Dairy Aseptic Packaging Material Market Size and Growth

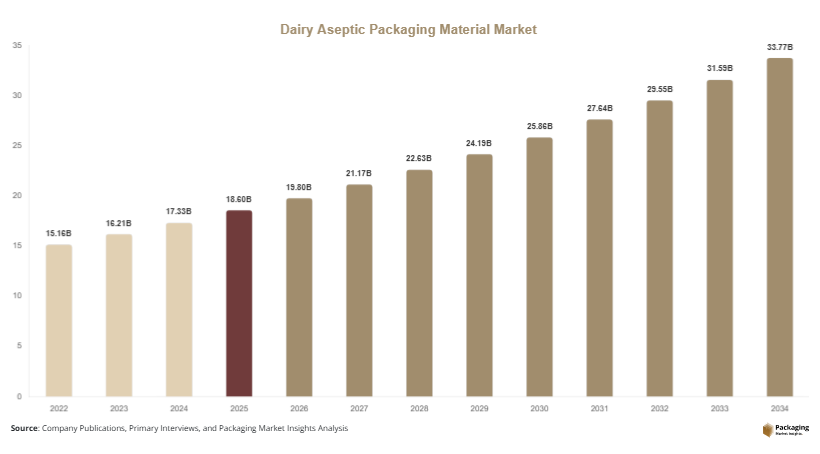

The global dairy aseptic packaging material market size is estimated to reach USD 18.6 billion in 2025 and is projected to grow to USD 19.8 billion in 2026. Over the forecast period, the market is expected to achieve a value of USD 33.9 billion by 2034, registering a CAGR of 6.9% from 2025 to 2034. This growth reflects increasing demand for extended shelf-life dairy products, especially in regions with limited cold chain infrastructure. The dairy aseptic packaging material market is experiencing steady expansion as the global dairy industry shifts toward safe, shelf-stable, and efficient packaging formats.

A major factor driving the dairy aseptic packaging material market is the rising consumption of ready-to-drink dairy beverages, including milk, flavored milk, and yogurt drinks. These products require packaging solutions that maintain freshness and safety without refrigeration. Another key factor is the increasing focus on food safety and hygiene standards, which is encouraging the adoption of aseptic packaging materials. Additionally, the expansion of organized retail and e-commerce channels is supporting demand for lightweight, durable, and transport-efficient packaging formats.

Key Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.2%.

- Paperboard-based materials led the type segment with a 42.8% share, while bio-based polymers are expected to grow at a CAGR of 7.5%.

- Plastic packaging dominated with a 50.6% share, while paper-based packaging is forecasted to grow at a CAGR of 7.1%.

- Dairy beverage applications led the segment with 61.3% share, while yogurt and fermented products are expected to grow at a CAGR of 6.8%.

- China remained the dominant country with a market size of USD 4.3 billion in 2025 and USD 4.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising adoption of sustainable and recyclable aseptic packaging materials

The dairy aseptic packaging material market is increasingly influenced by the shift toward sustainable packaging solutions. Manufacturers are focusing on developing recyclable and bio-based materials that reduce environmental impact while maintaining product integrity. Paperboard-based aseptic cartons are gaining popularity due to their renewable nature and compatibility with recycling systems. Companies are also reducing the use of fossil-based plastics by incorporating plant-based polymers. This trend is driven by regulatory requirements and growing consumer awareness regarding environmental sustainability. As a result, the adoption of eco-friendly aseptic packaging materials is expected to continue expanding across global markets.

Increasing demand for convenient and shelf-stable dairy products

The growing demand for convenient and long-lasting dairy products is shaping the dairy aseptic packaging material market. Consumers are seeking products that offer extended shelf life without refrigeration, especially in urban areas with busy lifestyles. Aseptic packaging enables the safe storage and transportation of dairy products, reducing the need for cold chain logistics. This trend is particularly strong in emerging markets, where infrastructure limitations make aseptic packaging a practical solution. Additionally, the rise of single-serve packaging formats is further driving demand for aseptic materials.

Market Drivers

Growing demand for extended shelf-life dairy products

The increasing demand for dairy products with longer shelf life is a key driver of the dairy aseptic packaging material market. Aseptic packaging allows dairy products to be stored at room temperature without compromising quality. This is particularly beneficial in regions with limited refrigeration facilities. The ability to extend product shelf life reduces food waste and improves supply chain efficiency. As consumer preferences shift toward convenient and ready-to-consume products, the demand for aseptic packaging materials is expected to grow.

Expansion of dairy processing and distribution networks

The expansion of dairy processing and distribution networks is another significant driver of market growth. Dairy companies are investing in advanced processing technologies to meet rising demand. Aseptic packaging materials play a crucial role in ensuring product safety during transportation and storage. The growth of organized retail and e-commerce platforms is also increasing the need for efficient packaging solutions. As distribution networks expand, the adoption of aseptic packaging materials is expected to rise.

Market Restraint

High initial investment and production costs

The dairy aseptic packaging material market faces challenges related to high initial investment and production costs. Aseptic packaging systems require advanced machinery and specialized materials, which can be expensive for manufacturers. Small and medium-sized dairy producers may find it difficult to adopt aseptic packaging due to these costs. Additionally, the complexity of multilayer packaging structures can increase production expenses. For example, the use of aluminum layers and specialized coatings adds to the overall cost of packaging materials. These factors may limit market growth, particularly in cost-sensitive regions.

Market Opportunities

Development of bio-based and recyclable packaging materials

The development of bio-based and recyclable materials presents significant opportunities in the dairy aseptic packaging material market. Companies are investing in research and development to create sustainable alternatives to traditional packaging materials. These innovations aim to reduce environmental impact while maintaining performance. The increasing adoption of circular economy practices is further supporting the demand for recyclable packaging solutions.

Growth in emerging markets with limited cold chain infrastructure

Emerging markets offer substantial growth opportunities for the dairy aseptic packaging material market. In regions where cold chain infrastructure is limited, aseptic packaging provides a practical solution for preserving dairy products. The rising demand for packaged dairy products in these markets is driving the adoption of aseptic materials. As infrastructure improves and consumer awareness increases, the market is expected to expand further.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.8 Billion |

| Market Size in 2034 | USD 33.9 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Paperboard-based materials dominated the dairy aseptic packaging material market in 2024, accounting for approximately 42.8% of the total share. These materials are widely used due to their renewable nature and excellent barrier properties when combined with other layers. Paperboard-based aseptic cartons are commonly used for packaging milk and other dairy beverages. Their lightweight structure and ease of handling make them a preferred choice among manufacturers.

Bio-based polymers are expected to grow at the fastest CAGR of 7.5% during the forecast period. These materials offer environmental benefits and align with sustainability goals. The increasing demand for eco-friendly packaging solutions is driving the growth of this segment.

By Packaging Type

Cartons accounted for the largest market share in 2024, representing 58.6% of the total market. Aseptic cartons are widely used for dairy products due to their ability to preserve freshness and extend shelf life. These cartons are available in various sizes and formats, making them suitable for different applications.

Bottles are expected to grow at the fastest CAGR of 6.8%. Aseptic bottles offer convenience and durability, making them suitable for on-the-go consumption. The increasing demand for single-serve packaging formats is driving the growth of this segment.

By Application

Dairy beverages dominated the market in 2024, accounting for 61.3% of the total share. The high consumption of milk and flavored dairy drinks is driving demand for aseptic packaging materials. These materials ensure product safety and extend shelf life, making them suitable for beverage applications.

Yogurt and fermented products are expected to grow at the fastest CAGR of 6.8%. The increasing popularity of probiotic and functional dairy products is driving the growth of this segment. Aseptic packaging helps maintain product quality and prevents contamination.

Dairy Aseptic Packaging Material Market Segmentations

By Material Type

- Paperboard

- Plastic

- Aluminum

- Bio-based Materials

By Packaging Type

- Cartons

- Bottles

- Pouches

By Application

- Milk

- Flavored Milk

- Yogurt & Fermented Products

- Cream & Others

Regional Analysis

North America

North America accounted for approximately 23.4% of the dairy aseptic packaging material market in 2025 and is expected to grow at a CAGR of 6.1% during the forecast period. The region’s well-established dairy industry and high demand for packaged dairy products are key factors driving market growth. Increasing focus on food safety and quality standards is also supporting the adoption of aseptic packaging materials.

The United States dominates the regional market due to its large consumer base and advanced food processing industry. A unique growth factor is the increasing demand for organic and premium dairy products, which require high-quality packaging solutions to maintain freshness and safety.

Europe

Europe held a market share of around 25.1% in 2025 and is projected to grow at a CAGR of 6.4%. The region’s strong regulatory framework and emphasis on sustainability are driving the adoption of aseptic packaging materials. The demand for recyclable and eco-friendly packaging solutions is particularly high.

Germany leads the European market due to its advanced manufacturing capabilities and strong dairy industry. A unique growth factor is the widespread adoption of sustainable packaging practices, which encourages the use of recyclable aseptic materials.

Asia Pacific

Asia Pacific dominated the dairy aseptic packaging material market in 2025 with a 39.2% share and is expected to grow at a CAGR of 7.0%. Rapid urbanization, population growth, and increasing consumption of dairy products are key factors driving market growth.

China is the dominant country in the region, supported by a large consumer base and expanding dairy industry. A unique growth factor is the increasing demand for shelf-stable dairy products in rural areas, where refrigeration infrastructure is limited.

Middle East & Africa

The Middle East & Africa region accounted for 6.8% of the market share in 2025 and is expected to grow at a CAGR of 6.2%. The growing demand for packaged dairy products and improving retail infrastructure are driving market growth.

Saudi Arabia is a key market in the region, supported by increasing consumption of dairy products. A unique growth factor is the need for long shelf-life products due to climatic conditions, which drives the adoption of aseptic packaging materials.

Latin America

Latin America held a market share of 5.5% in 2025 and is projected to grow at the fastest CAGR of 7.2%. The region’s growing middle class and increasing demand for convenient dairy products are key drivers of market growth.

Brazil dominates the regional market due to its large population and strong dairy industry. A unique growth factor is the expansion of retail and distribution networks, which supports the adoption of aseptic packaging materials.

Competitive Landscape

The dairy aseptic packaging material market is characterized by the presence of several global and regional players focusing on innovation and sustainability. Leading companies include Tetra Pak International S.A., SIG Combibloc Group, Elopak AS, Amcor plc, and Mondi Group. Among these, Tetra Pak International S.A. is recognized as a leading player due to its extensive product portfolio and strong global presence.

Companies are investing in research and development to create advanced packaging solutions that meet evolving consumer demands. Recent developments include the introduction of recyclable aseptic cartons and expansion of production capacities. Strategic partnerships and collaborations are also common in the market.

Key Players List

- Tetra Pak International S.A.

- SIG Combibloc Group

- Elopak AS

- Amcor plc

- Mondi Group

- Stora Enso Oyj

- Smurfit Kappa Group

- Uflex Ltd.

- Greatview Aseptic Packaging Co., Ltd.

- Ecolean AB

- Nippon Paper Industries Co., Ltd.

- DS Smith Plc

- Sonoco Products Company

- Huhtamaki Oyj

- Sealed Air Corporation