Cider Packaging Market Size and Growth

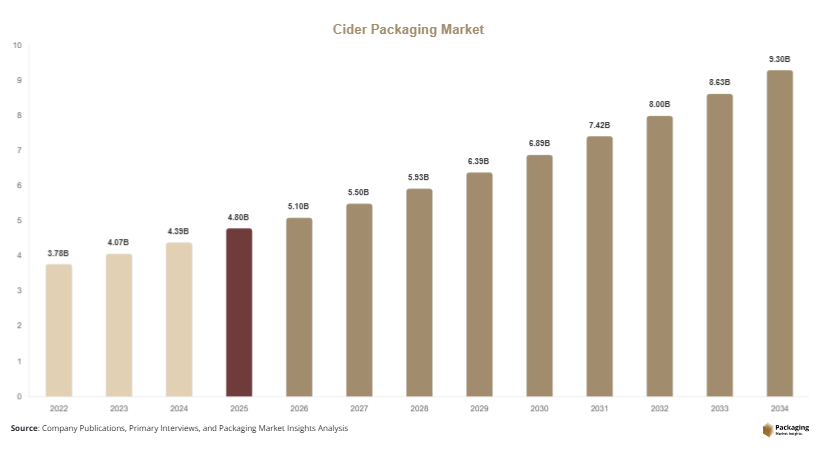

The global cider packaging market is valued at approximately USD 4.8 billion in 2025, reflecting stable growth supported by rising consumption of flavored alcoholic beverages and craft cider varieties. By 2026, the market is expected to reach USD 5.1 billion, driven by increasing retail penetration and expansion of online alcohol distribution channels. Looking ahead, the market is projected to attain USD 9.2 billion by 2034, registering a CAGR of 7.8% from 2025 to 2034. The Cider Packaging Market is witnessing steady expansion as global demand for cider continues to grow across both developed and emerging economies. Packaging plays a critical role in preserving product quality, enhancing shelf appeal, and ensuring safe transportation of alcoholic beverages.

Growth in the market is being influenced by multiple structural factors. One of the most significant drivers is the increasing popularity of craft and premium cider products, which require differentiated and visually appealing packaging formats. Another key factor is the rising focus on sustainability, where manufacturers are shifting toward recyclable glass, aluminum cans, and paper-based packaging materials. Additionally, the rapid expansion of e-commerce alcohol delivery platforms is increasing demand for tamper-proof and durable packaging solutions that ensure product integrity during transit.

Key Market Insights

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share.

- Plastic packaging dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Eco-Friendly Packaging Solutions

The cider packaging industry is increasingly moving toward sustainable packaging formats as environmental concerns and regulatory frameworks become more stringent. Manufacturers are adopting recyclable materials such as glass, aluminum, and biodegradable paper-based packaging to reduce environmental impact. In Europe, for example, cider producers are replacing plastic-based secondary packaging with compostable and recyclable alternatives. This shift is also visible in North America, where beverage companies are investing in lightweight glass bottles and aluminum cans to reduce carbon emissions during transportation. The trend is expected to intensify as governments introduce stricter packaging waste regulations and consumers demand environmentally responsible brands. Over time, sustainability will become a core requirement rather than a differentiation factor in the cider packaging market.

Integration of Smart Packaging and Digital Engagement Technologies

Smart packaging is emerging as a transformative trend in the cider packaging market. Beverage manufacturers are incorporating QR codes, NFC tags, and augmented reality features into packaging to enhance consumer interaction. These technologies allow consumers to access detailed product information such as fermentation process, ingredient sourcing, and authenticity verification. For instance, premium cider brands in France and the United States are using digital labels to create immersive storytelling experiences that connect consumers with brand heritage. This trend is also improving supply chain transparency by enabling real-time tracking and authentication. In the future, smart packaging is expected to evolve further with AI-driven personalization and interactive marketing capabilities, making packaging an active communication channel rather than just a protective layer.

Market Drivers

Rising Consumption of Cider and Alcoholic Beverages Globally

The increasing global consumption of cider and other alcoholic beverages is a major driver of the cider packaging market. Changing consumer preferences, urbanization, and rising disposable incomes are contributing to higher demand for flavored and low-alcohol beverages such as cider. In countries like the United States, United Kingdom, and Australia, cider has gained strong popularity as a refreshing alternative to beer. This growing consumption directly increases demand for packaging solutions such as glass bottles and aluminum cans. Beverage manufacturers are expanding production capacity and introducing new product variants, which further accelerates packaging demand. The growing trend of social drinking and lifestyle-oriented beverage consumption continues to support long-term market expansion.

Expansion of Retail Infrastructure and Online Alcohol Distribution

The rapid expansion of organized retail chains and online alcohol delivery platforms is significantly driving the cider packaging market. Supermarkets, convenience stores, and e-commerce platforms are increasingly stocking cider products, creating strong demand for efficient and durable packaging formats. Online alcohol delivery, in particular, requires packaging that ensures product safety during transportation, leading to increased use of tamper-proof and shock-resistant designs. For example, digital liquor platforms in urban India and the United States are prioritizing lightweight and protective packaging for cider products. This shift toward omnichannel distribution is encouraging manufacturers to innovate in packaging design, ensuring compatibility with logistics and last-mile delivery requirements.

Market Restraint

High Cost of Sustainable and Advanced Packaging Materials

One of the key challenges in the cider packaging market is the high cost associated with sustainable and advanced packaging materials. While eco-friendly solutions such as biodegradable plastics, recycled glass, and bio-based coatings are gaining traction, they remain significantly more expensive than conventional packaging options. This cost difference creates challenges for small and mid-sized cider manufacturers, particularly in price-sensitive markets. For example, transitioning from standard plastic labels to biodegradable alternatives can increase overall packaging costs substantially, affecting profit margins. Additionally, recycled aluminum and specialty glass packaging require advanced manufacturing infrastructure, further increasing production expenses. These cost barriers slow down large-scale adoption of sustainable packaging despite increasing regulatory pressure and consumer awareness.

Market Opportunities

Expansion of Premium and Craft Cider Packaging Segment

The growing demand for premium and craft cider presents a major opportunity for packaging innovation. Consumers are increasingly seeking unique and high-quality beverage experiences, which is driving demand for customized and aesthetically appealing packaging solutions. Premium cider brands are adopting embossed glass bottles, artistic labeling, and limited-edition packaging designs to differentiate their products in competitive retail environments. For instance, craft cider producers in Europe and North America are using storytelling-based packaging to enhance brand identity. This trend creates opportunities for packaging manufacturers to offer high-end customization services. In the future, premiumization will continue to drive demand for innovative packaging formats that combine visual appeal with functional performance.

Rapid Growth in Emerging Markets and Urban Consumption Trends

Emerging economies present strong growth opportunities for the cider packaging market due to rising urbanization and changing consumer lifestyles. Countries such as India, Brazil, and several Southeast Asian nations are witnessing increasing adoption of flavored alcoholic beverages, including cider. Urban consumers in these regions prefer convenient packaging formats such as cans and lightweight bottles, which support on-the-go consumption. For example, local beverage startups in Brazil are introducing fruit-based cider products in modern aluminum packaging to attract younger consumers. This trend is expected to expand as retail infrastructure improves and disposable incomes rise. Packaging manufacturers that offer cost-effective and scalable solutions are likely to benefit significantly from this market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.8 Billion |

| Market Size in 2026 | USD 5.1 Billion |

| Market Size in 2034 | USD 9.2 Billion |

| CAGR | 7.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

Type Segment

Glass bottles dominate the cider packaging market with a 41.3% share in 2024 due to their premium appearance and superior product preservation capabilities. Glass is widely used in Europe and North America, where cider is positioned as a high-quality beverage. It helps maintain flavor integrity and extends shelf life while offering strong branding opportunities through customized designs. Traditional cider producers continue to rely on glass packaging to reinforce authenticity and heritage values in their products.

Aluminum cans are the fastest-growing subsegment, with a CAGR of 8.9%, driven by convenience, portability, and sustainability advantages. Canned cider is increasingly popular among younger consumers and outdoor consumption occasions such as festivals and events. The lightweight nature of cans reduces transportation costs and improves recycling efficiency. Future growth is expected to be driven by innovation in resealable and digitally enhanced cans.

Material Segment

Glass remains the dominant material with a 38.5% share in 2024 due to its premium positioning and recyclability. It is widely used in traditional cider markets where product authenticity is a key selling factor. Glass packaging continues to be favored for premium and export-oriented cider products.

Paper-based packaging is the fastest-growing segment with a CAGR of 6.8%, driven by sustainability trends and regulatory pressure. Beverage companies are increasingly adopting paper-based secondary packaging solutions to reduce environmental impact. Advancements in barrier coatings are improving durability and moisture resistance, supporting wider adoption in the future.

End-Use Segment

Retail and supermarkets dominate the end-use segment with a 45.6% share in 2024 due to strong product visibility and consumer accessibility. Packaging plays a crucial role in influencing purchasing decisions in retail environments through design and branding.

Online retail is the fastest-growing end-use channel with a CAGR of 9.1%, driven by rapid expansion of e-commerce alcohol delivery services. Demand for durable and protective packaging is increasing as more consumers shift toward home delivery options.

Cider Packaging Market Segmentations

By Material Type

- Glass Bottles

- Metal Cans (Aluminum & Steel)

- Plastic Bottles (PET & Others)

- Paper-Based Packaging

- Compostable/Bio-Based Materials

By Packaging Type

- Bottles

- Cans

- Pouches

- Kegs & Bulk Containers

- Cartons & Boxes

By Closure Type

- Corks

- Screw Caps

- Crown Caps

- Snap-On Lids

- Dispensing Taps

By Distribution Channel

- On-Trade (Bars, Pubs, Restaurants)

- Off-Trade (Supermarkets & Hypermarkets)

- Online Retail

- Specialty Stores

- Direct-to-Consumer (DTC)

Regional Analysis

North America

North America accounted for approximately 28.6% of the global cider packaging market in 2025, with a projected CAGR of 7.2% through the forecast period. The region benefits from strong cider consumption patterns, particularly in the United States and Canada, where craft beverages are widely popular. Packaging demand is driven by premiumization trends and the expansion of flavored cider products. Sustainability initiatives are also influencing packaging material selection, with companies shifting toward recyclable aluminum cans and lightweight glass bottles. Increased focus on branding and product differentiation is further enhancing packaging innovation across the region.

The United States remains the dominant country in North America due to its large craft beverage industry and advanced retail infrastructure. A key growth driver is the expansion of direct-to-consumer alcohol delivery services, which require secure and durable packaging solutions. For instance, craft cider producers in states such as Oregon and California are increasingly adopting digitally enhanced packaging formats to engage consumers and strengthen brand identity.

Europe

Europe holds around 32.1% of the global cider packaging market in 2025, with a CAGR of 7.5%. The region has a long-standing tradition of cider production, particularly in the United Kingdom, France, and Spain. Sustainability regulations and strict recycling policies are key factors shaping packaging demand. Manufacturers are increasingly focusing on recyclable and lightweight packaging formats to comply with environmental standards.

The United Kingdom leads the European market due to high cider consumption and strong domestic production. A major growth driver is the implementation of extended producer responsibility policies that require companies to manage packaging waste efficiently. This has led to widespread adoption of eco-friendly glass bottles and recyclable labeling systems in the cider industry.

Asia Pacific

Asia Pacific dominates the global market with a 37.4% share in 2025 and is expected to grow at a CAGR of 8.4%, making it the fastest-growing region. Rising disposable incomes, urbanization, and increasing exposure to Western drinking habits are driving cider consumption. Packaging demand is expanding rapidly in countries such as China, Japan, Australia, and India.

China leads the regional market due to its large consumer base and expanding beverage industry. A key growth driver is the rapid expansion of online alcohol retail platforms, which are increasing demand for lightweight and durable packaging solutions. Imported cider products are increasingly being sold in canned formats to cater to urban consumers seeking convenience and affordability.

Middle East & Africa

The Middle East & Africa region holds 6.8% of the global market in 2025, with a CAGR of 6.1%. Growth is primarily supported by tourism, hospitality development, and expatriate consumption. Alcohol consumption is regulated in several countries, limiting market expansion but creating niche demand in urban hospitality sectors.

The United Arab Emirates leads the region due to its strong tourism industry and premium hospitality sector. A key driver is the increasing demand for imported alcoholic beverages in luxury hotels and licensed retail outlets. Premium glass packaging is widely used to enhance product presentation in high-end hospitality environments.

Latin America

Latin America accounts for 9.2% of the global market in 2025 and is expected to grow at a CAGR of 6.2%. Rising urbanization and increasing diversification of alcoholic beverage consumption are supporting market growth. Brazil and Argentina are the primary contributors.

Brazil dominates the regional market due to growing consumer interest in flavored alcoholic beverages. A key growth driver is the emergence of local craft beverage producers introducing innovative packaging formats such as aluminum cans and PET bottles. These packaging solutions are particularly popular among younger consumers seeking affordable and portable beverage options.

Competitive Landscape

The cider packaging market is moderately consolidated with key players focusing on sustainability, lightweight materials, and packaging innovation. Major companies include Amcor, Ball Corporation, Ardagh Group, Crown Holdings, and Owens-Illinois. Amcor leads the market due to its extensive global presence and strong portfolio of sustainable packaging solutions. Companies are investing in recyclable materials, smart packaging technologies, and capacity expansion to strengthen market position.

Key Players

- Amcor plc

- Ball Corporation

- Ardagh Group

- Crown Holdings Inc.

- Owens-Illinois Inc.

- Stora Enso

- Smurfit Kappa Group

- Berry Global Inc.

- WestRock Company

- DS Smith Plc

- Gerresheimer AG

- Vetropack Holding AG

- Nampak Ltd.

- Plastipak Holdings Inc.

- Verallia SA