Renewable Material Packaging Market Size and Growth

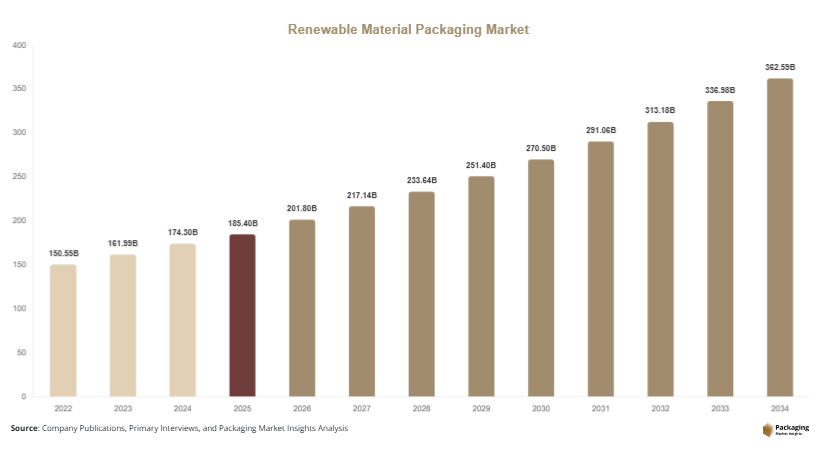

The global renewable material packaging market size was valued at approximately USD 185.4 billion in 2025 and is estimated to reach USD 201.8 billion in 2026. Over the forecast period from 2025 to 2034, the market is projected to grow at a compound annual growth rate (CAGR) of 7.6%, reaching around USD 392.5 billion by 2034.

Renewable material packaging refers to packaging solutions derived from biodegradable, compostable, or bio-based materials such as paper, cardboard, plant-based plastics, and agricultural residues. These materials are increasingly replacing conventional fossil-based plastics across multiple industries, including food and beverage, personal care, healthcare, and e-commerce.

Key Highlights:

- The market size reached USD 185.4 billion in 2025, reflecting the growing adoption of renewable material packaging across multiple industries. Rising awareness of environmental sustainability and regulatory initiatives contributed to this market valuation.

- It is expected to grow at a CAGR of 7.6% from 2025 to 2034, driven by increasing demand for eco-friendly packaging solutions and technological advancements in bio-based materials.

- The market is forecasted to reach USD 392.5 billion by 2034, supported by expanding applications in food & beverage, e-commerce, and personal care industries.

- There is strong demand from food & beverage and e-commerce sectors, as companies seek biodegradable, recyclable, and compostable packaging to reduce environmental impact and align with consumer preferences.

- Increasing regulatory pressure on plastic usage globally is accelerating the shift toward renewable materials, with governments enforcing bans on single-use plastics and encouraging sustainable packaging initiatives.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Biodegradable and Compostable Materials

The market is experiencing a noticeable shift toward biodegradable and compostable packaging materials, particularly in food service and retail sectors. Companies are investing in plant-based polymers such as polylactic acid (PLA) and starch-based blends to replace petroleum-derived plastics. These materials decompose naturally, reducing landfill waste and environmental impact. The growing availability of industrial composting facilities is further supporting this trend. Additionally, brands are promoting compostable packaging as a value proposition to attract environmentally conscious consumers, which is strengthening demand across developed and emerging markets.

Integration of Circular Economy Practices

Circular economy principles are shaping the development of renewable material packaging solutions. Companies are focusing on recyclability, reuse, and material recovery to minimize waste. Packaging designs are being optimized for easy recycling, while closed-loop systems are being implemented in manufacturing processes. Governments and organizations are encouraging extended producer responsibility (EPR), requiring manufacturers to manage the lifecycle of their packaging products. This trend is fostering innovation in material engineering and encouraging collaborations between packaging manufacturers, recyclers, and end-users to create sustainable value chains.

Market Drivers

Stringent Environmental Regulations and Policies

Governments across the globe are enforcing strict regulations to reduce plastic waste and carbon emissions. Policies such as plastic bans, recycling mandates, and carbon taxes are compelling companies to adopt renewable material packaging solutions. For instance, several countries have introduced legislation requiring a minimum percentage of recycled or bio-based content in packaging. These regulatory frameworks are creating a favorable environment for market growth by incentivizing sustainable practices and penalizing non-compliance, thereby accelerating the transition toward renewable packaging materials.

Growing Consumer Preference for Sustainable Products

Consumers are increasingly prioritizing sustainability in their purchasing decisions. Awareness about environmental issues such as ocean pollution and climate change has led to a preference for eco-friendly packaging. Brands that adopt renewable materials are gaining a competitive advantage by aligning with consumer values. This shift is particularly evident in the food and beverage and personal care sectors, where packaging plays a crucial role in brand perception. As a result, companies are investing in sustainable packaging innovations to enhance customer loyalty and meet evolving expectations.

Market Restraint

High Production Costs and Limited Infrastructure

Despite its advantages, renewable material packaging faces challenges related to higher production costs compared to conventional plastics. Bio-based materials often require specialized processing technologies and raw materials, which can increase manufacturing expenses. Additionally, the lack of widespread composting and recycling infrastructure limits the effective disposal and reuse of these materials. In developing regions, inadequate waste management systems hinder the adoption of renewable packaging solutions. For example, compostable packaging may end up in landfills due to the absence of industrial composting facilities, reducing its environmental benefits. These factors can discourage small and medium enterprises from transitioning to renewable materials, thereby restraining market growth.

Market Opportunities

Expansion of Sustainable E-commerce Packaging

The rapid growth of e-commerce is creating significant opportunities for renewable material packaging. Online retailers are seeking sustainable packaging solutions to reduce their environmental footprint and meet consumer expectations. Lightweight, biodegradable, and recyclable packaging materials are gaining traction in shipping and logistics. Companies are also exploring innovative designs such as reusable packaging and minimalistic packaging formats to reduce waste. As e-commerce continues to expand globally, the demand for renewable packaging solutions is expected to increase, offering growth opportunities for market players.

Advancements in Bio-based Material Technologies

Technological advancements in bio-based materials are opening new avenues for market growth. Research and development efforts are focused on improving the performance, durability, and cost efficiency of renewable materials. Innovations such as nanocellulose, algae-based plastics, and advanced biopolymers are enhancing the functionality of sustainable packaging. These materials offer improved barrier properties, strength, and flexibility, making them suitable for a wide range of applications. As technology continues to evolve, renewable material packaging is expected to become more competitive with traditional packaging solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 185.4 Billion |

| Market Size in 2026 | USD 201.8 Billion |

| Market Size in 2034 | USD 392.5 Billion |

| CAGR | 7.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

The paper and paperboard segment dominated the renewable material packaging market in 2024, accounting for approximately 42.6% of the total market share. This dominance is attributed to its widespread availability, recyclability, and cost-effectiveness. Paper-based packaging is extensively used in food service, retail, and e-commerce applications due to its biodegradability and ease of customization. The increasing demand for sustainable alternatives to plastic packaging is further driving the adoption of paper and paperboard materials. Additionally, advancements in coating technologies are enhancing the barrier properties of paper packaging, making it suitable for a wider range of applications.

The bioplastics segment is expected to be the fastest-growing, with a projected CAGR of 9.1% during the forecast period. Bioplastics, including PLA and PHA, are gaining popularity due to their renewable origin and compostability. The growth of this segment is driven by increasing investments in bio-based material technologies and rising demand for sustainable packaging solutions. Bioplastics offer improved functionality and performance, making them suitable for applications in food packaging, healthcare, and consumer goods. As production technologies advance, the cost of bioplastics is expected to decrease, further boosting their adoption.

By Application

The food and beverage segment held the largest market share of approximately 46.3% in 2024. This segment’s dominance is driven by the high demand for sustainable packaging solutions in the food industry. Renewable materials are widely used for packaging fresh produce, ready-to-eat meals, and beverages. The increasing focus on reducing plastic waste and improving food safety is encouraging the adoption of biodegradable and recyclable packaging. Additionally, regulatory requirements and consumer preferences are pushing food companies to transition toward renewable packaging materials.

The healthcare segment is expected to grow at the fastest CAGR of 8.7% during the forecast period. The demand for sustainable packaging in the healthcare industry is increasing due to environmental concerns and regulatory pressures. Renewable materials are being used for packaging medical devices, pharmaceuticals, and personal care products. The growth of this segment is supported by advancements in material technologies that ensure product safety and compliance with regulatory standards. The increasing focus on sustainability in healthcare supply chains is further driving the adoption of renewable packaging solutions.

By End-Use Industry

The retail and e-commerce segment dominated the market in 2024, accounting for approximately 38.9% of the total share. The rapid growth of online shopping has significantly increased the demand for packaging materials. Retailers are adopting renewable packaging solutions to reduce their environmental impact and meet consumer expectations. Paper-based packaging, biodegradable plastics, and reusable packaging formats are widely used in this segment. The increasing focus on sustainable logistics and green supply chains is further driving the adoption of renewable materials in retail and e-commerce.

The personal care and cosmetics segment is expected to be the fastest-growing, with a CAGR of 8.9%. The growth of this segment is driven by the rising demand for eco-friendly packaging in the beauty industry. Consumers are increasingly seeking sustainable products, prompting brands to adopt renewable materials for packaging. Innovations in design and material technology are enabling the development of attractive and functional packaging solutions. The emphasis on brand differentiation and sustainability is encouraging companies to invest in renewable packaging solutions.

Renewable Material Packaging Market Segmentations

By Type

- n-Butyraldehyde

- Iso-Butyraldehyde

- Crotonaldehyde

- Other Derivatives

By Application

- Plasticizers

- Solvents

- Resins & Polymers

- Fragrances & Flavors

- Other Industrial Chemicals

By End-Use Industry

- Automotive & Transportation

- Construction

- Electronics

- Consumer Goods

- Pharmaceuticals & Healthcare

Regional Analysis

North America

North America accounted for approximately 28.5% of the global renewable material packaging market share in 2025 and is expected to grow at a CAGR of around 6.9% during the forecast period. The region benefits from strong regulatory frameworks, high consumer awareness, and significant investments in sustainable technologies. The presence of leading packaging companies and advanced recycling infrastructure further supports market growth.

The United States dominates the regional market, driven by increasing adoption of sustainable packaging in the food and beverage sector. A key growth factor is the rising implementation of corporate sustainability initiatives by major brands. Companies are committing to reducing plastic usage and increasing the share of renewable materials in their packaging portfolios, which is driving demand.

Europe

Europe held a market share of about 26.2% in 2025 and is projected to grow at a CAGR of 7.2%. The region is characterized by stringent environmental regulations and strong government support for sustainable practices. Policies such as the European Green Deal and plastic waste directives are encouraging the adoption of renewable packaging solutions.

Germany leads the European market due to its advanced recycling infrastructure and strong industrial base. A unique growth factor is the widespread adoption of circular economy practices, with companies focusing on closed-loop systems and sustainable material sourcing. This approach is enhancing resource efficiency and reducing environmental impact.

Asia Pacific

Asia Pacific is the fastest-growing region, accounting for 30.8% of the market share in 2025 and expected to grow at a CAGR of 8.5%. Rapid industrialization, urbanization, and increasing environmental awareness are driving market expansion. The region is witnessing significant investments in sustainable packaging technologies.

China dominates the market, supported by government initiatives to reduce plastic waste and promote eco-friendly alternatives. A key growth factor is the expansion of the e-commerce sector, which is increasing demand for sustainable packaging solutions. The growing middle-class population is also contributing to higher consumption of packaged goods.

Middle East & Africa

The Middle East & Africa region held a market share of 7.1% in 2025 and is projected to grow at a CAGR of 6.4%. The market is gradually evolving, with increasing awareness about sustainability and environmental protection. Government initiatives are supporting the adoption of renewable packaging materials.

The United Arab Emirates is a leading country in the region, driven by sustainability initiatives and investments in green technologies. A unique growth factor is the focus on reducing plastic waste in tourism and hospitality sectors. This is encouraging the use of biodegradable and recyclable packaging solutions.

Latin America

Latin America accounted for 7.4% of the market share in 2025 and is expected to grow at a CAGR of 6.8%. The region is witnessing growing awareness about environmental issues and increasing adoption of sustainable packaging solutions. Government policies are gradually supporting market development.

Brazil dominates the regional market, supported by its large consumer base and expanding food and beverage industry. A key growth factor is the availability of abundant natural resources for bio-based materials, such as sugarcane and agricultural residues. This is enabling cost-effective production of renewable packaging materials.

Competitive Landscape

The renewable material packaging market is moderately fragmented, with several global and regional players competing based on product innovation, sustainability initiatives, and pricing strategies. Key companies are focusing on expanding their product portfolios and investing in research and development to enhance material performance.

One of the leading players in the market is Amcor plc, known for its strong focus on sustainable packaging solutions and global presence. The company has been actively investing in recyclable and bio-based materials to meet evolving market demands. Other major companies are also adopting strategies such as mergers, acquisitions, and partnerships to strengthen their market position.

A recent development includes increased collaboration between packaging manufacturers and raw material suppliers to develop advanced bio-based materials. These partnerships are aimed at improving product performance and reducing costs, thereby enhancing market competitiveness.

Key Players List

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- DS Smith plc

- Tetra Pak International S.A.

- WestRock Company

- Stora Enso Oyj

- UPM-Kymmene Corporation

- Huhtamaki Oyj

- Berry Global Inc.

- International Paper Company

- Sealed Air Corporation

- Sonoco Products Company

- Coveris Holdings S.A.

- Novamont S.p.A.