Beverage Packaging Market Size and Growth

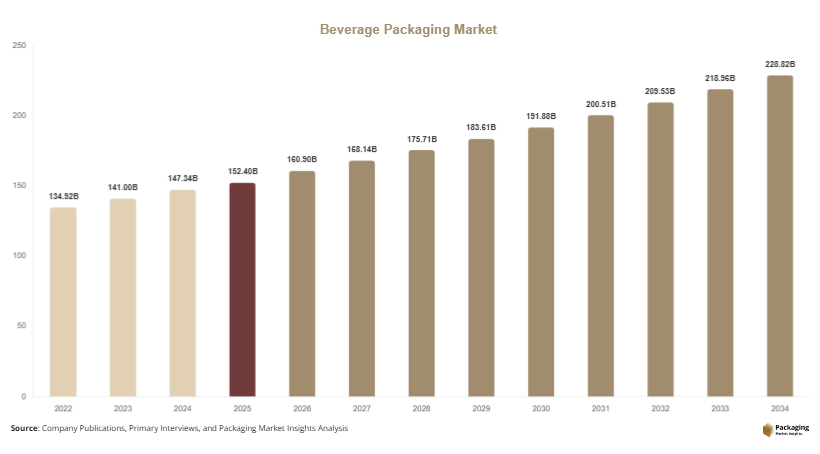

The global beverage packaging market was valued at approximately USD 152.4 billion in 2025 and is projected to reach USD 160.9 billion in 2026. With consistent demand across bottled water, carbonated drinks, juices, alcoholic beverages, and functional drinks, the market is expected to grow steadily to USD 238.6 billion by 2034, registering a CAGR of 4.5% during the forecast period (2025–2034).

Growth in this market is strongly supported by increasing urbanization and the shift toward convenience-oriented lifestyles. Consumers are prioritizing ready-to-drink products that are easy to carry, store, and consume, which is encouraging the use of lightweight and portable packaging formats. Additionally, sustainability concerns are influencing material choices, with manufacturers investing in recyclable plastics, biodegradable solutions, and paper-based alternatives. Governments worldwide are implementing regulations to reduce plastic waste, further pushing companies toward environmentally responsible packaging.

Key Market Insights:

- Asia Pacific dominated the market with a 38.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 5.8%.

- Plastic packaging led the material segment with a 49.7% share, while paper-based packaging is expected to grow at a CAGR of 5.6%.

- Bottles dominated the packaging type segment with a 44.3% share, while flexible pouches are forecasted to grow at a CAGR of 6.2%.

- Non-alcoholic beverages led the application segment with 57.6% share, while functional beverages are expected to grow at a CAGR of 6.5%.

- China remained the dominant country with a market size of USD 18.6 billion in 2025 and USD 19.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Beverage Packaging Market Trends

Rising shift toward sustainable and circular packaging systems

Sustainability is becoming a defining element in the beverage packaging market, influencing both material selection and production processes. Companies are increasingly adopting recyclable, compostable, and reusable packaging formats to align with environmental regulations and consumer expectations. Materials such as aluminum, glass, and paper-based cartons are gaining popularity due to their recyclability and reduced environmental footprint. Manufacturers are also focusing on lightweighting strategies to minimize raw material usage and lower transportation emissions.

The development of plant-based plastics and bio-polymers is further supporting this transition toward eco-friendly solutions. In addition, beverage companies are collaborating with packaging firms to establish closed-loop recycling systems and circular economy initiatives. These approaches aim to reduce waste and promote the reuse of materials, thereby enhancing long-term sustainability. As regulatory frameworks become stricter and consumers demand greater transparency, sustainable packaging solutions are expected to play a central role in shaping market dynamics.

Integration of smart and connected packaging technologies

Technological advancements are driving the adoption of smart and connected packaging solutions across the beverage industry. Packaging is increasingly being used as a communication tool, incorporating features such as QR codes, NFC tags, and augmented reality elements. These technologies enable consumers to access detailed product information, verify authenticity, and engage with brands in innovative ways.

Smart packaging also enhances supply chain efficiency by enabling real-time tracking and monitoring of products. Features such as temperature-sensitive labels and freshness indicators are particularly valuable for perishable beverages, ensuring product quality and safety. Additionally, digital packaging solutions allow companies to collect consumer data and gain insights into purchasing behavior, supporting targeted marketing strategies. As competition intensifies, the integration of intelligent packaging technologies is becoming a key factor in product differentiation and brand positioning.

Beverage Packaging Market Drivers

Growing demand for convenience-driven packaging formats

The increasing pace of modern lifestyles is significantly influencing the demand for convenient beverage packaging solutions. Consumers are seeking packaging that is easy to carry, open, and reseal, especially in urban environments where on-the-go consumption is common. Formats such as single-serve bottles, cans, and flexible pouches are gaining widespread acceptance due to their portability and ease of use.

Retail expansion, including supermarkets, convenience stores, and online platforms, is further supporting this trend by prioritizing packaging that enhances shelf visibility and transportation efficiency. Beverage manufacturers are continuously innovating to improve functionality, introducing ergonomic designs, spill-proof closures, and resealable caps. These advancements not only improve user experience but also help brands maintain a competitive edge. As consumer expectations for convenience continue to rise, packaging innovation remains a critical growth factor.

Expansion of global beverage consumption across categories

The steady growth of the global beverage industry is a major factor driving the beverage packaging market. Increasing consumption of bottled water, energy drinks, dairy beverages, and alcoholic products is creating sustained demand for diverse packaging solutions. Emerging markets are playing a crucial role in this expansion, supported by rising disposable incomes, urbanization, and changing dietary habits.

The introduction of new beverage categories, including plant-based drinks and functional beverages, is further contributing to market growth. These products often require specialized packaging to preserve nutritional value and maintain product integrity. Additionally, beverage companies are investing in advanced packaging designs to enhance brand visibility and differentiate their offerings in a competitive marketplace. As production volumes increase and distribution networks expand, the demand for efficient and innovative packaging solutions is expected to grow consistently.

Beverage Packaging Market Restraint

Regulatory pressure and environmental concerns related to plastic packaging

Environmental concerns associated with plastic waste present a significant challenge for the beverage packaging market. Governments across various regions are implementing strict regulations aimed at reducing single-use plastics, including bans, taxes, and recycling mandates. These measures are compelling manufacturers to shift toward alternative materials such as glass, aluminum, and paper-based packaging.

However, transitioning to sustainable materials involves higher costs and operational complexities. For example, glass packaging increases transportation expenses due to its weight and fragility, while biodegradable materials often require advanced production technologies. Small and medium-sized enterprises may face difficulties in adapting to these changes, which can impact overall market growth. Despite these challenges, companies are investing in research and development to create innovative and cost-effective sustainable packaging solutions, gradually addressing these constraints.

Beverage Packaging Market Opportunities

Rising demand in emerging economies with expanding consumer base

Emerging economies present significant opportunities for growth in the beverage packaging market due to rapid urbanization, population expansion, and increasing purchasing power. Regions such as Asia Pacific, Latin America, and parts of Africa are witnessing a surge in demand for packaged beverages, driven by changing consumer preferences and improved access to modern retail channels.

Local manufacturers are investing in cost-effective packaging solutions to cater to price-sensitive consumers while maintaining product quality. Additionally, multinational beverage companies are expanding their presence in these markets, creating demand for scalable and efficient packaging systems. As infrastructure and distribution networks continue to improve, the market is expected to benefit from increased penetration in rural and semi-urban areas, further driving growth.

Advancements in lightweight and high-performance packaging materials

Continuous innovation in packaging materials is creating new growth opportunities within the market. Lightweight packaging solutions are gaining traction as they reduce material usage, lower transportation costs, and minimize environmental impact. Advanced materials such as high-barrier films and hybrid composites are improving product protection and extending shelf life.

Functional features such as resealability, tamper evidence, and enhanced durability are becoming increasingly important in beverage packaging. These features not only improve product safety but also enhance consumer convenience and satisfaction. Companies that invest in advanced material technologies and innovative design solutions are likely to gain a competitive advantage, as they can meet evolving consumer demands while addressing sustainability concerns.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 152.4 Billion |

| Market Size in 2026 | USD 160.9 Billion |

| Market Size in 2034 | USD 238.6 Billion |

| CAGR | 4.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Beverage Packaging Market Segmental Analysis

By Material

Plastic packaging accounted for the largest share of 49.7% in 2024 due to its versatility, lightweight nature, and cost-effectiveness. It is widely used in the production of bottles, caps, and flexible packaging for beverages such as water, soft drinks, and juices. Plastic materials offer excellent barrier properties and durability, making them suitable for mass production and transportation.

Paper-based packaging is expected to witness the fastest growth, with a CAGR of 5.6% during the forecast period. This growth is driven by increasing environmental concerns and consumer preference for sustainable alternatives. Innovations in coating technologies are improving the performance of paper packaging, making it suitable for liquid applications while maintaining recyclability.

By Packaging Type

Bottles dominated the market with a 44.3% share in 2024, driven by their widespread use across various beverage categories. Glass and plastic bottles provide excellent product protection, visibility, and branding opportunities, making them a preferred choice for both premium and mass-market beverages.

Flexible pouches are projected to be the fastest-growing segment, with a CAGR of 6.2%. Their lightweight design and reduced material usage make them cost-effective and environmentally friendly. Increasing demand for portable and single-serve packaging solutions is supporting the growth of this segment.

By Application

Non-alcoholic beverages held the largest share of 57.6% in 2024 due to high consumption of bottled water, soft drinks, and juices. Packaging in this segment focuses on affordability, convenience, and shelf life, with manufacturers continuously innovating to improve product appeal.

Functional beverages are expected to grow at the fastest CAGR of 6.5%, driven by increasing health awareness among consumers. Packaging solutions for these products emphasize quality preservation and premium design, helping brands differentiate themselves in a competitive market.

Beverage Packaging Market Segmentations

By Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

By Packaging Type

- Bottles

- Cans

- Cartons

- Flexible Pouches

By Application

- Alcoholic Beverages

- Non-Alcoholic Beverages

- Functional Beverages

Beverage Packaging Market Regional Analysis

North America

North America accounted for approximately 24.6% of the beverage packaging market share in 2025 and is projected to grow at a CAGR of 3.9% during the forecast period. The region benefits from a well-established beverage industry, high consumption of packaged drinks, and advanced packaging infrastructure. Increasing awareness regarding sustainable packaging is influencing manufacturers to adopt recyclable and eco-friendly materials.

The United States dominates the regional market due to its strong beverage production capacity and technological advancements in packaging solutions. A key growth factor in the country is the increasing adoption of aluminum cans, supported by efficient recycling systems and consumer preference for environmentally responsible packaging formats.

Europe

Europe held around 21.8% of the global market share in 2025 and is expected to grow at a CAGR of 4.1%. The region is characterized by strict environmental regulations and a strong focus on reducing carbon emissions, which is shaping packaging strategies across the beverage industry. Companies are investing in sustainable materials and circular economy practices to comply with regulatory requirements.

Germany remains the leading country in this region due to its advanced manufacturing capabilities and strong recycling infrastructure. A unique growth factor is the implementation of deposit return schemes, which encourage consumers to return used packaging for recycling, thereby improving material recovery rates and reducing environmental impact.

Asia Pacific

Asia Pacific dominated the beverage packaging market with a 38.1% share in 2025 and is projected to grow at a CAGR of 5.2%. Rapid urbanization, population growth, and increasing disposable income are driving demand for packaged beverages across the region. The expansion of retail networks and e-commerce platforms is further supporting market growth.

China leads the regional market, driven by its large consumer base and expanding beverage industry. A significant growth factor is the rising demand for bottled water and ready-to-drink beverages, supported by changing lifestyles and concerns over water safety in urban areas.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.4% of the market share in 2025 and is expected to grow at a CAGR of 4.8%. Increasing urbanization and tourism are contributing to the growing demand for packaged beverages, particularly in urban centers and hospitality sectors.

Saudi Arabia dominates the regional market due to its expanding retail sector and increasing consumption of premium beverages. A key growth factor is the development of cold chain logistics, which supports the distribution of temperature-sensitive beverage products across the region.

Latin America

Latin America held a market share of 8.1% in 2025 and is projected to grow at the fastest CAGR of 5.8%. The region is experiencing growth in beverage consumption due to rising incomes, urbanization, and changing consumer preferences. Demand for convenient and affordable packaging solutions is increasing across various beverage categories.

Brazil leads the regional market, supported by its large population and well-established beverage industry. A unique growth factor is the growing adoption of flexible packaging formats, which offer cost efficiency, lightweight properties, and convenience for both manufacturers and consumers.

Beverage Packaging Market Competitive Landscape

The beverage packaging market is moderately fragmented, with several global and regional players competing through innovation, sustainability initiatives, and strategic partnerships. Companies are focusing on developing advanced packaging solutions that align with regulatory requirements and changing consumer preferences. Investments in research and development are enabling the introduction of lightweight, recyclable, and high-performance packaging materials.

Amcor plc is recognized as a leading company in the market, driven by its strong focus on sustainable packaging innovations. The company has introduced recyclable and reusable packaging solutions aimed at reducing environmental impact. Other major players are expanding their production capacities and forming collaborations to strengthen their market position and address the growing demand for eco-friendly packaging.

Key Players in the beverage packaging market

- Amcor plc

- Ball Corporation

- Crown Holdings, Inc.

- Tetra Pak International S.A.

- Ardagh Group S.A.

- O-I Glass, Inc.

- Berry Global Inc.

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Smurfit Kappa Group

- Huhtamaki Oyj

- WestRock Company

- DS Smith Plc

- Silgan Holdings Inc.