Beverage Closures Market Size and Growth

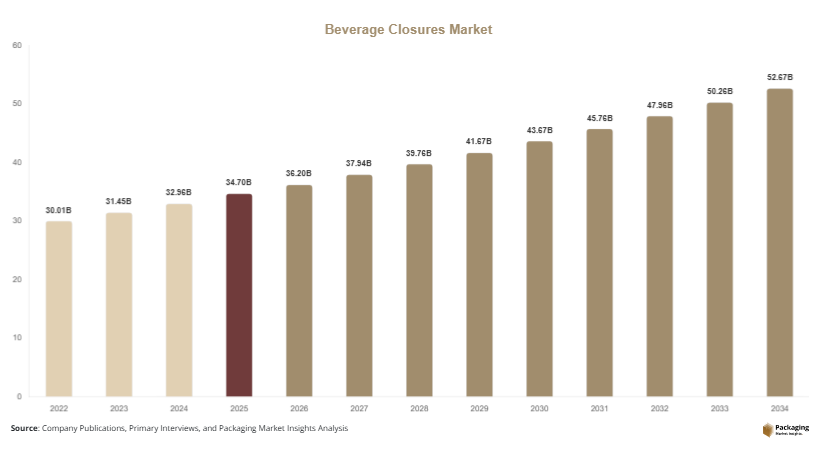

The global beverage closures market size is estimated at USD 34.7 billion in 2025 and is projected to reach USD 36.2 billion in 2026. Driven by packaging innovation, convenience trends, and sustainability initiatives, the market is expected to reach USD 52.9 billion by 2034, registering a CAGR of 4.8% during the forecast period (2025–2034). Beverage closures, including caps, corks, and lids, play a critical role in preserving product quality, ensuring safety, and enhancing consumer convenience. The beverage closures market is experiencing steady expansion as global beverage consumption rises across both alcoholic and non-alcoholic categories.

One of the major growth factors is the increasing demand for bottled beverages such as carbonated drinks, bottled water, juices, and alcoholic beverages. As consumption patterns evolve, manufacturers are focusing on closures that offer ease of use, resealability, and tamper evidence. Another key factor is the growth of premium and functional beverages, where closures contribute to product differentiation and brand identity. In addition, the expansion of the global beverage industry, particularly in emerging economies, is fueling the demand for cost-effective and high-performance closure solutions.

Key Highlights:

- Asia Pacific dominated the market with a 38.6% share in 2025, while Latin America is projected to grow at the fastest CAGR of 5.9%.

- Plastic closures led the type segment with a 57.2% share, while metal closures are expected to grow at a CAGR of 5.1%.

- Screw caps dominated with a 49.5% share, while dispensing closures are forecasted to grow at a CAGR of 5.7%.

- Non-alcoholic beverages led the segment with 62.4% share, while functional beverages are expected to grow at a CAGR of 6.2%.

- China remained the dominant country with a market size of USD 8.4 billion in 2025 and USD 8.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing focus on sustainable and recyclable closure materials

Sustainability is becoming a central theme in the beverage closures market as manufacturers respond to environmental concerns and regulatory pressures. Companies are shifting toward recyclable materials such as high-density polyethylene and polypropylene to reduce environmental impact. The development of tethered caps, which remain attached to bottles after opening, is gaining traction as part of efforts to reduce plastic waste. Beverage brands are also adopting closures made from bio-based materials to align with sustainability goals. These initiatives are particularly prominent in regions with strict environmental regulations, where companies are required to meet recycling targets and reduce packaging waste.

Growing demand for convenience-oriented and functional closures

Consumer preferences are evolving toward convenience and ease of use, influencing the design and functionality of beverage closures. Features such as easy-open mechanisms, resealability, and spill prevention are becoming essential in modern packaging. Dispensing closures and sports caps are gaining popularity, especially in the bottled water and energy drink segments. These closures enhance user experience by enabling controlled pouring and portability. Additionally, the rise of on-the-go consumption is driving demand for single-serve packaging with user-friendly closures. Manufacturers are focusing on ergonomic designs and innovative features to meet these changing consumer expectations.

Market Drivers

Expansion of global beverage consumption across categories

The increasing consumption of beverages across various categories is a key factor driving the beverage closures market. The demand for bottled water, carbonated drinks, juices, and alcoholic beverages continues to rise, supported by population growth and changing lifestyles. Urbanization and rising disposable incomes are further contributing to increased beverage consumption. As beverage production expands, the demand for reliable and efficient closure solutions also grows. Closures play a critical role in maintaining product quality and safety, making them an essential component of beverage packaging.

Advancements in packaging technologies and product innovation

Technological advancements in packaging are driving innovation in beverage closures. Manufacturers are developing lightweight closures that reduce material usage without compromising performance. Improved sealing technologies enhance product shelf life and prevent leakage, ensuring product integrity during transportation and storage. Additionally, innovations such as tamper-evident and child-resistant closures are addressing safety concerns and regulatory requirements. These advancements are enabling manufacturers to meet the evolving needs of the beverage industry while maintaining cost efficiency and sustainability.

Market Restraint

Environmental concerns related to plastic waste and recycling challenges

Environmental concerns associated with plastic waste pose a challenge to the beverage closures market. While plastic closures are widely used due to their cost-effectiveness and versatility, their disposal can contribute to environmental pollution if not properly managed. Recycling challenges, including contamination and collection inefficiencies, can limit the effectiveness of sustainability initiatives. For example, closures made from mixed materials may be difficult to recycle, reducing their environmental benefits. These issues are prompting regulatory authorities to impose stricter guidelines on plastic usage, which can increase compliance costs for manufacturers and impact market growth.

Market Opportunities

Development of bio-based and lightweight closure solutions

The growing emphasis on sustainability is creating opportunities for the development of bio-based and lightweight beverage closures. Manufacturers are exploring renewable materials such as plant-based plastics to reduce environmental impact. Lightweight closures help reduce material usage and transportation costs, contributing to overall sustainability. These innovations enable companies to meet regulatory requirements and consumer expectations while maintaining performance. The adoption of such solutions is expected to increase as sustainability becomes a priority in the beverage industry.

Expansion of beverage markets in emerging economies

Emerging markets offer significant growth opportunities for the beverage closures market. Rapid urbanization, increasing disposable incomes, and changing consumer preferences are driving demand for packaged beverages in these regions. The expansion of retail and distribution networks is further supporting market growth. Manufacturers can capitalize on these opportunities by offering cost-effective and adaptable closure solutions tailored to local market needs. The growing popularity of functional and premium beverages in emerging economies is also contributing to increased demand for advanced closure systems.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 34.7 Billion |

| Market Size in 2026 | USD 36.2 Billion |

| Market Size in 2034 | USD 52.9 Billion |

| CAGR | 4.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Plastic closures dominated the market in 2024, accounting for 57.2% of the total share. This dominance is attributed to their lightweight nature, cost-effectiveness, and versatility. Plastic closures are widely used across various beverage categories due to their ability to provide secure sealing and ease of use. Materials such as polypropylene and polyethylene are commonly used in closure manufacturing, offering durability and resistance to environmental conditions.

Metal closures are expected to grow at a CAGR of 5.1% during the forecast period. This growth is driven by their use in premium and alcoholic beverages, where aesthetics and durability are important. Metal closures provide a high level of sealing performance and are often used in glass bottle packaging. The increasing demand for premium beverages is supporting the growth of this segment.

By Product Type

Screw caps accounted for the largest share of 49.5% in 2024. These closures are widely used due to their convenience and ability to provide a secure seal. Screw caps are easy to open and reseal, making them suitable for a wide range of beverages. Their cost-effectiveness and compatibility with automated production processes further enhance their adoption.

Dispensing closures are projected to grow at a CAGR of 5.7%, driven by their functionality and convenience. These closures allow controlled dispensing of liquids, making them suitable for sports drinks and energy beverages. The increasing demand for on-the-go consumption is supporting the growth of this segment.

By Application

Non-alcoholic beverages held the largest share of 62.4% in 2024. This segment includes bottled water, soft drinks, and juices, which require reliable closure solutions to maintain product quality. The high consumption of these beverages globally is driving the demand for closures.

Functional beverages are expected to grow at a CAGR of 6.2% during the forecast period. This growth is driven by increasing consumer interest in health and wellness products. Functional beverages often require specialized closures that support convenience and usability, contributing to market growth.

Beverage Closures Market Segmentations

By Material Type

- Plastic Closures

- Metal Closures

By Product Type

- Screw Caps

- Dispensing Closures

By Application

- Non-Alcoholic Beverages

- Alcoholic Beverages

- Functional Beverages

Regional Analysis

North America

North America accounted for 21.9% of the beverage closures market share in 2025 and is expected to grow at a CAGR of 4.5% during the forecast period. The region benefits from a well-established beverage industry and advanced packaging technologies. The demand for convenience and premium packaging is driving the adoption of innovative closure solutions. Additionally, sustainability initiatives are encouraging the use of recyclable materials in closure manufacturing.

The United States dominates the regional market due to its large beverage production and consumption levels. A unique growth factor is the increasing demand for functional beverages such as sports drinks and flavored water, which require specialized closure designs for convenience and usability.

Europe

Europe held a market share of 23.8% in 2025 and is projected to grow at a CAGR of 4.7%. The region is characterized by strict environmental regulations and a strong focus on sustainability. The adoption of recyclable and bio-based closure materials is increasing as companies aim to reduce environmental impact. The presence of leading beverage manufacturers further supports market growth.

Germany is the dominant country in the European market, driven by its advanced manufacturing capabilities. A unique growth factor is the implementation of circular economy practices, which encourage the use of recyclable materials and efficient waste management systems in packaging.

Asia Pacific

Asia Pacific dominated the market with a 38.6% share in 2025 and is expected to grow at a CAGR of 5.4%. The region’s growth is driven by rapid urbanization, population growth, and increasing beverage consumption. The expansion of retail and e-commerce sectors is further supporting market growth. Cost-effective manufacturing and raw material availability also contribute to the region’s dominance.

China remains the leading country in the region due to its large beverage industry. A unique growth factor is the increasing demand for bottled water and ready-to-drink beverages, which is driving the need for efficient closure solutions.

Middle East & Africa

The Middle East & Africa region accounted for 7.1% of the market share in 2025 and is projected to grow at a CAGR of 5.2%. Growth is supported by increasing urbanization and rising demand for packaged beverages. The development of retail infrastructure is further contributing to market expansion.

South Africa is a key market in the region, supported by its growing beverage industry. A unique growth factor is the increasing adoption of bottled water due to concerns about water quality, which is driving demand for beverage closures.

Latin America

Latin America held an 8.6% share in 2025 and is expected to grow at the fastest CAGR of 5.9%. The region’s growth is driven by increasing consumer demand and expanding beverage production. The adoption of sustainable packaging solutions is also gaining momentum.

Brazil dominates the regional market due to its large population and strong beverage industry. A unique growth factor is the rising popularity of carbonated and alcoholic beverages, which is increasing the demand for various types of closures.

Competitive Landscape

The beverage closures market is moderately competitive, with several global and regional players focusing on innovation, sustainability, and cost efficiency. Companies are investing in research and development to introduce advanced closure solutions that meet evolving consumer and regulatory requirements. Strategic partnerships and acquisitions are common strategies used to strengthen market presence.

Crown Holdings, Inc. is a leading player in the market, known for its extensive portfolio of metal and plastic closures. The company recently introduced lightweight and recyclable closure solutions to support sustainability initiatives. Other players are also focusing on expanding their product offerings and enhancing manufacturing capabilities to meet growing demand.

Key Players List

- Crown Holdings, Inc.

- Amcor plc

- Berry Global Inc.

- AptarGroup, Inc.

- Silgan Holdings Inc.

- Closure Systems International, Inc.

- Guala Closures Group

- Bericap Holding GmbH

- O.Berk Company, LLC

- Nippon Closures Co., Ltd.

- Albea Group

- Phoenix Closures, Inc.

- United Caps Luxembourg S.A.

- Plastic Closures Limited

- Mold-Rite Plastics