Biofoam Packaging Market Size and Growth

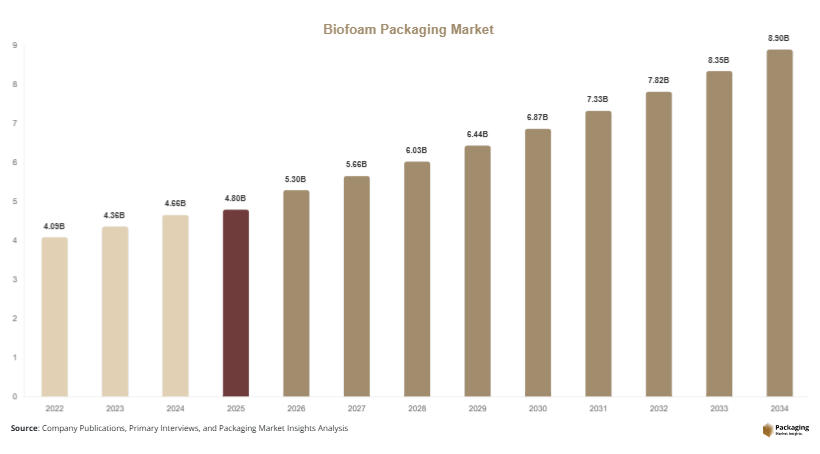

The global market size is estimated at USD 4.8 billion in 2025 and is projected to reach approximately USD 5.3 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to grow at a CAGR of 6.7%, reaching nearly USD 9.2 billion by 2034. The biofoam packaging market is experiencing consistent expansion as industries transition toward sustainable and biodegradable alternatives to petroleum-based packaging materials.

Biofoam packaging, developed using renewable resources such as corn starch, agricultural fibers, and mycelium, is gaining traction due to its eco-friendly properties and compatibility with circular economy goals. Increasing regulatory pressure on single-use plastics across multiple regions has encouraged manufacturers to adopt biodegradable packaging solutions. Governments are implementing bans and restrictions on plastic packaging, particularly in food service and retail sectors, which is accelerating the shift toward biofoam materials.

Key Market Highlights

- Asia Pacific dominated the market with a 36.8% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.1%.

- Starch-based biofoam led the type segment with a 41.2% share, while mushroom-based biofoam is expected to grow at a CAGR of 7.4%.

- Plant-based materials dominated with a 55.6% share, while hybrid bio-composites are forecasted to grow at a CAGR of 7.0%.

- Food & beverage applications led the segment with 44.7% share, while electronics packaging is expected to grow at a CAGR of 6.9%.

- China remained the dominant country with a market size of USD 1.1 billion in 2025 and USD 1.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising adoption of mycelium-based and agricultural waste-derived packaging

The market is witnessing a noticeable shift toward packaging solutions derived from mushroom mycelium and agricultural byproducts. These materials are cultivated using organic waste such as husks and fibers, which are bonded naturally by fungal growth to create protective foam structures. This approach reduces reliance on industrial processing and eliminates toxic byproducts. Packaging manufacturers are increasingly collaborating with agricultural supply chains to source raw materials efficiently, which also supports rural economies. For example, electronics and furniture brands are adopting molded mycelium packaging to replace expanded polystyrene inserts. The future impact of this trend is expected to include greater commercialization of low-energy production techniques, wider product customization capabilities, and improved scalability that will enable cost parity with traditional foam packaging.

Expansion of sustainable packaging integration in e-commerce logistics

The growth of online retail and last-mile delivery systems has accelerated the demand for eco-friendly protective packaging. Biofoam is increasingly being integrated into automated packaging lines due to its adaptability and cushioning properties. Logistics companies are exploring biodegradable void fillers and protective inserts to align with sustainability commitments. Several global retailers are transitioning toward fully compostable packaging solutions to reduce environmental impact and improve brand perception. This trend is further supported by regulatory requirements and consumer expectations regarding waste reduction. Over the forecast period, integration of biofoam into supply chain automation, along with innovations in lightweight packaging design, is expected to enhance operational efficiency while reducing material usage and disposal challenges.

Market Drivers

Regulatory push toward biodegradable and compostable packaging materials

Stringent environmental policies aimed at reducing plastic waste are significantly influencing the adoption of biofoam packaging. Governments across Europe, North America, and parts of Asia are enforcing restrictions on single-use plastics and promoting compostable alternatives. These regulatory frameworks are creating a favorable ecosystem for biofoam manufacturers. For instance, food service operators are increasingly required to adopt biodegradable containers, leading to higher demand for starch-based and plant-derived foam products. This regulatory pressure directly translates into increased investments in sustainable packaging technologies. As policies become more stringent, industries are expected to accelerate their transition, further strengthening market growth.

Shifting consumer behavior toward environmentally responsible consumption

Consumer awareness regarding environmental sustainability is reshaping purchasing patterns across industries. Buyers are increasingly favoring brands that use eco-friendly packaging, encouraging companies to adopt biofoam solutions. This shift is particularly evident in the food delivery and retail sectors, where packaging visibility plays a crucial role in brand perception. Companies are leveraging sustainable packaging as a differentiator in competitive markets. For example, restaurants and takeaway chains are replacing plastic containers with biodegradable foam alternatives to appeal to environmentally conscious customers. This growing preference is expected to drive long-term demand for biofoam packaging, especially among younger consumer demographics.

Market Restraint

High production costs and limited economies of scale

The relatively high cost of producing biofoam packaging compared to conventional plastic foam remains a key challenge for market growth. Bio-based materials often require specialized processing techniques and consistent supply of agricultural inputs, which can increase operational expenses. Additionally, fluctuations in raw material availability, such as corn or biomass residues, can impact production efficiency and pricing. Small and medium enterprises may face difficulties in adopting biofoam solutions due to cost constraints, limiting widespread adoption. For example, packaging manufacturers in developing regions often continue to rely on cheaper plastic alternatives due to budget limitations. Although technological advancements are gradually improving efficiency, cost competitiveness remains a critical barrier that could slow market penetration in the near term.

Market Opportunities

Growth potential in emerging economies with evolving sustainability policies

Emerging markets are presenting significant opportunities for the expansion of biofoam packaging solutions. Rapid urbanization, growing middle-class populations, and increasing environmental awareness are driving demand for sustainable packaging. Governments in countries such as India, Brazil, and Indonesia are introducing regulations to reduce plastic waste and promote biodegradable materials. These policy shifts are encouraging local manufacturers to invest in biofoam production facilities. Additionally, the expansion of organized retail and food delivery platforms in these regions is creating new application areas. Over time, localized manufacturing and improved distribution networks are expected to enhance accessibility and affordability of biofoam packaging.

Advancements in bio-based material engineering and performance enhancement

Continuous innovation in material science is opening new avenues for biofoam packaging applications. Researchers and manufacturers are developing hybrid materials that combine natural fibers with biodegradable polymers to enhance strength, moisture resistance, and thermal insulation. These advancements are expanding the usability of biofoam in sectors such as electronics, healthcare, and industrial packaging. For instance, improved moisture-resistant biofoam can be used for packaging perishable goods, while high-density variants are suitable for protective shipping applications. The future outlook includes increased commercialization of advanced bio-composites, reduced production costs through process optimization, and broader adoption across high-performance packaging segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.8 Billion |

| Market Size in 2026 | USD 5.3 Billion |

| Market Size in 2034 | USD 9.2 Billion |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Starch-based biofoam held the dominant position in the market with a 41.2% share in 2024. This segment benefits from the widespread availability of raw materials such as corn, potato, and tapioca starch, which makes it cost-effective compared to other bio-based alternatives. The material is widely used in food service packaging, protective inserts, and cushioning applications due to its lightweight nature and biodegradability. Its compatibility with conventional molding technologies allows manufacturers to scale production efficiently. For instance, takeaway food containers and disposable trays made from starch-based foam are increasingly replacing polystyrene products. The segment also benefits from strong regulatory support favoring compostable materials, particularly in developed economies.

Mushroom-based biofoam is emerging as the fastest-growing type segment, registering a CAGR of 7.4% over the forecast period. This growth is driven by its ability to utilize agricultural waste and offer fully compostable packaging solutions. The material is gaining popularity in high-value applications such as electronics and furniture packaging due to its superior cushioning and customization capabilities. Companies are increasingly investing in mycelium-based technologies to develop innovative packaging products. Future developments are expected to focus on improving scalability and reducing production time, which will further enhance adoption across industries.

By Material

Plant-based materials dominated the segment with a 55.6% market share in 2024. These materials include renewable resources such as corn, sugarcane, and other biomass, which are widely used in the production of biofoam packaging. The dominance of this segment is attributed to its established supply chain and relatively lower production costs. Plant-based biofoam is extensively used in food packaging, protective packaging, and disposable containers. Manufacturers are leveraging these materials to meet sustainability goals and comply with environmental regulations. The segment is expected to maintain its dominance due to continuous demand from the food service and retail industries.

Hybrid bio-composites are the fastest-growing material segment, with a projected CAGR of 7.0%. These materials combine natural fibers with biodegradable polymers to enhance performance characteristics such as strength, durability, and moisture resistance. The increasing demand for high-performance packaging solutions is driving the adoption of hybrid bio-composites. For example, electronics manufacturers are using these materials for protective packaging to ensure product safety during transit. Future advancements in material engineering are expected to improve cost efficiency and expand application areas, particularly in industrial and healthcare packaging.

By End-Use

The food and beverage segment accounted for the largest share of 44.7% in 2024. The dominance of this segment is driven by the increasing demand for sustainable packaging solutions in takeaway and food delivery services. Biofoam packaging is widely used for containers, trays, and cups due to its thermal insulation and biodegradability. Restaurants and food service providers are adopting biofoam to comply with environmental regulations and meet consumer expectations. The growth of online food delivery platforms is further supporting demand in this segment.

Electronics packaging is the fastest-growing end-use segment, with a CAGR of 6.9%. The growth is driven by the increasing need for protective and sustainable packaging solutions in the electronics industry. Biofoam provides excellent cushioning properties, making it suitable for packaging delicate components. Manufacturers are replacing traditional plastic foam with bio-based alternatives to reduce environmental impact. Future growth is expected to be supported by increasing production of consumer electronics and the adoption of sustainable packaging practices by major technology companies.

Biofoam Packaging Market Segmentations

By Type

- Starch-Based

- Mushroom-Based

- Others

By Material

- Plant-Based

- Hybrid Bio-Composites

- Others

By End-User

- Food & Beverage

- Electronics

- Healthcare

- Others

Regional Analysis

North America

North America accounted for approximately 24.5% of the global biofoam packaging market share in 2025 and is expected to grow at a CAGR of 6.2% through 2034. The region demonstrates strong adoption of sustainable packaging solutions driven by corporate sustainability commitments and regulatory initiatives. The United States and Canada are witnessing increasing demand for biodegradable packaging in food service, retail, and e-commerce sectors. The presence of advanced manufacturing technologies and established supply chains supports efficient production and distribution of biofoam products. Additionally, consumer awareness regarding environmental issues is significantly higher in this region, which contributes to steady demand growth.

The United States remains the dominant contributor within North America due to its large consumer base and strong focus on sustainable innovation. A distinctive growth factor in this region is the integration of sustainability goals into corporate strategies. Major retail and food service companies are actively replacing plastic packaging with compostable alternatives. For example, several quick-service restaurant chains are transitioning toward biodegradable containers and cushioning materials. The expansion of green certification programs and eco-labeling initiatives is also influencing purchasing decisions. These trends are expected to drive consistent growth in biofoam packaging adoption across North America.

Europe

Europe held a market share of 28.3% in 2025 and is projected to expand at a CAGR of 6.5% over the forecast period. The region is characterized by strict environmental regulations and a strong commitment to reducing carbon emissions. Policies under sustainability frameworks are encouraging the use of biodegradable and compostable materials across industries. The presence of advanced recycling infrastructure and high consumer awareness further supports the adoption of biofoam packaging solutions. Additionally, the region's focus on circular economy principles is driving innovation in sustainable materials.

Germany leads the European market, supported by its robust industrial base and proactive environmental policies. A unique driver in this region is the enforcement of packaging waste directives, which require companies to reduce non-recyclable materials. For instance, the food service industry is rapidly adopting biodegradable containers to comply with regulations. Retailers are also investing in eco-friendly packaging to align with sustainability targets. The increasing demand for organic and sustainable products is reinforcing the need for environmentally responsible packaging solutions. These factors collectively contribute to the steady growth of the biofoam packaging market in Europe.

Asia Pacific

Asia Pacific dominated the biofoam packaging market with a 36.8% share in 2025 and is expected to grow at a CAGR of 7.0% during the forecast period. Rapid industrialization, urbanization, and population growth are driving demand for sustainable packaging solutions across the region. The expansion of the e-commerce sector, coupled with rising environmental concerns, is accelerating the adoption of biofoam materials. Governments are increasingly implementing policies to reduce plastic waste, which is further supporting market growth.

China is the leading country in the Asia Pacific region due to its large manufacturing capacity and strong policy support for sustainability. A key growth factor is the implementation of nationwide restrictions on single-use plastics, which is encouraging the adoption of biodegradable alternatives. For example, major cities in China have introduced bans on plastic packaging in food delivery services. This has led to increased investments in biofoam production and innovation. Additionally, the availability of agricultural raw materials supports cost-effective manufacturing. The region is expected to maintain its dominance due to strong demand and continuous policy support.

Middle East & Africa

The Middle East & Africa region accounted for 5.6% of the market share in 2025 and is anticipated to grow at a CAGR of 6.1%. The adoption of sustainable packaging solutions in this region is gradually increasing due to rising environmental awareness and government initiatives. The growth of the hospitality, retail, and food service sectors is contributing to the demand for biodegradable packaging. Additionally, increasing investments in infrastructure and urban development are supporting market expansion.

The United Arab Emirates is the dominant country in this region, driven by its focus on sustainability and innovation. A distinct growth driver is the rapid expansion of the tourism and hospitality industry, which is increasingly adopting eco-friendly packaging solutions. For example, hotels and restaurants are replacing plastic containers with biodegradable alternatives to enhance their environmental image. Government-led sustainability initiatives and awareness campaigns are also encouraging businesses to adopt green practices. These developments are expected to drive steady growth in the biofoam packaging market across the region.

Latin America

Latin America held a market share of 4.8% in 2025 and is projected to grow at the fastest CAGR of 7.1% during the forecast period. The region is experiencing increasing demand for sustainable packaging solutions due to rising environmental concerns and regulatory developments. The expansion of retail and food delivery sectors is also contributing to the growth of biofoam packaging adoption. Additionally, the availability of agricultural resources supports the production of bio-based materials.

Brazil is the leading country in the Latin American market, supported by its strong agricultural base and growing industrial sector. A unique growth factor in this region is the development of local manufacturing capabilities for biofoam production. Companies are investing in production facilities to reduce reliance on imports and lower costs. For example, packaging manufacturers are utilizing agricultural waste to produce biodegradable foam materials. This trend is expected to enhance supply chain efficiency and support market growth. Increasing awareness among consumers and businesses regarding sustainable practices is further driving adoption across the region.

Competitive Landscape

The biofoam packaging market is characterized by moderate competition, with several global and regional players focusing on innovation and sustainability. One leading company has established a strong position through continuous investment in research and development, enabling the introduction of advanced biofoam materials with improved performance characteristics. Companies are adopting strategies such as product innovation, strategic partnerships, and capacity expansion to strengthen their market presence.

Manufacturers are increasingly focusing on developing cost-effective and scalable production processes to enhance competitiveness. Collaborations with agricultural suppliers and research institutions are also becoming common to ensure a steady supply of raw materials and drive innovation. Recent developments include the launch of new biodegradable packaging products and expansion into emerging markets. The adoption of sustainability certifications and eco-labeling is also playing a crucial role in differentiating products in the market.

Key Players List

- Sealed Air Corporation

- BASF SE

- Stora Enso

- UFP Technologies

- Eco-Products Inc.

- Genpak LLC

- Sonoco Products Company

- Arkema Group

- Dow Inc.

- Smurfit Kappa Group

- DS Smith Plc

- Huhtamaki Oyj

- Vegware Ltd

- Green Cell Foam

- Zume Inc.