Ceramic Packaging Market Size and Growth

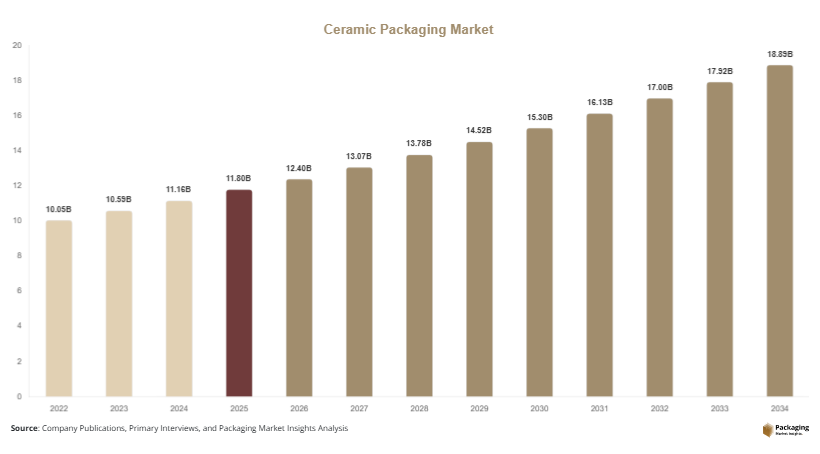

The global ceramic packaging market was valued at USD 11.8 billion in 2025 and is projected to reach USD 18.9 billion by 2034, expanding at a CAGR of 5.4% during the forecast period from 2025 to 2034. The market reached an estimated value of USD 12.4 billion in 2026, driven by increasing demand for high-performance packaging materials across electronics, healthcare, aerospace, automotive, and semiconductor industries. Ceramic packaging solutions are widely used in applications that require high thermal stability, corrosion resistance, electrical insulation, and durability under extreme operating conditions.

The growing semiconductor manufacturing industry is one of the primary growth drivers supporting market expansion. Ceramic packaging materials are increasingly adopted for integrated circuits, sensors, LEDs, and microelectronic devices because they provide superior thermal conductivity and long operational life. Rising investments in advanced electronics manufacturing across Asia Pacific and North America continue to strengthen demand for ceramic substrates and multilayer ceramic packages.

Key Market Highlights

- Asia Pacific dominated the market with a 41.3% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Alumina ceramic packaging led the type segment with a 36.8% share.

- Ceramic-metal composite materials dominated with a 48.7% share.

- Electronics and semiconductor applications led the segment with 52.1% share.

- The US remained the dominant country with a market size of USD 2.6 billion in 2025 and USD 2.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Ceramic Packaging in Semiconductor Manufacturing

The semiconductor industry is increasingly adopting ceramic packaging solutions due to rising demand for advanced computing, artificial intelligence processors, and high-frequency communication devices. Ceramic materials provide superior heat dissipation and electrical insulation, which are essential for high-performance integrated circuits and power electronics. Semiconductor manufacturers are transitioning toward multilayer ceramic substrates and hermetic ceramic packages to improve component durability and reliability.

For example, advanced semiconductor fabrication facilities in Taiwan, South Korea, and the United States are investing in ceramic packaging technologies for next-generation processors and AI accelerators. These packaging solutions help maintain device stability under high thermal loads while enabling compact component integration. Future developments in chip miniaturization and high-density electronics are expected to increase demand for ceramic packaging across data centers, industrial automation systems, and telecommunications infrastructure.

Expansion of Ceramic Packaging in Electric Vehicle Electronics

The rapid expansion of electric vehicle production is creating strong demand for ceramic packaging materials used in automotive electronics. Electric vehicles require advanced packaging solutions capable of handling high temperatures, voltage fluctuations, and harsh operating conditions. Ceramic packaging is increasingly used in power modules, battery systems, onboard chargers, and electronic control units.

Automotive manufacturers are integrating ceramic substrates into power semiconductor systems to improve thermal management and energy efficiency. For instance, silicon carbide power devices used in electric vehicles rely heavily on ceramic packaging for operational reliability. As governments continue to support electric mobility adoption and charging infrastructure expansion, the demand for durable and lightweight ceramic packaging solutions is expected to rise steadily. Future innovations may include ultra-thin ceramic substrates and hybrid ceramic-polymer packaging systems for next-generation mobility applications.

Market Drivers

Increasing Demand for High-Performance Electronics

The growing demand for high-performance electronic devices is one of the major factors driving the ceramic packaging market. Industries such as telecommunications, aerospace, consumer electronics, and industrial automation increasingly require packaging materials capable of handling high temperatures and electrical loads. Ceramic packaging offers excellent thermal conductivity, corrosion resistance, and dimensional stability, making it suitable for sensitive electronic components.

The expansion of 5G networks and artificial intelligence infrastructure has significantly increased the use of advanced semiconductors and microelectronics. Ceramic packaging solutions help improve device lifespan while ensuring stable performance in high-frequency environments. For example, telecommunications equipment manufacturers are using ceramic substrates in radio frequency modules and signal amplifiers. The increasing complexity of electronic devices is expected to strengthen long-term demand for ceramic packaging technologies.

Growth of Medical Electronics and Implantable Devices

The rising use of medical electronics and implantable healthcare devices is another important growth driver supporting market expansion. Medical applications require highly reliable packaging solutions capable of protecting sensitive components from moisture, contamination, and chemical exposure. Ceramic packaging materials provide strong biocompatibility and long-term stability, making them suitable for implantable electronics and diagnostic equipment.

Healthcare companies are increasingly investing in miniaturized medical sensors, wearable monitoring systems, and implantable cardiac devices. Ceramic packages help maintain performance consistency while supporting device safety and durability. For instance, ceramic housings are widely used in pacemakers and neurostimulation systems because they can withstand harsh biological environments. As healthcare infrastructure expands globally and medical electronics adoption rises, ceramic packaging demand is expected to grow significantly during the forecast period.

Market Restraint

High Manufacturing Costs and Complex Processing Requirements

High manufacturing costs remain a significant restraint affecting the ceramic packaging market. Ceramic packaging materials require specialized manufacturing processes involving high-temperature sintering, precision machining, multilayer integration, and strict quality control measures. These production requirements increase operational expenses and limit adoption among cost-sensitive industries.

Compared to plastic and metal packaging alternatives, ceramic packaging solutions often involve higher raw material costs and longer production cycles. Small and medium-sized electronics manufacturers may face challenges in integrating ceramic packaging technologies due to capital investment requirements. Additionally, advanced ceramic composites used in aerospace and semiconductor applications require sophisticated processing equipment and technical expertise.

For example, semiconductor-grade ceramic packages must meet strict dimensional accuracy and thermal performance standards, increasing production complexity. Supply chain disruptions affecting ceramic raw materials such as alumina and zirconia can also impact manufacturing costs. While ceramic packaging offers superior durability and reliability, pricing limitations may restrict wider adoption in low-cost consumer electronics applications. Manufacturers continue to focus on automation and material optimization strategies to reduce production costs and improve scalability.

Market Opportunities

Growing Opportunities in Aerospace and Defense Electronics

The aerospace and defense industries are creating substantial opportunities for ceramic packaging manufacturers. Aircraft communication systems, radar modules, satellite electronics, and defense sensors require highly durable packaging materials capable of operating under extreme temperatures and environmental conditions. Ceramic packaging provides thermal resistance, mechanical stability, and electromagnetic shielding, making it suitable for mission-critical applications.

Governments worldwide are increasing defense modernization investments and expanding satellite communication infrastructure. Ceramic packaging solutions are increasingly used in avionics systems, missile guidance technologies, and military communication equipment. For example, aerospace electronics manufacturers are adopting multilayer ceramic substrates for high-frequency radar applications. The increasing use of space exploration technologies and advanced defense electronics is expected to generate long-term growth opportunities for the market.

Expansion of Renewable Energy Infrastructure

The expansion of renewable energy systems is also creating new opportunities for ceramic packaging applications. Solar power systems, wind turbines, and energy storage infrastructure require advanced power electronics capable of handling high voltages and harsh environmental conditions. Ceramic packaging materials improve thermal management and operational reliability in renewable energy equipment.

Manufacturers are increasingly integrating ceramic substrates into inverters, power converters, and battery management systems used in renewable energy projects. For example, ceramic packaging is widely used in silicon carbide power devices that improve energy conversion efficiency in solar installations. The growing focus on energy efficiency and carbon emission reduction is expected to increase investment in advanced power electronics, supporting demand for ceramic packaging technologies during the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.8 Billion |

| Market Size in 2026 | USD 12.4 Billion |

| Market Size in 2034 | USD 18.9 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Alumina ceramic packaging dominated the type segment with a 36.8% market share in 2024 due to its excellent thermal conductivity, electrical insulation, and cost-effectiveness. Alumina ceramics are widely used across semiconductor packaging, industrial electronics, and automotive power modules because they provide strong mechanical durability and high resistance to thermal stress. Electronics manufacturers increasingly prefer alumina ceramic substrates for integrated circuits and LED packaging applications due to their long operational lifespan and stable performance. For example, semiconductor fabrication companies use alumina-based packages in high-power devices and communication equipment. The growing expansion of 5G infrastructure and industrial automation systems has further strengthened demand for alumina ceramic packaging solutions globally.

Silicon nitride ceramic packaging is projected to register the fastest CAGR of 6.8% during the forecast period. The segment is witnessing rapid growth due to increasing demand for lightweight and high-strength materials in electric vehicles and aerospace electronics. Silicon nitride offers superior fracture toughness and thermal shock resistance compared to traditional ceramic materials. Automotive manufacturers are increasingly adopting silicon nitride substrates for high-voltage power electronics and battery systems used in electric vehicles. In addition, aerospace companies are integrating advanced ceramic packaging into radar systems and avionics equipment. Future growth is expected to be supported by expanding renewable energy infrastructure and increasing demand for high-efficiency semiconductor devices.

By Material

Ceramic-metal composite materials accounted for the largest market share of 48.7% in 2024 due to their ability to combine the thermal performance of ceramics with the structural strength of metals. These materials are widely used in aerospace, defense, and semiconductor applications where durability and heat dissipation are essential. Manufacturers increasingly rely on ceramic-metal composites for hermetic electronic packaging and high-frequency communication systems. For example, multilayer ceramic-metal packages are extensively used in military communication equipment and industrial power electronics. The increasing complexity of semiconductor devices and the growing use of high-performance sensors are further contributing to segment dominance.

Advanced ceramic composites are expected to grow at the fastest CAGR of 6.5% during the forecast period. The segment is benefiting from rising demand for lightweight materials with superior mechanical properties and thermal efficiency. Advanced ceramic composites are increasingly used in electric mobility systems, medical electronics, and next-generation telecommunications equipment. Manufacturers are focusing on developing hybrid ceramic materials that support miniaturization and improved energy efficiency. For instance, advanced ceramic composites are being integrated into silicon carbide power modules used in renewable energy systems and electric vehicles. Increasing investments in advanced materials research and semiconductor packaging innovation are expected to drive future segment growth.

By End-Use

Electronics and semiconductor applications dominated the end-use segment with a 52.1% market share in 2024. The segment benefits from rising global demand for semiconductors, integrated circuits, communication modules, and industrial electronics. Ceramic packaging solutions are widely used in electronic devices because they offer superior thermal management, dimensional stability, and corrosion resistance. Semiconductor manufacturers increasingly adopt ceramic packages for advanced processors, power modules, and high-frequency communication systems. For example, ceramic substrates are commonly used in artificial intelligence processors and cloud computing infrastructure. The continued expansion of data centers, telecommunications infrastructure, and consumer electronics production is expected to support segment growth during the forecast period.

Healthcare applications are projected to witness the fastest CAGR of 6.7% through 2034 due to increasing adoption of implantable electronics, wearable monitoring systems, and diagnostic equipment. Ceramic packaging materials provide biocompatibility, moisture resistance, and long-term reliability required for medical applications. Medical device manufacturers are increasingly integrating ceramic housings into pacemakers, neurostimulators, and imaging systems. The growing aging population and rising healthcare technology investments are accelerating demand for advanced medical electronics globally. Future opportunities are expected to emerge from miniaturized implantable devices and remote patient monitoring technologies that require highly durable and compact ceramic packaging solutions.

Ceramic Packaging Market Segmentations

By Type

- Alumina Ceramic Packaging

- Aluminum Nitride Ceramic Packaging

- Silicon Nitride Ceramic Packaging

- Zirconia Ceramic Packaging

- Glass Ceramic Packaging

By Material

- Ceramic-Metal Composite Materials

- Advanced Ceramic Composites

- Multilayer Ceramic Materials

- Oxide Ceramics

- Non-Oxide Ceramics

By End-User

- Electronics & Semiconductor

- Healthcare & Medical Devices

- Automotive Electronics

- Aerospace & Defense

- Industrial Equipment

- Telecommunications

Regional Analysis

North America

North America accounted for 24.6% of the global ceramic packaging market share in 2025 and is projected to expand at a CAGR of 5.2% during the forecast period. The region benefits from strong semiconductor manufacturing investments, growing aerospace production, and rising adoption of advanced medical electronics. The United States and Canada continue to invest heavily in next-generation electronics infrastructure, including artificial intelligence systems, cloud computing facilities, and defense communication technologies. The growing demand for high-frequency packaging solutions in telecommunications and automotive electronics is supporting regional market expansion. Increasing research activities focused on advanced ceramic materials are also contributing to technological innovation across the packaging industry.

The United States remained the dominant country in North America due to its advanced semiconductor ecosystem and expanding aerospace industry. Rising investments in electric vehicle manufacturing and military electronics continue to drive ceramic packaging demand. For example, semiconductor companies in Arizona and Texas are expanding fabrication facilities that require advanced ceramic substrates and packaging solutions. The country is also witnessing growing adoption of ceramic packaging in implantable medical devices and diagnostic systems. Increasing government support for domestic semiconductor manufacturing and technology innovation is expected to strengthen market growth during the forecast period.

Europe

Europe represented 22.1% of the global ceramic packaging market in 2025 and is forecast to grow at a CAGR of 5.0% through 2034. The region is witnessing increasing demand for ceramic packaging solutions across automotive electronics, industrial automation, and renewable energy applications. European manufacturers are focusing on energy-efficient electronics and sustainable industrial production, supporting adoption of advanced ceramic materials. The rapid expansion of electric vehicle infrastructure across Germany, France, and the Nordic countries is increasing demand for power electronics packaging solutions. Rising investments in smart manufacturing and industrial robotics are further supporting market growth across the region.

Germany emerged as the leading country within the European market due to its strong automotive and industrial electronics industries. The country’s rapid transition toward electric mobility has increased demand for ceramic packaging materials used in battery systems and power semiconductors. For instance, automotive suppliers in Germany are adopting ceramic substrates for high-voltage electric vehicle modules to improve thermal management and energy efficiency. The country also benefits from strong research capabilities in advanced ceramics and semiconductor technologies. Increasing adoption of industrial automation systems is expected to strengthen long-term market expansion.

Asia Pacific

Asia Pacific dominated the global ceramic packaging market with a 41.3% share in 2025 and is projected to grow at a CAGR of 5.9% during the forecast period. The region benefits from large-scale semiconductor production, expanding electronics manufacturing, and rapid industrialization across China, Japan, South Korea, and India. Rising consumer electronics demand and increasing investments in 5G infrastructure are driving significant adoption of ceramic packaging technologies. Countries across the region continue to expand semiconductor fabrication capacity to meet global electronics demand. The strong presence of packaging material suppliers and electronics manufacturers supports regional market leadership.

China remained the dominant country in Asia Pacific due to its extensive semiconductor manufacturing ecosystem and rapidly expanding electric vehicle industry. The country continues to invest heavily in domestic chip production and advanced packaging technologies. For example, Chinese electronics manufacturers are increasing adoption of ceramic substrates for power electronics and telecommunications equipment. Rising demand for renewable energy infrastructure and industrial automation systems is further contributing to market growth. Government support for advanced manufacturing and technology localization initiatives is expected to strengthen ceramic packaging demand throughout the forecast period.

Middle East & Africa

The Middle East & Africa ceramic packaging market accounted for 6.8% of the global share in 2025 and is expected to grow at a CAGR of 5.6% during the forecast period. Increasing investments in industrial infrastructure, renewable energy projects, and telecommunications networks are supporting regional market development. Countries across the Gulf region are focusing on industrial diversification strategies that include electronics manufacturing and smart infrastructure projects. Growing demand for durable packaging materials in harsh environmental conditions is encouraging adoption of ceramic-based solutions across industrial applications.

Saudi Arabia emerged as the leading country within the regional market due to expanding industrial automation and renewable energy investments. The country is investing in advanced manufacturing technologies as part of its economic diversification programs. For instance, renewable energy projects in Saudi Arabia increasingly require advanced power electronics that use ceramic packaging materials for improved thermal performance. Rising investments in smart city infrastructure and telecommunications expansion are also creating demand for high-performance electronic packaging solutions. The region is expected to witness gradual growth as industrial modernization activities continue to expand.

Latin America

Latin America held 5.2% of the global ceramic packaging market share in 2025 and is projected to register the fastest CAGR of 6.4% during the forecast period. The region is witnessing rising adoption of industrial electronics, automotive manufacturing, and renewable energy infrastructure. Countries including Brazil and Mexico are expanding electronics assembly operations and automotive production capacity, increasing demand for advanced packaging materials. Growing investments in industrial automation and consumer electronics distribution networks are also supporting market development across the region.

Brazil remained the dominant country within the Latin American market due to expanding automotive production and industrial modernization initiatives. The country is increasingly adopting ceramic packaging technologies for industrial control systems and renewable energy applications. For example, power electronics manufacturers in Brazil are integrating ceramic substrates into energy storage systems and industrial converters to improve efficiency and reliability. Rising demand for advanced medical devices and telecommunications infrastructure is further supporting market growth. Government initiatives promoting industrial development and technology investments are expected to create additional opportunities for ceramic packaging suppliers.

Competitive Landscape

The ceramic packaging market is moderately consolidated, with global manufacturers focusing on material innovation, semiconductor partnerships, and expansion of advanced ceramics production facilities. Companies are investing heavily in multilayer ceramic technologies, hermetic sealing solutions, and high-thermal-conductivity substrates to strengthen their market position across electronics, healthcare, automotive, and aerospace industries.

Kyocera Corporation emerged as one of the leading players in the market due to its extensive ceramic component portfolio, strong semiconductor packaging capabilities, and broad global manufacturing presence. The company continues to expand its advanced ceramic substrate production to support rising demand from semiconductor and automotive electronics applications.

Murata Manufacturing Co., Ltd. is focusing on miniaturized ceramic packaging solutions for communication modules and wearable electronics. The company is increasing investments in multilayer ceramic technologies to improve packaging density and thermal efficiency.

NGK Spark Plug Co., Ltd. is strengthening its position in automotive electronics and industrial ceramics through advanced substrate technologies and high-performance ceramic materials designed for harsh operating environments.

CoorsTek Inc. is expanding its advanced ceramic packaging offerings for aerospace, medical, and defense applications. The company is investing in precision ceramic manufacturing and custom-engineered packaging systems to meet rising demand for mission-critical electronics.

Materion Corporation is emphasizing ceramic-metal packaging technologies and thermal management materials used in semiconductor and defense applications. Strategic collaborations with semiconductor manufacturers are supporting its market expansion efforts.

Manufacturers across the industry are also prioritizing automation, sustainable production processes, and advanced composite materials to improve operational efficiency and reduce manufacturing costs. Increasing demand for electric vehicles, AI processors, and renewable energy systems is expected to intensify competition and encourage further innovation within the market.

Key Players List

- Kyocera Corporation

- Murata Manufacturing Co., Ltd.

- NGK Spark Plug Co., Ltd.

- CoorsTek Inc.

- Materion Corporation

- CeramTec GmbH

- Toshiba Materials Co., Ltd.

- Maruwa Co., Ltd.

- SCHOTT AG

- Amkor Technology, Inc.

- Hitachi Metals, Ltd.

- AdTech Ceramics

- Rogers Corporation

- Heraeus Holding GmbH

- Tong Hsing Electronic Industries Ltd.

- Mitsubishi Materials Corporation

- Fujitsu Limited

- Samsung Electro-Mechanics Co., Ltd.