Carbonated Soft Drink Packaging Market Size and Growth

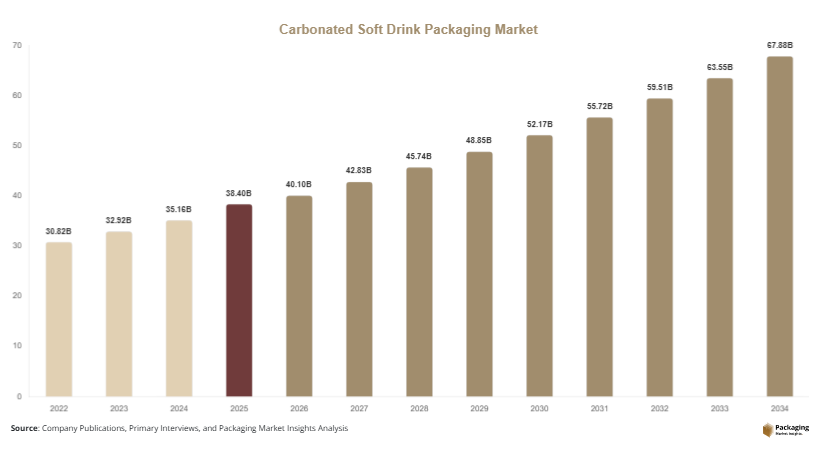

The global carbonated soft drink packaging market size was valued at USD 38.4 billion in 2025 and is projected to reach USD 40.1 billion in 2026, further growing to approximately USD 67.9 billion by 2034, registering a CAGR of 6.8% during 2025–2034. The growth trajectory reflects increased consumption of ready-to-drink beverages and ongoing innovations in packaging formats and materials. The carbonated soft drink packaging market continues to expand steadily, supported by sustained demand for carbonated beverages and evolving consumer preferences for convenience and sustainability.

One of the key growth factors is the rising consumption of carbonated soft drinks in emerging economies. Rapid urbanization, growing disposable incomes, and expanding retail networks are supporting higher product penetration. Additionally, the increasing popularity of smaller, single-serve packaging formats is driving demand for flexible and lightweight packaging solutions.

Key Highlights:

- Asia Pacific dominated the market with a 37.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.5%.

- Rigid packaging led the type segment with a 61.3% share, while flexible packaging is expected to grow at a CAGR of 6.9%.

- Plastic materials dominated with a 48.6% share, while aluminum is forecasted to grow at a CAGR of 7.2%.

- Bottled soft drinks led the application segment with 55.4% share, while canned beverages are expected to grow at a CAGR of 7.1%.

- China remained the dominant country with a market size of USD 6.8 billion in 2025 and USD 7.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Shift Toward Sustainable and Recyclable Packaging

Sustainability has become a central focus in the carbonated soft drink packaging market, with manufacturers actively adopting recyclable and reusable materials. PET bottles with higher recycled content, aluminum cans, and biodegradable packaging alternatives are gaining traction. Companies are redesigning packaging to reduce material usage and improve recyclability. Lightweight packaging solutions are also helping reduce transportation emissions and overall environmental impact. This trend is driven by both regulatory requirements and consumer awareness, particularly in developed markets. As sustainability initiatives continue to evolve, companies are expected to invest further in eco-friendly packaging innovations.

Growth of On-the-Go and Single-Serve Packaging Formats

The demand for convenient, single-serve packaging formats is increasing, driven by busy lifestyles and changing consumption patterns. Consumers prefer smaller packaging sizes that are easy to carry and consume. This has led to the growth of mini cans, slim bottles, and resealable packaging options. These formats are particularly popular in urban areas and among younger consumers. Additionally, packaging designs are being optimized for portability and ease of use. The trend is also influencing product pricing and marketing strategies, as brands introduce smaller packs at competitive price points to attract a broader consumer base.

Market Drivers

Rising Demand for Ready-to-Drink Beverages

The increasing consumption of ready-to-drink carbonated beverages is a major driver for the carbonated soft drink packaging market. Consumers are seeking convenient beverage options that require no preparation, leading to higher demand for packaged soft drinks. This trend is particularly strong in urban areas, where busy lifestyles drive the need for quick refreshment options. Packaging plays a critical role in maintaining product quality and ensuring ease of consumption. Manufacturers are focusing on innovative packaging designs that enhance convenience and extend shelf life.

Expansion of Retail and Distribution Networks

The growth of organized retail and distribution channels is supporting market expansion. Supermarkets, convenience stores, and online platforms are increasing the availability of carbonated soft drinks. This requires efficient and durable packaging solutions that can withstand transportation and storage conditions. Additionally, the rise of e-commerce is driving demand for packaging that ensures product safety during delivery. Companies are investing in packaging technologies that improve durability and reduce damage during transit, further supporting market growth.

Market Restraint

Environmental Concerns and Regulatory Pressure

Environmental concerns related to plastic waste and carbon emissions are posing challenges to the carbonated soft drink packaging market. Governments worldwide are implementing strict regulations to reduce single-use plastics and promote recycling. Compliance with these regulations often requires significant investment in new materials and technologies. For example, transitioning from conventional plastic bottles to recyclable or biodegradable alternatives can increase production costs and require changes in manufacturing processes. Additionally, consumer pressure for sustainable packaging is increasing, forcing companies to adapt quickly. These factors can impact profitability and slow down market growth in certain regions.

Market Opportunities

Development of Lightweight and Cost-Effective Packaging

The development of lightweight packaging solutions presents significant opportunities in the market. Reducing the weight of packaging materials helps lower transportation costs and environmental impact. Advances in material science are enabling the production of thinner yet durable bottles and cans. These innovations not only improve cost efficiency but also enhance sustainability. Companies that invest in lightweight packaging technologies can gain a competitive advantage by offering cost-effective and eco-friendly solutions.

Adoption of Smart Packaging Technologies

Smart packaging technologies are creating new opportunities for market growth. Features such as QR codes, NFC tags, and temperature-sensitive labels are enhancing consumer engagement and product traceability. These technologies allow brands to provide additional information and interactive experiences to consumers. Smart packaging also helps improve supply chain management by enabling real-time tracking and monitoring. As the demand for premium and innovative products increases, the adoption of smart packaging solutions is expected to grow.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38.4 Billion |

| Market Size in 2026 | USD 40.1 Billion |

| Market Size in 2034 | USD 67.9 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Rigid packaging dominated the market, accounting for 61.3% share in 2024. This segment includes bottles and cans that are widely used for carbonated soft drinks. Rigid packaging provides excellent protection against pressure and carbonation loss, ensuring product quality and safety. It also offers durability and ease of handling, making it suitable for large-scale distribution.

Flexible packaging is expected to be the fastest-growing segment, with a CAGR of 6.9%. This includes pouches and flexible containers that are gaining popularity due to their lightweight design and cost efficiency. The growth of this segment is driven by increasing demand for innovative packaging formats and sustainability considerations.

By Material

Plastic dominated the market with a 48.6% share in 2024, due to its versatility, durability, and cost-effectiveness. PET bottles are widely used for carbonated soft drinks due to their ability to withstand pressure and maintain product freshness. Plastic packaging also allows for various shapes and sizes, enhancing product differentiation.

Aluminum is the fastest-growing segment, with a CAGR of 7.2%. Aluminum cans are gaining popularity due to their recyclability and lightweight properties. They also provide excellent barrier protection, preserving the taste and quality of beverages. The increasing focus on sustainability is driving the adoption of aluminum packaging.

By Application

Bottled soft drinks dominated the market, accounting for 55.4% share in 2024. Bottles are widely used due to their convenience, portability, and resealability. They are suitable for both single-serve and multi-serve packaging formats, making them a preferred choice for consumers.

Canned beverages are expected to be the fastest-growing segment, with a CAGR of 7.1%. Cans are gaining popularity due to their recyclability and compact design. They are particularly favored for single-serve packaging and on-the-go consumption, driving their growth in the market.

Carbonated Soft Drink Packaging Market Segmentations

By Type

- Rigid Packaging

- Flexible Packaging

By Material

- Plastic

- Glass

- Metal (Aluminum)

By Application

- Bottled Soft Drinks

- Canned Beverages

- Other Formats

Regional Analysis

North America

North America accounted for approximately 28.7% of the market share in 2025 and is expected to grow at a CAGR of 6.4%. The region benefits from a well-established beverage industry and high consumer demand for carbonated soft drinks. The adoption of sustainable packaging solutions is also gaining momentum, driven by regulatory requirements and consumer preferences.

The United States dominates the regional market due to its large consumer base and strong presence of beverage manufacturers. A key growth factor is the increasing demand for recyclable aluminum cans, which are widely used in the region due to their sustainability and convenience.

Europe

Europe held a market share of 23.9% in 2025 and is projected to grow at a CAGR of 6.6%. The region is characterized by strict environmental regulations and a strong focus on sustainability. Companies are investing in recyclable and biodegradable packaging materials to comply with these regulations.

Germany is the leading country in the European market, supported by its advanced manufacturing capabilities. A unique growth factor is the widespread adoption of deposit return schemes, which encourage recycling and increase the use of sustainable packaging materials.

Asia Pacific

Asia Pacific dominated the market with a 37.1% share in 2025 and is expected to grow at a CAGR of 7.1%. Rapid urbanization, rising disposable incomes, and expanding retail networks are driving demand for carbonated soft drinks in the region.

China is the dominant country, driven by its large population and growing beverage industry. A key growth factor is the increasing consumption of affordable packaged beverages, which is driving demand for cost-effective packaging solutions.

Middle East & Africa

The Middle East & Africa region accounted for a 5.6% share in 2025 and is expected to grow at a CAGR of 6.9%. The market is expanding due to increasing urbanization and rising demand for packaged beverages.

The United Arab Emirates leads the regional market, supported by its growing retail sector. A unique growth factor is the increasing demand for premium beverage products, which require high-quality packaging solutions.

Latin America

Latin America held a market share of 4.7% in 2025 and is projected to grow at the fastest CAGR of 7.5%. The region is witnessing increasing demand for carbonated soft drinks, driven by changing consumer preferences and economic growth.

Brazil is the dominant country in the region, supported by its large consumer base. A key growth factor is the expansion of local beverage brands, which is driving demand for innovative and cost-effective packaging solutions.

Competitive Landscape

The carbonated soft drink packaging market is highly competitive, with several global players focusing on innovation, sustainability, and cost efficiency. Companies are investing in advanced materials and technologies to enhance packaging performance and reduce environmental impact.

Ball Corporation is a leading player in the market, known for its aluminum packaging solutions. The company recently introduced lightweight aluminum cans to reduce material usage and improve sustainability. Other major players such as Amcor plc, Crown Holdings, and Ardagh Group are also focusing on expanding their product portfolios and strengthening their market presence.

Strategic partnerships, mergers, and acquisitions are common in the market, as companies aim to enhance their capabilities and reach new markets. The focus on sustainability and innovation is expected to drive competition in the coming years.

Key Players List

- Ball Corporation

- Amcor plc

- Crown Holdings, Inc.

- Ardagh Group S.A.

- O-I Glass, Inc.

- Berry Global Inc.

- Silgan Holdings Inc.

- Tetra Pak International S.A.

- Mondi Group

- Sealed Air Corporation

- DS Smith plc

- WestRock Company

- Sonoco Products Company

- Graham Packaging Company

- Plastipak Holdings Inc.