Confectionery Packaging Market Size and Growth

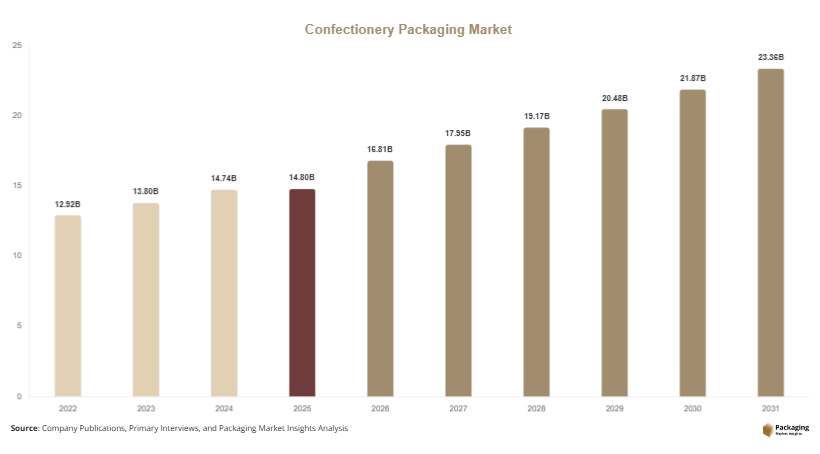

The Confectionery Packaging Market was valued at USD 14.80 billion in 2025 and is projected to reach USD 21.95 billion by 2030, expanding at a CAGR of 6.8% during 2025–2031. The market growth is being driven by the steady global demand for confectionery products, including chocolates, candies, gums, and premium sweets, which require innovative, protective, and visually appealing packaging solutions. A key global factor supporting market expansion is the rapid evolution of retail formats and e-commerce platforms, which has increased the need for durable and attractive packaging that enhances product shelf life and consumer appeal.

The increasing consumption of impulse-buy confectionery products, combined with the demand for sustainable and flexible packaging materials, is reshaping the industry landscape. Manufacturers are focusing on lightweight materials, recyclability, and branding enhancements to differentiate their offerings. Additionally, advancements in printing technologies and smart packaging features are further influencing market dynamics.

Key Highlights:

• Europe dominated the market with a 32.5% share in 2025, while Asia Pacific is expected to grow at the fastest CAGR of 8.2% during the forecast period.

• Flexible packaging emerged as the leading type segment, while biodegradable materials are projected to grow at a CAGR of 9.1%, making it the fastest-growing subsegment.

• The United States led the market, with values of USD 3.10 billion in 2025 and USD 3.28 billion in 2026, driven by high confectionery consumption and strong retail infrastructure.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Eco-Friendly Packaging

Sustainability has become a central trend in the Confectionery Packaging Market, with manufacturers increasingly adopting biodegradable, recyclable, and compostable materials. Consumers are showing a strong preference for environmentally responsible packaging, prompting brands to reduce plastic usage and invest in paper-based and bio-based alternatives. Regulatory pressures across regions, especially in Europe, are also accelerating this shift. Companies are redesigning packaging formats to minimize waste while maintaining product integrity and shelf appeal.

Premiumization and Innovative Packaging Designs

The rise of premium confectionery products is influencing packaging innovation. Brands are focusing on high-quality materials, unique shapes, and enhanced printing techniques to create visually appealing packaging that reflects product quality. Features such as resealable packs, portion-controlled designs, and gift-ready packaging formats are gaining traction. Digital printing and personalization trends are also enabling brands to cater to niche consumer segments, thereby enhancing customer engagement and brand loyalty.

Market Drivers

Rising Global Consumption of Confectionery Products

The increasing demand for chocolates, candies, and sugar-based snacks is a primary driver of the Confectionery Packaging Market. Urbanization, rising disposable incomes, and changing consumer lifestyles have led to higher consumption of ready-to-eat confectionery items. Seasonal demand during festivals and celebrations further boosts packaging requirements. This consistent demand creates a strong need for efficient, attractive, and protective packaging solutions.

Expansion of Organized Retail and E-Commerce Channels

The growth of supermarkets, hypermarkets, and online retail platforms has significantly influenced packaging requirements. Confectionery products need durable packaging to withstand transportation and storage while maintaining freshness and visual appeal. E-commerce growth has also increased demand for secondary and protective packaging formats. As a result, manufacturers are innovating packaging designs that balance protection, cost efficiency, and branding.

Market Restraint

Environmental Concerns and Regulatory Pressures

One of the major challenges facing the Confectionery Packaging Market is the increasing concern over plastic waste and environmental sustainability. Governments and regulatory bodies across various regions are implementing strict regulations on single-use plastics and non-recyclable materials. These regulations are compelling manufacturers to shift toward sustainable alternatives, which often involve higher production costs and technological complexities.

Additionally, transitioning to eco-friendly materials requires significant investment in research and development, as well as modifications in manufacturing processes. Smaller players may find it difficult to adapt quickly, leading to operational challenges. While sustainable packaging offers long-term benefits, the initial cost burden and supply chain limitations can hinder market growth in the short term.

Market Opportunities

Growth of Biodegradable and Compostable Packaging

The increasing demand for environmentally friendly packaging solutions presents significant opportunities in the Confectionery Packaging Market. Biodegradable and compostable materials are gaining traction as consumers and regulatory bodies push for sustainable alternatives. Innovations in material science are enabling manufacturers to develop packaging that maintains product quality while reducing environmental impact. This segment is expected to witness strong growth, particularly in developed markets.

Technological Advancements in Smart Packaging

Smart packaging technologies, including QR codes, NFC tags, and temperature-sensitive indicators, are creating new growth avenues. These technologies enhance consumer engagement by providing product information, authenticity verification, and interactive experiences. In the confectionery sector, smart packaging can also help maintain product quality and monitor shelf life. As digitalization continues to expand, the integration of smart features into packaging is expected to drive market innovation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.80 Billion |

| Market Size in 2026 | USD 16.81 Billion |

| Market Size in 2031 | USD 21.95 Billion |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Plastic-based packaging dominated the Confectionery Packaging Market in 2024, accounting for 48.0% of the total share, due to its cost-effectiveness, flexibility, and barrier properties. Materials such as polyethylene and polypropylene were widely used for packaging chocolates and candies, ensuring product freshness and extended shelf life.

Biodegradable materials will grow at the fastest CAGR of 9.1% during the forecast period, driven by increasing environmental awareness and regulatory pressures. The shift toward sustainable materials will encourage manufacturers to adopt compostable and recyclable solutions, particularly in developed markets.

By Packaging Type

Flexible packaging held the largest share of 52.5% in 2024, owing to its lightweight nature, cost efficiency, and convenience. Formats such as pouches, wrappers, and films were widely used for confectionery products, offering easy handling and storage.

Rigid packaging is expected to grow at a CAGR of 7.2%, supported by the demand for premium and gift-oriented confectionery products. Rigid boxes and containers will gain popularity due to their durability and aesthetic appeal.

By Product Type

Chocolate packaging dominated the market with a 45.0% share in 2024, driven by high global consumption of chocolate products. Packaging solutions for chocolates focus on maintaining freshness, preventing melting, and enhancing visual appeal.

Sugar confectionery packaging will grow at a CAGR of 7.8%, fueled by increasing demand for candies, gums, and jellies. The need for colorful and attractive packaging will support growth in this segment.

By End-Use

The food and beverage industry accounted for 60.0% of the market share in 2024, as confectionery products are a major segment within packaged foods. The demand for convenient and safe packaging solutions has driven growth in this segment.

The retail segment will expand at a CAGR of 7.5%, supported by the growth of supermarkets and online retail channels. Increased shelf visibility and branding requirements will influence packaging innovations.

Confectionery Packaging Market Segmentations

By Material

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Biodegradable Materials

By Packaging Type

- Flexible Packaging

- Rigid Packaging

By Product Type

- Chocolate

- Sugar Confectionery

- Gum & Chewing Candy

By End-Use

- Food & Beverage

- Retail

- E-commerce.

Regional Analysis

North America

North America accounted for 24.0% of the Confectionery Packaging Market share in 2025 and was driven by strong consumption patterns and advanced packaging technologies. The region will continue to expand at a CAGR of 5.9% during 2025–2033, supported by increasing demand for premium confectionery products and sustainable packaging solutions. The presence of established packaging manufacturers and advanced retail infrastructure has contributed to market stability.

The United States dominated the regional market due to high consumption of chocolates and candies. The growing demand for convenience packaging formats, such as resealable pouches and single-serve packs, has been a key growth factor. Additionally, the increasing adoption of eco-friendly packaging solutions has encouraged innovation among manufacturers.

Europe

Europe held the largest share of 32.5% in 2025 in the Confectionery Packaging Market, reflecting strong demand for premium and sustainable packaging solutions. The region will grow at a CAGR of 6.3% through 2033, driven by strict environmental regulations and consumer preference for eco-friendly materials.

Germany led the regional market due to its advanced manufacturing capabilities and strong focus on sustainability. The country's emphasis on recyclable packaging and reduced plastic usage has influenced the adoption of paper-based and biodegradable materials, supporting market growth.

Asia Pacific

Asia Pacific represented 27.0% of the market share in 2025 and will expand at the fastest CAGR of 8.2% during 2025–2033. Rapid urbanization, population growth, and rising disposable incomes are driving the demand for confectionery products and packaging solutions in the region.

China dominated the market due to its large consumer base and expanding retail sector. The growth of e-commerce platforms and increasing demand for packaged confectionery products have fueled the need for efficient and cost-effective packaging solutions.

Middle East & Africa

The Middle East & Africa held a 9.0% market share in 2025 and will grow at a CAGR of 6.7% through 2033. The market growth is supported by increasing urbanization and rising demand for packaged food products.

The United Arab Emirates emerged as a key market due to its strong retail sector and growing tourism industry. The demand for premium confectionery products has driven the adoption of high-quality packaging solutions.

Latin America

Latin America accounted for 7.5% of the market share in 2025 and will expand at a CAGR of 6.5% during 2025–2033. The region is experiencing steady growth due to increasing consumption of confectionery products and expanding retail infrastructure.

Brazil led the regional market, supported by a growing middle-class population and rising demand for affordable confectionery products. The increasing adoption of flexible packaging formats has contributed to market expansion.

Competitive Landscape

The Confectionery Packaging Market is moderately fragmented, with key players focusing on innovation, sustainability, and strategic partnerships. Leading companies are investing in advanced materials and digital printing technologies to enhance product differentiation.

Amcor plc is a prominent market leader, known for its extensive portfolio of flexible and rigid packaging solutions. The company has recently introduced recyclable packaging solutions aimed at reducing environmental impact.

Other major players include Mondi Group, Sealed Air Corporation, Berry Global Inc., and Sonoco Products Company, all of which are actively expanding their product offerings and global presence. These companies are focusing on sustainable packaging innovations and strategic acquisitions to strengthen their market position.

Key Players in the Confectionery Packaging Market

- Amcor plc

- Mondi Group

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Huhtamaki Oyj

- WestRock Company

- Smurfit Kappa Group

- Constantia Flexibles

- DS Smith Plc

- Coveris Holdings S.A.

- ProAmpac LLC

- Clondalkin Group

- UFlex Ltd.

- Winpak Ltd.