Commodity Plastics Market Size and Growth

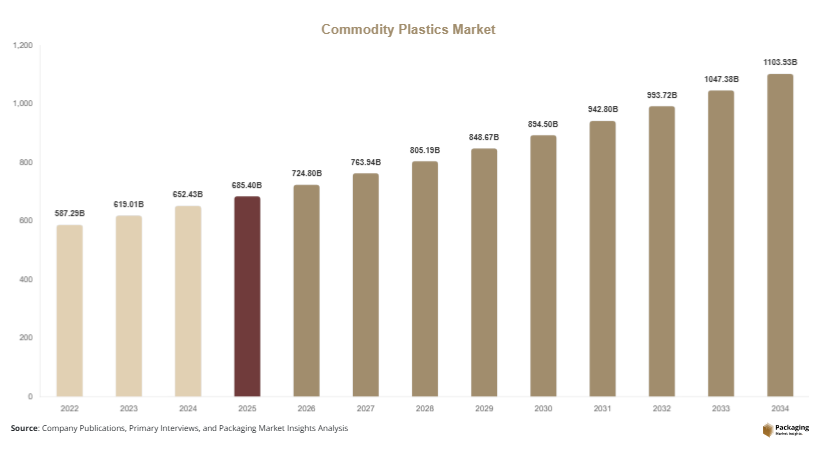

In 2025, the global commodity plastics market size was valued at approximately USD 685.4 billion, and it is projected to reach USD 724.8 billion in 2026. Over the forecast period, the market is expected to grow to USD 1,102.6 billion by 2034, registering a CAGR of 5.4% from 2025 to 2034. The commodity plastics market continues to expand steadily, supported by rising industrialization, consumer goods demand, and infrastructure development across emerging economies.

Commodity plastics, including polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), and polystyrene (PS), are widely used due to their cost-effectiveness, versatility, and ease of processing. These materials are essential across industries such as packaging, automotive, construction, and consumer goods, making them fundamental to modern manufacturing ecosystems.

Key Highlights:

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.3%.

- Polyethylene led the type segment with a 34.7% share, while polypropylene is expected to grow at a CAGR of 6.1%.

- Packaging applications dominated with a 41.5% share, while automotive applications are forecasted to grow at a CAGR of 5.9%.

- Consumer goods accounted for 28.3% of end-use share, while construction is expected to grow at a CAGR of 5.6%.

- China remained the dominant country with a market size of USD 142.6 billion in 2025 and USD 150.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Recycled and Sustainable Plastics

The commodity plastics market is witnessing a noticeable shift toward sustainability, driven by regulatory pressures and changing consumer preferences. Manufacturers are increasingly incorporating recycled plastics into their production processes to reduce environmental impact and comply with government mandates. Advanced recycling technologies, such as chemical recycling, are enabling the conversion of plastic waste into high-quality raw materials. This trend is particularly prominent in packaging applications, where companies are committing to using a higher percentage of recycled content in their products.

Additionally, brand owners and retailers are setting sustainability targets, pushing suppliers to innovate and offer eco-friendly alternatives. The demand for recyclable and reusable plastic products is growing, especially in developed markets. This trend is expected to reshape the supply chain, encouraging investments in waste management infrastructure and recycling capabilities.

Expansion of E-commerce and Flexible Packaging Demand

The rapid growth of e-commerce has significantly influenced the demand for commodity plastics, particularly in flexible packaging solutions. Online retail requires durable, lightweight, and cost-effective packaging materials to ensure safe product delivery. Commodity plastics such as polyethylene and polypropylene are widely used in packaging films, bubble wraps, and protective materials.

As consumer preferences shift toward convenience and fast delivery, packaging requirements are becoming more complex. This has led to increased demand for multilayer films and advanced plastic formulations that provide better strength and barrier properties. Emerging markets are also experiencing a surge in online shopping, further boosting demand for plastic packaging solutions. This trend is expected to continue as digital commerce expands globally.

Market Drivers

Growth in Packaging Industry Across Multiple Sectors

The packaging industry remains one of the strongest drivers of the commodity plastics market. Increasing consumption of packaged food, beverages, pharmaceuticals, and personal care products is driving demand for plastic packaging materials. Commodity plastics offer advantages such as lightweight, flexibility, durability, and cost efficiency, making them ideal for large-scale packaging applications.

In addition, the rise of ready-to-eat meals and convenience foods is fueling the need for advanced packaging solutions that preserve freshness and extend shelf life. Developing regions are witnessing rapid urbanization and lifestyle changes, which further contribute to the growth of packaged goods consumption. This widespread use of plastics in packaging is expected to sustain demand throughout the forecast period.

Increasing Use in Automotive and Construction Applications

Commodity plastics are gaining traction in automotive and construction industries due to their versatility and performance characteristics. In the automotive sector, plastics are used to reduce vehicle weight, which improves fuel efficiency and lowers emissions. Components such as dashboards, bumpers, and interior panels are increasingly made from plastics.

In the construction sector, plastics are widely used in pipes, insulation materials, and window frames. Their resistance to corrosion, moisture, and chemicals makes them suitable for long-term use in infrastructure projects. Governments worldwide are investing in infrastructure development, particularly in emerging economies, which is driving demand for construction materials, including plastics. This trend is expected to contribute significantly to market growth.

Market Restraint

Environmental Concerns and Regulatory Restrictions

Environmental concerns related to plastic waste and pollution pose a significant restraint to the commodity plastics market. Governments and regulatory bodies across the globe are implementing strict regulations to limit the use of single-use plastics and promote sustainable alternatives. These regulations are affecting production volumes and increasing compliance costs for manufacturers.

For example, bans on plastic bags and restrictions on certain packaging materials have impacted demand in specific segments. Additionally, public awareness regarding environmental issues is influencing consumer behavior, leading to reduced plastic consumption in some regions. Companies are required to invest in sustainable practices, recycling technologies, and alternative materials, which can increase operational costs. This restraint is expected to create challenges for market growth, particularly for traditional plastic manufacturers.

Market Opportunities

Development of Bio-based and Biodegradable Plastics

The increasing focus on sustainability is creating opportunities for bio-based and biodegradable plastics within the commodity plastics market. These materials are derived from renewable sources and offer reduced environmental impact compared to conventional plastics. Governments and organizations are encouraging the adoption of such materials through incentives and regulations.

Research and development activities are leading to improved performance and cost efficiency of bio-based plastics, making them more competitive. Industries such as packaging and agriculture are adopting these materials to meet sustainability goals. This shift presents a significant growth opportunity for manufacturers willing to invest in innovation and sustainable product development.

Expansion in Emerging Economies

Emerging economies present substantial growth opportunities for the commodity plastics market due to rapid industrialization, urbanization, and population growth. Countries in Asia Pacific, Latin America, and Africa are experiencing increased demand for consumer goods, infrastructure, and automotive products, all of which rely heavily on plastics.

Improving economic conditions and rising disposable incomes are driving consumption patterns in these regions. Additionally, government initiatives to promote manufacturing and infrastructure development are supporting market expansion. Companies are increasingly focusing on these regions to establish production facilities and expand their market presence, which is expected to drive long-term growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 685.4 Billion |

| Market Size in 2026 | USD 724.8 Billion |

| Market Size in 2034 | USD 1102.6 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polyethylene dominated the commodity plastics market in 2024, accounting for approximately 34.7% of the total share. Its widespread use in packaging applications, including films, containers, and bottles, contributes to its dominance. Polyethylene is favored for its flexibility, durability, and resistance to moisture, making it suitable for a variety of applications.

Polypropylene is the fastest-growing segment, expected to grow at a CAGR of 6.1% during the forecast period. Its increasing use in automotive components, medical devices, and packaging is driving growth. The material’s lightweight and chemical resistance properties make it a preferred choice in various industries.

By Application

Packaging emerged as the dominant application segment in 2024, holding a 41.5% share. The demand for plastic packaging is driven by its cost-effectiveness and ability to protect products. The growth of e-commerce and food delivery services further supports this segment.

Automotive applications are expected to grow at the fastest CAGR of 5.9%. The need for lightweight materials to improve fuel efficiency is driving the use of plastics in vehicle manufacturing. Increasing production of electric vehicles is also contributing to segment growth.

By End-Use

Consumer goods accounted for 28.3% of the market share in 2024, driven by high demand for plastic products such as household items, electronics, and personal care products. The versatility and affordability of plastics make them ideal for mass production.

The construction segment is expected to grow at a CAGR of 5.6%. The increasing use of plastics in pipes, insulation, and building materials is driving demand. Infrastructure development in emerging economies is a key growth factor for this segment.

Commodity Plastics Market Segmentations

By Type

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

By Application

- Packaging

- Automotive

- Construction

- Consumer Goods

By End-User

- Consumer Goods

- Construction

- Automotive

- Healthcare

Regional Analysis

North America

North America accounted for approximately 22.5% of the global commodity plastics market share in 2025 and is projected to grow at a CAGR of 4.6% during the forecast period. The region benefits from advanced manufacturing infrastructure and strong demand from packaging and automotive industries. The presence of established market players and continuous technological innovation further supports growth.

The United States dominates the North American market, driven by high consumption of packaged goods and increasing adoption of sustainable materials. A key growth factor in the region is the rising investment in recycling infrastructure, which supports the development of a circular economy and enhances the use of recycled plastics.

Europe

Europe held a 19.8% market share in 2025 and is expected to grow at a CAGR of 4.3% over the forecast period. The region is characterized by stringent environmental regulations and a strong focus on sustainability. Demand for recyclable and biodegradable plastics is increasing across industries.

Germany is the leading country in Europe, supported by its strong industrial base and automotive sector. A unique growth factor in the region is the implementation of strict policies promoting plastic recycling and waste reduction, which is encouraging innovation in sustainable materials.

Asia Pacific

Asia Pacific dominated the market with a 38.2% share in 2025 and is projected to grow at a CAGR of 5.9%. Rapid industrialization, urbanization, and population growth are key factors driving demand in the region. The expanding packaging and construction industries are major contributors.

China leads the Asia Pacific market due to its large manufacturing base and high consumption of plastics. A key growth factor is the increasing demand for consumer goods and infrastructure development, which continues to drive the use of commodity plastics across various applications.

Middle East & Africa

The Middle East & Africa region accounted for 9.6% of the market share in 2025 and is expected to grow at a CAGR of 5.1%. The region benefits from abundant raw material availability and growing industrial activities.

Saudi Arabia dominates the market, supported by its petrochemical industry. A unique growth factor is the expansion of downstream petrochemical industries, which is boosting the production and consumption of commodity plastics in the region.

Latin America

Latin America held a 9.9% market share in 2025 and is projected to grow at the fastest CAGR of 6.3%. The region is experiencing increased demand for packaging and consumer goods.

Brazil is the leading country in Latin America, driven by its growing population and expanding retail sector. A key growth factor is the increasing adoption of plastic packaging in the food and beverage industry, which is supporting market expansion.

Competitive Landscape

The commodity plastics market is moderately consolidated, with key players focusing on capacity expansion, product innovation, and sustainability initiatives. Major companies are investing in advanced technologies to improve product quality and reduce environmental impact.

One of the leading players in the market is ExxonMobil, which has a strong global presence and extensive product portfolio. The company continues to invest in chemical recycling technologies to enhance sustainability.

Other prominent players include BASF SE, Dow Inc., SABIC, and LyondellBasell Industries. These companies are focusing on strategic partnerships and acquisitions to strengthen their market position. Recent developments include investments in bio-based plastics and expansion of production facilities to meet growing demand.

Key Players List

- ExxonMobil Corporation

- BASF SE

- Dow Inc.

- SABIC

- LyondellBasell Industries

- INEOS Group

- Formosa Plastics Corporation

- LG Chem

- Reliance Industries Limited

- Chevron Phillips Chemical Company

- Braskem S.A.

- Borealis AG

- TotalEnergies SE

- Mitsubishi Chemical Group

- China National Petroleum Corporation