Biohazard Bags Market Size and Growth

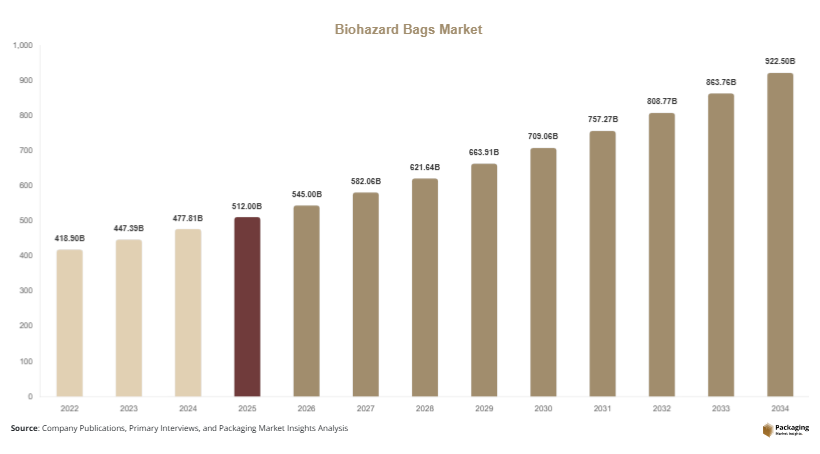

The global biohazard bags market was valued at approximately USD 512 million in 2025 and is projected to reach USD 545 million in 2026. By 2034, the market is forecasted to attain nearly USD 925 million, registering a CAGR of 6.8% during 2025–2034. Biohazard bags are widely used for the collection, handling, transportation, and disposal of infectious medical waste generated by hospitals, diagnostic laboratories, research centers, pharmaceutical manufacturing facilities, and veterinary clinics. The biohazard bags market is experiencing stable expansion due to increasing healthcare waste generation, stricter medical waste disposal regulations, and rising investments in infection prevention infrastructure across hospitals and laboratories.

One of the key growth factors driving the biohazard bags market is the increasing volume of healthcare waste generated globally. Growing hospitalization rates, expansion of diagnostic testing, and rising surgical procedures are significantly increasing the demand for secure biomedical waste disposal products. Another major growth factor is the implementation of stricter government regulations regarding hazardous waste segregation and disposal. Healthcare institutions are increasingly required to use certified color-coded biohazard bags for infectious waste management to comply with environmental and public health standards.

Key Highlights

- North America dominated the market with a 35.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.2%.

- Autoclave biohazard bags led the type segment with a 38.4% share.

- Polyethylene materials dominated with a 58.9% share.

- Hospitals & clinics led the end-use segment with 46.2% share.

- The US remained the dominant country with a market size of USD 148 million in 2025 and USD 156 million in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Biohazard Waste Disposal Solutions

Sustainability is becoming an important trend in the biohazard bags market as healthcare facilities and waste management companies seek environmentally responsible disposal products. Manufacturers are increasingly developing biodegradable and compostable biohazard bags that can reduce landfill waste while maintaining safety compliance for infectious waste handling. Hospitals in Europe and North America are gradually replacing traditional plastic-based biohazard bags with recyclable or low-emission alternatives to align with sustainability initiatives. For example, several healthcare networks are implementing waste reduction programs focused on minimizing single-use plastics in non-critical disposal applications. This trend is expected to encourage further innovation in bio-based polymer materials and low-carbon medical waste management systems during the forecast period.

Growth of Color-Coded and High-Strength Waste Segregation Systems

Healthcare institutions are increasingly adopting advanced color-coded waste segregation systems to improve compliance with biomedical waste management regulations. Biohazard bags with enhanced puncture resistance, high tensile strength, and leak-proof sealing capabilities are gaining popularity across hospitals, diagnostic laboratories, and research facilities. Several countries are introducing updated guidelines requiring separate disposal systems for infectious waste, pharmaceutical waste, and pathological materials. For instance, large healthcare facilities are deploying multilayer red and yellow biohazard bags capable of handling sharp and contaminated waste without tearing during transportation. This trend is expected to improve workplace safety and reduce contamination risks across healthcare environments while supporting demand for premium-quality biohazard disposal products.

Market Drivers

Rising Healthcare Waste Generation Across Hospitals and Laboratories

The increasing generation of biomedical waste is one of the primary drivers supporting the biohazard bags market. Growing patient admissions, diagnostic testing volumes, and surgical procedures are creating substantial demand for secure infectious waste disposal systems. Hospitals generate large quantities of contaminated gloves, syringes, bandages, laboratory samples, and disposable protective equipment that require safe handling and transportation. Biohazard bags play a critical role in reducing contamination risks and maintaining regulatory compliance during waste disposal operations. For example, diagnostic laboratories processing infectious disease samples are using high-strength autoclave-compatible biohazard bags to ensure secure disposal after sterilization procedures. As healthcare infrastructure expands globally, the demand for medical waste containment products is expected to rise steadily.

Stringent Government Regulations for Biomedical Waste Management

Government regulations regarding infectious waste handling and disposal are significantly driving the adoption of biohazard bags across healthcare facilities. Regulatory authorities in countries such as the United States, Germany, Japan, and India have implemented strict guidelines for segregation, storage, transportation, and disposal of hazardous medical waste. Healthcare institutions are increasingly required to use certified color-coded disposal bags with biohazard labeling to prevent contamination and improve worker safety. For instance, hospitals must separate infectious waste from general waste streams using designated disposal systems to comply with healthcare waste management standards. These regulatory requirements are encouraging healthcare providers to invest in high-quality biohazard containment solutions, supporting long-term market growth.

Market Restraint

Environmental Concerns Associated with Plastic-Based Biohazard Bags

One of the key restraints affecting the biohazard bags market is the growing concern regarding plastic waste generated by disposable biomedical waste disposal products. Most conventional biohazard bags are manufactured using polyethylene and other petroleum-based plastics that contribute to landfill accumulation and environmental pollution after disposal. Healthcare facilities generate substantial volumes of single-use disposal bags daily, particularly during infectious disease outbreaks and emergency medical operations. Environmental agencies and sustainability organizations are increasingly pressuring healthcare providers to reduce plastic dependency and improve waste recycling practices. However, transitioning toward biodegradable alternatives remains challenging because sustainable materials often involve higher production costs and may not yet provide the same durability as traditional polymers. For example, smaller healthcare facilities in developing economies may continue relying on low-cost plastic disposal bags due to budget limitations, slowing the adoption of environmentally friendly alternatives.

Market Opportunities

Expansion of Healthcare Infrastructure in Emerging Economies

The expansion of healthcare infrastructure in emerging economies is creating major growth opportunities for the biohazard bags market. Countries across Asia Pacific, Latin America, and Africa are increasing investments in hospitals, diagnostic laboratories, and healthcare waste management systems to improve public health services. Rising healthcare access and growing patient volumes are increasing the demand for infectious waste disposal products across both public and private healthcare facilities. Governments are also strengthening biomedical waste management regulations, encouraging healthcare institutions to adopt standardized disposal systems. Future growth opportunities are expected to emerge from rural healthcare development programs and expanding laboratory testing capacities in rapidly urbanizing regions.

Development of Biodegradable and Advanced Polymer Biohazard Bags

Technological advancements in biodegradable plastics and advanced polymer materials are opening new opportunities for market participants. Manufacturers are increasingly developing compostable biohazard bags capable of maintaining leak resistance and durability while reducing environmental impact. Healthcare providers are seeking sustainable waste disposal products that align with corporate sustainability goals and environmental compliance requirements. Several packaging companies are introducing multilayer biodegradable bags designed specifically for infectious waste segregation applications. Future opportunities are likely to emerge from innovations in antimicrobial polymer coatings, odor-control technologies, and temperature-resistant materials suitable for high-volume hospital waste disposal systems. As sustainability concerns continue to grow globally, demand for advanced eco-friendly biohazard disposal products is expected to increase steadily.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 512 Billion |

| Market Size in 2026 | USD 545 Billion |

| Market Size in 2034 | USD 925 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Autoclave biohazard bags dominated the market in 2024, accounting for approximately 38.4% of the global market share. These bags are widely used across hospitals, laboratories, and pharmaceutical facilities because they are specifically designed to withstand high-temperature sterilization processes before waste disposal. Autoclave-compatible bags help healthcare providers safely decontaminate infectious waste while reducing contamination risks during transportation and handling. The increasing use of sterilization procedures in diagnostic laboratories and research institutions has significantly strengthened demand for these products. In addition, autoclave bags are commonly manufactured using durable polymer blends capable of resisting punctures and leakage under high-pressure sterilization conditions. Their widespread use in infectious disease testing facilities and surgical waste management applications continues to support segment dominance.

Compostable biohazard bags are projected to be the fastest-growing subsegment, expanding at a CAGR of 7.8% during the forecast period. Healthcare providers are increasingly adopting compostable disposal products to reduce plastic waste generation and improve environmental sustainability. Manufacturers are developing bio-based polymer materials capable of delivering leak resistance and durability comparable to traditional plastics while offering improved biodegradability. Several hospitals and healthcare networks in Europe and North America are implementing pilot programs focused on sustainable biomedical waste disposal practices. Future growth is expected to be driven by stricter environmental regulations and increasing investment in green healthcare procurement strategies. As advancements in compostable polymer technologies improve product performance, adoption is likely to accelerate across both developed and emerging markets.

By Material

Polyethylene materials held the dominant market share of 58.9% in 2024 due to their durability, flexibility, and cost efficiency. Polyethylene biohazard bags are widely used because they provide strong puncture resistance and reliable containment for infectious waste. Hospitals and diagnostic laboratories prefer polyethylene-based disposal bags because they can safely handle sharp materials, contaminated protective equipment, and fluid-containing waste without tearing during transportation. These materials are also compatible with autoclave sterilization processes, making them suitable for high-volume medical waste applications. Additionally, manufacturers continue improving multilayer polyethylene films to enhance tensile strength and leakage prevention capabilities. Their affordability and widespread availability continue to support strong demand across healthcare waste management systems globally.

Biodegradable polymers are expected to be the fastest-growing material segment, registering a CAGR of 8.1% during the forecast period. Environmental concerns regarding plastic waste are encouraging healthcare institutions to transition toward sustainable biomedical waste disposal products. Manufacturers are increasingly introducing biodegradable polymer blends derived from renewable resources such as starch-based materials and bio-resins. These products are gaining popularity in healthcare facilities seeking to reduce landfill contributions and improve sustainability compliance. Future growth opportunities are expected to emerge from advancements in antimicrobial biodegradable films capable of improving hygiene performance while maintaining structural integrity. As governments strengthen environmental regulations for healthcare waste management, demand for biodegradable polymer-based biohazard bags is anticipated to increase steadily.

By End-Use

Hospitals & clinics dominated the end-use segment in 2024, accounting for approximately 46.2% of the global market share. Hospitals generate substantial quantities of infectious waste, including surgical materials, contaminated protective equipment, disposable syringes, and pathological waste requiring secure disposal. Biohazard bags are essential for maintaining infection control and preventing contamination during waste collection and transportation processes. Large healthcare institutions increasingly rely on color-coded disposal systems to comply with regulatory guidelines regarding biomedical waste segregation. In addition, the growing number of surgical procedures, emergency care services, and intensive care admissions globally is contributing to sustained demand for high-capacity and puncture-resistant biohazard disposal bags. The expansion of multi-specialty hospitals in emerging economies is expected to further strengthen segment growth.

Pharmaceutical laboratories are anticipated to be the fastest-growing end-use segment, expanding at a CAGR of 7.5% through 2034. Increasing pharmaceutical research activities, vaccine development programs, and biotechnology innovations are generating higher volumes of hazardous laboratory waste. Research facilities require secure disposal systems for contaminated cultures, chemical residues, and biological testing materials. Several pharmaceutical companies are adopting advanced multilayer biohazard bags with leak-proof sealing systems to improve laboratory safety and comply with hazardous waste disposal regulations. Future growth is expected to be supported by increasing investments in clinical trials and biologics manufacturing. The rising expansion of pharmaceutical research hubs in Asia Pacific and North America is also anticipated to create additional demand for specialized biohazard waste management products.

Biohazard Bags Market Segmentations

By Type

- Autoclave Biohazard Bags

- Compostable Biohazard Bags

- Infectious Waste Bags

- Specimen Collection Bags

- Leak-Proof Disposal Bags

By Material

- Polyethylene

- Polypropylene

- Biodegradable Polymers

- High-Density Plastic Films

By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Pharmaceutical Laboratories

- Research Institutes

- Veterinary Clinics

Regional Analysis

North America

North America accounted for approximately 35.6% of the global biohazard bags market share in 2025 and is projected to expand at a CAGR of 6.1% during the forecast period. The region benefits from advanced healthcare infrastructure, high healthcare spending, and strict biomedical waste management regulations. Hospitals, pharmaceutical companies, and research laboratories across the United States and Canada generate substantial volumes of infectious waste, increasing demand for secure disposal systems. Rising surgical procedures and diagnostic testing activities are also contributing to market growth. Additionally, healthcare institutions are increasingly adopting premium leak-proof and puncture-resistant biohazard bags to improve workplace safety and regulatory compliance across healthcare environments.

The United States dominates the regional market due to its extensive healthcare network and strong regulatory oversight regarding infectious waste management. One unique growth driver is the increasing use of disposable medical products in outpatient care and home healthcare services. The growth of diagnostic laboratories processing infectious disease samples has also strengthened demand for high-strength autoclave-compatible biohazard bags. Several healthcare systems in the country are implementing sustainability-focused waste management programs encouraging the adoption of recyclable and biodegradable disposal products. These initiatives are expected to support further innovation in eco-friendly biohazard containment solutions.

Europe

Europe represented approximately 27.4% of the global biohazard bags market share in 2025 and is expected to grow at a CAGR of 5.9% through 2034. The regional market is strongly influenced by strict environmental and healthcare waste disposal regulations established by European authorities. Healthcare institutions are required to implement color-coded segregation systems for infectious and hazardous waste, increasing demand for certified biohazard disposal products. Rising investments in laboratory research and pharmaceutical manufacturing are also contributing to market growth. Additionally, several countries in Europe are encouraging the adoption of sustainable healthcare products, including recyclable and biodegradable biomedical waste disposal bags.

Germany remains the dominant country within the European market due to its advanced healthcare and pharmaceutical industries. A key growth factor is the increasing focus on infection prevention in elderly care facilities and rehabilitation centers. German healthcare providers are investing in advanced multilayer biohazard bags with improved puncture resistance to safely manage contaminated waste generated from long-term care services. Several hospitals are also integrating sustainable biomedical waste disposal practices into procurement strategies. This trend is encouraging local manufacturers to expand production of biodegradable and low-emission medical waste containment products.

Asia Pacific

Asia Pacific held a market share of 25.8% in 2025 and is anticipated to register the fastest regional CAGR of 7.4% during the forecast period. Rapid healthcare infrastructure expansion, increasing population, and rising infectious disease testing activities are driving regional market growth. Countries such as China, India, Japan, and South Korea are witnessing increasing demand for medical waste management products due to higher hospitalization rates and growing healthcare access. Government investments in hospital modernization and diagnostic laboratory development are also contributing to the adoption of standardized biomedical waste disposal systems. In addition, growing awareness regarding healthcare worker safety is supporting demand for durable biohazard disposal products.

China dominates the Asia Pacific market because of its large healthcare system and expanding biotechnology sector. One unique growth driver is the rapid growth of diagnostic laboratory networks in urban and semi-urban regions. Increasing testing volumes for infectious diseases and chronic illnesses are generating substantial quantities of laboratory waste requiring secure disposal solutions. Several Chinese healthcare facilities are adopting high-capacity color-coded biohazard bag systems integrated with automated waste collection processes. The increasing production of disposable medical devices and protective equipment is also expected to strengthen market demand across the country.

Middle East & Africa

The Middle East & Africa accounted for around 5.1% of the global biohazard bags market share in 2025 and is projected to grow at a CAGR of 6.5% during the forecast period. Rising healthcare investments and increasing hospital construction projects are contributing to regional market growth. Countries in the Gulf Cooperation Council are expanding healthcare infrastructure and introducing stricter waste management regulations to improve public health standards. Demand for infectious waste disposal products is also increasing due to higher imports of medical devices and growing laboratory testing capacities. Additionally, healthcare providers are focusing on improving contamination prevention measures in hospitals and diagnostic facilities.

The United Arab Emirates remains the leading market within the region due to its advanced healthcare infrastructure and growing medical tourism sector. A distinctive growth driver is the increasing establishment of specialized healthcare centers and private diagnostic laboratories. Several healthcare providers in the UAE are investing in premium biohazard disposal systems with enhanced leak-proof and odor-control properties to improve infection prevention standards. The expansion of pharmaceutical manufacturing and clinical research activities is also contributing to the rising demand for secure biomedical waste handling products across the country.

Latin America

Latin America represented approximately 6.1% of the global biohazard bags market share in 2025 and is expected to grow at the fastest CAGR of 7.2% through 2034. Increasing healthcare expenditure, expanding diagnostic services, and improving biomedical waste management awareness are supporting regional market growth. Countries such as Brazil, Mexico, and Argentina are investing in healthcare modernization programs that include improved infectious waste disposal systems. Rising demand for disposable medical products and increasing vaccination campaigns are also generating higher volumes of contaminated waste requiring safe containment. In addition, regional governments are introducing stricter waste disposal regulations for hospitals and laboratories.

Brazil dominates the Latin American market due to its large healthcare system and expanding pharmaceutical sector. One unique growth factor is the increasing implementation of centralized biomedical waste treatment facilities across urban healthcare networks. Hospitals and diagnostic laboratories are adopting standardized color-coded waste disposal systems to comply with updated public health regulations. Several private healthcare providers are also investing in biodegradable biohazard bags as part of broader sustainability initiatives. These trends are expected to support long-term market growth across Brazil and neighboring countries.

Competitive Landscape

The biohazard bags market is moderately fragmented, with companies focusing on product durability, sustainability, and regulatory compliance to strengthen market competitiveness. Thermo Fisher Scientific Inc. remains one of the leading players due to its extensive healthcare product portfolio and strong distribution network across hospitals and laboratories. The company recently expanded its range of high-strength autoclave-compatible biohazard disposal bags designed for laboratory sterilization applications.

Other major companies include Stericycle Inc., Daniels Health, McKesson Corporation, and Medline Industries. These companies are investing in biodegradable waste disposal materials, multilayer polymer technologies, and advanced leak-proof sealing systems to improve product performance. Strategic collaborations with healthcare providers and waste management companies are becoming increasingly common across the market. Manufacturers are also expanding regional production facilities to meet rising demand from emerging healthcare economies. Growing emphasis on infection prevention and environmental sustainability is expected to intensify competition among market participants during the forecast period.

Key Players List

- Thermo Fisher Scientific Inc.

- Stericycle Inc.

- Daniels Health

- McKesson Corporation

- Medline Industries

- Cardinal Health Inc.

- VWR International LLC

- BioMedical Waste Solutions LLC

- Inteplast Group

- Justrite Safety Group

- STERIS plc

- Bel-Art Products

- Veolia Environment S.A.

- Clean Harbors Inc.

- Healthmark Industries Co., Inc.