number of clinical trials and approvals is supporting segment growth.

Vaccine development is projected to grow at a CAGR of 7.4%, driven by increasing demand for effective vaccines. DNA-based vaccines require reliable packaging systems to ensure stability and delivery efficiency. The expansion of global vaccination programs is supporting growth in this segment.

Dna Packaging Systems Market Segmentations

By Type

- Viral Vectors

- Non-Viral Vectors

By Material

- Synthetic Carriers

- Lipid-Based Carriers

- Polymer-Based Carriers

By Application

- Gene Therapy

- Vaccine Development

- Research Applications

Regional Analysis

North America

North America accounted for a 31.2% share of the dna packaging systems market in 2025 and is projected to grow at a CAGR of 6.8% during the forecast period. The region benefits from a strong biotechnology industry and advanced research infrastructure. The presence of leading pharmaceutical companies and research institutions is driving demand for DNA packaging systems. Additionally, government funding and supportive regulatory frameworks are contributing to market growth.

The United States dominates the regional market due to its extensive research activities and high investment in biotechnology. A key growth factor is the increasing number of clinical trials for gene therapies and vaccines. This is driving demand for advanced DNA packaging solutions that support efficient and safe delivery of genetic material.

Europe

Europe held a market share of 26.4% in 2025 and is expected to grow at a CAGR of 7.0%. The region’s growth is supported by strong research capabilities and increasing investment in biotechnology. European countries are focusing on advancing genomic research and developing innovative therapies. The presence of established pharmaceutical companies also supports market expansion.

Germany is the leading country in the European market, driven by its strong research infrastructure and focus on innovation. A unique growth factor is the country’s investment in biotechnology research programs, which is driving demand for advanced DNA packaging systems. This trend is expected to support market growth.

Asia Pacific

Asia Pacific dominated the market with a 35.6% share in 2025 and is projected to grow at a CAGR of 7.8%. The region’s growth is driven by increasing healthcare investment, expanding biotechnology sector, and rising demand for advanced therapies. Countries such as China, India, and Japan are witnessing significant growth in research activities and pharmaceutical production.

China is the dominant country in the region, supported by its large population and growing biotechnology industry. A key growth factor is the increasing government support for genomic research and drug development. This is driving demand for efficient DNA packaging systems.

Middle East & Africa

The Middle East & Africa region accounted for 3.9% of the market share in 2025 and is expected to grow at a CAGR of 6.5%. The region is experiencing growth in healthcare infrastructure and research activities. Governments are investing in biotechnology development, which is supporting market growth.

The United Arab Emirates is a key market in the region due to its focus on innovation and healthcare development. A unique growth factor is the establishment of research centers and partnerships with global organizations, which is driving demand for DNA packaging systems.

Latin America

Latin America held a 2.9% share in 2025 and is projected to grow at a CAGR of 7.6%. The region’s growth is driven by increasing healthcare investment and expanding research activities. The development of pharmaceutical industries is also contributing to market growth.

Brazil dominates the regional market, supported by its growing biotechnology sector and research initiatives. A key growth factor is the increasing focus on vaccine development and public health programs, which is driving demand for DNA packaging systems.

Competitive Landscape

The dna packaging systems market is moderately competitive, with key players focusing on innovation and technological advancements. Companies are investing in research and development to improve the efficiency and safety of DNA packaging systems. Strategic partnerships and collaborations are common strategies used to expand market presence.

Thermo Fisher Scientific is recognized as a leading player in the market, offering a wide range of biotechnology solutions. The company recently introduced advanced DNA delivery systems designed to improve efficiency and scalability. Other major players are also focusing on expanding their product portfolios and enhancing their technological capabilities to remain competitive.

Key Players List

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Lonza Group AG

- Danaher Corporation

- Bio-Rad Laboratories Inc.

- Qiagen N.V.

- Agilent Technologies Inc.

- Promega Corporation

- GenScript Biotech Corporation

- Takara Bio Inc.

- Oxford Biomedica plc

- Novasep Holding S.A.S.

- Charles River Laboratories

- Sartorius AG

- Catalent Inc.