Cups And Lids Market Size and Growth

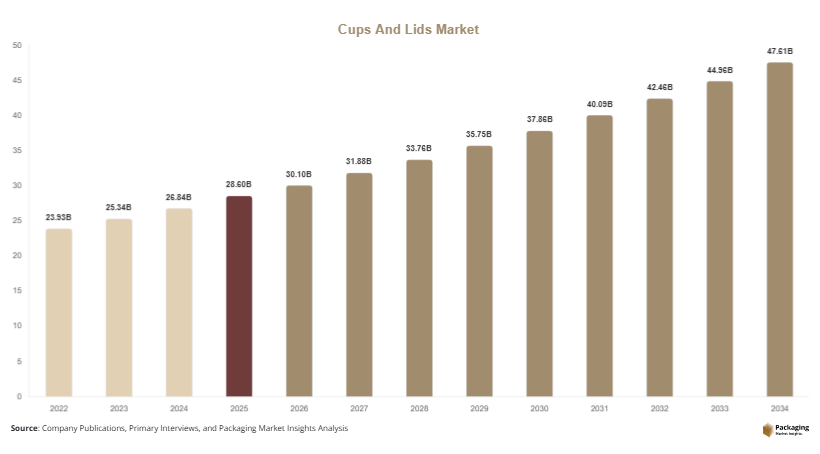

The global cups and lids market was valued at USD 28.6 billion in 2025 and is projected to reach USD 30.1 billion in 2026. The market is forecasted to attain USD 47.8 billion by 2034, expanding at a CAGR of 5.9% during the 2025–2034 period. The global cups and lids market is experiencing consistent growth due to rising demand for convenient food and beverage packaging solutions across quick-service restaurants, cafes, institutional catering, food delivery platforms, and retail beverage chains. Cups and lids are essential packaging products used for hot drinks, cold beverages, desserts, dairy products, and takeaway food applications.

One of the major growth factors supporting the cups and lids market is the rapid expansion of food delivery and takeaway services globally. Consumers increasingly prefer on-the-go beverages and ready-to-consume meals, which is driving demand for durable and leak-resistant disposable packaging solutions. Coffee chains, bubble tea outlets, and fast-food restaurants continue to expand their store networks across urban and semi-urban regions, increasing consumption of paper cups, plastic lids, and sustainable beverage containers.

Key Market Insights

- Asia Pacific dominated the market with a 36.9% share.

- Latin America is projected to grow at the fastest CAGR of 6.7%.

- Disposable cups led the type segment with a 42.5% share.

- Plastic material dominated with a 48.1% share.

- Foodservice and beverage chains led the end-use segment with 44.3% share.

- The US remained the dominant country with a market size of USD 5.8 billion in 2025 and USD 6.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Compostable Packaging

Sustainability has become a major trend influencing the cups and lids market as foodservice operators and beverage brands focus on reducing plastic waste and meeting environmental regulations. Restaurants, cafes, and convenience stores are increasingly replacing conventional plastic cups and lids with compostable paper cups, molded fiber lids, and biodegradable packaging solutions. This shift is particularly strong in North America and Europe, where restrictions on single-use plastics are encouraging adoption of eco-friendly alternatives.

Packaging manufacturers are introducing plant-based coatings and recyclable materials that improve product durability while maintaining compostability standards. For example, several coffee chains are transitioning toward fiber-based lids and recyclable paper beverage containers to improve sustainability performance and enhance brand image. Over the forecast period, demand for sustainable packaging is expected to rise further as consumers increasingly prefer environmentally responsible products and governments continue implementing stricter waste reduction policies.

Growth of Customization and Premium Beverage Packaging

The increasing popularity of premium beverages and branded foodservice experiences is driving demand for customized cups and lids across the global market. Beverage chains are using innovative packaging designs, digital printing technologies, and unique lid structures to strengthen consumer engagement and improve product differentiation. Custom cups with seasonal branding, promotional messaging, and interactive QR codes are becoming increasingly common in coffee shops, bubble tea stores, and fast-food outlets.

Manufacturers are also introducing ergonomic lid designs, heat-resistant cups, and spill-proof beverage packaging to improve customer convenience. For instance, premium coffee brands are investing in double-wall insulated paper cups and resealable lids to enhance beverage temperature retention during takeaway and delivery operations. Future developments in smart printing technologies and sustainable decorative materials are expected to further accelerate demand for premium customized packaging solutions.

Market Drivers

Expansion of Quick-Service Restaurants and Café Chains

The rapid expansion of quick-service restaurants and café chains is a major driver supporting growth in the cups and lids market. Urban consumers increasingly prefer takeaway beverages, ready-to-eat meals, and convenient dining formats, which is increasing demand for disposable beverage packaging products. Global coffee chains, fast-food brands, and bubble tea outlets are expanding aggressively across emerging markets, leading to higher consumption of cups, lids, and beverage carriers.

The rise of franchise-based restaurant models is also contributing to packaging demand because standardized beverage packaging improves operational consistency and branding. Quick-service operators prefer lightweight and stackable packaging products that support high-volume beverage sales while minimizing transportation and storage costs. As foodservice chains continue expanding into tier-2 and tier-3 cities, packaging manufacturers are expected to witness increasing demand from both domestic and international restaurant operators.

Rising Demand for Food Delivery and Takeaway Services

The rapid growth of online food delivery platforms is significantly contributing to the expansion of the cups and lids market. Consumers increasingly rely on food delivery applications for beverages, desserts, smoothies, and ready-to-drink products, creating strong demand for leak-resistant and tamper-evident packaging solutions. Beverage containers with secure lids are essential for preventing spills and maintaining product quality during transportation.

Food delivery platforms and cloud kitchens are increasingly investing in high-quality takeaway packaging to improve customer satisfaction and strengthen brand identity. Beverage chains are also adopting insulated cups and advanced sealing lids to maintain product temperature during delivery. The continued expansion of digital food ordering platforms across Asia Pacific, North America, and the Middle East is expected to sustain long-term demand for innovative beverage packaging products.

Market Restraint

Fluctuating Raw Material Costs and Environmental Compliance Challenges

Volatility in raw material prices remains a major restraint affecting the cups and lids market. Manufacturers depend heavily on paper pulp, polyethylene, polypropylene, and polystyrene materials, all of which are influenced by fluctuations in crude oil prices, transportation costs, and supply chain disruptions. Sudden increases in resin or paper prices can reduce manufacturer profit margins and increase product costs for foodservice operators.

Environmental regulations targeting single-use plastics are also creating compliance challenges for packaging manufacturers. Several countries are implementing restrictions on plastic lids and disposable packaging products, forcing companies to invest in alternative materials and production technologies. Transitioning to compostable and recyclable packaging systems often involves higher manufacturing costs and additional certification requirements. For example, small beverage chains may struggle to adopt sustainable packaging due to higher procurement costs associated with biodegradable materials. These challenges may slow market growth in price-sensitive regions and increase operational complexity for packaging suppliers.

Market Opportunities

Expansion of Sustainable Fiber-Based Packaging Solutions

The growing shift toward sustainable food packaging is creating significant opportunities for the cups and lids market. Consumers and regulatory authorities are increasingly encouraging the use of recyclable and compostable packaging products, leading to rising demand for paper cups, molded fiber lids, and biodegradable beverage containers. Packaging manufacturers are investing in innovative fiber-based materials with moisture resistance and improved heat retention capabilities.

Foodservice chains are increasingly partnering with sustainable packaging suppliers to reduce environmental impact and strengthen brand reputation. The expansion of zero-waste retail concepts and eco-friendly cafes is further supporting demand for compostable beverage packaging products. Future opportunities are expected to emerge from advancements in plant-based coatings, recyclable barrier technologies, and industrial composting infrastructure across developed economies.

Rising Demand from Emerging Markets and Convenience Retail

Emerging economies are creating substantial growth opportunities for the cups and lids market due to rapid urbanization, increasing disposable incomes, and changing food consumption habits. Convenience stores, cinema chains, supermarkets, and fuel station retailers are witnessing increasing demand for ready-to-drink beverages and takeaway food products, supporting higher consumption of disposable cups and lids.

Countries such as India, Brazil, Indonesia, and Vietnam are experiencing rapid growth in organized foodservice and café culture, increasing the need for affordable and durable beverage packaging solutions. Packaging manufacturers are expanding regional production facilities and distribution partnerships to capitalize on rising demand from local foodservice operators. Continued investment in retail modernization and food delivery infrastructure is expected to support long-term market growth in emerging economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.6 Billion |

| Market Size in 2026 | USD 30.1 Billion |

| Market Size in 2034 | USD 47.8 Billion |

| CAGR | 5.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Disposable cups accounted for the largest share of the cups and lids market in 2024, representing approximately 42.5% of total revenue. These products remain highly preferred across coffee chains, fast-food restaurants, cinemas, and institutional catering services because they offer convenience, lightweight handling, and cost efficiency. Disposable paper and plastic cups are widely used for serving hot beverages, cold drinks, smoothies, and desserts across high-volume foodservice operations. The dominance of this segment is also supported by rising demand for takeaway beverages and increasing growth in food delivery applications. Beverage chains continue to invest in customized cup designs and branded packaging to improve customer engagement and strengthen brand recognition. The growing expansion of café culture and organized foodservice operations is expected to sustain demand for disposable beverage cups globally.

Compostable lids are projected to emerge as the fastest-growing type segment, registering a CAGR of 7.4% during the forecast period. Environmental concerns and regulations restricting plastic packaging are encouraging foodservice operators to adopt biodegradable and fiber-based lid alternatives. Compostable lids made from molded pulp, bagasse, and plant-based polymers are increasingly being introduced across coffee shops and quick-service restaurants to reduce environmental impact. Packaging manufacturers are investing in leak-resistant compostable lid designs that maintain beverage functionality while improving sustainability performance. Future growth is expected to be supported by government initiatives promoting compostable food packaging and rising consumer demand for environmentally responsible takeaway products.

By Material

Plastic material dominated the cups and lids market in 2024 with a revenue share of approximately 48.1%. Plastic lids and beverage containers remain widely used because they provide durability, transparency, lightweight handling, and cost-effective production capabilities. Polypropylene and polyethylene materials are commonly utilized for cold beverage cups, smoothie containers, and spill-resistant lids across foodservice applications. Beverage chains and convenience retailers prefer plastic packaging because it supports mass production and offers compatibility with advanced sealing systems and customized printing technologies. The widespread availability of plastic raw materials and established manufacturing infrastructure also contribute to segment dominance.

Paper and fiber materials are anticipated to witness the fastest growth during the forecast period, expanding at a CAGR of 7.0% through 2034. Increasing restrictions on plastic waste and rising demand for sustainable packaging solutions are encouraging foodservice companies to transition toward paper cups and molded fiber lids. Packaging manufacturers are introducing moisture-resistant coatings and recyclable barrier technologies to improve durability and beverage insulation capabilities. Consumer preference for eco-friendly products is also supporting demand for compostable paper-based beverage packaging. Continued innovation in fiber-based materials and expansion of industrial composting facilities are expected to accelerate adoption across global foodservice markets.

By End-Use

Foodservice and beverage chains represented the dominant end-use segment in the cups and lids market in 2024, accounting for approximately 44.3% of overall revenue. Quick-service restaurants, coffee chains, bubble tea outlets, and cinema food counters rely heavily on cups and lids for serving beverages and takeaway meals. Rising urbanization and changing consumer lifestyles are increasing demand for convenient beverage packaging products that support portability and ease of consumption. Major beverage brands are also investing in customized packaging and innovative lid designs to strengthen brand identity and improve customer convenience. The continued expansion of organized foodservice operations across emerging economies is further supporting segment growth.

Online food delivery applications are expected to register the fastest CAGR of 7.6% during the forecast period. The rapid growth of digital food ordering platforms is increasing demand for leak-resistant, insulated, and tamper-evident beverage packaging solutions capable of maintaining product quality during transportation. Cloud kitchens and food delivery operators are increasingly investing in high-quality cups and lids to improve customer satisfaction and minimize beverage spills. Packaging suppliers are introducing advanced sealing lids and temperature-retention packaging systems designed specifically for delivery applications. The expansion of mobile ordering technologies and urban food delivery infrastructure is expected to create long-term growth opportunities for market participants.

Cups And Lids Market Segmentations

By Type

- Disposable Cups

- Reusable Cups

- Plastic Lids

- Paper Lids

- Compostable Lids

By Material

- Plastic

- Paper and Fiber

- Bioplastics

- Aluminum

By End-User

- Foodservice and Beverage Chains

- Online Food Delivery

- Institutional Catering

- Retail and Convenience Stores

- Household Applications

Regional Analysis

North America

North America accounted for approximately 24.6% of the global cups and lids market share in 2025 and is projected to register a CAGR of 5.5% during the forecast period. The regional market benefits from strong demand across coffee chains, quick-service restaurants, institutional foodservice, and convenience retail sectors. Consumers in the United States and Canada increasingly prefer takeaway beverages and ready-to-consume food products, supporting consistent demand for beverage packaging solutions. Sustainability regulations and corporate environmental commitments are encouraging restaurants and beverage companies to adopt recyclable and compostable cups and lids. Rising investment in digital ordering and food delivery platforms is also contributing to regional packaging consumption.

The United States remains the dominant country in North America due to its extensive foodservice industry and high beverage consumption rates. A key growth driver in the country is the increasing demand for premium coffee and specialty beverages requiring customized and insulated packaging solutions. Coffee chains are investing in fiber-based lids, recyclable cups, and branded beverage containers to improve sustainability performance and customer engagement. The expansion of food delivery applications and convenience retail formats is also supporting demand for tamper-evident and spill-resistant beverage packaging products across the country.

Europe

Europe represented nearly 26.1% of the global cups and lids market in 2025 and is forecasted to expand at a CAGR of 5.7% through 2034. The regional market is supported by strict environmental regulations targeting single-use plastics and increasing consumer demand for sustainable packaging alternatives. Countries including Germany, France, Italy, and the United Kingdom are witnessing strong adoption of compostable cups, paper lids, and recyclable beverage containers. Foodservice operators are increasingly replacing conventional plastic products with fiber-based packaging to comply with regional waste reduction policies.

Germany dominates the European market due to its strong packaging manufacturing sector and advanced recycling infrastructure. One unique growth driver in the country is the rapid adoption of reusable cup systems across coffee chains and urban takeaway beverage outlets. Beverage retailers are implementing deposit-return packaging programs that encourage consumers to return reusable cups and lids for cleaning and redistribution. Growing demand for premium beverages, combined with sustainability-focused consumer preferences, is expected to support continued investment in innovative foodservice packaging solutions across Germany.

Asia Pacific

Asia Pacific held the largest share of the cups and lids market at 36.9% in 2025 and is expected to register a CAGR of 6.5% during the forecast period. Rapid urbanization, rising disposable incomes, and expansion of organized foodservice industries are major factors supporting regional market growth. Countries including China, India, Japan, South Korea, and Indonesia are witnessing increasing consumption of takeaway beverages, bubble tea products, and ready-to-eat meals. The rapid growth of café chains, food delivery platforms, and convenience stores is significantly increasing demand for disposable beverage packaging products.

China remains the leading market in Asia Pacific due to its large-scale foodservice sector and expanding retail beverage industry. A major growth driver is the increasing popularity of bubble tea and specialty beverage chains requiring customized cups and sealing lids. Packaging manufacturers are investing in lightweight materials, digital printing technologies, and leak-resistant lid designs to improve product functionality and branding opportunities. India is also emerging as a major growth market due to the expansion of quick-service restaurant chains and rising demand for takeaway coffee products. Continued growth in urban food consumption is expected to sustain strong regional market demand.

Middle East & Africa

The Middle East & Africa accounted for approximately 6.4% of the global cups and lids market share in 2025 and is projected to grow at a CAGR of 6.0% through 2034. Expanding tourism activities, urban retail development, and rising foodservice investments are supporting demand for beverage packaging solutions across the region. International coffee chains, fast-food operators, and convenience retailers are expanding operations in Gulf countries and major African cities, increasing consumption of disposable cups and lids. Growth in outdoor dining and takeaway beverage culture is also contributing to regional market expansion.

Saudi Arabia dominates the regional market due to the rapid growth of café culture and premium beverage consumption. One unique growth driver is the increasing establishment of international coffee brands and food delivery platforms in urban centers such as Riyadh and Jeddah. Beverage retailers are investing in premium packaging formats and customized branding solutions to attract younger consumers and tourists. In Africa, South Africa is witnessing rising demand for takeaway beverage packaging due to growth in convenience retail and quick-service restaurant industries. Ongoing urbanization and retail modernization are expected to support long-term market expansion across the region.

Latin America

Latin America represented approximately 6.0% of the global cups and lids market in 2025 and is expected to witness the fastest CAGR of 6.7% during the forecast period. The regional market is benefiting from increasing urbanization, rising food delivery activity, and expansion of café and fast-food chains. Countries such as Brazil, Mexico, and Argentina are witnessing strong growth in convenience food consumption and takeaway beverage sales, creating higher demand for disposable packaging products. The expansion of shopping malls, multiplex cinemas, and fuel station retail formats is also contributing to market growth.

Brazil dominates the Latin American market due to its large foodservice sector and expanding coffee consumption. One important growth driver is the increasing adoption of takeaway coffee culture among urban consumers and office workers. Beverage chains are investing in branded paper cups and spill-resistant lids to improve consumer convenience and product differentiation. Packaging manufacturers are also expanding local production capacity to reduce supply chain costs and improve service capabilities for regional foodservice operators. Rising demand for affordable takeaway packaging is expected to support continued market expansion across Latin America.

Competitive Landscape

The cups and lids market is highly competitive, with global and regional manufacturers focusing on sustainable packaging innovation, product customization, and production expansion strategies. Leading companies are investing heavily in recyclable materials, fiber-based packaging solutions, and lightweight designs to meet evolving regulatory standards and consumer preferences. Product differentiation through custom branding, spill-resistant lids, and premium beverage packaging remains a major competitive strategy across the industry.

Huhtamaki is recognized as a leading company in the market due to its broad foodservice packaging portfolio and strong global manufacturing presence. The company continues to expand investments in sustainable packaging technologies and compostable beverage container solutions. Other key players are strengthening market position through mergers, acquisitions, and partnerships with beverage chains and quick-service restaurant operators.

Manufacturers are also investing in digital printing technologies and smart packaging innovations that improve product aesthetics and supply chain efficiency. Expansion of regional manufacturing facilities in Asia Pacific and Latin America is enabling companies to improve delivery timelines and reduce operational costs. Increased demand for eco-friendly foodservice packaging is expected to remain a central focus area for industry participants throughout the forecast period.

Key Players List

- Huhtamaki Oyj

- Dart Container Corporation

- Berry Global Inc.

- Graphic Packaging International LLC

- Pactiv Evergreen Inc.

- Genpak LLC

- International Paper Company

- Sabert Corporation

- WinCup Inc.

- Eco-Products Inc.

- Georgia-Pacific LLC

- WestRock Company

- Stora Enso Oyj

- Coveris Holdings S.A.

- Reynolds Consumer Products

- Detmold Group