Containerboard Market Size and Growth

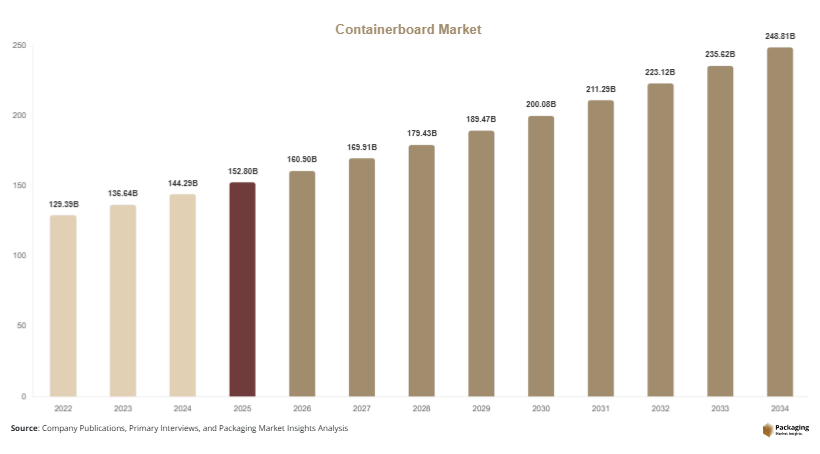

The global containerboard market was valued at USD 152.8 billion in 2025 and is projected to reach USD 160.9 billion in 2026. The market is expected to attain USD 248.7 billion by 2034, registering a CAGR of 5.6% during the forecast period from 2025 to 2034. The market is experiencing consistent growth due to rising e-commerce shipments, increasing demand for sustainable packaging materials, and expanding industrial production across developing economies.

Containerboard is widely utilized for manufacturing corrugated boxes, folding cartons, protective packaging, and industrial transport packaging. Growing global trade activities and rapid expansion of online retail platforms are significantly increasing the demand for corrugated packaging products. Businesses across food & beverage, electronics, healthcare, and consumer goods sectors are increasingly adopting lightweight and recyclable containerboard materials to improve packaging efficiency and reduce environmental impact.

Key Market Insights

- Asia Pacific dominated the containerboard market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4% during the forecast period.

- Kraft liner led the type segment with a 34.8% market share.

- Virgin fiber-based containerboard dominated the material segment with a 57.2% share.

- Food & beverage applications accounted for 42.5% of total market share.

- The US remained the dominant country in North America with a market size of USD 31.4 billion in 2025 and USD 33.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable Corrugated Packaging Solutions

Sustainability has become one of the most influential trends in the containerboard market. Packaging manufacturers and consumer goods companies are increasingly shifting toward recyclable and biodegradable packaging materials to reduce environmental impact and comply with stricter sustainability regulations. Containerboard products are gaining strong acceptance because they are recyclable, renewable, and suitable for circular economy initiatives.

Major retailers and e-commerce companies are replacing plastic shipping materials with corrugated packaging made from recycled containerboard. For example, food delivery and online grocery platforms are increasingly utilizing lightweight corrugated boxes that reduce transportation emissions and improve recyclability. Paper manufacturers are also investing in closed-loop recycling systems that improve fiber recovery and reduce raw material consumption. Future growth of sustainable packaging mandates across North America and Europe is expected to accelerate adoption of environmentally friendly containerboard products throughout global supply chains.

Increasing Automation in Corrugated Packaging Production

Automation and digitalization are transforming containerboard manufacturing and corrugated packaging operations. Packaging companies are integrating robotic handling systems, automated cutting technologies, and digital printing solutions to improve operational efficiency and reduce production costs. Automated manufacturing systems also enable companies to produce customized packaging solutions for different industries with greater speed and precision.

Digital printing technologies are becoming increasingly popular in corrugated packaging because they support short production runs, personalized branding, and improved graphics quality. For example, electronics and food companies are adopting digitally printed corrugated packaging for promotional campaigns and retail-ready packaging applications. Automation also improves inventory management and reduces material waste in large-scale packaging facilities. Over the next decade, advanced smart manufacturing systems are expected to increase production efficiency and strengthen profit margins for containerboard manufacturers.

Market Drivers

Rapid Expansion of Global E-Commerce Industry

The rapid growth of the global e-commerce industry is a major driver supporting the containerboard market. Increasing online shopping activities are generating substantial demand for corrugated boxes and protective packaging materials used in shipping and logistics operations. E-commerce packaging requires durable, lightweight, and cost-efficient materials capable of protecting products during transportation and warehousing.

Large online retail companies are increasingly utilizing customized corrugated packaging solutions to improve customer experience and reduce shipping damage. For instance, electronics, apparel, and grocery delivery platforms rely heavily on containerboard packaging due to its high strength and recyclability. The expansion of cross-border e-commerce trade has further accelerated demand for export-grade corrugated packaging products. Growth in same-day delivery services and rising consumer demand for sustainable packaging are expected to continue driving strong market expansion during the forecast period.

Increasing Demand from Food and Beverage Packaging Industry

The food and beverage industry is another significant driver of the containerboard market. Rising consumption of packaged foods, beverages, and ready-to-eat products is increasing demand for corrugated transport packaging and retail-ready display boxes. Food manufacturers prefer containerboard packaging because it provides product protection, easy stacking, and strong printability for branding applications.

The growth of supermarket chains, organized retail stores, and food delivery services is also contributing to higher containerboard consumption. Beverage manufacturers are increasingly adopting corrugated multipack cartons and shelf-ready packaging formats to improve logistics efficiency and reduce packaging waste. For example, fruit exporters and processed food companies widely utilize moisture-resistant corrugated boxes to maintain product quality during transportation. Continued expansion of food processing industries across emerging economies is expected to strengthen long-term demand for containerboard packaging solutions.

Market Restraint

Volatility in Raw Material and Energy Costs

Fluctuating raw material and energy prices remain a significant restraint for the containerboard market. The industry relies heavily on wood pulp, recycled paper, chemicals, and energy-intensive production processes, making manufacturers vulnerable to cost volatility. Changes in global pulp supply, recycling collection rates, and fuel prices can significantly impact manufacturing expenses and profit margins.

Recycled fiber shortages and increasing transportation costs are creating additional operational challenges for packaging producers. Smaller manufacturers often face difficulties maintaining stable production costs during periods of raw material inflation. For example, disruptions in recovered paper supply chains can increase recycled fiber prices and affect production planning for corrugated packaging manufacturers. Rising electricity and natural gas costs in Europe and parts of Asia are also increasing operational expenses for paper mills. These challenges may limit pricing flexibility and create profitability pressures across the global containerboard industry despite growing long-term demand.

Market Opportunities

Growth of Recycled Fiber-Based Packaging Solutions

The increasing adoption of recycled fiber packaging presents substantial opportunities for containerboard manufacturers. Governments and businesses are emphasizing waste reduction and circular economy initiatives, encouraging broader utilization of recycled paper materials in packaging production. Recycled containerboard solutions reduce dependence on virgin wood pulp and support sustainability goals across multiple industries.

Packaging manufacturers are investing in advanced recycling technologies that improve fiber quality and enable production of high-strength recycled containerboard products. Retail companies and consumer goods brands are increasingly requesting packaging made from post-consumer recycled content to improve environmental performance. Future expansion of recycling infrastructure in developing economies is expected to create additional opportunities for recycled containerboard production and export activities.

Expanding Industrialization in Emerging Economies

Rapid industrial growth across emerging economies is generating strong opportunities for the containerboard market. Countries such as India, Vietnam, Indonesia, Brazil, and Mexico are witnessing increasing manufacturing output, retail expansion, and export activities that require efficient transport packaging solutions. Growth in automotive, electronics, pharmaceuticals, and consumer goods industries is increasing demand for corrugated industrial packaging.

Governments are also investing heavily in logistics infrastructure, warehousing facilities, and industrial corridors that support packaging demand. For example, industrial manufacturers in Southeast Asia are increasing exports of consumer electronics and appliances packaged in corrugated containerboard boxes. Rising urbanization and increasing disposable income levels are expected to further strengthen packaged goods consumption and create sustained opportunities for containerboard suppliers over the next decade.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 152.8 Billion |

| Market Size in 2026 | USD 160.9 Billion |

| Market Size in 2034 | USD 248.7 Billion |

| CAGR | 5.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Kraft liner dominated the containerboard market in 2024 with a market share of 34.8%. The segment’s dominance is attributed to its high strength, superior durability, and widespread use in corrugated packaging applications. Kraft liner is primarily manufactured from virgin wood fibers, enabling it to provide excellent tear resistance and stacking performance for industrial transport packaging. Industries such as food & beverage, electronics, automotive, and e-commerce rely heavily on kraft liner-based corrugated boxes for safe product transportation and storage. The growing demand for export-grade packaging has further strengthened the adoption of kraft liner products due to their ability to withstand long-distance shipping conditions. Packaging manufacturers are also developing lightweight kraft liner solutions that reduce transportation costs while maintaining structural integrity. Increasing global trade activities and expansion of organized retail distribution networks continue to support stable demand for kraft liner containerboard products.

Recycled containerboard is projected to witness the fastest growth, registering a CAGR of 6.7% during the forecast period. The segment is gaining strong momentum because industries are increasingly prioritizing sustainable packaging materials with lower environmental impact. Recycled containerboard products are manufactured using recovered paper fibers and support circular economy objectives by reducing landfill waste and dependence on virgin raw materials. Retailers and consumer goods companies are actively adopting recycled corrugated packaging to meet sustainability commitments and comply with environmental regulations. Technological advancements in fiber recovery and recycling processes are also improving the strength and quality of recycled containerboard products. Growing investments in paper recycling infrastructure across Asia Pacific and Europe are expected to accelerate future segment expansion significantly.

By Material

Virgin fiber-based containerboard held the largest market share of 57.2% in 2024 due to its superior strength, consistency, and performance in heavy-duty packaging applications. Virgin fiber materials provide better compression resistance and durability compared to recycled fibers, making them suitable for industrial transport packaging and export logistics. Food manufacturers, electronics companies, and automotive suppliers increasingly utilize virgin fiber containerboard because it offers reliable protection during storage and long-distance transportation. The segment also benefits from strong demand for premium packaging solutions with improved print quality and moisture resistance. Packaging companies continue investing in advanced pulp processing technologies that enhance paper quality and reduce material consumption. Increasing international trade and rising demand for durable corrugated packaging solutions are expected to sustain strong adoption of virgin fiber-based containerboard products throughout the forecast period.

Recycled fiber-based containerboard is anticipated to expand at the fastest CAGR of 6.9% through 2034. Growth in this segment is being driven by rising environmental awareness and increasing pressure to reduce packaging waste across global industries. Governments and environmental organizations are promoting recycled packaging adoption through stricter sustainability regulations and recycling targets. Recycled fiber containerboard is increasingly used for e-commerce shipping boxes, food delivery packaging, and retail display cartons due to its lower carbon footprint. Packaging manufacturers are also introducing high-strength recycled paper grades that improve performance while maintaining sustainability benefits. Future growth is expected to accelerate further as brands continue transitioning toward environmentally responsible packaging systems.

By End-Use

Food & beverage applications accounted for the largest share of the containerboard market in 2024, representing 42.5% of total revenue. The segment’s dominance is primarily driven by rising demand for packaged food products, beverages, fresh produce transportation, and retail-ready corrugated packaging. Food manufacturers widely utilize corrugated boxes because they provide product protection, ventilation, and easy handling throughout distribution networks. Increasing supermarket expansion and growth in food delivery services are further strengthening demand for containerboard packaging products. Beverage companies are also increasingly adopting corrugated multipack cartons and shelf-ready display boxes to improve logistics efficiency and reduce plastic packaging usage. Growth in agricultural exports and processed food manufacturing across emerging economies continues to support higher consumption of food-grade containerboard solutions globally.

E-commerce packaging is projected to witness the fastest growth, expanding at a CAGR of 7.1% during the forecast period. The rapid increase in online shopping activities and parcel delivery volumes is significantly driving demand for corrugated shipping boxes and protective packaging materials. E-commerce companies require lightweight, durable, and customizable packaging solutions capable of handling high transportation volumes and automated logistics operations. Retailers are increasingly investing in right-sized corrugated packaging designs that reduce shipping costs and improve sustainability performance. Technological innovations such as digitally printed corrugated boxes and smart packaging labels are also gaining traction in online retail logistics. Continued expansion of cross-border e-commerce trade and same-day delivery services is expected to create strong long-term opportunities for containerboard manufacturers.

Containerboard Market Segmentations

By Type

- Kraft Liner

- Test Liner

- Fluting Medium

- Recycled Containerboard

- White Top Liner

By Material

- Virgin Fiber

- Recycled Fiber

- Mixed Fiber

By End-User

- Food & Beverage

- E-Commerce

- Consumer Goods

- Electronics

- Industrial Packaging

Regional Analysis

North America

North America accounted for 27.8% of the global containerboard market share in 2025 and is projected to register a CAGR of 5.1% through 2034. The region benefits from advanced packaging infrastructure, strong e-commerce penetration, and high demand for sustainable packaging solutions. Corrugated packaging demand continues to rise due to increasing online retail shipments and expanding food delivery services throughout the United States and Canada. Packaging companies across the region are investing in lightweight containerboard grades and automated corrugated box manufacturing technologies to improve operational efficiency. Additionally, sustainability regulations encouraging recyclable packaging materials are supporting wider adoption of paper-based transport packaging across consumer goods industries.

The United States remained the dominant country in North America due to its extensive retail and logistics network. One of the key growth drivers in the country is the expansion of e-commerce warehousing and fulfillment operations. Major online retailers are increasingly utilizing customized corrugated packaging systems to improve product protection and reduce shipping costs. For example, grocery delivery and electronics companies are adopting high-strength corrugated packaging solutions designed for automated logistics operations. Increasing demand for recyclable shipping materials and growth in packaged food exports are expected to continue supporting market expansion throughout the forecast period.

Europe

Europe represented 24.2% of the global containerboard market in 2025 and is anticipated to grow at a CAGR of 4.9% during the forecast period. The region’s market growth is primarily driven by stringent sustainability policies, rising recycled packaging adoption, and increasing retail packaging demand. European packaging manufacturers are focusing heavily on recyclable and fiber-based packaging alternatives to comply with environmental regulations aimed at reducing plastic waste. Demand for shelf-ready corrugated packaging and customized retail display boxes is also increasing among supermarkets and consumer goods companies. Furthermore, growth in pharmaceutical logistics and food exports is strengthening the requirement for durable containerboard packaging across regional supply chains.

Germany emerged as the dominant country in the European market due to its strong manufacturing base and advanced paper recycling infrastructure. A major growth driver in Germany is the increasing demand for sustainable industrial packaging within automotive and machinery export sectors. Manufacturers are utilizing high-performance corrugated packaging to improve transportation safety and reduce material waste. For instance, automotive suppliers increasingly rely on recyclable corrugated packaging systems for shipping spare parts and industrial equipment across Europe. The country’s strong focus on circular economy initiatives is expected to further accelerate recycled containerboard adoption in the coming years.

Asia Pacific

Asia Pacific dominated the global containerboard market with a 38.6% market share in 2025 and is expected to register a CAGR of 6.2% through 2034. Rapid industrialization, expanding manufacturing activities, and strong retail sector growth are driving substantial demand for corrugated packaging products across the region. Rising urbanization and increasing disposable income levels are encouraging higher consumption of packaged foods, electronics, and household products, thereby supporting containerboard demand. The region also benefits from growing export-oriented industries that require reliable and cost-efficient transport packaging solutions. Increasing investments in recycling infrastructure and paper manufacturing facilities are further strengthening regional production capabilities.

China remained the leading country in Asia Pacific due to its large-scale manufacturing industry and strong export economy. One of the primary growth drivers in China is the rapid expansion of e-commerce logistics and industrial packaging demand. Packaging manufacturers are investing in automated corrugated box production facilities to meet rising requirements from electronics, consumer goods, and food delivery sectors. For example, Chinese export manufacturers increasingly utilize lightweight corrugated packaging designed for international shipping efficiency. India is also emerging as a significant contributor due to increasing organized retail expansion and rising consumption of packaged consumer products.

Middle East & Africa

The Middle East & Africa accounted for 4.9% of the global containerboard market share in 2025 and is projected to grow at a CAGR of 5.7% during the forecast period. Increasing investments in food processing industries, retail infrastructure, and logistics development are supporting market expansion across the region. Governments are promoting domestic manufacturing and industrial diversification strategies that require efficient transport packaging solutions. Corrugated packaging demand is also increasing due to rising imports of consumer goods and growth in organized retail chains. Additionally, expansion of cold chain logistics and agricultural exports is encouraging the use of moisture-resistant containerboard products.

Saudi Arabia emerged as the dominant country within the region due to growing industrial investments and expanding food packaging demand. One of the key growth drivers is the development of local food manufacturing and distribution networks supported by economic diversification initiatives. Packaging suppliers are increasing production of corrugated boxes used for processed food, beverages, and pharmaceutical transport applications. For example, regional logistics providers are adopting stronger corrugated packaging materials for long-distance transportation across Gulf markets. South Africa is also witnessing rising demand due to increasing agricultural exports and growth in retail packaging consumption.

Latin America

Latin America held 4.5% of the global containerboard market in 2025 and is forecasted to record the fastest CAGR of 6.4% through 2034. Expanding consumer goods industries, rising retail modernization, and growing agricultural exports are driving strong demand for corrugated packaging products throughout the region. Increasing urban populations and rising e-commerce activities are encouraging broader use of lightweight and recyclable shipping materials. Governments are also supporting paper recycling initiatives to reduce packaging waste and strengthen domestic paper manufacturing industries.

Brazil remained the dominant country in the Latin American market due to its large agricultural and food processing industries. One major growth driver in Brazil is the increasing export of fruits, beverages, and processed foods requiring durable corrugated packaging for transportation. Packaging manufacturers are investing in moisture-resistant containerboard solutions suitable for export logistics and cold chain applications. For example, beverage producers and food exporters are increasingly utilizing recyclable corrugated multipack cartons to improve product handling efficiency. Mexico is also experiencing strong market growth due to expanding automotive manufacturing and cross-border trade activities with North America.

Competitive Landscape

The containerboard market is highly competitive, with leading companies focusing on production capacity expansion, sustainable packaging innovation, and strategic acquisitions to strengthen market presence. Major players are investing heavily in recycled fiber technologies, lightweight paper solutions, and automated corrugated packaging systems to improve operational efficiency and meet evolving customer requirements.

International Paper remains one of the leading companies in the market due to its extensive global manufacturing network and strong corrugated packaging portfolio. The company continues expanding recycled containerboard production and investing in sustainable forestry initiatives. Smurfit Westrock is also strengthening its market position through innovative recyclable packaging solutions and integrated paper recycling operations.

Packaging Corporation of America has increased investments in corrugated box manufacturing facilities to support rising e-commerce demand across North America. Mondi Group continues focusing on fiber-based sustainable packaging innovations for industrial and retail applications. DS Smith is expanding circular economy packaging solutions and digital packaging technologies designed for e-commerce and retail sectors. Competition within the market is expected to intensify as manufacturers prioritize sustainability, automation, and lightweight packaging development.

Key Players List

- International Paper

- Smurfit Westrock

- Packaging Corporation of America

- Mondi Group

- DS Smith

- Nine Dragons Paper

- Oji Holdings Corporation

- Stora Enso

- Lee & Man Paper

- Klabin S.A.

- Georgia-Pacific

- Rengo Co., Ltd.

- Nippon Paper Industries

- WestRock Company

- Saica Group