Consumer Goods Packaging Market Size and Growth

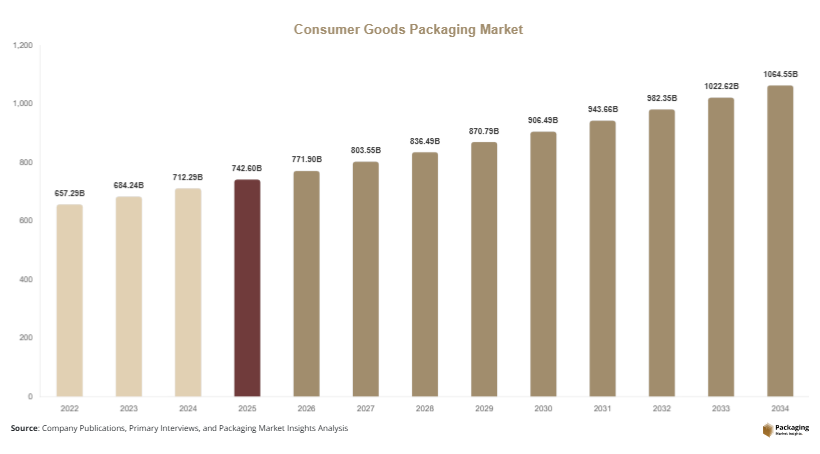

The global consumer goods packaging market was valued at USD 742.6 billion in 2025 and is estimated to reach USD 771.9 billion in 2026. The market is projected to reach USD 1,068.4 billion by 2034, expanding at a CAGR of 4.1% during the forecast period from 2025 to 2034. The market is experiencing steady growth due to rising demand for packaged consumer products, rapid expansion of e-commerce retail channels, and increasing investments in sustainable packaging technologies. Consumer goods packaging includes rigid and flexible packaging solutions used across food, beverages, personal care, household products, healthcare, electronics, and retail sectors. Manufacturers continue to focus on lightweight materials, recyclable packaging formats, and digital printing technologies to improve operational efficiency and strengthen brand visibility.

The expansion of organized retail and online shopping platforms has significantly increased the demand for durable and visually attractive packaging. Consumer brands are investing in advanced packaging materials that improve product shelf life, reduce transportation costs, and support sustainability targets. Flexible packaging, recyclable paperboard cartons, and mono-material plastics are becoming widely adopted across multiple consumer product categories. The growing preference for convenience-oriented products, especially among urban populations, is also supporting market expansion. Single-serve packaging, resealable pouches, and smart labeling technologies are increasingly integrated into packaging systems for enhanced consumer engagement.

Key Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 5.4%.

- Flexible packaging led the type segment with a 34.8% share.

- Plastic packaging dominated with a 46.7% share.

- Food & beverage applications led the segment with 41.6% share.

- The US remained the dominant country with a market size of USD 118.4 billion in 2025 and USD 123.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Recyclable Packaging

Sustainability has become one of the most influential trends shaping the consumer goods packaging market. Consumer brands are increasingly replacing multi-layer plastic packaging with recyclable paperboard, biodegradable films, and mono-material flexible packaging solutions. Governments across Europe and North America are introducing stricter packaging waste regulations, encouraging manufacturers to reduce virgin plastic consumption and improve recycling rates. Large retail companies are also implementing packaging reduction targets to strengthen their environmental commitments.

For example, consumer product companies in the beverage and personal care sectors are shifting toward refill pouches and reusable containers to reduce packaging waste. Several food brands are introducing paper-based snack packaging and compostable delivery packaging for e-commerce shipments. This trend is expected to accelerate investments in bio-based polymers, water-based inks, and recyclable barrier coatings. Over the next decade, sustainable packaging innovation is expected to become a key competitive factor for packaging manufacturers and consumer goods brands.

Growth of Smart and Digitally Connected Packaging

The integration of smart technologies into consumer goods packaging is gaining traction across food, healthcare, and personal care industries. Smart packaging solutions include QR codes, RFID labels, temperature-sensitive indicators, and interactive labels that improve supply chain visibility and consumer engagement. Companies are increasingly using digital packaging tools to provide product authentication, traceability, and personalized marketing experiences.

For instance, beverage companies are incorporating QR-enabled labels that allow consumers to access nutritional information and promotional campaigns through smartphones. Electronics and healthcare packaging manufacturers are also using RFID-enabled packaging to monitor inventory movement and reduce counterfeit risks. The future impact of this trend is expected to be substantial as retailers and brands adopt digital supply chain management systems. Smart packaging technologies are likely to improve operational efficiency, reduce product losses, and support data-driven marketing strategies across the consumer goods sector.

Market Drivers

Expansion of E-Commerce and Organized Retail

The rapid growth of e-commerce platforms and organized retail networks is significantly driving demand in the consumer goods packaging market. Online retailing requires durable and lightweight packaging solutions capable of protecting products during transportation and warehousing operations. Consumer brands are increasing investments in corrugated boxes, flexible pouches, and protective cushioning materials to support rising online order volumes.

Large e-commerce companies are also demanding sustainable and cost-efficient shipping packaging to reduce logistics expenses. For example, electronics and cosmetics companies are using lightweight molded fiber packaging and recyclable corrugated cartons to optimize shipping efficiency. The growth of direct-to-consumer business models is increasing the importance of visually attractive packaging designs that enhance customer experience. As global online retail sales continue to expand, packaging manufacturers are expected to witness rising demand for customized and high-performance packaging formats.

Rising Consumption of Packaged Food and Household Products

Urbanization, changing lifestyles, and rising disposable income levels are increasing global demand for packaged consumer products. Consumers are increasingly purchasing ready-to-eat meals, frozen foods, beverages, and household cleaning products due to convenience and time-saving benefits. This trend is driving strong demand for packaging solutions that offer extended shelf life, product protection, and easy handling.

Food manufacturers are investing in high-barrier films and resealable packaging systems to maintain freshness and improve portability. Household product companies are also introducing concentrated refill packs to reduce packaging material usage and improve transportation efficiency. Emerging economies such as India, Indonesia, and Brazil are witnessing rapid growth in packaged consumer product consumption due to expanding urban populations and retail infrastructure. This shift is expected to sustain long-term demand for flexible, rigid, and paper-based packaging solutions.

Market Restraint

Fluctuating Raw Material Prices and Recycling Challenges

Volatility in raw material prices remains a major restraint for the consumer goods packaging market. Packaging manufacturers rely heavily on petroleum-based plastics, paper pulp, aluminum, and specialty chemicals, all of which are vulnerable to price fluctuations caused by supply chain disruptions and changing energy costs. Rising transportation expenses and labor shortages are also increasing operational costs for packaging producers.

Another challenge involves the limited recycling infrastructure available in several emerging economies. Multi-layer plastic packaging and mixed-material packaging formats are difficult to recycle efficiently, creating waste management concerns. For example, flexible snack packaging often contains multiple polymer layers that complicate sorting and recycling processes. Environmental organizations and regulators are placing pressure on packaging companies to improve recyclability and reduce landfill waste. These challenges may increase compliance costs and slow the adoption of certain packaging materials. Smaller manufacturers, particularly in developing markets, may struggle to invest in advanced recycling systems and sustainable material innovations.

Market Opportunities

Growth in Biodegradable and Compostable Packaging

The increasing focus on environmental sustainability is creating major opportunities for biodegradable and compostable packaging materials. Consumer brands are actively searching for alternatives to conventional plastic packaging due to rising regulatory pressure and changing consumer preferences. Packaging manufacturers are investing in plant-based polymers, compostable films, and biodegradable coatings to address sustainability requirements.

Food delivery companies and retail chains are increasingly adopting compostable packaging for takeaway meals, grocery deliveries, and fresh produce packaging. Several personal care companies are also introducing paper-based refill systems and biodegradable sachets. Future growth opportunities are expected to emerge in regions implementing stricter single-use plastic bans. Advances in material science and industrial composting infrastructure are likely to improve the commercial viability of biodegradable packaging over the forecast period.

Expansion of Smart Packaging Applications

The increasing adoption of digital technologies in retail and supply chain management is creating growth opportunities for smart packaging solutions. Smart labels, NFC-enabled packaging, and sensor-based packaging systems are helping companies improve inventory tracking and customer interaction. Consumer brands are using connected packaging to deliver product information, promotional content, and authentication services directly to consumers.

Healthcare and food industries are expected to become major adopters of intelligent packaging systems due to rising concerns regarding product safety and traceability. Temperature-sensitive labels and freshness indicators are becoming increasingly important for cold-chain logistics and pharmaceutical packaging applications. As artificial intelligence and IoT technologies continue to expand across manufacturing and logistics operations, smart packaging solutions are expected to become more affordable and widely adopted across consumer goods industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 742.6 Billion |

| Market Size in 2026 | USD 771.9 Billion |

| Market Size in 2034 | USD 1,068.4 Billion |

| CAGR | 4.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flexible packaging dominated the consumer goods packaging market in 2024 with a market share of 34.8%. The segment continues to lead due to its lightweight structure, lower transportation costs, and high adaptability across food, personal care, and household product applications. Flexible packaging formats such as stand-up pouches, sachets, wraps, and resealable bags are widely used because they improve shelf life while reducing storage space requirements. Food manufacturers increasingly prefer multilayer flexible films for snacks, dairy products, and frozen foods due to strong barrier protection and printing flexibility. Personal care brands are also shifting toward refill pouches and travel-sized packaging formats to meet changing consumer preferences. The growth of e-commerce has further strengthened demand for durable flexible packaging solutions that minimize shipping damage while maintaining cost efficiency. In addition, advancements in recyclable mono-material flexible packaging are supporting long-term adoption among sustainability-focused brands.

Smart packaging is projected to be the fastest-growing type segment, expanding at a CAGR of 6.1% during the forecast period. Growth is driven by increasing integration of digital technologies into consumer packaging systems. Smart labels, RFID-enabled packaging, freshness indicators, and QR code solutions are gaining popularity among food, pharmaceutical, and cosmetic manufacturers. Retail companies are using connected packaging to improve inventory visibility and enhance consumer engagement through personalized digital experiences. For example, beverage brands are implementing interactive labels that provide nutritional data and promotional campaigns through smartphone scanning. The rise of counterfeit prevention technologies in cosmetics and electronics packaging is also accelerating smart packaging demand. Future developments in IoT integration and real-time supply chain monitoring are expected to create new growth opportunities for intelligent packaging solutions across multiple industries.

By Material

Plastic packaging accounted for the largest share of the consumer goods packaging market in 2024, representing 46.7% of total revenue. Plastic materials continue to dominate due to their durability, lightweight properties, affordability, and strong barrier protection capabilities. PET, polyethylene, and polypropylene remain widely used across beverage bottles, food containers, household cleaning product packaging, and personal care packaging. Plastic packaging offers cost advantages for manufacturers while supporting large-scale production requirements. Beverage companies continue to rely on PET bottles for water, carbonated drinks, and juices due to their transportation efficiency and design flexibility. Flexible plastic films are also heavily used in snack foods and frozen food applications. Furthermore, recycled plastic content integration is increasing as companies seek to meet sustainability goals and reduce virgin plastic consumption. Packaging manufacturers are investing in chemical recycling and advanced resin technologies to improve the recyclability of plastic packaging materials.

Paper-based packaging is expected to witness the fastest growth during the forecast period, registering a CAGR of 5.8%. Growing environmental awareness and government restrictions on single-use plastics are encouraging the transition toward paperboard cartons, molded fiber packaging, and corrugated boxes. Food delivery services, e-commerce retailers, and consumer goods brands are increasingly replacing plastic packaging with recyclable paper alternatives. Corrugated packaging demand is particularly rising due to expansion in online retail and shipping activities. Consumer electronics companies are also reducing plastic inserts and introducing fiber-based cushioning materials for product protection. Advances in water-resistant coatings and barrier technologies are improving the functionality of paper packaging across food and beverage applications. Future investments in sustainable forestry practices and recycling infrastructure are expected to support continued growth in paper-based packaging adoption worldwide.

By End-Use

Food and beverage applications dominated the consumer goods packaging market in 2024 with a market share of 41.6%. The segment benefits from rising global consumption of packaged snacks, dairy products, ready-to-eat meals, bottled beverages, and frozen foods. Packaging plays a critical role in preserving freshness, extending shelf life, and ensuring safe transportation across food supply chains. Flexible films, corrugated boxes, PET containers, and metal cans are widely used across the sector due to their strong protective properties. The expansion of online grocery delivery services is further increasing demand for lightweight and durable food packaging solutions. Beverage manufacturers are also investing in sustainable packaging formats such as recyclable aluminum cans and tethered bottle caps to comply with environmental regulations. Emerging economies are witnessing significant growth in packaged food demand due to urbanization, changing dietary habits, and increasing disposable income levels.

Personal care packaging is projected to be the fastest-growing end-use segment, expanding at a CAGR of 5.7% through 2034. Growth is supported by rising consumer spending on skincare, cosmetics, haircare, and hygiene products. Premiumization trends in beauty and wellness industries are increasing demand for visually attractive and innovative packaging solutions. Cosmetic brands are adopting airless pumps, refillable packaging systems, and eco-friendly containers to strengthen brand differentiation and sustainability positioning. E-commerce growth is also influencing packaging design, as companies require protective yet lightweight solutions for direct-to-consumer shipments. For example, skincare brands are increasingly using recyclable glass jars and biodegradable cartons to appeal to environmentally conscious consumers. Future growth opportunities are expected to emerge from smart cosmetic packaging featuring digital authentication and personalized consumer interaction technologies.

Consumer Goods Packaging Market Segmentations

By Type

- Rigid Packaging

- Flexible Packaging

- Semi-Rigid Packaging

- Protective Packaging

By Material

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Biodegradable Materials

By End-User

- Food & Beverage

- Personal Care & Cosmetics

- Household Products

- Consumer Electronics

- Healthcare & Pharmaceuticals

- E-commerce & Retail

Regional Analysis

North America

North America accounted for 24.8% of the consumer goods packaging market share in 2025 and is projected to expand at a CAGR of 3.9% through 2034. The region benefits from strong demand for sustainable packaging, advanced retail infrastructure, and high packaged food consumption. E-commerce growth across the United States and Canada continues to support demand for corrugated packaging and flexible protective materials. Companies are increasingly investing in recyclable plastic packaging and lightweight paperboard solutions to comply with sustainability targets. Rising investments in automation and smart manufacturing technologies are also strengthening packaging production efficiency across the region.

The United States remained the dominant country in North America due to high consumer spending and strong packaged food demand. A major growth driver in the country is the rapid expansion of direct-to-consumer brands that require customized and visually appealing packaging solutions. Beverage companies are increasingly adopting recyclable aluminum cans and fiber-based carriers to reduce environmental impact. Retailers are also implementing packaging reduction initiatives to improve sustainability performance. Growth in subscription-based consumer product delivery services continues to create demand for durable shipping packaging and smart labeling technologies.

Europe

Europe represented 22.3% of the global consumer goods packaging market in 2025 and is expected to grow at a CAGR of 4.0% during the forecast period. The region is characterized by strict environmental regulations and strong adoption of recyclable packaging materials. Countries across Europe are introducing extended producer responsibility policies that encourage packaging waste reduction and recycling improvements. Demand for fiber-based packaging, reusable containers, and compostable materials continues to rise across food and household product industries.

Germany remained the leading market within Europe due to its advanced manufacturing sector and established recycling infrastructure. A key growth driver in Germany is the increasing adoption of circular economy packaging systems by consumer goods companies. Retail chains are replacing conventional plastic trays with molded fiber alternatives and recyclable mono-material films. Demand for premium cosmetic and pharmaceutical packaging is also supporting investments in digital printing and lightweight packaging technologies. Export-oriented consumer goods manufacturing further contributes to stable packaging demand across the region.

Asia Pacific

Asia Pacific dominated the consumer goods packaging market with a 39.2% share in 2025 and is projected to grow at a CAGR of 5.1% through 2034. The region benefits from rapid urbanization, expanding middle-class populations, and large-scale manufacturing activities. Rising consumption of packaged foods, beverages, cosmetics, and household products is creating substantial demand for flexible and rigid packaging solutions. The expansion of e-commerce platforms in China, India, and Southeast Asia is also accelerating packaging demand across logistics and retail sectors.

China remained the dominant country in Asia Pacific due to its large consumer goods manufacturing base and extensive export activities. A major growth driver in the country is the expansion of automated packaging production facilities focused on cost efficiency and sustainability. Chinese manufacturers are increasing investments in recyclable plastic packaging and high-speed flexible packaging systems. Government support for green manufacturing and waste reduction programs is further encouraging sustainable packaging innovation. The country’s strong food processing and personal care industries continue to support long-term market growth.

Middle East & Africa

The Middle East & Africa region accounted for 6.8% of the global consumer goods packaging market in 2025 and is forecast to grow at a CAGR of 4.6% during the forecast period. Economic diversification initiatives and retail sector expansion are driving packaging demand across the region. Rising urban populations and growing consumption of packaged food and personal care products are increasing the need for modern packaging solutions. Flexible packaging and PET containers remain widely used due to cost efficiency and durability.

Saudi Arabia emerged as the dominant country in the region due to strong retail investments and increasing food manufacturing activities. A unique growth driver in the country is the expansion of organized supermarket chains and convenience retail formats. Food companies are investing in shelf-ready packaging and lightweight beverage containers to improve distribution efficiency. Growth in local manufacturing and tourism-related consumption is also supporting packaging demand. Additionally, government sustainability initiatives are encouraging gradual adoption of recyclable and reusable packaging materials.

Latin America

Latin America held 6.9% of the consumer goods packaging market share in 2025 and is expected to record the fastest CAGR of 5.4% through 2034. The region is witnessing increasing demand for packaged consumer products due to retail modernization and rising disposable income levels. Flexible packaging solutions are gaining popularity across food, beverage, and household product industries because of affordability and convenience. Packaging manufacturers are also benefiting from growing exports of processed foods and agricultural products.

Brazil remained the dominant country in Latin America due to its large consumer base and strong food processing sector. A significant growth driver in Brazil is the expansion of regional e-commerce logistics networks requiring durable transportation packaging. Beverage manufacturers are increasingly adopting lightweight PET bottles and recyclable aluminum packaging to reduce operational costs. The growing popularity of packaged snacks and ready-to-drink beverages is also supporting flexible packaging demand. Investments in domestic recycling infrastructure are expected to improve sustainable packaging adoption across the country.

Competitive Landscape

The consumer goods packaging market is highly competitive and characterized by the presence of global packaging manufacturers, regional suppliers, and material innovation companies. Major participants focus on sustainability, lightweight packaging development, automation, and smart packaging technologies to strengthen market positioning. Companies are increasingly investing in recyclable materials, bio-based polymers, and advanced printing technologies to address changing consumer preferences and regulatory requirements.

Amcor plc remains one of the leading companies in the market due to its strong global manufacturing network and broad portfolio of flexible and rigid packaging solutions. The company continues to expand investments in recyclable packaging technologies and lightweight product development. Berry Global Inc. is focusing on sustainable plastic packaging innovations and post-consumer recycled material integration across consumer product applications. Mondi plc is strengthening its paper-based packaging portfolio to capitalize on growing demand for environmentally friendly packaging formats.

Sealed Air Corporation is investing in automation and protective packaging systems for e-commerce and food delivery applications. Sonoco Products Company continues to expand its rigid paper container and industrial packaging operations through acquisitions and strategic partnerships. Several companies are also increasing research and development activities related to smart packaging, digital printing, and barrier coating technologies. Partnerships between packaging manufacturers and consumer goods brands are expected to accelerate sustainable packaging commercialization over the forecast period.

Key Players List

- Amcor plc

- Berry Global Inc.

- Mondi plc

- Sealed Air Corporation

- Sonoco Products Company

- Smurfit Westrock plc

- DS Smith plc

- International Paper Company

- Huhtamaki Oyj

- Ball Corporation

- Crown Holdings, Inc.

- Tetra Pak International S.A.

- AptarGroup, Inc.

- Silgan Holdings Inc.

- Graphic Packaging International, LLC