Bottled Water Packaging Market Report Size and Growth

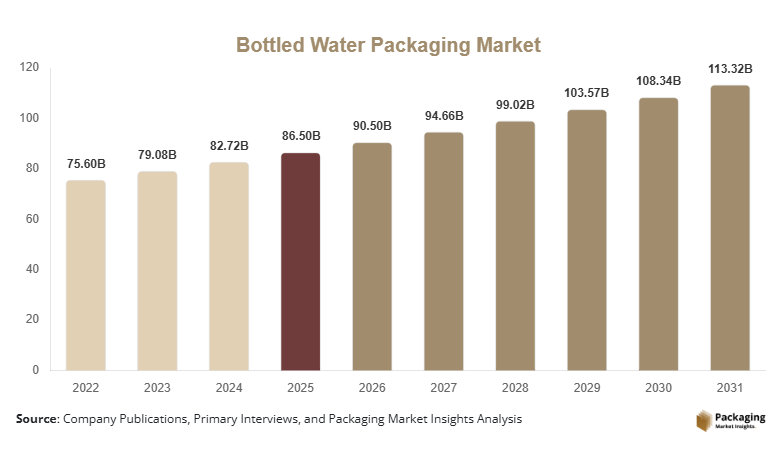

The Bottled Water Packaging Market was valued at USD 86.5 billion in 2025 and is projected to reach USD 112.4 billion by 2030, registering a compound annual growth rate (CAGR) of 4.6% during 2025–2031. Growth in the bottled water packaging market size is primarily supported by the increasing consumption of packaged drinking water across urban and semi-urban regions worldwide. Changing lifestyles, rising health awareness, and concerns over tap water safety have accelerated demand for bottled water products, which directly supports the need for reliable, lightweight, and cost-efficient packaging solutions.

Manufacturers are increasingly focusing on packaging formats that offer product safety, transportation efficiency, and shelf appeal. Plastic bottles, particularly polyethylene terephthalate (PET), continue to dominate due to their cost efficiency, durability, and recyclability potential. At the same time, sustainability concerns are encouraging companies to invest in recycled plastics and alternative materials to reduce environmental impact.

Technological developments in packaging manufacturing, including lightweight bottle design, advanced barrier properties, and high-speed filling lines, have also contributed to the expansion of the bottled water packaging market share. In addition, the expansion of retail distribution channels, including convenience stores, supermarkets, and e-commerce platforms, has strengthened the market outlook.

Emerging economies across Asia Pacific, Latin America, and the Middle East are witnessing rising bottled water consumption due to urban population growth and limited access to safe drinking water infrastructure. This shift is expected to support long-term bottled water packaging market growth across both premium and mass-market bottled water segments.

Key Highlights

- North America accounted for the dominant regional share of 32.4% in 2025, while Asia Pacific is expected to register the fastest growth with a CAGR of 6.2%.

- By material, PET plastic bottles led the market with 61% share, while recycled PET (rPET) is expected to grow fastest at 7.4% CAGR.

- By packaging type, single-serve bottles dominated with 48% share, while large bulk containers are projected to grow at 5.9% CAGR.

- The United States remained the dominant country with USD 21.6 billion in 2025, increasing to USD 22.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable Packaging Materials

Environmental awareness and regulatory pressure are encouraging beverage companies to transition toward sustainable packaging solutions. Brands are increasingly adopting recycled plastics, biodegradable materials, and lightweight bottle designs to reduce plastic waste and carbon emissions. Packaging manufacturers are focusing on higher percentages of recycled PET (rPET) in bottled water containers. In several markets, beverage companies are committing to using 50–100% recycled plastic in bottles over the coming decade. This trend is expected to influence bottled water packaging market growth as producers invest in recycling infrastructure and advanced processing technologies.

Growth of Premium and Functional Water Packaging

Premium bottled water categories such as mineral water, alkaline water, and vitamin-enhanced water are driving demand for differentiated packaging designs. These products often use aesthetically appealing bottles, unique shapes, and premium materials such as glass or high-clarity plastics to create brand distinction. Packaging is becoming a key marketing tool that communicates product quality and brand identity. Manufacturers are also incorporating ergonomic bottle designs and resealable closures to improve convenience. The rise of premiumization within the bottled water industry is therefore contributing to innovation in packaging formats and materials.

Market Drivers

Increasing Demand for Safe Drinking Water

One of the primary drivers supporting the bottled water packaging market size is the rising global demand for safe and hygienic drinking water. In many urban regions, concerns about water contamination and aging municipal water infrastructure have led consumers to rely more heavily on bottled water products. This trend is particularly visible in developing economies where access to safe drinking water remains limited. As bottled water consumption increases, the need for reliable packaging solutions that ensure product integrity and shelf stability also rises.

Expansion of Organized Retail and Distribution Channels

The rapid expansion of organized retail networks has strengthened bottled water sales globally. Supermarkets, hypermarkets, convenience stores, and online grocery platforms provide extensive shelf space for bottled water products in various packaging formats. These distribution channels require packaging that is durable, stackable, and easy to transport. As beverage companies expand their retail presence, demand for efficient packaging formats such as lightweight bottles, multipack shrink wrapping, and bulk containers continues to increase, supporting overall bottled water packaging market growth.

Market Restraint

Environmental Concerns Related to Plastic Waste

Despite the strong demand for bottled water products, environmental concerns related to plastic waste remain a major challenge for the bottled water packaging market. Single-use plastic bottles contribute significantly to global plastic pollution, particularly in regions with limited recycling infrastructure. Governments and environmental organizations are increasingly advocating for stricter regulations on plastic packaging, including bans on certain single-use plastics and mandates for higher recycled content.

These regulations can increase compliance costs for packaging manufacturers and beverage companies. Transitioning to alternative materials or increasing recycled content requires investments in recycling technology, supply chain adjustments, and redesign of packaging formats. Additionally, consumer preferences are gradually shifting toward environmentally responsible products, which may reduce demand for traditional plastic bottles if sustainable alternatives are not adopted.

As a result, manufacturers must balance cost efficiency with sustainability initiatives to maintain competitiveness. Investments in circular packaging systems, refillable containers, and recyclable materials are expected to play an important role in addressing this restraint while maintaining bottled water packaging market share.

Market Opportunities

Adoption of Recycled and Circular Packaging Systems

The adoption of circular economy principles presents a significant opportunity for the bottled water packaging market. Packaging companies are increasingly investing in recycling technologies that enable the reuse of plastic materials in new bottles. Recycled PET (rPET) is gaining popularity due to its ability to reduce reliance on virgin plastic while maintaining packaging performance. Beverage brands are also launching bottle return and recycling programs to support sustainable packaging initiatives. These developments are expected to create long-term growth opportunities for manufacturers specializing in recycled packaging materials.

Expansion of Bottled Water Consumption in Emerging Markets

Emerging economies across Asia, Africa, and Latin America offer strong growth opportunities for the bottled water packaging industry. Rapid urbanization, population growth, and rising disposable income are increasing demand for packaged drinking water products in these regions. Additionally, improvements in retail infrastructure and transportation networks are making bottled water more accessible to consumers. Packaging manufacturers can benefit from this growth by developing cost-effective and durable packaging formats suitable for high-volume production and long-distance distribution.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 86.5 Billion |

| Market Size in 2026 | USD 90.5 Billion |

| Market Size in 2031 | USD 113.3 Billion |

| CAGR | 4.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Plastic materials dominated the bottled water packaging market. PET bottles accounted for approximately 61% of the market share in 2024, driven by their lightweight structure, transparency, and cost efficiency. PET packaging has been widely adopted by beverage manufacturers due to its durability and ability to maintain product quality during transportation and storage.

The recycled PET (rPET) segment is expected to register the fastest growth and will likely expand at a CAGR of 7.4% during the forecast period. Increasing sustainability commitments by beverage brands and regulatory initiatives encouraging recycled plastic usage will support demand for rPET packaging materials.

By Packaging Type

The single-serve bottle segment dominated the bottled water packaging market with a 48% share in 2024. These bottles are widely used in convenience stores, vending machines, and retail outlets due to their portability and consumer convenience. Single-serve packaging formats have become an important component of beverage consumption patterns, particularly among urban consumers.

The bulk water container segment, including large bottles used for home and office water dispensers, is expected to grow at a CAGR of 5.9%. Increasing demand for large water containers in commercial offices and residential complexes will support the expansion of this segment.

By Capacity

The 500 ml to 1 liter capacity segment accounted for the largest share of approximately 46% in 2024. These bottle sizes are widely distributed through retail channels and are preferred by consumers seeking convenient hydration options.

The 1.5 liter to 2 liter capacity segment is expected to experience faster growth with a CAGR of 5.6%. This growth will likely be driven by family consumption patterns and demand for value-based packaging formats in supermarkets.

By Distribution Channel

The supermarkets and hypermarkets segment dominated the market with a 39% share in 2024. These retail outlets provide wide product variety and large shelf space for bottled water products, making them a major distribution channel for beverage manufacturers.

The online retail segment is expected to grow at a CAGR of 8.1%. Increasing adoption of e-commerce grocery platforms and home delivery services will support the expansion of bottled water sales through digital retail channels.

Bottled Water Packaging Market Segmentations

By Material

- PET

- Recycled PET (rPET)

- HDPE

- Glass

- Aluminum

By Packaging Type

- Single-Serve Bottles

- Bulk Water Containers

- Multipack Bottles

By Capacity

- Up to 500 ml

- 500 ml – 1 Liter

- 1 Liter – 1.5 Liter

- 1.5 Liter – 2 Liter

- Above 2 Liter

By Distribution Channel

- Supermarkets & Hypermarkets

- 4Convenience Stores

- Online Retail

- Institutional Sales

Regional Analysis

North America

North America accounted for 32.4% of the bottled water packaging market share in 2025. The region has a well-established bottled water industry supported by strong consumer demand for packaged beverages and advanced packaging manufacturing infrastructure. The market in this region is expected to grow steadily and will likely register a CAGR of 4.1% during 2025–2033.

The United States represented the dominant country within North America due to its high bottled water consumption and extensive beverage distribution network. Large beverage manufacturers operate advanced bottling facilities across the country, enabling high production volumes. Demand for convenient packaging formats such as single-serve bottles and multipack containers continues to support packaging innovation in the U.S. market.

Europe

Europe held 25.7% of the bottled water packaging market size in 2025. The region has a strong bottled water culture, particularly in countries where mineral water consumption is historically high. The European market is expected to grow moderately and will likely record a CAGR of 3.9% during 2025–2033.

Germany emerged as the dominant country in the region due to its well-developed beverage manufacturing industry and high recycling rates for packaging materials. The country’s deposit return system for beverage containers has encouraged higher recycling efficiency and the use of reusable bottles. This regulatory environment has influenced packaging design and material usage within the European bottled water packaging market.

Asia Pacific

Asia Pacific represented 23.6% of the bottled water packaging market share in 2025. The region is characterized by rapidly growing urban populations and increasing consumption of packaged beverages. Asia Pacific is expected to be the fastest-growing regional market with a CAGR of 6.2% during 2025–2033.

China dominated the regional market due to its large population and expanding bottled water industry. Domestic beverage companies have significantly increased production capacity to meet rising demand from urban consumers. The development of large-scale manufacturing facilities and packaging production plants has supported the expansion of bottled water packaging solutions across the country.

Middle East & Africa

The Middle East & Africa accounted for 10.1% of the global bottled water packaging market in 2025. Limited freshwater resources and high demand for packaged drinking water contribute to the importance of bottled water products in the region. The market is expected to grow and will likely register a CAGR of 5.4% during 2025–2033.

Saudi Arabia emerged as a key country within the region due to its high reliance on bottled water for daily consumption. Beverage companies in the country have expanded production facilities to meet domestic demand, leading to increased consumption of packaging materials such as PET bottles and large water containers.

Latin America

Latin America held 8.2% of the bottled water packaging market share in 2025. Growing urbanization and expanding retail networks have increased the availability of bottled water products in the region. The market is projected to grow steadily and will likely register a CAGR of 4.8% during 2025–2033.

Brazil dominated the regional market due to its large beverage industry and extensive distribution network. Local beverage companies have invested in modern bottling facilities and packaging lines to increase production efficiency. These investments are expected to support continued demand for bottled water packaging solutions in the country.

Competitive Landscape

The bottled water packaging market features a mix of global packaging manufacturers and regional suppliers. Companies focus on material innovation, lightweight packaging designs, and sustainability initiatives to maintain market competitiveness.

Major industry participants include Amcor Plc, Berry Global Inc., ALPLA Group, Plastipak Holdings Inc., and Graham Packaging Company. These companies supply packaging solutions to global beverage brands and invest in advanced manufacturing technologies.

Amcor Plc is considered one of the leading companies in the market due to its extensive global manufacturing network and focus on recyclable packaging solutions. The company has recently introduced lightweight PET bottles designed to reduce plastic usage while maintaining structural performance.

Packaging manufacturers are also investing in recycled material processing capabilities and partnerships with beverage companies to develop sustainable packaging formats. These developments are expected to shape future bottled water packaging market trends and industry competition.

Key Players in the Bottled Water Packaging Market

- Amcor Plc

- Berry Global Inc.

- ALPLA Group

- Plastipak Holdings Inc.

- Graham Packaging Company

- O-I Glass Inc.

- Silgan Holdings Inc.

- Gerresheimer AG

- DS Smith Plc

- Sonoco Products Company

- Tetra Pak International S.A.

- Ball Corporation

- Crown Holdings Inc.

- RPC Group Plc

- CKS Packaging Inc.