Compostable Shrink Wrap Market Size and Growth

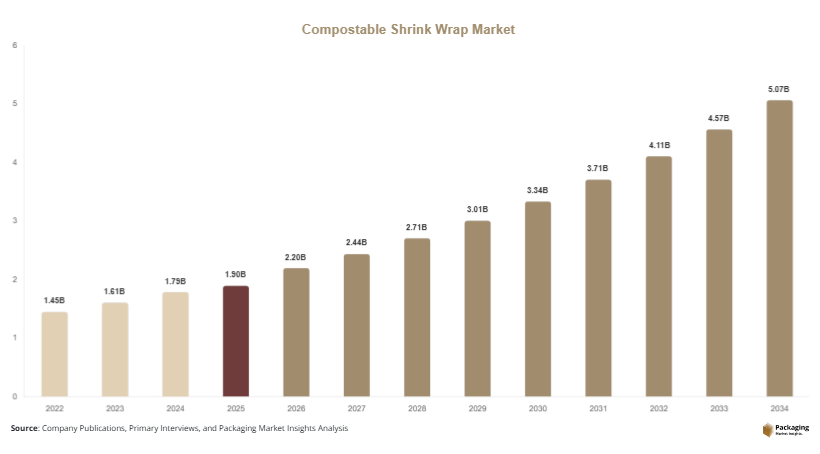

The global compostable shrink wrap market size is estimated at USD 1.9 billion in 2025 and is expected to reach USD 2.2 billion in 2026. With increasing regulatory pressure and growing consumer awareness regarding plastic waste, the market is projected to reach USD 5.1 billion by 2034, registering a CAGR of 11.0% during the forecast period (2025–2034). Compostable shrink wrap is manufactured from bio-based materials such as polylactic acid (PLA), starch blends, and cellulose derivatives, offering an eco-friendly alternative to conventional plastic shrink films. The compostable shrink wrap market is gaining traction as industries shift toward sustainable and environmentally responsible packaging solutions.

One of the primary growth factors is the increasing emphasis on sustainability across packaging industries, particularly in food, beverage, and retail sectors. Companies are adopting compostable materials to align with environmental regulations and corporate sustainability goals. Another significant factor is the rise of e-commerce and retail packaging requirements, where shrink wrap is widely used for bundling and product protection. Compostable alternatives provide a viable solution without compromising environmental standards. Additionally, government initiatives aimed at reducing single-use plastics are encouraging the adoption of biodegradable and compostable packaging materials.

Key Highlights:

- Asia Pacific dominated the market with a 36.9% share in 2025, while Latin America is projected to grow at the fastest CAGR of 11.8%.

- PLA-based films led the type segment with a 42.6% share, while cellulose-based films are expected to grow at a CAGR of 12.2%.

- Food packaging dominated with a 48.3% share, while retail packaging is forecasted to grow at a CAGR of 11.6%.

- Beverage packaging applications led the segment with 39.7% share, while pharmaceutical packaging is expected to grow at a CAGR of 11.9%.

- China remained the dominant country with a market size of USD 0.62 billion in 2025 and USD 0.71 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising demand for eco-friendly and compostable packaging solutions

The shift toward environmentally sustainable packaging is a key trend in the compostable shrink wrap market. Consumers and businesses are increasingly prioritizing materials that reduce environmental impact and support waste management goals. Compostable shrink wrap is gaining attention as it decomposes under composting conditions without leaving harmful residues. Retailers and food producers are adopting such materials to enhance their sustainability credentials and meet regulatory requirements. This trend is further supported by global efforts to reduce plastic waste and promote circular economy practices, encouraging the use of compostable materials across packaging applications.

Advancements in bio-based polymer technology

Technological innovation in bio-based polymers is significantly influencing the compostable shrink wrap market. Manufacturers are developing materials with improved mechanical strength, clarity, and shrink performance, making compostable shrink wrap more competitive with conventional plastic films. Enhanced processing techniques are enabling large-scale production while maintaining product quality. These advancements are expanding the use of compostable shrink wrap in various industries, including food and beverage packaging. The ability to customize properties such as thickness and shrink ratio is also increasing its versatility and adoption.

Market Drivers

Increasing regulatory pressure to reduce plastic waste

Government regulations aimed at reducing plastic waste are a major driver of the compostable shrink wrap market. Many countries are implementing bans and restrictions on single-use plastics, encouraging the adoption of sustainable alternatives. Compostable shrink wrap offers a viable solution that complies with these regulations while maintaining packaging functionality. Companies are adopting such materials to avoid penalties and enhance their environmental performance. This regulatory environment is expected to continue driving market growth.

Growing consumer awareness and demand for sustainable products

Consumer awareness regarding environmental issues is influencing purchasing decisions, driving demand for sustainable packaging solutions. Customers are increasingly choosing products with eco-friendly packaging, encouraging brands to adopt compostable materials. Compostable shrink wrap aligns with these preferences, offering a sustainable alternative to traditional plastic films. This shift in consumer behavior is prompting manufacturers to invest in sustainable packaging innovations, further supporting market growth.

Market Restraint

High production costs and limited infrastructure for composting

The high cost of producing compostable shrink wrap compared to conventional plastic films is a key challenge for market growth. Bio-based materials and advanced manufacturing processes can increase production costs, making these products less competitive in price-sensitive markets. Additionally, the lack of widespread composting infrastructure limits the effectiveness of compostable packaging solutions. For example, in regions where industrial composting facilities are not available, compostable shrink wrap may not be properly processed, reducing its environmental benefits. These factors can hinder adoption, particularly in developing economies.

Market Opportunities

Expansion of composting infrastructure and waste management systems

The development of composting infrastructure presents significant opportunities for the compostable shrink wrap market. Governments and organizations are investing in waste management systems that support composting, enabling the proper disposal of biodegradable materials. As infrastructure improves, the adoption of compostable shrink wrap is expected to increase. Companies that align their products with these systems can benefit from growing demand and regulatory support.

Increasing adoption in food and beverage packaging applications

The food and beverage industry offers substantial growth opportunities for compostable shrink wrap. These industries require packaging solutions that maintain product freshness while meeting sustainability goals. Compostable shrink wrap provides an effective solution for bundling and protecting products. The increasing demand for organic and eco-friendly food products is further driving adoption. Manufacturers can capitalize on this trend by developing specialized compostable packaging solutions tailored to food and beverage applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.9 Billion |

| Market Size in 2026 | USD 2.2 Billion |

| Market Size in 2034 | USD 5.1 Billion |

| CAGR | 11.0% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

PLA-based films dominated the market in 2024, accounting for 42.6% of the total share. These films are widely used due to their biodegradability and compatibility with existing packaging processes. PLA-based shrink wraps offer good clarity and shrink performance, making them suitable for food and retail packaging applications.

Cellulose-based films are expected to grow at a CAGR of 12.2% during the forecast period. This growth is driven by their natural origin and superior compostability. These films are gaining popularity in premium packaging applications where sustainability is a key consideration.

By Application

Food packaging accounted for the largest share of 48.3% in 2024. Compostable shrink wrap is widely used in this segment for bundling and protecting food products. The increasing demand for sustainable packaging in the food industry is driving this segment’s growth.

Retail packaging is projected to grow at a CAGR of 11.6%, driven by the expansion of e-commerce and consumer goods industries. Compostable shrink wrap is being adopted for packaging retail products to enhance sustainability and meet consumer expectations.

By End-Use

Beverage packaging held the largest share of 39.7% in 2024. The use of compostable shrink wrap in beverage packaging is increasing as companies aim to reduce plastic waste. The material provides effective bundling and protection for beverage products.

Pharmaceutical packaging is expected to grow at a CAGR of 11.9% during the forecast period. This growth is driven by the need for sustainable packaging solutions in the pharmaceutical industry. Compostable shrink wrap offers a viable alternative to traditional plastic packaging.

Compostable Shrink Wrap Market Segmentations

By Type

- PLA-Based Films

- Cellulose-Based Films

- Starch-Based Films

By Application

- Food Packaging

- Retail Packaging

By End-Use

- Beverage

- Pharmaceutical

- Consumer Goods

Regional Analysis

North America

North America accounted for 23.5% of the compostable shrink wrap market share in 2025 and is expected to grow at a CAGR of 10.6% during the forecast period. The region’s growth is supported by strong environmental regulations and increasing consumer awareness regarding sustainable packaging. The presence of advanced waste management systems further supports the adoption of compostable materials.

The United States dominates the regional market due to its large packaging industry and focus on sustainability. A unique growth factor is the increasing adoption of corporate sustainability initiatives, where companies are committing to reducing plastic waste and adopting eco-friendly packaging solutions.

Europe

Europe held a market share of 26.1% in 2025 and is projected to grow at a CAGR of 10.9%. The region is characterized by strict environmental policies and a strong emphasis on circular economy practices. The adoption of compostable packaging is increasing as companies aim to comply with regulations and reduce environmental impact.

Germany is the leading country in the European market, driven by its advanced manufacturing sector. A unique growth factor is the integration of compostable materials into packaging standards, which is encouraging widespread adoption across industries.

Asia Pacific

Asia Pacific dominated the market with a 36.9% share in 2025 and is expected to grow at a CAGR of 11.2%. The region’s growth is driven by increasing industrialization and rising awareness of environmental issues. The expansion of retail and e-commerce sectors is further supporting demand for sustainable packaging solutions.

China remains the dominant country in the region due to its large manufacturing base. A unique growth factor is the government’s initiatives to reduce plastic pollution, which are encouraging the adoption of compostable materials.

Middle East & Africa

The Middle East & Africa region accounted for 6.8% of the market share in 2025 and is projected to grow at a CAGR of 10.7%. Growth is supported by increasing awareness of environmental issues and gradual adoption of sustainable packaging solutions.

South Africa is a key market in the region, supported by its developing retail sector. A unique growth factor is the increasing investment in waste management infrastructure, which is supporting the adoption of compostable packaging.

Latin America

Latin America held a 6.7% share in 2025 and is expected to grow at the fastest CAGR of 11.8%. The region’s growth is driven by increasing consumer awareness and regulatory initiatives aimed at reducing plastic waste.

Brazil dominates the regional market due to its large consumer base. A unique growth factor is the expansion of sustainable packaging initiatives, which is encouraging the adoption of compostable shrink wrap solutions.

Competitive Landscape

The compostable shrink wrap market is characterized by a growing number of players focusing on innovation and sustainability. Companies are investing in research and development to improve material performance and reduce production costs. Strategic partnerships and collaborations are common as companies aim to expand their market presence.

NatureWorks LLC is a leading player in the market, known for its bio-based polymer solutions. The company recently introduced new PLA-based shrink films with enhanced performance characteristics, reflecting its commitment to innovation. Other players are also focusing on expanding their product portfolios and improving manufacturing capabilities.

Key Players List

- NatureWorks LLC

- BASF SE

- Novamont S.p.A.

- Futamura Group

- Taghleef Industries

- Innovia Films Ltd.

- Plantic Technologies Limited

- Cortec Corporation

- Biome Bioplastics Ltd.

- Walki Group Oy

- Mondi Group

- Amcor plc

- TIPA Corp Ltd.

- BioBag International AS

- Clondalkin Group