Dental Retainer Packaging Market Size and Growth

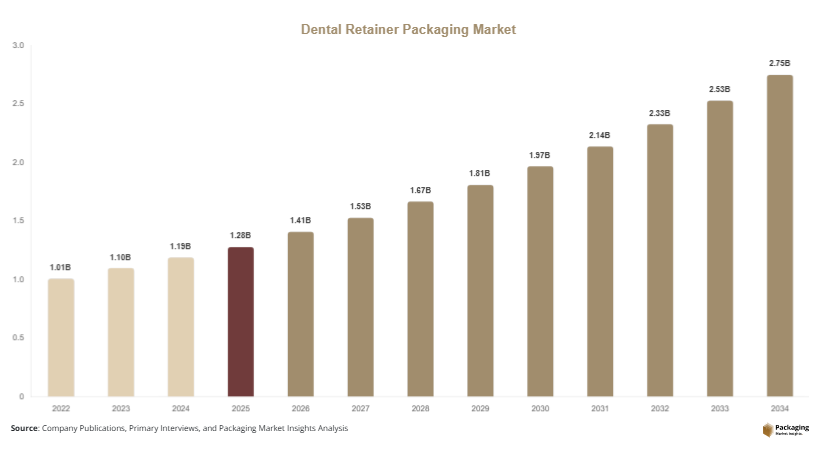

In 2025, the global dental retainer packaging market size is estimated at USD 1.28 billion, and it is projected to reach USD 1.41 billion in 2026. By 2034, the market is expected to attain approximately USD 2.78 billion, expanding at a CAGR of 8.7% during 2025–2034. This growth reflects the increasing use of clear aligners and retainers in post-orthodontic care across both developed and emerging economies. The dental retainer packaging market is witnessing steady expansion driven by the rising adoption of orthodontic treatments, increasing awareness of oral healthcare, and growing demand for protective and hygienic storage solutions for dental retainers.

One of the primary growth factors is the rising prevalence of orthodontic disorders, particularly among adolescents and young adults, which is increasing the demand for retainers and their protective packaging. Another key factor is the expansion of dental clinics and orthodontic service providers, which is boosting the requirement for hygienic, tamper-proof, and durable packaging solutions. Additionally, technological advancements in medical-grade plastics and antimicrobial packaging materials are improving product safety, shelf life, and patient compliance, further supporting market expansion.

Key Highlights

- Asia Pacific dominated the market with a 37.4% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share, while antimicrobial additives are expected to grow at a CAGR of 6.5%.

- Plastic packaging dominated with a 52.3% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

- Food & beverage applications led the segment with 43.1% share, while healthcare packaging is expected to grow at a CAGR of 6.3%.

- China remained dominant with USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Antimicrobial and Hygienic Packaging Solutions

The dental retainer packaging market is experiencing a strong shift toward antimicrobial and hygiene-focused packaging materials. As retainers are directly placed in the mouth, maintaining cleanliness and preventing microbial contamination is critical. Manufacturers are increasingly incorporating antimicrobial coatings and materials such as silver-ion infused plastics and treated polymers to enhance safety. These solutions help reduce bacterial growth during storage and transportation, improving patient health outcomes. Dental clinics are also adopting single-use sterile packaging formats for retainers to comply with infection control standards. This trend is particularly strong in developed healthcare systems where regulatory compliance and patient safety standards are highly stringent.

Growth of Custom-Molded and Patient-Specific Packaging Designs

Another significant trend is the increasing demand for custom-molded packaging solutions tailored to individual dental retainers. With the rise of 3D printing and digital orthodontics, retainers are now often designed based on patient-specific dental impressions. This has led to packaging manufacturers developing customized storage cases that precisely fit unique retainer shapes. These designs improve protection, reduce deformation risk, and enhance patient convenience. Additionally, orthodontic clinics are offering branded and personalized packaging kits to improve patient experience and reinforce brand identity. The integration of ergonomic design and lightweight materials is further enhancing usability and portability of retainer packaging solutions.

Market Drivers

Rising Demand for Orthodontic Treatments and Clear Aligners

The increasing prevalence of dental misalignment and orthodontic disorders is a key driver of the dental retainer packaging market. Growing awareness of dental aesthetics, particularly among younger populations, has led to a surge in orthodontic treatments, including braces and clear aligners. Post-treatment retainers are essential for maintaining teeth alignment, directly increasing demand for protective packaging solutions. Dental clinics and orthodontic providers require durable, hygienic, and easy-to-handle packaging to store and distribute retainers safely. Additionally, rising disposable income levels and improved access to dental care services in emerging markets are further accelerating market growth.

Expansion of Dental Clinics and Digital Orthodontics

Another major driver is the rapid expansion of dental clinics and the adoption of digital orthodontics technologies. Clinics are increasingly using 3D scanning and CAD/CAM systems to design customized retainers, which require equally precise packaging solutions. This shift toward digital dentistry is increasing demand for high-quality packaging that ensures product integrity during handling and delivery. Moreover, the growth of dental service chains and specialized orthodontic centers is contributing to higher consumption of standardized packaging formats. Increasing patient turnover in clinics is also driving demand for cost-effective, bulk packaging solutions for retainers.

Market Restraint

Limited Standardization and Variability in Packaging Requirements

One of the key restraints in the dental retainer packaging market is the lack of standardized packaging formats across dental care providers. Different orthodontic clinics and manufacturers use varying retainer designs, which leads to inconsistent packaging requirements. This variability increases production complexity and raises manufacturing costs for packaging suppliers. Additionally, smaller dental clinics often prefer low-cost, generic packaging solutions, limiting adoption of advanced antimicrobial or customized packaging products. The absence of universal packaging standards in the dental sector creates challenges for large-scale manufacturers seeking operational efficiency and uniform product distribution.

Market Opportunities

Development of Smart and Digitally Traceable Packaging Solutions

The integration of smart technologies into dental retainer packaging presents a significant growth opportunity. Packaging solutions embedded with QR codes, RFID tags, and digital tracking systems are being developed to improve traceability and patient compliance. These smart packaging formats allow dental clinics to track usage instructions, appointment schedules, and maintenance guidelines. Additionally, digital integration enhances patient engagement and improves treatment adherence. As digital dentistry continues to evolve, smart packaging is expected to become a key value-added feature in orthodontic care solutions.

Expansion of Sustainable and Eco-Friendly Packaging Materials

Sustainability is emerging as a major opportunity in the dental retainer packaging market. Manufacturers are increasingly focusing on biodegradable plastics, recyclable polymers, and paper-based packaging alternatives to reduce environmental impact. Dental clinics are also adopting eco-friendly packaging to align with healthcare sustainability initiatives. The shift toward green packaging materials is particularly strong in regions with strict environmental regulations. Additionally, innovations in bio-based polymers are enabling the development of durable yet sustainable retainer packaging solutions that maintain hygiene standards while reducing plastic waste.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.28 Billion |

| Market Size in 2026 | USD 1.41 Billion |

| Market Size in 2034 | USD 2.78 Billion |

| CAGR | 8.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

Material

The Material Type segment is dominated by polypropylene-based packaging materials, which accounted for approximately 38.4% share in 2024. These materials are widely used due to their durability, chemical resistance, and cost efficiency. Polypropylene is commonly used in manufacturing retainer cases and protective storage boxes due to its lightweight structure and ability to withstand repeated use. Dental clinics prefer polypropylene-based packaging because it provides adequate protection while maintaining affordability for large-scale patient distribution. The material also supports easy molding into custom shapes, making it suitable for orthodontic applications.

The fastest-growing subsegment is biodegradable polymer-based packaging, projected to grow at a CAGR of 9.1%, driven by increasing demand for sustainable healthcare packaging solutions. These materials are gaining traction due to rising environmental awareness and regulatory pressure on plastic usage. Biodegradable packaging offers reduced environmental impact while maintaining necessary hygiene standards for medical applications. Dental practices in developed regions are increasingly adopting eco-friendly packaging alternatives to align with sustainability goals.

Product

The storage cases segment dominated with a 42.7% share in 2024, driven by widespread use of reusable retainer cases in orthodontic care. These cases provide durable protection and are commonly distributed by dental clinics to patients after treatment. Storage cases are designed to prevent deformation, contamination, and loss of retainers, making them essential in post-treatment care.

The blister packaging segment is the fastest-growing, expanding at a CAGR of 8.8%, driven by increasing demand for single-use sterile packaging formats. Blister packs are widely used in clinical environments where hygiene and infection control are critical. Their tamper-evident design enhances patient safety and ensures product integrity during distribution.

End-Use Segment

Dental clinics dominated the end-use segment with a 49.3% share in 2024, driven by high patient volumes and frequent orthodontic procedures. Clinics require standardized and cost-effective packaging solutions for retainers distributed after treatment completion. Bulk procurement and consistent usage patterns make this segment the largest consumer of packaging products.

The e-commerce dental supply segment is the fastest-growing, expanding at a CAGR of 8.5%, driven by rising online sales of dental care products. Digital platforms are increasingly offering orthodontic kits and accessories, including retainer packaging solutions, directly to consumers and clinics.

Dental Retainer Packaging Market Segmentations

By Material Type

- Polypropylene (PP)

- Polyethylene (PE)

- Biodegradable Polymers

- Thermoplastic Elastomers

By Product Type

- Storage Cases

- Blister Packaging

- Pouches & Bags

- Custom Molded Cases

By End Use

- Dental Clinics

- Hospitals

- Orthodontic Centers

- E-commerce Dental Suppliers

Regional Analysis

North America

North America accounted for approximately 28.6% market share in 2025, with a projected CAGR of 8.3% through 2034. The region’s growth is supported by advanced dental care infrastructure and high adoption of orthodontic treatments.

The United States dominates the regional market due to strong healthcare expenditure and widespread use of clear aligners. A key growth factor is the increasing demand for premium orthodontic services supported by digital dentistry adoption.

Europe

Europe held around 26.9% market share in 2025, with a CAGR of 8.1% projected through 2034. Growth is driven by well-established dental care systems and rising awareness of orthodontic treatments.

Germany leads the European market due to strong dental healthcare infrastructure. A key growth factor is increasing adoption of advanced orthodontic procedures in private dental clinics.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025, growing at a CAGR of 9.4%. The region benefits from a large patient population and increasing access to dental care services.

China remains the leading country due to expanding dental clinic networks. A key growth factor is rising awareness of orthodontic treatments among younger populations.

Middle East & Africa

The Middle East & Africa region accounted for 3.9% market share in 2025, with a CAGR of 6.8%. Growth is supported by improving healthcare infrastructure and rising dental tourism.

The UAE leads the region due to advanced dental clinics. A key growth factor is increasing investment in cosmetic dentistry services.

Latin America

Latin America held 2.6% market share in 2025, with the fastest CAGR of 6.2%. The region is witnessing growing demand for affordable orthodontic solutions.

Brazil dominates the market due to expanding dental care access. A key growth factor is increasing adoption of private dental clinics in urban areas.

Competitive Landscape

The dental retainer packaging market is moderately fragmented, with key players focusing on product innovation, customization, and sustainable material development. Major companies include Dentsply Sirona, Align Technology Inc., 3M Company, Henry Schein Inc., and Keystone Industries. Among these, Align Technology Inc. holds a strong position due to its leadership in clear aligner systems and integrated orthodontic solutions.

Recent developments include expansion of antimicrobial packaging product lines, introduction of eco-friendly biodegradable retainer cases, and integration of digital patient tracking systems into orthodontic packaging solutions. Companies are also investing in 3D printing technologies to support customized packaging designs aligned with digital dentistry workflows.

Key Players List

- Dentsply Sirona

- Align Technology Inc.

- 3M Company

- Henry Schein Inc.

- Keystone Industries

- Ormco Corporation

- GC Corporation

- Shofu Dental Corporation

- Ivoclar Vivadent AG

- Ultradent Products Inc.

- Danaher Corporation (Envista Holdings)

- Parkell Inc.

- Great Lakes Dental Technologies

- American Orthodontics

- TP Orthodontics Inc.