Biodegradable Packaging Materials Market Size and Growth

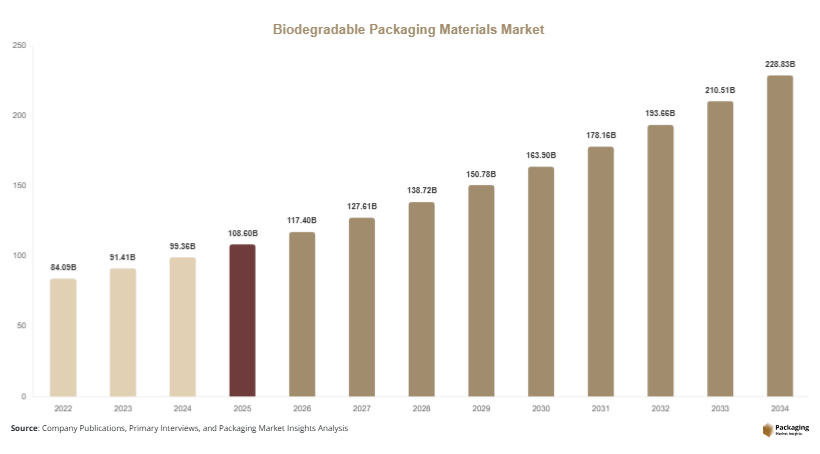

The global biodegradable packaging materials market was valued at approximately USD 108.6 billion in 2025 and is projected to reach USD 117.4 billion in 2026. By 2034, the market is expected to attain nearly USD 228.7 billion, registering a CAGR of 8.7% during 2025–2034. Biodegradable packaging materials are increasingly used in food & beverage, personal care, healthcare, e-commerce, and industrial applications due to their lower environmental impact and compatibility with circular economy initiatives. The biodegradable packaging materials market is witnessing significant expansion due to rising environmental concerns, increasing restrictions on single-use plastics, and growing adoption of sustainable packaging across multiple industries.

One of the primary growth factors driving the biodegradable packaging materials market is the implementation of stringent government regulations targeting plastic waste reduction. Countries across Europe, North America, and Asia Pacific are introducing bans and taxes on conventional plastic packaging, encouraging businesses to shift toward biodegradable alternatives. Another major growth factor is the increasing consumer preference for sustainable products. Consumers are becoming more aware of environmental issues and are favoring brands that use eco-friendly packaging materials. This shift is influencing packaging procurement strategies across food service, retail, and e-commerce industries.

Key Highlights

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 9.2%.

- Starch-based biodegradable packaging led the type segment with a 33.8% share.

- Bioplastics dominated the material segment with a 49.4% share.

- Food & beverage applications led the end-use segment with 44.3% share.

- The US remained the dominant country with a market size of USD 21.6 billion in 2025 and USD 23.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Compostable Flexible Packaging Solutions

The growing demand for environmentally responsible packaging is accelerating the adoption of compostable flexible packaging solutions across food delivery, retail, and consumer goods industries. Flexible biodegradable packaging materials are gaining popularity because they reduce material usage while maintaining product protection and transportation efficiency. Packaging manufacturers are increasingly introducing compostable films and pouches made from starch blends, polylactic acid, and cellulose fibers. For example, snack food and coffee brands are replacing multilayer plastic pouches with biodegradable alternatives that can decompose under industrial composting conditions. This trend is expected to encourage broader investment in compostable packaging technologies, particularly as governments strengthen restrictions on conventional flexible plastics used in consumer packaging applications.

Integration of Agricultural Waste in Biodegradable Packaging Production

Packaging manufacturers are increasingly using agricultural waste materials such as sugarcane bagasse, rice husks, wheat straw, and corn fiber to produce biodegradable packaging products. This trend is reducing dependence on petroleum-based plastics while supporting circular economy initiatives in agricultural industries. Several food service companies are adopting molded fiber trays and containers derived from agricultural residues to improve sustainability performance. For instance, restaurant chains and takeaway food providers are using sugarcane bagasse containers as alternatives to expanded polystyrene packaging. Future growth is expected to be supported by technological advancements improving the moisture resistance and durability of agricultural waste-based packaging materials. These innovations are likely to strengthen commercial adoption across food packaging and industrial protective packaging applications.

Market Drivers

Stringent Government Regulations on Plastic Waste Reduction

Government regulations targeting plastic pollution are one of the key drivers supporting the biodegradable packaging materials market. Countries across Europe, Asia Pacific, and North America are introducing bans, taxes, and recycling mandates for conventional single-use plastics, encouraging industries to adopt biodegradable alternatives. Food service companies, retailers, and packaging manufacturers are increasingly shifting toward compostable and renewable packaging materials to comply with environmental regulations. For example, several countries have prohibited plastic carry bags and foam food containers, creating strong demand for biodegradable packaging products. These regulatory initiatives are expected to continue driving investments in sustainable packaging technologies and manufacturing capacity expansion globally.

Rising Consumer Preference for Sustainable Packaging

Consumers are increasingly prioritizing sustainability when purchasing packaged products, creating strong demand for biodegradable packaging materials. Retail brands and food companies are responding by integrating environmentally friendly packaging into product lines to improve brand image and customer loyalty. Growing awareness regarding marine pollution, landfill waste, and carbon emissions is influencing consumer purchasing behavior across developed and emerging economies. For instance, e-commerce retailers are introducing biodegradable mailers and paper-based cushioning materials to reduce plastic waste associated with shipping operations. This shift in consumer expectations is encouraging packaging producers to develop innovative compostable and recyclable packaging formats, supporting long-term market expansion.

Market Restraint

High Production Costs and Limited Industrial Composting Infrastructure

One of the major restraints affecting the biodegradable packaging materials market is the relatively high production cost of biodegradable materials compared to conventional plastics. Biopolymers derived from renewable feedstocks often involve higher raw material and processing expenses, making sustainable packaging products more expensive for manufacturers and consumers. Small businesses and price-sensitive industries may hesitate to transition fully toward biodegradable solutions due to budget constraints. Additionally, limited industrial composting infrastructure in several countries restricts the effective disposal and decomposition of biodegradable packaging materials. For example, biodegradable plastic packaging may still end up in landfills in regions lacking proper composting facilities, reducing environmental benefits. These infrastructure and cost-related challenges could slow widespread adoption in certain developing economies during the forecast period.

Market Opportunities

Expansion of Sustainable E-commerce Packaging Solutions

The rapid growth of e-commerce is creating substantial opportunities for biodegradable packaging manufacturers. Online retail companies are increasingly adopting sustainable shipping materials to reduce packaging waste and meet consumer sustainability expectations. Biodegradable mailers, paper-based cushioning, compostable tape, and molded fiber protective packaging are gaining traction among e-commerce retailers and logistics providers. Several major retail brands are implementing packaging reduction programs focused on replacing plastic packaging with compostable alternatives. Future growth opportunities are expected to emerge from smart biodegradable packaging systems designed for reusable and recyclable shipping applications. As online retail continues expanding globally, demand for environmentally friendly shipping solutions is anticipated to rise steadily.

Increasing Demand from Healthcare and Pharmaceutical Packaging

The healthcare and pharmaceutical industries are creating new growth opportunities for biodegradable packaging materials. Rising demand for sustainable medical packaging, disposable healthcare products, and eco-friendly pharmaceutical containers is encouraging manufacturers to develop biodegradable alternatives suitable for sterile and sensitive applications. Several healthcare companies are investing in compostable blister packs, biodegradable medical trays, and renewable packaging films for over-the-counter medicines. Future opportunities are expected to emerge from bio-based packaging solutions designed for temperature-sensitive pharmaceutical products and single-use medical devices. Growing environmental awareness within healthcare systems is likely to support broader adoption of sustainable packaging technologies over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 108.6 Billion |

| Market Size in 2026 | USD 117.4 Billion |

| Market Size in 2034 | USD 228.7 Billion |

| CAGR | 8.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Starch-based biodegradable packaging dominated the market in 2024, accounting for approximately 33.8% of the global market share. These packaging materials are widely used because of their biodegradability, cost efficiency, and compatibility with food-contact applications. Starch-based packaging solutions are commonly produced from corn, potato, and tapioca starch and are increasingly used for disposable food containers, films, and shopping bags. Food service companies and retailers prefer starch-based materials because they decompose more efficiently than conventional plastics under composting conditions. In addition, ongoing advancements in starch blending technologies are improving moisture resistance and structural strength, enabling broader application across flexible packaging and industrial packaging segments. Their affordability and large-scale commercial availability continue supporting strong market demand globally.

Cellulose-based biodegradable packaging is expected to be the fastest-growing subsegment, registering a CAGR of 9.5% during the forecast period. Cellulose packaging materials derived from wood pulp and plant fibers are gaining popularity due to their renewable nature and high compostability. Several packaging manufacturers are introducing transparent cellulose films and molded cellulose containers as alternatives to petroleum-based plastics. Demand is particularly strong within premium food packaging, cosmetics, and healthcare applications where sustainability and product appearance are important purchasing factors. Future growth opportunities are expected to emerge from nanocellulose technologies capable of improving barrier properties and packaging durability. As investments in renewable fiber processing increase, cellulose-based packaging is anticipated to witness broader commercial adoption globally.

By Material

Bioplastics held the dominant market share of 49.4% in 2024 due to their extensive use across flexible packaging, food containers, bottles, and protective packaging applications. Materials such as polylactic acid, polyhydroxyalkanoates, and biodegradable polyester blends are increasingly replacing conventional plastics in consumer packaging industries. Bioplastics provide lightweight properties, improved design flexibility, and compatibility with industrial composting systems. Food manufacturers and beverage companies are increasingly adopting bioplastic films and containers to meet sustainability goals and comply with plastic reduction regulations. In addition, technological advancements in biopolymer processing are improving product durability, heat resistance, and shelf-life performance. These developments continue supporting strong demand for bioplastic packaging materials across global packaging markets.

Molded fiber materials are projected to be the fastest-growing material segment, expanding at a CAGR of 9.1% during the forecast period. Molded fiber packaging produced from recycled paper and agricultural residues is gaining popularity due to its recyclability and compostability. E-commerce companies and electronics manufacturers are increasingly replacing plastic protective inserts with molded fiber cushioning solutions to reduce packaging waste. Food service companies are also using molded fiber trays and clamshell containers for takeaway packaging applications. Future growth is expected to be supported by improvements in moisture resistance coatings and high-strength molded fiber technologies capable of supporting industrial packaging applications. Rising restrictions on expanded polystyrene packaging are likely to accelerate demand for molded fiber alternatives.

By End-Use

Food & beverage dominated the end-use segment in 2024, accounting for approximately 44.3% of the global biodegradable packaging materials market share. The food industry is rapidly adopting compostable packaging materials for takeaway containers, beverage cups, snack packaging, and fresh produce packaging. Rising consumer demand for environmentally responsible food packaging and increasing government restrictions on single-use plastics are driving strong segment growth. Restaurants, supermarkets, and packaged food companies are integrating biodegradable packaging into sustainability programs to improve brand reputation and reduce environmental impact. In addition, the rapid expansion of food delivery services and online grocery platforms is increasing demand for compostable packaging products capable of maintaining product freshness and transportation durability.

Healthcare packaging is expected to be the fastest-growing end-use segment, registering a CAGR of 9.4% through 2034. Healthcare companies are increasingly adopting biodegradable packaging solutions for disposable medical products, pharmaceutical containers, and healthcare shipping materials. Sustainability initiatives within hospitals and pharmaceutical industries are encouraging the use of renewable packaging materials to reduce medical waste generation. Several manufacturers are developing biodegradable sterile packaging films and compostable medical trays suitable for healthcare applications. Future growth opportunities are expected to emerge from temperature-resistant biodegradable packaging materials designed for pharmaceutical cold chain logistics. The increasing focus on sustainable healthcare infrastructure is likely to support broader adoption of biodegradable packaging technologies across medical industries.

Biodegradable Packaging Materials Market Segmentations

By Type

- Starch-Based Packaging

- Cellulose-Based Packaging

- PLA-Based Packaging

- PHA-Based Packaging

- Bagasse-Based Packaging

By Material

- Bioplastics

- Molded Fiber

- Paper & Paperboard

- Agricultural Waste Materials

By End-User

- Food & Beverage

- Healthcare Packaging

- Personal Care & Cosmetics

- E-commerce Packaging

- Industrial Packaging

Regional Analysis

North America

North America accounted for approximately 27.4% of the global biodegradable packaging materials market share in 2025 and is projected to expand at a CAGR of 8.1% during the forecast period. The region benefits from strong sustainability awareness, advanced packaging technologies, and increasing government initiatives supporting plastic waste reduction. Food service companies, retail chains, and e-commerce businesses across the United States and Canada are increasingly adopting biodegradable packaging materials to meet environmental targets and consumer preferences. Rising investments in compostable packaging manufacturing facilities and bio-based polymer research are also contributing to market growth. In addition, corporate sustainability commitments among multinational consumer goods companies are accelerating demand for renewable packaging materials across multiple industries.

The United States dominates the regional market due to its large retail and packaged food industries. One unique growth driver is the increasing adoption of sustainable packaging standards among major e-commerce companies. Online retailers are implementing plastic reduction strategies that encourage suppliers to use biodegradable mailers, cushioning materials, and recyclable shipping containers. Several states in the U.S. are also introducing regulations restricting foam food containers and non-recyclable plastics, further supporting market demand. Growing investments in industrial composting infrastructure are expected to improve the disposal efficiency of biodegradable packaging materials and strengthen long-term market expansion.

Europe

Europe represented approximately 29.1% of the global biodegradable packaging materials market share in 2025 and is expected to grow at a CAGR of 8.4% through 2034. The region remains strongly influenced by strict environmental policies, circular economy initiatives, and packaging waste reduction targets established by European authorities. Packaging manufacturers and food companies are increasingly transitioning toward compostable and fiber-based packaging formats to comply with sustainability regulations. Demand for biodegradable packaging materials is particularly strong in food delivery, cosmetics, and retail applications. In addition, growing investments in recycling and composting infrastructure are improving the commercial viability of biodegradable packaging products across European countries.

Germany remains the dominant country within the European market due to its advanced manufacturing sector and strong environmental regulations. A key growth factor is the increasing adoption of biodegradable industrial packaging solutions within automotive and consumer goods industries. German manufacturers are integrating molded fiber packaging and starch-based cushioning materials into export packaging operations to reduce plastic waste. Several retail chains are also introducing private-label products packaged in biodegradable containers and compostable films. These developments are expected to strengthen regional demand for advanced biodegradable packaging materials during the forecast period.

Asia Pacific

Asia Pacific held the largest market share of 38.6% in 2025 and is anticipated to register the fastest regional CAGR of 9.0% through 2034. Rapid urbanization, rising consumer awareness regarding environmental sustainability, and increasing government restrictions on plastic waste are driving regional market growth. Countries such as China, India, Japan, and South Korea are witnessing growing demand for biodegradable packaging materials across food service, retail, and e-commerce sectors. The expansion of organized retail and online grocery delivery services is also increasing the use of compostable packaging products. Furthermore, rising investments in biopolymer manufacturing and agricultural waste processing are strengthening regional production capabilities for sustainable packaging materials.

China dominates the Asia Pacific market due to its large manufacturing base and expanding packaging industry. One distinctive growth driver is the rapid expansion of biodegradable food delivery packaging solutions in urban areas. Several food delivery platforms and restaurant chains in China are adopting compostable containers, paper straws, and starch-based cutlery to comply with government plastic reduction initiatives. Chinese packaging manufacturers are also increasing investments in large-scale biopolymer production facilities to support domestic and export demand. These developments are expected to sustain strong market growth across the country over the forecast period.

Middle East & Africa

The Middle East & Africa accounted for approximately 2.8% of the global biodegradable packaging materials market share in 2025 and is projected to grow at a CAGR of 7.9% during the forecast period. Rising environmental awareness, increasing retail modernization, and government sustainability initiatives are contributing to regional market growth. Countries within the Gulf Cooperation Council are introducing regulations encouraging the use of biodegradable shopping bags and food packaging materials. The hospitality and tourism industries are also supporting demand for sustainable packaging products used in takeaway food and beverage applications. Additionally, several packaging companies are investing in renewable packaging technologies to align with broader environmental sustainability strategies across the region.

The United Arab Emirates remains the dominant market within the region due to its growing retail and food service industries. One unique growth driver is the increasing adoption of biodegradable packaging products in hospitality and tourism operations. Hotels, restaurants, and entertainment venues are replacing conventional plastic packaging with compostable alternatives to improve sustainability performance and attract environmentally conscious consumers. Several retail chains in the UAE are also introducing biodegradable shopping bags as part of government-supported plastic reduction programs. These trends are expected to strengthen market demand across the country during the forecast period.

Latin America

Latin America represented approximately 2.1% of the global biodegradable packaging materials market share in 2025 and is expected to register the fastest CAGR of 9.2% during the forecast period. Increasing environmental regulations, rising food exports, and growing consumer awareness regarding sustainable packaging are supporting regional market growth. Countries such as Brazil, Mexico, and Chile are adopting policies aimed at reducing single-use plastics and encouraging biodegradable packaging alternatives. The food processing and agricultural export sectors are increasingly using compostable packaging materials to improve sustainability performance and meet international trade requirements. In addition, rising e-commerce activity is increasing demand for biodegradable shipping and protective packaging products across the region.

Brazil dominates the Latin American market due to its large agricultural sector and expanding food packaging industry. A distinctive growth factor is the increasing production of biodegradable packaging materials derived from sugarcane bagasse and agricultural residues. Brazilian packaging manufacturers are utilizing abundant renewable feedstocks to develop compostable trays, containers, and cushioning materials for domestic and export applications. Several multinational food companies operating in Brazil are also implementing sustainable packaging initiatives focused on biodegradable materials. These developments are expected to support long-term market growth across the country and neighboring Latin American economies.

Competitive Landscape

The biodegradable packaging materials market is moderately competitive, with companies focusing on sustainable material innovation, production expansion, and strategic partnerships to strengthen market presence. Amcor plc remains one of the leading players in the market due to its broad sustainable packaging portfolio and strong global distribution network. The company recently expanded its recyclable and compostable flexible packaging solutions for food and healthcare applications.

Other major companies include Mondi Group, Sealed Air Corporation, Smurfit Kappa Group, and TIPA Corp. These companies are investing heavily in biodegradable film technologies, molded fiber production, and renewable feedstock sourcing to meet rising demand for eco-friendly packaging solutions. Strategic collaborations with food service providers, retail brands, and e-commerce companies are becoming increasingly common across the market. Several manufacturers are also expanding biopolymer production facilities across Asia Pacific and Europe to strengthen supply chain capabilities. Growing emphasis on circular economy initiatives and sustainable packaging regulations is expected to intensify competition among market participants during the forecast period.

Key Players List

- Amcor plc

- Mondi Group

- Sealed Air Corporation

- Smurfit Kappa Group

- TIPA Corp

- BASF SE

- Novamont S.p.A.

- NatureWorks LLC

- DS Smith Plc

- Huhtamaki Oyj

- WestRock Company

- Stora Enso Oyj

- International Paper Company

- Biopak Pty Ltd

- Vegware Ltd