Clinical Trial Packaging Market Size and Growth

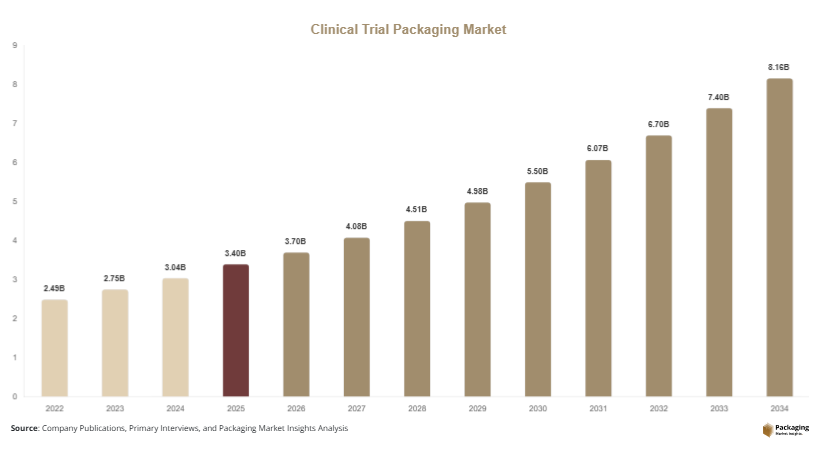

The global clinical trial packaging market size is estimated at USD 3.4 billion ion 2025, driven by increased clinical research outsourcing and rising global trial volumes. By 2026, the market is projected to reach USD 3.7 billion, supported by expansion in oncology and rare disease trials. Looking ahead, the market is forecasted to reach USD 8.2 billion by 2034, registering a CAGR of 10.4% (2025–2034). This growth reflects increasing regulatory complexity, demand for tamper-evident packaging, and rising adoption of patient-centric trial designs.

One of the primary growth factors is the expansion of global clinical research outsourcing (CRO) activities, particularly in emerging economies where trial costs are lower and patient recruitment is faster. Another key driver is the rise of decentralized clinical trials, which require home-delivered investigational products with precise labeling and temperature control. A third factor is the increasing complexity of biologics and cell and gene therapies, which require specialized cold-chain and light-sensitive packaging systems.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share.

- Plastic packaging dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 1.4 billion in 2025 and USD 1.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rise of Patient-Centric and Decentralized Trial Packaging Models

A major trend shaping the clinical trial packaging market is the shift toward patient-centric and decentralized clinical trial models. These models require investigational drugs to be packaged in formats suitable for direct shipment to patients’ homes rather than centralized clinical sites. Packaging systems now include pre-dosed blister packs, clearly labeled multi-dose kits, and temperature-controlled transport containers. For example, oncology trials in North America increasingly use home delivery kits that include secure packaging with tamper-evident seals and digital tracking codes. This approach improves patient compliance and reduces site visits. In the future, decentralized trials are expected to dominate early-phase studies, further increasing demand for flexible and patient-friendly packaging systems integrated with digital monitoring tools.

Integration of Smart Packaging and Digital Tracking Technologies

Another significant trend is the integration of smart packaging technologies such as RFID tags, QR codes, and IoT-enabled sensors. These technologies allow real-time tracking of clinical trial materials across global supply chains, ensuring temperature integrity and reducing loss or contamination risks. For instance, pharmaceutical companies conducting multi-country trials use RFID-enabled packaging to monitor drug location and storage conditions. In vaccine trials, temperature-sensitive indicators are embedded in packaging to ensure cold-chain compliance. The future of clinical trial packaging will increasingly rely on digital ecosystems that connect packaging data with clinical trial management systems, improving transparency, regulatory compliance, and supply chain efficiency.

Market Drivers

Growth in Global Clinical Research Outsourcing

The expansion of contract research organizations (CROs) is a key driver of the clinical trial packaging market. Pharmaceutical companies are outsourcing clinical trials to reduce costs, improve efficiency, and access diverse patient populations. CROs handle packaging, labeling, and distribution of investigational drugs across multiple geographies. For example, India and Eastern Europe have become major hubs for outsourced clinical trials due to cost advantages and regulatory efficiency. This has increased demand for localized packaging solutions that comply with regional regulatory standards. As outsourcing continues to grow, specialized packaging providers are expected to play a larger role in global clinical trial supply chains.

Rising Complexity of Biologics and Advanced Therapies

The increasing development of biologics, cell therapies, and gene therapies is another major driver. These therapies require highly sensitive packaging systems that ensure stability, sterility, and temperature control. For instance, CAR-T cell therapies require ultra-low temperature packaging solutions to maintain cell viability during transport. Similarly, monoclonal antibody trials require light-protective and cold-chain compliant packaging formats. Pharmaceutical companies are investing in advanced packaging materials such as insulated containers and phase-change materials. As advanced therapies expand globally, demand for specialized clinical trial packaging is expected to rise significantly.

Market Restraint

High Regulatory Complexity and Operational Costs

A major restraint in the clinical trial packaging market is the complexity of global regulatory frameworks and the high cost of compliance. Clinical trial packaging must meet strict labeling, serialization, and traceability requirements across different countries. This creates operational challenges for packaging providers managing multi-region trials. Additionally, small and mid-sized pharmaceutical companies face high costs associated with validation, temperature-controlled logistics, and documentation systems. For example, packaging a single oncology trial across multiple countries requires compliance with FDA, EMA, and local regulatory guidelines simultaneously. These requirements increase lead times and operational costs, limiting scalability for smaller players in the market.

Market Opportunities

Expansion of Cell and Gene Therapy Trials

The rapid expansion of cell and gene therapy trials presents a major opportunity for the clinical trial packaging market. These therapies require highly specialized packaging solutions that ensure cryogenic stability and contamination prevention. Packaging providers are developing ultra-low temperature containers and secure labeling systems for personalized therapies. For example, gene therapy trials in Europe and the United States rely on customized cryo-packaging systems to maintain sample integrity. As the number of approved cell and gene therapies increases, demand for advanced clinical trial packaging solutions will grow significantly.

Growth in Emerging Market Clinical Trial Activity

Emerging economies such as India, Brazil, and Southeast Asian countries are becoming major clinical trial destinations due to lower costs and large patient populations. This creates strong opportunities for localized packaging solutions that comply with global regulatory standards. For instance, India has seen increased oncology and vaccine trials requiring region-specific packaging formats. Packaging providers are expanding operations in these regions to support decentralized trial models. Over the forecast period, emerging markets are expected to become key growth hubs for clinical trial packaging demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.4 Billion |

| Market Size in 2026 | USD 3.7 Billion |

| Market Size in 2034 | USD 8.2 Billion |

| CAGR | 10.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Primary packaging dominated the market with a 2024 share of 46.8%, driven by its critical role in protecting investigational drugs. It includes blister packs, vials, and ampoules widely used in clinical trials. For example, oncology trials rely heavily on sterile primary packaging to ensure drug safety.

Secondary packaging is the fastest-growing segment with a CAGR of 11.8%, driven by labeling, serialization, and patient-specific kit packaging. Future demand will increase due to decentralized trials and regulatory requirements.

By Material

Plastic materials dominated with a 2024 share of 51.3%, due to durability, cost efficiency, and flexibility in design. They are widely used in blister packs and containers.

Glass materials are the fastest-growing segment with a CAGR of 10.9%, driven by biologics and injectable drugs requiring high stability.

By End-Use

Pharmaceutical companies dominated with a 2024 share of 58.4%, driven by high clinical trial volumes. CROs are the fastest-growing segment with increasing outsourcing demand.

Clinical Trial Packaging Market Segmentations

By Packaging Type

- Primary Packaging (Blisters, Vials, Ampoules)

- Secondary Packaging (Kitting, Labeling, Cartons)

- Tertiary Packaging (Cold Chain Shippers, Transport Boxes)

- Custom Patient-Specific Kits

By Material

- Plastic (PP, PET, PVC)

- Glass

- Aluminum

- Paper & Paperboard

- Composite & Barrier Materials

By End-User

- Pharmaceutical Companies

- Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Hospital-Based Clinical Trials

By Distribution Channel

- Direct Pharma Packaging Providers

- CRO Supply Chain Services

- Contract Manufacturing Organizations (CMOs)

- Specialized Clinical Logistics Providers

- Third-Party Packaging Vendors

Regional Analysis

North America

North America accounted for 34.2% of the clinical trial packaging market in 2025, with a projected CAGR of 9.8% through 2034. The region benefits from strong pharmaceutical R&D infrastructure and high clinical trial activity, particularly in oncology and rare diseases. Demand is further supported by advanced regulatory frameworks and strong presence of CROs.

The United States dominates the region due to its high concentration of pharmaceutical companies and research institutions. A key driver is the rapid adoption of decentralized clinical trials, where investigational drugs are delivered directly to patients. For example, several US-based trials now use home delivery kits with smart packaging for remote patient monitoring.

Europe

Europe held a 27.6% market share in 2025, growing at a CAGR of 9.2% through 2034. The region is driven by strong regulatory standards and increasing biotech research activity. Countries such as Germany, France, and the UK are key contributors.

Germany leads the region due to its strong pharmaceutical manufacturing base. A unique driver is the expansion of cross-border clinical trials within the EU, requiring harmonized packaging standards. For instance, EU-sponsored oncology trials use standardized packaging systems across multiple countries.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025, growing at a CAGR of 11.3% through 2034. Growth is driven by large patient pools, lower trial costs, and increasing pharmaceutical outsourcing.

China is the dominant country due to its expanding biotech sector. A key driver is government support for clinical research infrastructure. For example, China is increasingly hosting global oncology trials requiring advanced packaging systems for biologics.

Middle East & Africa

The region accounted for 4.8% of the market in 2025, with a CAGR of 8.7% through 2034. Growth is supported by expanding healthcare infrastructure and increasing clinical research participation.

Israel leads the region due to its strong biotech innovation ecosystem. A key driver is rising participation in early-phase drug trials, requiring specialized packaging solutions.

Latin America

Latin America held a 5.4% share in 2025, growing at the fastest CAGR of 11.6% through 2034. Growth is driven by increasing clinical trial outsourcing and expanding pharmaceutical investments.

Brazil dominates the region due to its large patient base. A key driver is the rising number of oncology and vaccine trials requiring localized packaging solutions.

Competitive Landscape

The clinical trial packaging market is moderately consolidated with key players including Catalent Inc., Sharp Services, PCI Pharma Services, Almac Group, and Thermo Fisher Scientific. Catalent Inc. leads the market due to its extensive global clinical supply network and integrated packaging solutions.

Companies are focusing on automation, cold-chain expansion, and digital tracking integration. Recent developments include expansion of clinical supply facilities in Asia and investment in smart packaging technologies.

Key Players List

- Catalent Inc.

- Sharp Services

- PCI Pharma Services

- Almac Group

- Thermo Fisher Scientific

- Parexel International

- Labcorp Drug Development

- Patheon (Thermo Fisher)

- West Pharmaceutical Services

- Aenova Group

- Biocair

- Movianto

- Bilcare Limited

- Klöckner Pentaplast

- Gerresheimer AG