Chlorine Free Shrink Bags Market Size and Growth

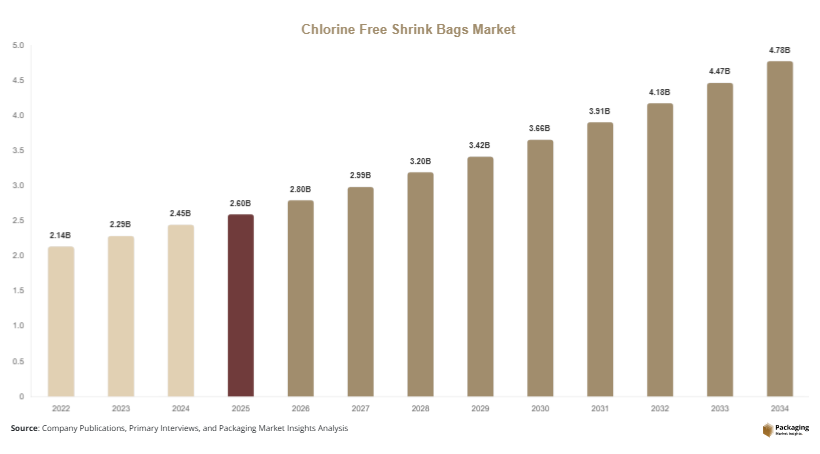

The global chlorine free shrink bags market was valued at USD 2.6 billion in 2025 and is projected to reach USD 4.8 billion by 2034, expanding at a CAGR of 6.9% (2025–2034). The market is also estimated to reach USD 2.8 billion in 2026, supported by steady adoption across food packaging, industrial bundling, and pharmaceutical logistics applications. Chlorine-free shrink bags are flexible packaging solutions manufactured without chlorine-based compounds, primarily designed to reduce environmental toxicity and improve recyclability. These bags are widely used in sectors requiring high clarity packaging, strong sealing performance, and reduced environmental footprint.

The market is experiencing consistent expansion due to several structural growth factors. First, increasing regulatory pressure on PVC-based packaging materials is pushing manufacturers toward chlorine-free alternatives such as polyethylene (PE) and polyolefin-based shrink films. Second, rising demand for sustainable food packaging in retail and e-commerce logistics is strengthening adoption across global supply chains. Third, advancements in multilayer film technology are improving barrier strength, clarity, and shrink performance, making chlorine-free variants more competitive.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share.

- Plastic packaging dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 10.4 billion in 2025 and USD 11.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Polyolefin-Based Chlorine-Free Shrink Films

One of the most significant trends in the chlorine free shrink bags market is the rapid shift from PVC-based shrink films to polyolefin-based alternatives. Polyolefin materials provide superior clarity, better sealing strength, and significantly lower environmental impact compared to chlorine-based polymers. Retail and food packaging companies are increasingly adopting these materials for bundled packaging of beverages, bakery products, and frozen foods. For example, supermarket chains in Europe are replacing traditional PVC shrink wraps with PE-based chlorine-free alternatives to comply with environmental regulations. In the future, this trend is expected to accelerate as brand owners prioritize sustainability labeling and recyclable packaging certification.

Growth of E-Commerce Protective Packaging Applications

Another key trend is the increasing use of chlorine-free shrink bags in e-commerce logistics and protective packaging. The rise in global online retail has increased demand for tamper-evident, lightweight, and durable packaging solutions. Chlorine-free shrink bags are widely used to secure electronics, cosmetics, and consumer goods during transportation. Companies such as Amazon and regional logistics providers in Asia are integrating shrink packaging for bundle sealing and product protection. In the coming years, automation in packaging lines and smart logistics systems will further expand adoption, particularly in cross-border e-commerce shipments requiring high packaging durability.

Market Drivers

Regulatory Push Against Chlorine-Based Plastics

The primary driver of the market is the global regulatory shift away from chlorine-based plastics such as PVC due to environmental and health concerns. Governments in Europe, North America, and parts of Asia are implementing strict regulations on toxic emissions during production and disposal of chlorine-containing materials. This has forced packaging manufacturers to transition toward chlorine-free alternatives. For example, the European Union’s packaging waste directives are encouraging FMCG companies to adopt recyclable shrink packaging solutions. As compliance costs rise for traditional plastics, chlorine-free shrink bags are becoming a preferred alternative across industries.

Expansion of Processed Food and Retail Packaging Demand

Another major driver is the rapid expansion of processed food, frozen food, and organized retail sectors. Chlorine-free shrink bags are widely used for multipack bundling of food items, beverages, and household products. The rise of supermarkets, hypermarkets, and convenience stores in emerging economies is increasing demand for visually appealing and durable packaging. For instance, food brands in India and Southeast Asia are increasingly adopting shrink packaging for snack bundles and bottled beverages. The continued growth of modern retail infrastructure is expected to significantly support long-term market expansion.

Market Restraint

High Cost of Raw Materials and Processing Complexity

A key restraint in the chlorine free shrink bags market is the relatively high production cost compared to conventional PVC shrink films. Polyolefin and polyethylene-based resins used in chlorine-free shrink bags require advanced polymerization processes, increasing manufacturing costs. Additionally, multilayer film structures used to enhance performance add further complexity and cost to production.

Small and medium-sized packaging manufacturers often face challenges in adopting chlorine-free solutions due to capital investment requirements for new extrusion and sealing equipment. In price-sensitive markets such as Africa and parts of Latin America, traditional PVC shrink films still dominate due to their lower cost. For example, local food packaging suppliers often continue using chlorine-based shrink materials for bulk packaging despite environmental concerns. This cost disparity slows down full-scale adoption, especially in developing economies where cost efficiency outweighs sustainability considerations.

Market Opportunities

Rising Demand for Sustainable FMCG Packaging

A major opportunity lies in the growing demand for sustainable packaging across FMCG brands. Global consumer goods companies are actively transitioning toward eco-friendly packaging to meet sustainability targets. Chlorine-free shrink bags are increasingly being used for personal care products, bottled beverages, and packaged foods. Companies such as multinational beverage brands are redesigning packaging lines to incorporate recyclable shrink wraps. This shift presents significant opportunities for manufacturers to supply high-performance sustainable films with improved branding and recyclability features.

Technological Advancements in Multilayer Film Engineering

Another major opportunity is the development of advanced multilayer shrink film technologies. Innovations in polymer blending, nano-coatings, and barrier enhancement are improving performance characteristics such as puncture resistance, shrink ratio, and transparency. These advancements allow chlorine-free shrink bags to compete directly with traditional PVC films. In the future, smart packaging integration and biodegradable additives may further expand application areas in pharmaceuticals and high-value electronics packaging.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.6 Billion |

| Market Size in 2026 | USD 2.8 Billion |

| Market Size in 2034 | USD 4.8 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Standard chlorine-free shrink bags dominate the market with the largest share due to their wide usage in retail bundling and food packaging applications. These bags offer cost efficiency, flexibility, and compatibility with automated packaging systems.

High-performance shrink bags are the fastest-growing segment due to increasing demand for premium packaging in pharmaceuticals and electronics.

By Material

Polyethylene-based shrink bags dominate due to superior flexibility and recyclability. They are widely used in food and beverage packaging applications.

Polyolefin-based shrink bags are the fastest-growing due to their high clarity, strength, and environmental advantages.

By End-Use

Food & beverage is the dominant segment due to extensive use in multipack packaging and retail bundling.

E-commerce logistics is the fastest-growing segment due to rising online retail shipments and demand for protective packaging solutions.

Chlorine Free Shrink Bags Market Segmentations

By Source Type

- Post-Consumer Glass

- Industrial Waste Glass

- Commercial Scrap Glass

- Construction & Demolition Glass Waste

By End-Use Application

- Packaging (Bottles & Containers)

- Construction Materials

- Fiberglass Manufacturing

- Road Construction & Aggregates

- Decorative & Art Glass

By Processing Type

- Crushed Cullet Processing

- Color-Sorted Recycling

- Mixed Glass Recycling

- Refined High-Purity Glass Processing

Regional Analysis

North America

North America accounted for a significant share of the market in 2025, driven by strong demand from food retail, pharmaceuticals, and e-commerce packaging. The region benefits from strict environmental regulations and high consumer awareness regarding sustainable packaging. Growth is supported by expanding online grocery delivery services and retail modernization.

The United States dominates the region, driven by large-scale adoption of eco-friendly packaging in FMCG and logistics sectors. Major retail chains are increasingly replacing PVC shrink films with chlorine-free alternatives for compliance with sustainability commitments.

Europe

Europe holds a strong market share due to strict regulatory frameworks on plastic usage and high recycling standards. The region continues to lead in sustainability adoption, especially in Germany, France, and the UK.

Germany is the dominant country, supported by advanced packaging manufacturing infrastructure and strong circular economy policies. Retailers in Germany are heavily investing in recyclable shrink packaging systems for food and beverage distribution.

Asia Pacific

Asia Pacific dominates the global market due to large-scale manufacturing, rising population, and expanding retail infrastructure. The region also benefits from cost-effective production facilities and growing export-oriented packaging industries.

China leads the region, driven by massive food processing industries and strong packaging export demand. Increasing e-commerce penetration is also accelerating shrink bag consumption across logistics applications.

Middle East & Africa

The region is experiencing steady growth due to rising food import dependency and expansion of retail supermarkets. Demand is increasing for durable packaging solutions in logistics and food distribution.

The UAE is the dominant country, supported by its role as a regional trade hub. Growth is driven by increasing adoption of modern retail formats and imported packaged goods.

Latin America

Latin America is projected to be the fastest-growing region due to increasing urbanization, retail expansion, and rising packaged food consumption. Demand is increasing across Brazil, Mexico, and Argentina.

Brazil leads the region, driven by expansion of supermarket chains and food processing industries. Growing awareness of sustainable packaging is also supporting chlorine-free shrink bag adoption.

Competitive Landscape

The market is moderately consolidated with key players focusing on sustainability, product innovation, and capacity expansion. Major companies include Sealed Air Corporation, Amcor plc, Berry Global Inc., Coveris Holdings, and Sigma Plastics Group.

Among these, Amcor plc is a leading player due to its strong global presence and continuous investment in recyclable and chlorine-free packaging solutions.

Companies are focusing on bio-based materials, advanced film extrusion technologies, and strategic partnerships with FMCG brands. Recent developments include expansion of sustainable film production facilities and introduction of high-performance recyclable shrink packaging lines.

Key Players List

- Amcor plc

- Sealed Air Corporation

- Berry Global Inc.

- Coveris Holdings

- Sigma Plastics Group

- Winpak Ltd.

- Intertape Polymer Group

- Plastissimo Film Co.

- Flexopack SA

- Bolloré Group

- DuPont Teijin Films

- Sudpack Verpackungen

- RKW Group

- Bonset America Corporation

- Ceisa Packaging