Canada Household Packaging Market Size and Growth

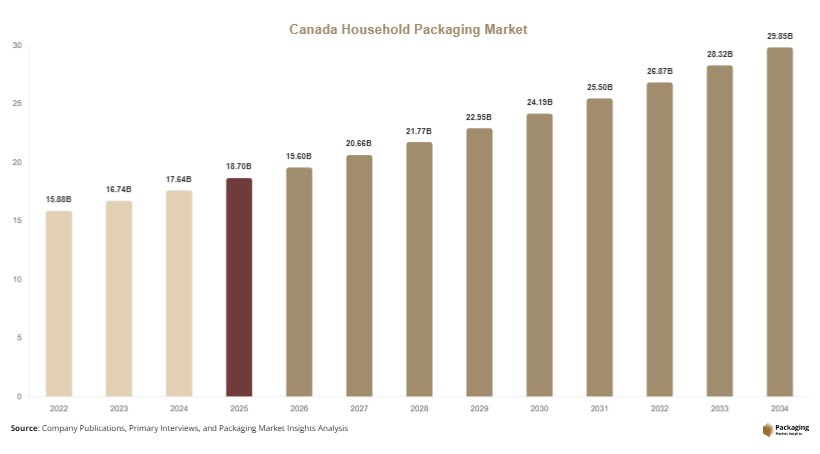

The canada household packaging market size was valued at USD 18.7 billion in 2025 and is projected to reach USD 19.6 billion in 2026. With steady demand from urban households and rising adoption of eco-friendly packaging materials, the market is expected to reach approximately USD 29.8 billion by 2034, registering a CAGR of 5.4% during the forecast period from 2025 to 2034. The canada household packaging market is experiencing stable growth driven by increasing consumer demand for convenient, sustainable, and functional packaging solutions across food, personal care, cleaning products, and other household categories.

Household packaging in Canada includes flexible packaging, rigid containers, cartons, bottles, pouches, and wraps used in everyday consumer goods. The increasing focus on sustainability is one of the primary growth factors shaping the market. Canadian consumers are actively seeking recyclable and biodegradable packaging solutions, prompting manufacturers to innovate and shift away from traditional plastics. Government regulations aimed at reducing single-use plastics are further accelerating this transition.

Key Highlights:

- North America dominated the market with a 34.6% share in 2025, while Asia Pacific is projected to grow at the fastest CAGR of 6.3%.

- Flexible packaging led the type segment with a 36.2% share, while rigid plastic containers are expected to grow at a CAGR of 5.8%.

- Plastic packaging dominated with a 49.7% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

- Food & beverage applications led the segment with 42.5% share, while personal care packaging is expected to grow at a CAGR of 5.7%.

- Canada remained the dominant country with a market size of USD 18.7 billion in 2025 and USD 19.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Recyclable Packaging

The canada household packaging market is witnessing a strong shift toward sustainable and recyclable packaging solutions. Consumers are increasingly aware of environmental issues and are demanding packaging that minimizes waste and supports recycling. This trend is encouraging manufacturers to adopt materials such as paper, cardboard, and biodegradable plastics. Companies are also investing in innovative designs that reduce material usage while maintaining functionality. Retailers are supporting this trend by promoting eco-friendly products, which is further driving adoption. As a result, sustainability is becoming a key competitive factor in the market.

Growth of Flexible Packaging Formats

Flexible packaging is gaining popularity in the canada household packaging market due to its convenience, cost-effectiveness, and reduced environmental impact compared to rigid packaging. Formats such as pouches, sachets, and wraps are widely used for household products, including food, cleaning supplies, and personal care items. These packaging solutions offer advantages such as lightweight design, ease of storage, and extended shelf life. Advances in material technology are improving the barrier properties of flexible packaging, making it suitable for a wider range of applications. This trend is expected to continue as consumers seek convenient and sustainable packaging options.

Market Drivers

Increasing Demand for Convenience Packaging

The growing demand for convenience packaging is a major driver of the canada household packaging market. Consumers are looking for packaging solutions that are easy to use, store, and dispose of. Features such as resealable closures, easy-open designs, and portion control are becoming increasingly important. This is particularly relevant for food and personal care products, where convenience plays a significant role in purchasing decisions. Manufacturers are responding by developing innovative packaging formats that enhance user experience and meet consumer expectations.

Expansion of E-commerce and Retail Channels

The expansion of e-commerce and retail channels is significantly driving the canada household packaging market. Online shopping has increased the demand for packaging that can protect products during transportation and handling. Packaging solutions need to be durable, lightweight, and cost-efficient to meet the requirements of e-commerce logistics. Additionally, the growth of organized retail is increasing the demand for attractive and functional packaging that enhances product visibility and brand appeal. This driver is expected to remain strong as digital commerce continues to grow.

Market Restraint

High Cost of Sustainable Packaging Materials

One of the key challenges in the canada household packaging market is the high cost associated with sustainable packaging materials. While there is a strong demand for eco-friendly packaging, materials such as biodegradable plastics and recycled paper can be more expensive than traditional options. This can impact profit margins for manufacturers and increase product prices for consumers. For example, small and medium-sized companies may face difficulties in adopting sustainable packaging due to cost constraints. Additionally, the need for specialized production processes can further increase costs. This restraint highlights the importance of technological advancements and economies of scale to make sustainable packaging more affordable.

Market Opportunities

Innovation in Smart and Functional Packaging

The development of smart and functional packaging presents significant opportunities in the canada household packaging market. Technologies such as QR codes, temperature indicators, and freshness sensors are being integrated into packaging solutions to enhance consumer engagement and product safety. These innovations provide additional value to consumers and help brands differentiate their products in a competitive market. As technology continues to evolve, the adoption of smart packaging is expected to increase, creating new growth opportunities.

Rising Demand for Private Label Products

The increasing popularity of private label products is creating opportunities for packaging manufacturers in Canada. Retailers are expanding their private label offerings to provide cost-effective alternatives to branded products. This trend is driving demand for customized packaging solutions that align with retailer branding strategies. Packaging companies can benefit by offering design, printing, and production services tailored to private label products. This opportunity is expected to grow as consumers continue to seek value-oriented options.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.7 Billion |

| Market Size in 2026 | USD 19.6 Billion |

| Market Size in 2034 | USD 29.8 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flexible packaging dominated the canada household packaging market in 2024, accounting for approximately 36.2% of the total share. This segment includes pouches, sachets, wraps, and films that are widely used in food, personal care, and cleaning products. Flexible packaging offers advantages such as lightweight design, cost efficiency, and ease of storage. It also supports sustainability goals by reducing material usage compared to rigid packaging. The increasing demand for convenience and portability is further driving the growth of this segment.

Rigid plastic containers are expected to be the fastest-growing segment, with a CAGR of 5.8% during the forecast period. These containers are widely used for packaging liquids, detergents, and personal care products due to their durability and strength. Innovations in recyclable plastics and improved design features are enhancing the appeal of rigid packaging.

By Material

Plastic packaging dominated the market in 2024, accounting for 49.7% of the total share. Plastic materials are widely used due to their versatility, durability, and cost-effectiveness. They are commonly used in bottles, containers, and flexible packaging formats.

Paper-based packaging is projected to grow at the fastest CAGR of 5.9%. Increasing environmental awareness and regulatory pressure to reduce plastic usage are driving the adoption of paper-based materials. Advances in coating technologies are improving performance and expanding applications.

By Application

Food and beverage applications dominated the market in 2024, accounting for 42.5% of the total share. Packaging plays a critical role in maintaining product quality and safety in this sector. The increasing demand for packaged and processed food products is driving growth.

Personal care packaging is expected to grow at the fastest CAGR of 5.7% during the forecast period. The rising demand for beauty and hygiene products is driving the need for innovative packaging solutions.

Canada Household Packaging Market Segmentations

By Product Type

- Flexible Packaging

- Rigid Packaging

- Semi-rigid Packaging

By Application

- Food & Beverage

- Personal Care

- Household Cleaning Products

- Others

By Material

- Plastic

- Paper

- Metal

- Glass

Regional Analysis

North America

North America accounted for approximately 34.6% of the canada household packaging market share in 2025 and is projected to grow at a CAGR of 5.4% during the forecast period. The region benefits from advanced packaging technologies, strong consumer demand, and well-developed retail infrastructure. Increasing focus on sustainability and regulatory initiatives to reduce plastic waste are further supporting market growth.

The United States plays a significant role in the regional market due to its large consumer base and strong manufacturing capabilities. A key growth factor is the increasing adoption of innovative packaging solutions that enhance convenience and sustainability.

Europe

Europe held a 21.8% market share in 2025 and is expected to grow at a CAGR of 5.2%. The region is characterized by strict environmental regulations and a strong emphasis on sustainable packaging practices. These factors are driving the adoption of eco-friendly packaging materials.

Germany is a leading country in the European market, supported by its strong industrial base and focus on innovation. A unique growth factor is the widespread adoption of circular economy practices.

Asia Pacific

Asia Pacific accounted for 28.7% of the market share in 2025 and is projected to grow at the fastest CAGR of 6.3%. Rapid urbanization, increasing disposable incomes, and expanding retail sectors are driving demand for household packaging solutions.

China dominates the region due to its large population and growing consumer market. A significant growth factor is the increasing demand for packaged goods in urban areas.

Middle East & Africa

The Middle East & Africa region held 6.1% of the market share in 2025 and is expected to grow at a CAGR of 5.8%. The region is experiencing steady growth due to increasing urbanization and changing consumer lifestyles.

The United Arab Emirates is a key market, driven by its expanding retail and logistics sectors. A unique growth factor is the rising demand for premium packaging solutions.

Latin America

Latin America accounted for 8.8% of the market share in 2025 and is projected to grow at a CAGR of 6.1%. The region is witnessing growth in the packaging industry due to increasing consumer demand and economic development.

Brazil is the dominant country in the region, supported by its large population and growing retail sector. A key growth factor is the increasing adoption of packaged consumer goods.

Competitive Landscape

The canada household packaging market is characterized by the presence of several global and regional players competing on innovation, sustainability, and cost efficiency. Companies are focusing on developing eco-friendly packaging solutions and expanding their product portfolios. Strategic collaborations, mergers, and acquisitions are common strategies used to strengthen market position.

Amcor Plc is a leading player in the market, known for its extensive product portfolio and focus on sustainability. The company has recently introduced recyclable packaging solutions to meet evolving consumer demands. Other major players are also investing in advanced technologies and expanding their production capacities to remain competitive.

Key Players List

- Amcor Plc

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Mondi Group

- Huhtamaki Oyj

- WestRock Company

- Smurfit Kappa Group

- DS Smith Plc

- International Paper Company

- Winpak Ltd.

- Cascades Inc.

- TC Transcontinental Inc.

- ProAmpac LLC

- Coveris Holdings S.A.