Brick Liquid Cartons Market Size and Growth

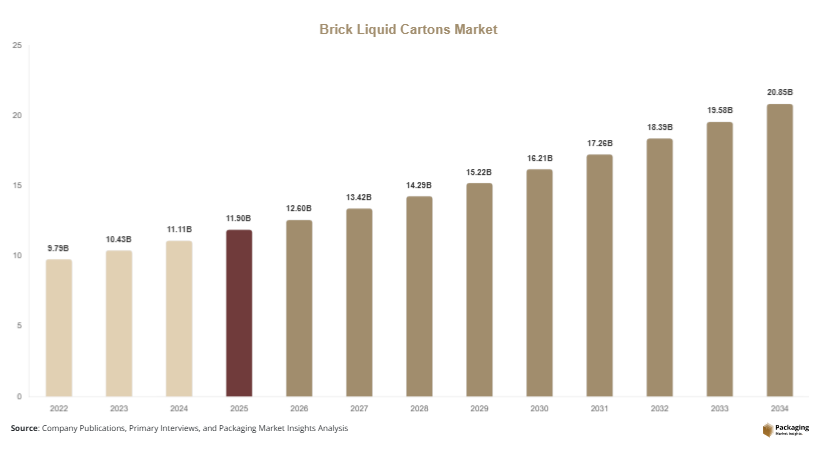

The global brick liquid cartons market size was valued at USD 11.9 billion in 2025 and is projected to reach USD 12.6 billion in 2026. By 2034, the market is forecast to attain approximately USD 20.8 billion, registering a CAGR of 6.5% during the forecast period (2025–2034). Market growth is being driven by rising demand for long shelf-life packaging, expanding dairy and beverage production, and increasing adoption of recyclable paper-based packaging materials.

The brick liquid cartons market is experiencing steady expansion as food and beverage manufacturers increasingly adopt lightweight, shelf-stable, and sustainable packaging formats for dairy products, juices, plant-based beverages, liquid foods, and ready-to-drink products. Brick liquid cartons are widely recognized for their efficient rectangular design, which optimizes storage, transportation, and retail shelf utilization. The growing emphasis on environmentally responsible packaging solutions and the rising consumption of packaged beverages are supporting market development across both developed and emerging economies.

Key Market Highlights

- Asia Pacific dominated the market with a 40.3% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.2%.

- Aseptic brick cartons led the type segment with a 58.6% share.

- Paperboard-based cartons dominated the material segment with a 69.4% share.

- Dairy beverage applications led the end-use segment with 42.8% share.

- The US remained the dominant country with a market size of USD 2.2 billion in 2025 and USD 2.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Renewable and Recyclable Carton Materials

A significant trend in the brick liquid cartons market is the increasing use of renewable and recyclable packaging materials. Beverage producers are actively seeking alternatives to traditional plastic packaging to align with sustainability objectives and changing consumer preferences. Carton manufacturers are responding by increasing the use of responsibly sourced paperboard and renewable polymer components. For example, several beverage brands have introduced cartons incorporating plant-based caps and bio-derived barrier layers. These innovations help reduce carbon footprints while maintaining product protection and shelf life. Looking ahead, continued advancements in fiber-based packaging technologies are expected to increase recyclability rates and further strengthen the role of brick liquid cartons in sustainable packaging strategies.

Expansion of Aseptic Packaging for Shelf-Stable Beverages

The growing popularity of aseptic packaging technologies is shaping the future of the brick liquid cartons market. Aseptic cartons allow products to remain shelf-stable without refrigeration, reducing distribution costs and expanding market reach. This trend is particularly evident in dairy alternatives, nutritional beverages, flavored milk, and fruit juices. For example, many beverage companies now use aseptic brick cartons for plant-based drinks sold through supermarkets and convenience stores. The ability to maintain product freshness while reducing cold-chain requirements offers substantial economic benefits. Future investments in advanced aseptic processing and filling equipment are expected to accelerate adoption across emerging and developed markets alike.

Market Drivers

Rising Demand for Packaged Dairy and Beverage Products

The increasing consumption of packaged dairy products and beverages is a primary growth driver for the brick liquid cartons market. Urbanization, changing dietary habits, and busy lifestyles are encouraging consumers to purchase ready-to-drink products that offer convenience and extended shelf life. Milk, flavored dairy drinks, fruit juices, and nutritional beverages increasingly rely on brick carton packaging because of its portability and product protection capabilities. For instance, dairy processors continue expanding packaged milk distribution into rural and urban markets using aseptic cartons. As beverage consumption continues growing globally, manufacturers are expected to increase investment in carton-based packaging solutions.

Regulatory Pressure to Reduce Plastic Packaging Waste

Government regulations targeting single-use plastics are encouraging businesses to adopt more sustainable packaging alternatives. Brick liquid cartons offer a paper-based solution that aligns with environmental policies focused on waste reduction and recycling. Many food and beverage producers are transitioning from plastic bottles to carton packaging to improve sustainability performance. For example, several beverage brands have introduced carton-packaged product lines to meet corporate environmental commitments. This shift directly increases demand for brick liquid cartons and is expected to remain a significant market growth driver throughout the forecast period.

Market Restraint

Complex Recycling Infrastructure for Multi-Layer Cartons

One of the primary restraints affecting the brick liquid cartons market is the complexity associated with recycling multi-layer packaging structures. Most brick liquid cartons consist of paperboard combined with polyethylene and aluminum layers to provide moisture and oxygen protection. While these materials enhance product preservation, they require specialized recycling processes that are not universally available.

The lack of adequate recycling infrastructure in some regions can limit consumer acceptance and increase waste management challenges. For example, developing economies often face difficulties separating and processing composite packaging materials. This situation can reduce recycling rates and create concerns among sustainability-focused consumers. Additionally, investments in collection systems and recycling facilities are required to improve circularity. Although technological advancements are addressing these issues, recycling complexity remains a challenge that may restrain market growth in certain regions.

Market Opportunities

Expansion of Plant-Based Beverage Packaging

The rapid growth of plant-based beverages presents a significant opportunity for the brick liquid cartons market. Products such as oat milk, almond milk, soy milk, and coconut beverages require packaging formats that provide extended shelf life and strong branding potential. Brick cartons are increasingly preferred due to their lightweight design and compatibility with aseptic processing. As consumer interest in plant-based nutrition continues expanding, beverage manufacturers are expected to increase demand for specialized carton packaging solutions. Future product launches in functional and alternative dairy categories will further strengthen market opportunities.

Development of Fully Renewable Carton Structures

The development of fully renewable and fossil-fuel-free carton packaging offers substantial future growth potential. Manufacturers are investing in bio-based polymers, renewable barrier materials, and sustainably sourced paperboard to create environmentally responsible packaging solutions. These innovations support corporate sustainability targets while addressing consumer concerns regarding packaging waste. Future applications may include entirely plant-based cartons for premium beverages and organic products. As technology advances and production costs decline, renewable carton structures are expected to become increasingly attractive across global food and beverage markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.9 Billion |

| Market Size in 2026 | USD 12.6 Billion |

| Market Size in 2034 | USD 20.8 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Aseptic Brick Cartons dominated the market in 2024 with approximately 58.6% share. These cartons are widely used because they enable products to remain shelf-stable for extended periods without refrigeration. Dairy beverages, juices, plant-based drinks, and nutritional products extensively utilize aseptic packaging to reduce distribution costs and improve product accessibility. The segment benefits from growing demand for convenient beverage formats and expanding retail distribution networks. Manufacturers continue investing in advanced aseptic filling technologies to enhance production efficiency and product quality. The ability to preserve flavor, nutrients, and freshness makes aseptic brick cartons the preferred choice across multiple beverage categories.

Fresh Liquid Cartons are expected to be the fastest-growing segment, registering a CAGR of 6.9% during the forecast period. Growth is driven by increasing consumption of refrigerated dairy products and premium beverages. Advances in carton design and barrier technologies are improving product protection and extending freshness. Future demand is expected to remain strong as consumers increasingly seek convenient and sustainable packaging solutions.

By Material

Paperboard-Based Cartons accounted for approximately 69.4% of market share in 2024, making them the dominant material segment. Paperboard provides structural strength, lightweight performance, and sustainability advantages. Most beverage manufacturers prefer paperboard due to its renewable sourcing potential and compatibility with recycling systems. The material also offers excellent printability for branding and product communication. Continued investments in responsibly sourced fiber materials are supporting segment growth. As sustainability becomes increasingly important, paperboard-based carton packaging is expected to maintain a leading market position.

Bio-Based Barrier Materials are projected to be the fastest-growing material segment with a CAGR of 7.5% through 2034. These materials reduce reliance on fossil-based polymers while maintaining barrier performance. Packaging suppliers are actively developing renewable barrier technologies to improve recyclability and environmental performance. Continued innovation is expected to drive adoption across beverage applications.

By End-Use

Dairy Beverages dominated the market with approximately 42.8% share in 2024. Milk, flavored milk, yogurt drinks, and nutritional dairy products continue to represent major applications for brick liquid cartons. The packaging format provides extended shelf life, product safety, and efficient transportation. Dairy producers increasingly utilize aseptic cartons to expand product distribution into regions with limited refrigeration infrastructure. Growing global dairy consumption supports sustained demand for carton packaging solutions.

Plant-Based Beverages are anticipated to be the fastest-growing end-use segment, expanding at a CAGR of 8.1% through 2034. Consumer demand for dairy alternatives is increasing across both developed and emerging markets. Oat milk, almond milk, soy beverages, and functional plant-based drinks frequently utilize brick carton packaging because of its sustainability profile and shelf-life benefits. Continued innovation in alternative beverage products is expected to drive substantial segment growth.

Brick Liquid Cartons Market Segmentations

By Type

- Aseptic Brick Cartons

- Fresh Liquid Brick Cartons

- Slim Brick Cartons

- Family-Size Brick Cartons

- Portion-Pack Brick Cartons

By Material

- Paperboard

- Polyethylene

- Aluminum Foil

- Bio-Based Polymers

By End-User

- Dairy Products

- Juice & Beverages

- Plant-Based Drinks

- Liquid Food Products

- Others

Regional Analysis

North America

North America accounted for approximately 27.2% of the global brick liquid cartons market share in 2025 and is expected to register a CAGR of 6.1% through 2034. The region benefits from strong demand for packaged dairy products, premium juices, and functional beverages. Consumers increasingly prefer sustainable packaging formats, encouraging beverage manufacturers to adopt carton-based alternatives. The growing popularity of plant-based drinks and nutritional beverages further supports market expansion. Investments in advanced aseptic packaging facilities and recycling initiatives are also contributing to regional growth.

The United States dominates the North American market. A unique growth driver is the rapid expansion of plant-based beverage consumption. Major beverage producers are introducing new oat milk, almond milk, and protein drink products packaged in brick cartons. Retailers are allocating additional shelf space to carton-packaged beverages as sustainability concerns influence purchasing decisions. This trend is expected to strengthen demand for brick liquid cartons throughout the forecast period.

Europe

Europe represented approximately 25.8% of global market share in 2025 and is projected to grow at a CAGR of 6.0% through 2034. Strong environmental regulations and consumer preference for recyclable packaging are supporting widespread adoption of carton-based beverage packaging. Dairy, juice, and nutritional drink manufacturers continue replacing plastic packaging with renewable paperboard solutions. Investments in recycling infrastructure and circular economy initiatives further strengthen market prospects. Demand for premium packaged beverages also supports carton packaging growth across the region.

Germany remains the dominant country within Europe. A unique growth driver is the country's extensive recycling ecosystem and strong consumer awareness regarding sustainable packaging. Beverage manufacturers increasingly highlight renewable packaging attributes on product labels to attract environmentally conscious consumers. Continued innovation in recyclable carton materials is expected to support long-term market expansion in Germany.

Asia Pacific

Asia Pacific dominated the market with a 40.3% share in 2025 and is forecast to expand at a CAGR of 6.9% through 2034. Rising urbanization, population growth, and increasing consumption of packaged beverages are driving regional demand. Expanding dairy industries in China, India, and Southeast Asia are creating substantial opportunities for carton packaging suppliers. The growing availability of modern retail channels and cold-chain alternatives further supports market growth. Beverage companies continue investing in aseptic packaging technologies to improve product distribution efficiency.

China leads the Asia Pacific market. A unique growth driver is the rapid expansion of shelf-stable dairy beverage consumption. Consumers increasingly purchase packaged milk, yogurt drinks, and nutritional beverages packaged in aseptic cartons. Investments in domestic dairy production and beverage processing capacity are expected to maintain strong demand for brick liquid cartons in the country.

Middle East & Africa

The Middle East & Africa accounted for approximately 3.9% of global market share in 2025 and is expected to grow at a CAGR of 6.7% during the forecast period. Population growth, rising disposable incomes, and expanding food distribution networks are contributing to increased beverage consumption. Carton packaging provides an effective solution for distributing shelf-stable products in regions with limited refrigeration infrastructure. Demand for packaged milk and juice products remains particularly strong in several countries. Investments in food processing facilities further support market development.

The Saudi Arabia market leads the region. A unique growth driver is the growing demand for long shelf-life dairy products suitable for distribution across vast geographic areas. Beverage producers increasingly utilize aseptic brick cartons to improve product availability while reducing cold-chain dependence. This trend is expected to support continued market expansion.

Latin America

Latin America held approximately 2.8% of global market share in 2025 and is projected to register the fastest CAGR of 7.2% through 2034. Increasing beverage consumption, expanding retail networks, and growing demand for affordable packaging solutions are driving regional growth. Dairy producers and juice manufacturers continue investing in carton packaging to improve transportation efficiency and shelf stability. Rising awareness of sustainable packaging also contributes to market expansion.

Brazil dominates the Latin American market. A unique growth driver is the country's strong fruit juice production industry. Beverage manufacturers increasingly utilize brick cartons to package juice products for domestic and export markets. Ongoing investments in beverage processing and packaging infrastructure are expected to create additional growth opportunities.

Competitive Landscape

The brick liquid cartons market is characterized by strong competition among global carton packaging manufacturers and aseptic packaging technology providers. Tetra Pak International S.A. remains the market leader due to its extensive product portfolio, global manufacturing network, and leadership in aseptic packaging technologies.

Other key market participants include SIG Group AG, Elopak ASA, Greatview Aseptic Packaging Co., Ltd., and Nippon Paper Industries Co., Ltd. These companies focus on sustainable packaging innovations, renewable material development, and expansion of aseptic filling capabilities.

Recent strategies include investments in bio-based polymers, recyclable barrier layers, and digital printing technologies. Market participants are also collaborating with beverage manufacturers to develop customized packaging solutions tailored to specific product categories. As sustainability and convenience continue influencing consumer preferences, competition is expected to intensify across the global carton packaging industry.

Key Players List

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Greatview Aseptic Packaging Co., Ltd.

- Nippon Paper Industries Co., Ltd.

- Stora Enso Oyj

- Mondi plc

- WestRock Company

- Evergreen Packaging LLC

- Uflex Limited

- Billerud AB

- Smurfit Westrock

- Liquibox Corporation

- Refresco Packaging Solutions

- Pactiv Evergreen Inc.