Corrugated Packaging Market Size and Growth

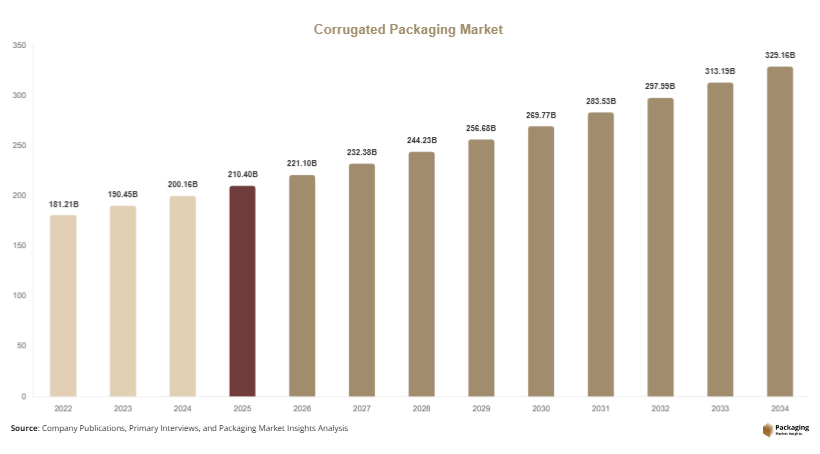

The corrugated packaging market was valued at USD 210.4 billion in 2025 and is projected to reach USD 328.6 billion by 2034, expanding at a CAGR of 5.1% from 2025 to 2034. Corrugated packaging remains a widely adopted solution across logistics, food and beverage, consumer goods, and e-commerce sectors due to its durability, recyclability, and cost efficiency. Rising global trade and the continued expansion of organized retail and digital commerce have created sustained demand for protective and lightweight packaging formats.

One of the major global factors supporting the growth of the corrugated packaging market is the rapid expansion of e-commerce fulfillment networks. Online retailers require durable, lightweight, and customizable packaging to ensure safe product delivery while minimizing transportation costs. Corrugated boxes provide an ideal combination of structural strength and sustainability, aligning with corporate packaging reduction strategies and regulatory sustainability goals. In addition, increased emphasis on recyclable materials and circular economy initiatives has reinforced the adoption of corrugated materials compared with plastic alternatives.

Key Highlights

- Asia Pacific dominated the market with a 42% share in 2025, while Latin America is expected to grow the fastest at a CAGR of 6.2% during the forecast period.

- In terms of type, single wall corrugated boxes accounted for 48% of the market in 2025, while double wall corrugated boxes are projected to expand at a CAGR of 5.8%.

- By application, food & beverage packaging held the leading share at 36%, while e-commerce packaging is expected to grow at a CAGR of 6.5%.

- The United States represented the dominant country market, valued at USD 48.7 billion in 2025 and estimated to reach USD 51.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Packaging Materials

Sustainability has become a defining trend influencing the corrugated packaging market. Governments, consumers, and brand owners are increasingly prioritizing environmentally responsible packaging materials. corrugated packaging is manufactured primarily from recycled paper and can be reused or recycled multiple times, making it compatible with circular economy frameworks. Many global consumer brands are shifting away from plastic packaging and adopting corrugated solutions to reduce environmental impact. Packaging manufacturers are also introducing lighter board grades and optimized structural designs to reduce material consumption without compromising strength. These initiatives support cost savings and sustainability targets, strengthening the adoption of corrugated packaging across industries.

Growth of Digital Printing and Custom Packaging

Digital printing technology is transforming the corrugated packaging market by enabling cost-efficient short production runs and customized designs. Companies increasingly require personalized packaging to improve brand visibility and customer engagement. Digital printing enables rapid design modifications and eliminates the need for traditional printing plates, allowing manufacturers to produce small batches economically. This capability is particularly useful for e-commerce businesses that rely on branded packaging to enhance consumer experience. As digital technologies continue to evolve, corrugated packaging manufacturers are expected to invest further in automation and advanced printing systems to improve production efficiency and design flexibility.

Market Drivers

Expansion of Global E-commerce Logistics

The rapid expansion of global e-commerce platforms continues to drive demand in the corrugated packaging market. Online retail businesses require packaging solutions that can withstand transportation stress while maintaining product integrity. corrugated boxes provide cushioning, stacking strength, and protection during shipment, making them suitable for high-volume fulfillment operations. As online shopping penetration increases across emerging economies, logistics companies are expanding distribution centers and warehouse networks. This expansion directly increases demand for corrugated boxes and protective inserts used for product shipment.

Rising Demand from Food and Beverage Industry

The food and beverage industry remains one of the major end-use sectors supporting growth in the corrugated packaging market. corrugated cartons are widely used for transporting fresh produce, processed foods, and beverages. Their lightweight structure reduces transportation costs, while their strength helps maintain product safety throughout the supply chain. In addition, corrugated packaging allows airflow for certain perishable goods, improving product shelf life during distribution. As global food production and consumption continue to rise, packaging suppliers are increasingly producing specialized corrugated packaging formats designed for food logistics and retail display.

Market Restraint

Fluctuation in Raw Material Prices

Volatility in raw material prices remains a significant challenge for the corrugated packaging market. corrugated packaging is primarily manufactured from kraft paper and containerboard, which are derived from wood pulp and recycled paper. The cost of these materials is influenced by several factors including forestry regulations, supply chain disruptions, and energy prices.

Fluctuations in pulp and recycled fiber prices can directly impact production costs for corrugated packaging manufacturers. When raw material prices increase, manufacturers may face difficulties maintaining profit margins while remaining competitive in price-sensitive markets. Additionally, supply chain disruptions related to transportation or raw material shortages can affect production schedules and inventory management.

Packaging companies often attempt to mitigate these risks through long-term supplier agreements and operational efficiency improvements. However, sustained price volatility can influence pricing strategies and create uncertainty in the corrugated packaging market outlook. As a result, companies continue to invest in recycling infrastructure and alternative fiber sources to stabilize supply and reduce reliance on virgin pulp materials.

Market Opportunities

Growth of Shelf-Ready and Retail-Ready Packaging

Retailers increasingly demand packaging formats that can move directly from transport to store shelves without additional handling. Shelf-ready packaging allows retailers to reduce labor costs and improve merchandising efficiency. corrugated packaging manufacturers are developing innovative designs that combine protective shipping functionality with retail display capability. These designs improve product visibility while maintaining structural strength during transportation. As retail chains focus on operational efficiency and faster product replenishment, demand for retail-ready corrugated packaging solutions is expected to increase.

Expansion of Packaging Demand in Emerging Economies

Emerging economies are presenting significant growth opportunities for the corrugated packaging market. Rapid urbanization, rising disposable income, and the expansion of modern retail infrastructure are increasing demand for packaged consumer goods. Countries in Asia, Latin America, and parts of Africa are witnessing growth in manufacturing and logistics industries, which directly increases demand for protective packaging materials. Corrugated packaging manufacturers are expanding production facilities in these regions to capture growing demand and reduce transportation costs. Localized production capabilities allow companies to serve regional supply chains more efficiently.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 210.4 Billion |

| Market Size in 2026 | USD 221.1 Billion |

| Market Size in 2034 | USD 328.6 Billion |

| CAGR | 5.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Single wall corrugated boxes represented the dominant subsegment with a 48% share in 2025. These boxes consist of one fluted medium placed between two linerboards, providing sufficient strength for most consumer goods packaging. Single wall boxes are widely used for shipping electronics, clothing, household items, and packaged food products. Their lightweight structure and cost efficiency make them suitable for high-volume packaging applications. The widespread availability of standardized box sizes also contributed to their leading share in the corrugated packaging market.

Double wall corrugated boxes will be the fastest-growing subsegment with a projected CAGR of 5.8% during the forecast period. These boxes contain two layers of fluting and linerboard, providing additional stacking strength and durability. Industries that transport heavy or fragile products increasingly prefer double wall boxes to ensure product safety during long-distance shipments. The growth of international trade and the need for stronger transport packaging will support expansion of this segment.

By Material

Recycled fiber materials held the largest share of approximately 64% in 2025 in the corrugated packaging market. Corrugated packaging manufacturers widely use recycled paper due to its lower cost and environmental benefits. Recycled fiber production requires less energy and water compared with virgin pulp manufacturing, making it attractive for companies focusing on sustainable operations. Strong recycling infrastructure in major economies also supports the availability of recycled materials for corrugated packaging production.

Virgin fiber materials will grow at a CAGR of around 4.9% during the forecast period. Although recycled materials dominate the market, certain applications require higher strength and durability provided by virgin fiber containerboard. Industries that ship heavy industrial products or require enhanced moisture resistance often rely on virgin fiber packaging solutions. Growing demand for high-performance packaging in industrial sectors will contribute to the expansion of this segment.

By Application

The food and beverage application segment accounted for the largest share of 36% in 2025. Corrugated packaging is widely used for transporting fruits, vegetables, beverages, and packaged food products. The material’s structural strength ensures safe transportation while its ventilation capabilities support freshness for perishable goods. Food manufacturers and distributors rely on corrugated cartons for both storage and retail distribution.

The e-commerce packaging segment will grow at the fastest CAGR of approximately 6.5% during the forecast period. Online retailers require large volumes of packaging for parcel delivery, creating significant demand for corrugated boxes and protective inserts. Packaging manufacturers are designing lightweight yet durable corrugated boxes that optimize shipping efficiency. The continued growth of online retail platforms will support expansion of this segment.

By End-Use Industry

The consumer goods industry represented the dominant share at 33% in 2025 within the corrugated packaging market. Consumer electronics, household products, and personal care items require reliable packaging solutions for storage and distribution. Corrugated packaging provides cushioning and structural integrity while enabling efficient stacking during transportation. Large-scale manufacturing of consumer goods contributes to sustained demand for corrugated packaging products.

The logistics and transportation industry will be the fastest-growing end-use segment with a CAGR of 6.0%. Logistics companies increasingly require durable packaging materials to handle rising shipment volumes. Corrugated packaging manufacturers are developing specialized solutions designed for automated warehouses and conveyor-based handling systems. Growth in global trade and supply chain networks will drive demand within this segment.

Corrugated Packaging Market Segmentations

Type

- Single Wall Corrugated Boxes

- Double Wall Corrugated Boxes

- Triple Wall Corrugated Boxes

Material

- Recycled Fiber

- Virgin Fiber

Application

- Food & Beverage Packaging

- E-commerce Packaging

- Electronics Packaging

- Industrial Packaging

- Consumer Goods Packaging

End-Use Industry

- Consumer Goods

- Food & Beverage

- Logistics & Transportation

- Electronics

- Industrial Manufacturing

Regional Analysis

North America

North America accounted for 26% of the corrugated packaging market share in 2025. The region benefited from a well-established packaging industry and high adoption of automated manufacturing technologies. During the forecast period, the regional market will grow at a CAGR of approximately 4.7% between 2025 and 2034. Growth will be supported by continued expansion of distribution networks and demand for packaging solutions across retail, manufacturing, and logistics sectors. In addition, strong recycling infrastructure in the region supports the sustainable production of corrugated materials.

The United States remained the dominant country market in North America due to its extensive logistics and retail infrastructure. The country’s growth was supported by a large network of warehouses, fulfillment centers, and transportation hubs that require high volumes of corrugated boxes. Manufacturing companies and food processors rely heavily on corrugated packaging for transportation and storage. In addition, the presence of large packaging manufacturers and technological advancements in automated packaging systems supported the country’s leadership in the regional market.

Europe

Europe represented 24% of the corrugated packaging market share in 2025. The regional market benefited from strict environmental regulations encouraging the use of recyclable packaging materials. The European market will expand at a CAGR of around 4.5% during the forecast period. Sustainability policies, waste reduction targets, and increased recycling rates are expected to support long-term demand for corrugated packaging solutions across multiple industries.

Germany dominated the European market due to its strong manufacturing sector and advanced packaging technologies. The country has a large automotive, electronics, and industrial equipment manufacturing base that requires protective packaging for shipping and export operations. Corrugated packaging manufacturers in Germany focus on producing high-quality industrial packaging solutions capable of protecting heavy or fragile goods. Continuous investment in automation and packaging innovation supported the country’s position as a leading market in the region.

Asia Pacific

Asia Pacific held the largest share of the corrugated packaging market at 42% in 2025. The region experienced strong demand from manufacturing industries, export-oriented production, and expanding retail markets. The Asia Pacific market will grow at a CAGR of approximately 5.6% between 2025 and 2034. Industrialization, infrastructure development, and rising consumer demand for packaged goods will support the region’s growth.

China emerged as the dominant country market in the region due to its extensive manufacturing sector and export activities. The country produces a wide range of consumer goods and industrial products that require protective packaging during transportation. Corrugated packaging manufacturers benefit from large-scale production facilities and established supply chains for paper and recycled fiber. Rapid growth in domestic e-commerce platforms also contributed to strong demand for corrugated boxes used in parcel shipments.

Middle East & Africa

The Middle East & Africa accounted for 4% of the global corrugated packaging market share in 2025. Although the region represents a smaller share compared with other markets, it is gradually expanding due to industrial development and increased demand for packaged goods. The regional market will grow at a CAGR of approximately 5.0% during the forecast period. Growth will be supported by investments in manufacturing facilities, logistics infrastructure, and food processing industries.

Saudi Arabia remained the leading country in the region due to its expanding industrial base and strong investments in supply chain infrastructure. Government initiatives aimed at diversifying the economy beyond oil production have encouraged growth in manufacturing and retail sectors. As domestic production increases, the demand for transport and protective packaging solutions continues to rise. Corrugated packaging manufacturers are expanding their regional presence to support industrial and consumer product distribution.

Latin America

Latin America held 4% of the corrugated packaging market share in 2025. The region has experienced steady growth in agricultural exports and consumer goods manufacturing, both of which require reliable packaging solutions. The Latin American corrugated packaging market will grow at the fastest CAGR of approximately 6.2% between 2025 and 2034. Increased industrial production and trade activities are expected to contribute to rising demand.

Brazil dominated the regional market due to its large agricultural sector and export activities. Corrugated packaging is widely used to transport fresh produce, processed foods, and industrial goods within domestic and international markets. Packaging manufacturers in Brazil are investing in modern corrugation equipment and recycling facilities to meet growing demand while improving production efficiency. These developments support the expansion of the corrugated packaging market across the region.

Competitive Landscape

The corrugated packaging market is characterized by the presence of several large multinational packaging companies along with numerous regional manufacturers. Competition is primarily based on production capacity, product innovation, sustainability initiatives, and supply chain efficiency. Major players focus on expanding corrugation facilities, improving recycling infrastructure, and introducing advanced packaging designs.

Among the industry participants, International Paper is considered a leading company in the corrugated packaging market due to its extensive global manufacturing network and strong product portfolio. The company continues to invest in sustainable packaging technologies and advanced corrugated solutions. A recent development includes expansion of automated box production capabilities to meet increasing demand from logistics and consumer goods industries.

Other companies such as WestRock, Smurfit Kappa, and DS Smith focus on strategic acquisitions and product innovations to strengthen their market position. These companies are actively expanding their geographic presence and improving manufacturing efficiency to support the growing demand for corrugated packaging solutions.

Key Players

- International Paper

- WestRock

- Smurfit Kappa

- DS Smith

- Mondi Group

- Packaging Corporation of America

- Oji Holdings Corporation

- Georgia-Pacific

- Nine Dragons Paper Holdings

- Rengo Co., Ltd.

- Pratt Industries

- KapStone Paper and Packaging

- Stora Enso

- Cascades Inc.

- Saica Group