Cork Packaging Market Size and Growth

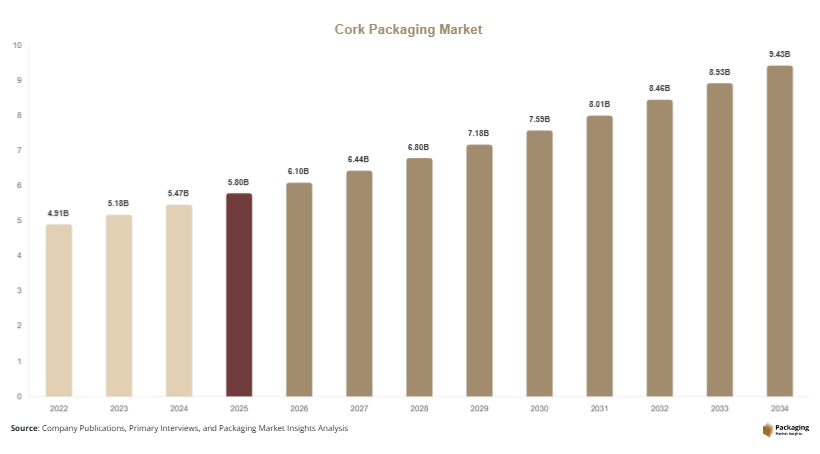

The global cork packaging market size reached approximately USD 5.8 billion in 2025 and is estimated to grow to USD 6.1 billion in 2026, with projections indicating it will achieve USD 9.4 billion by 2034, reflecting a CAGR of 5.6% from 2025 to 2034. This consistent growth is supported by rising environmental awareness, stricter packaging regulations, and growing demand for premium packaging formats across multiple industries. The global cork packaging market is steadily expanding as industries increasingly shift toward environmentally responsible materials.

Cork packaging, derived from renewable cork oak bark, offers a unique combination of sustainability, durability, and functional performance. Its biodegradable nature and recyclability position it as a preferred alternative to plastic and metal closures. In particular, industries such as wine, spirits, cosmetics, and specialty foods are increasingly adopting cork packaging to align with sustainability goals and enhance brand perception.

Market Insights:

- Asia Pacific dominated the market with a 36.8% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.4%.

- Natural cork led the type segment with a 42.7% share, while technical cork is expected to grow at a CAGR of 6.1%.

- Beverage packaging dominated with a 58.2% share, while cosmetics packaging is forecasted to grow at a CAGR of 6.3%.

- Wine applications led the segment with 47.5% share, while pharmaceutical packaging is expected to grow at a CAGR of 5.9%.

- China remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Demand for Sustainable and Biodegradable Packaging

Sustainability continues to shape the direction of the cork packaging market as industries transition toward environmentally responsible materials. Cork stands out as a renewable and biodegradable resource that aligns with global sustainability targets and corporate environmental commitments. Increasing consumer awareness regarding plastic pollution has led to a shift in purchasing behavior, encouraging brands to adopt eco-friendly packaging alternatives. Cork packaging offers a strong value proposition due to its carbon sequestration properties and minimal environmental impact throughout its lifecycle.

Major brands across beverage and cosmetics sectors are incorporating cork packaging into their sustainability strategies to improve brand image and meet regulatory requirements. The growing importance of circular economy models is further supporting the use of cork, as it can be recycled and reused without significant loss of performance. As sustainability becomes a central business priority, cork packaging is expected to witness broader adoption across multiple industries.

Advancements in Cork Processing Technologies

Technological progress in cork manufacturing is enhancing product quality and expanding its range of applications. Modern processing techniques such as micro-agglomeration and advanced sterilization methods have significantly reduced defects and contamination risks associated with natural cork. These improvements are increasing confidence among manufacturers and enabling cork to compete with synthetic alternatives.

Digital quality control systems and automated inspection technologies are also playing a crucial role in maintaining consistency and efficiency in production. Furthermore, hybrid packaging solutions that combine cork with other materials are emerging, offering improved functionality and design flexibility. These innovations are opening new opportunities for cork packaging in sectors such as pharmaceuticals and luxury cosmetics, contributing to sustained market growth.

Market Drivers

Expansion of Premium Beverage Consumption

The growth of premium beverage consumption is a key factor driving the cork packaging market. Cork closures are widely associated with quality and tradition, making them a preferred choice for high-end wine and spirits packaging. As consumers increasingly seek premium experiences, manufacturers are focusing on packaging that enhances product perception and preserves quality.

Cork’s natural elasticity and sealing properties help maintain the integrity of beverages, ensuring optimal aging conditions for wine. This functional advantage, combined with its premium appeal, supports its widespread adoption in the beverage industry. Emerging markets are also witnessing increased demand for premium alcoholic beverages due to rising disposable incomes, further strengthening the demand for cork packaging solutions.

Regulatory Push Toward Sustainable Packaging

Government regulations aimed at reducing plastic waste are significantly influencing packaging material choices. Policies promoting biodegradable and recyclable materials are encouraging manufacturers to shift toward cork packaging. These regulations are particularly stringent in developed regions, where sustainability standards are high.

Companies are increasingly adopting cork packaging to comply with environmental regulations and improve their sustainability credentials. The alignment of cork packaging with circular economy principles further supports its adoption. As regulatory frameworks continue to evolve, the demand for cork packaging is expected to increase across various industries.

Market Restraint

Limited Raw Material Availability and Cost Constraints

The cork packaging market faces challenges related to limited raw material availability and relatively high production costs. Cork is primarily sourced from specific geographic regions, which limits supply scalability. The harvesting process requires time, as cork oak trees take several years to regenerate, creating potential supply constraints.

Higher production and processing costs compared to synthetic materials can also restrict adoption, particularly in cost-sensitive markets. These challenges may lead some manufacturers to opt for alternative packaging materials such as plastic or aluminum. Despite these constraints, ongoing investments in sustainable forestry and efficient processing techniques are expected to mitigate supply challenges over time.

Market Opportunities

Growing Use in Cosmetics and Personal Care Packaging

The cosmetics and personal care industry presents strong growth potential for cork packaging. As consumers increasingly prefer sustainable and natural products, brands are adopting eco-friendly packaging solutions to enhance their market positioning. Cork packaging offers a unique aesthetic appeal that aligns with premium and organic product lines.

Its lightweight and durable properties make it suitable for packaging a variety of cosmetic products, including perfumes and skincare items. The rising demand for luxury packaging and sustainable branding strategies is expected to drive the adoption of cork packaging in this sector.

Increasing Adoption in Pharmaceutical Applications

The pharmaceutical industry is emerging as a promising application area for cork packaging. Cork’s natural resistance to moisture and microbial growth makes it suitable for specific pharmaceutical uses. Increasing emphasis on sustainable healthcare packaging is encouraging the adoption of eco-friendly materials.

Advancements in cork processing technologies are enabling its use in specialized pharmaceutical packaging formats. As the pharmaceutical industry continues to expand globally, the demand for sustainable packaging solutions is expected to create new opportunities for cork packaging manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.8 Billion |

| Market Size in 2026 | USD 6.1 Billion |

| Market Size in 2034 | USD 9.4 Billion |

| CAGR | 5.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Natural cork accounted for the largest share of the cork packaging market in 2024, contributing approximately 42.7% of total revenue. This dominance is driven by its extensive use in wine closures, where it provides superior sealing performance and supports product aging. Natural cork is also valued for its sustainability and premium perception, making it a preferred choice in high-end applications.

Technical cork is expected to witness the fastest growth, registering a CAGR of 6.1% during the forecast period. This growth is driven by advancements in manufacturing processes that enhance product consistency and reduce contamination risks. Technical cork products are increasingly used across various industries, including cosmetics and pharmaceuticals.

By Application

Beverage packaging dominated the market in 2024, accounting for 58.2% of total revenue. The widespread use of cork closures in wine and spirits packaging is the primary factor supporting this segment’s dominance. Cork’s ability to preserve product quality and enhance brand value further strengthens its position.

Cosmetics packaging is expected to grow at the fastest rate, with a CAGR of 6.3%. The increasing demand for sustainable and visually appealing packaging solutions is driving the adoption of cork in this segment. Its natural texture and eco-friendly properties align well with the preferences of modern consumers.

By End-Use

The wine industry dominated the cork packaging market in 2024, accounting for 47.5% of total revenue. Cork closures remain the preferred choice for wine packaging due to their traditional appeal and functional benefits. Strong demand for premium wines continues to support this segment.

The pharmaceutical sector is projected to grow at a CAGR of 5.9%, driven by the need for sustainable packaging solutions. Cork’s natural properties and advancements in processing technologies are enabling its use in specialized pharmaceutical applications, supporting segment growth.

Cork Packaging Market Segmentations

By Type

- Natural Cork

- Technical Cork

- Agglomerated Cork

By Application

- Beverage Packaging

- Cosmetics Packaging

- Food Packaging

- Pharmaceutical Packaging

By End-Use

- Wine Industry

- Spirits Industry

- Cosmetics Industry

- Healthcare Industry

Regional Analysis

North America

North America held a notable share of the cork packaging market in 2025, accounting for approximately 24.6% of global revenue. The region is projected to grow at a CAGR of 5.2% during the forecast period, supported by increasing demand for sustainable packaging solutions and premium beverages. The presence of established wine industries and strong distribution networks contributes to steady demand for cork closures.

The United States remains the leading country in this region, driven by high consumption of premium wines and spirits. A key growth factor is the increasing adoption of cork packaging in the cosmetics sector, where sustainability and product aesthetics are becoming critical factors influencing consumer purchasing decisions.

Europe

Europe accounted for the largest share of the cork packaging market in 2025, contributing approximately 34.2% of global revenue. The region is expected to grow at a CAGR of 5.4%, supported by strong environmental regulations and high awareness of sustainable packaging practices. Europe also benefits from being a primary producer of cork, ensuring stable supply and cost advantages.

Portugal dominates the regional market due to its extensive cork production capacity. The strong tradition of wine consumption and production acts as a major growth factor, sustaining high demand for cork closures. Additionally, the presence of established cork manufacturers supports continuous innovation and market expansion.

Asia Pacific

Asia Pacific emerged as a rapidly growing region in the cork packaging market, capturing 36.8% of global share in 2025 and expected to grow at a CAGR of 6.0%. The region’s growth is driven by increasing urbanization, rising disposable incomes, and expanding demand for premium products.

China leads the regional market due to its growing wine consumption and packaging industry. A significant growth factor is the increasing adoption of sustainable packaging solutions, supported by government initiatives and rising consumer awareness regarding environmental issues.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.5% of the cork packaging market in 2025 and is expected to grow at a CAGR of 5.1%. Growth is supported by rising demand for premium products and gradual adoption of sustainable packaging solutions.

South Africa is a key contributor to the regional market, supported by its established wine industry. Increasing wine exports serve as a major growth factor, driving demand for high-quality cork closures and supporting market development.

Latin America

Latin America held a share of approximately 9.9% in 2025 and is projected to grow at the fastest CAGR of 6.4%. The region’s growth is driven by expanding wine production and increasing awareness of sustainable packaging solutions.

Brazil dominates the market in this region, supported by its growing beverage industry. A key growth factor is the increasing export of premium beverages, which requires high-quality and sustainable packaging solutions such as cork.

Competitive Landscape

The cork packaging market is characterized by moderate competition, with several key players focusing on innovation, sustainability, and expansion strategies. Companies are investing in advanced processing technologies to improve product quality and meet evolving industry requirements. Strategic partnerships and acquisitions are also common as players aim to strengthen their market presence.

Amorim Group remains a leading player in the market, supported by its extensive product portfolio and strong global presence. The company has recently introduced advanced quality control technologies to enhance product reliability and reduce defects. Other companies are focusing on expanding their production capacities and developing new applications for cork packaging to remain competitive.

Key Players List

- Amorim Group

- Cork Supply Group

- Diam Bouchage

- M.A. Silva

- WidgetCo

- Jelinek Cork Group

- Lafitte Cork & Capsule

- Sugherificio Molinas

- Bangor Cork

- Natural Cork Company

- Portocork

- Vinventions

- Precision Elite Limited

- Crown Cork & Seal

- Intercork