Boxboard Packaging Market Size and Growth

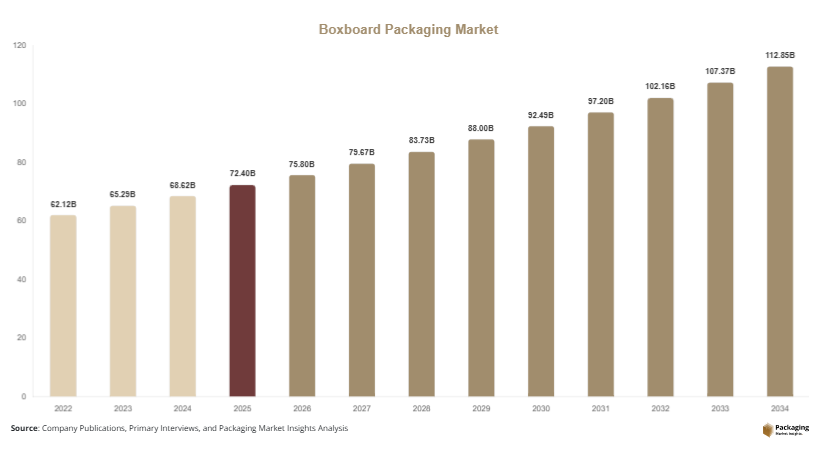

The global market size is estimated at USD 72.4 billion inh 2025, supported by strong demand from food & beverage, retail, and healthcare industries. By 2026, the market is projected to reach approximately USD 75.8 billion, driven by steady recovery in consumer goods manufacturing and rising demand for sustainable packaging materials. By 2034, the market is expected to reach nearly USD 112.6 billion, expanding at a CAGR of 5.1% (2025–2034).

Key growth factors include rising sustainability regulations restricting plastic packaging usage, increasing demand for premium packaging in e-commerce and retail sectors, and expansion of processed food consumption globally. Additionally, growing pharmaceutical production is boosting demand for high-barrier boxboard packaging formats. Increasing investments in recyclable packaging infrastructure are also accelerating market penetration across both developed and emerging economies.

Key Highlights

- Asia Pacific dominated the market with a 37.4% share in 2025

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share.

- Plastic packaging dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained a key North American market with a market size of approximately USD 18.6 billion in 2025 and USD 19.4 billion in 2026

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable Fiber-Based Packaging

The boxboard packaging industry is witnessing a strong shift toward sustainable fiber-based materials as companies reduce reliance on plastic packaging. Brands in food, cosmetics, and pharmaceuticals are increasingly adopting recyclable boxboard cartons to meet regulatory and consumer sustainability expectations. For example, food delivery brands are replacing plastic containers with coated boxboard packaging to reduce environmental impact. This trend is further reinforced by government bans on single-use plastics in several regions. In the future, advancements in biodegradable coatings and water-resistant fiber technologies are expected to further expand application areas of boxboard packaging.

Growth of Digital Printing and Premium Packaging Design

Another major trend is the increasing use of digital printing technologies in boxboard packaging production. Brands are focusing on high-quality visual packaging to enhance shelf appeal and consumer engagement. Digital printing enables customization, short-run production, and rapid design changes, making it ideal for seasonal and promotional packaging. For instance, cosmetic companies are increasingly using embossed and digitally printed folding cartons to differentiate products in competitive retail shelves. In the coming years, integration of AI-driven design tools and smart packaging features is expected to further enhance branding capabilities.

Market Drivers

Expansion of Food and Beverage Packaging Demand

The food and beverage industry is a major driver of the boxboard packaging market due to rising consumption of packaged and processed foods. Boxboard is widely used for cereal boxes, frozen food cartons, bakery packaging, and takeaway containers. Its ability to provide hygiene, printability, and structural strength makes it ideal for food contact applications. For example, global QSR chains are increasingly shifting to paperboard-based packaging for sustainability compliance. As urbanization and disposable incomes rise, packaged food consumption continues to grow, directly supporting boxboard demand.

Rising Pharmaceutical and Healthcare Packaging Requirements

The pharmaceutical sector is another key driver, as boxboard is extensively used in medicine cartons, blister packaging outer boxes, and medical device packaging. Its ability to provide protection, labeling clarity, and regulatory compliance makes it essential for healthcare logistics. Increasing global pharmaceutical production, particularly in India, the United States, and Europe, is significantly boosting demand. For instance, vaccine distribution programs and temperature-sensitive drug packaging require high-quality printed boxboard cartons for traceability and branding.

Market Restraint

Volatility in Raw Material Supply and Recycling Limitations

A major restraint in the boxboard packaging market is the volatility in pulp and recycled fiber supply chains. Fluctuations in raw material availability directly affect production costs and pricing stability. Additionally, contamination in recycled fiber streams reduces quality consistency, limiting usage in high-end applications. In developing regions, inadequate recycling infrastructure further restricts availability of high-grade recycled board. This creates supply chain inefficiencies and increases dependency on virgin fiber, impacting sustainability goals of packaging manufacturers.

Market Opportunities

Expansion of E-commerce Packaging Applications

E-commerce growth presents significant opportunities for boxboard packaging, particularly in secondary and protective packaging formats. Online retail requires lightweight, printable, and durable packaging solutions that enhance customer experience. Boxboard cartons are increasingly used for shipping cosmetics, electronics accessories, and apparel. For example, global fashion retailers use branded folding cartons to improve unboxing experience. Future opportunities include smart packaging integration such as QR codes and augmented reality-enabled cartons.

Growth in Emerging Market Retail and FMCG Sector

Emerging economies present strong opportunities due to rapid expansion of retail and FMCG industries. Countries in Asia, Africa, and Latin America are witnessing increased demand for packaged goods, driving adoption of boxboard packaging. Local manufacturers are investing in cost-efficient packaging solutions for consumer products such as snacks, personal care items, and household goods. Future growth will be supported by increasing urbanization and expansion of modern retail infrastructure.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 72.4 Billion |

| Market Size in 2026 | USD 75.8 Billion |

| Market Size in 2034 | USD 112.6 Billion |

| CAGR | 5.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Solid Bleached Sulfate (SBS) dominates with a 41.2% share in 2024 due to its high brightness, printability, and strength. It is widely used in cosmetics, pharmaceuticals, and premium food packaging. For example, cosmetic brands use SBS folding cartons for luxury product packaging due to superior visual appeal.

Coated Recycled Board (CRB) is the fastest-growing segment with a CAGR of 5.6%. Growth is driven by sustainability initiatives and cost advantages. It is widely used in FMCG packaging and retail cartons. Future demand will increase due to rising recycled fiber availability and environmental regulations.

By Material

Virgin fiber boxboard dominates with a 53.4% share in 2024 due to superior strength and hygiene properties. It is preferred in pharmaceutical and food packaging applications.

Recycled fiber board is the fastest-growing material segment with a CAGR of 6.1%, driven by sustainability goals and circular economy initiatives. Increasing investments in recycling infrastructure support its expansion.

By End-Use

Food & beverage leads with a 43.1% share in 2024 due to high demand for packaged foods. Boxboard is widely used for cereals, frozen foods, and bakery packaging.

Healthcare is the fastest-growing end-use segment with a CAGR of 6.3%, driven by pharmaceutical packaging demand and regulatory compliance requirements.

Boxboard Packaging Market Segmentations

By Type

- Solid Bleached Sulfate (SBS)

- Coated Recycled Board (CRB)

- Folding Boxboard (FBB)

By Material

- Virgin Fiber

- Recycled Fiber

By End-Use

- Food & Beverage

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- Retail & E-commerce

- Industrial Packaging

Regional Analysis

North America

North America holds a significant share of the boxboard packaging market at approximately 28.3% in 2025, with a CAGR of 4.8%. The region is driven by strong demand from food processing, pharmaceuticals, and e-commerce industries. Sustainability regulations and corporate ESG initiatives are increasing adoption of recyclable packaging materials. A key growth factor is the shift toward plastic replacement in retail packaging systems.

The United States dominates the region due to its large FMCG and pharmaceutical industries. A major driver is the expansion of e-commerce packaging demand, where companies use branded boxboard cartons for shipping and retail presentation. For example, subscription box services in the U.S. heavily rely on customized folding cartons for customer engagement.

Europe

Europe accounts for 26.7% of the market in 2025, growing at a CAGR of 5.2%. Strict environmental regulations and circular economy policies are major growth drivers. Germany, France, and the UK are leading adopters of sustainable packaging solutions. A key factor is the EU’s push toward reducing plastic packaging waste.

Germany dominates due to its strong packaging machinery and printing industry. A unique driver is high demand for premium cosmetic packaging using coated boxboard cartons. Luxury brands in France also extensively use embossed and recyclable folding cartons for product differentiation.

Asia Pacific

Asia Pacific leads the global market with a 37.4% share in 2025 and a CAGR of 5.8%. Rapid industrialization, expanding FMCG sector, and growing e-commerce penetration are key drivers. China, India, and Japan are major contributors. A significant factor is rising domestic consumption of packaged goods.

China dominates due to its large-scale manufacturing and export-oriented industries. A key driver is increasing food delivery and packaged food consumption, where boxboard cartons are widely used for takeaway and retail packaging applications.

Middle East & Africa

The region holds a 4.8% share in 2025, growing at a CAGR of 4.6%. Growth is supported by retail expansion and food import dependency. UAE and Saudi Arabia lead the market. A key driver is expansion of modern retail infrastructure and hospitality sector packaging demand.

Latin America

Latin America accounts for 2.8% share in 2025, growing at the fastest CAGR of 6.2%. Brazil and Mexico dominate the region. A key growth driver is expansion of FMCG and packaged food industries. Increasing supermarket penetration is boosting demand for cost-effective boxboard packaging solutions.

Competitive Landscape

The boxboard packaging market is moderately consolidated with major players focusing on sustainability, innovation, and capacity expansion. Key companies include International Paper, WestRock, Smurfit Kappa, Mondi Group, Stora Enso, Georgia-Pacific, Nippon Paper, Nine Dragons Paper, Graphic Packaging International, and Packaging Corporation of America.

International Paper leads the market due to its extensive fiber-based packaging portfolio and global supply chain presence. Companies are investing in recycled fiber capacity expansion, lightweight packaging development, and digital printing technologies to enhance competitiveness.

Key Players

- International Paper

- WestRock Company

- Smurfit Kappa Group

- Mondi Group

- Stora Enso

- Georgia-Pacific

- Graphic Packaging International

- Packaging Corporation of America

- Nippon Paper Industries

- Nine Dragons Paper

- Oji Holdings

- Sappi Limited

- Mayr-Melnhof Karton

- ITC Limited

- Rengo Co. Ltd