Beer Glass Packaging Market Size and Growth

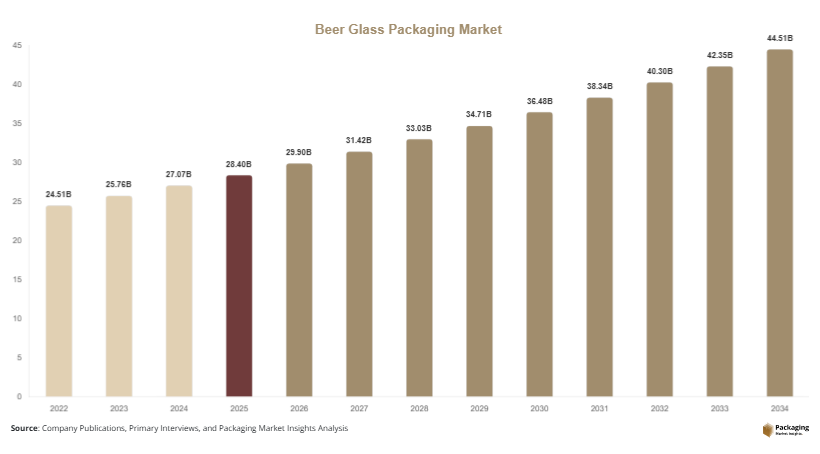

The global beer glass packaging market size is estimated to reach USD 28.4 billion in 2025 and is projected to grow to approximately USD 29.9 billion in 2026. Over the forecast period, the market is expected to reach USD 44.7 billion by 2034, registering a CAGR of 5.1% from 2025 to 2034. Glass packaging remains a preferred choice in the beer industry due to its ability to preserve taste, maintain carbonation, and offer a premium product appearance. The beer glass packaging market is witnessing steady expansion driven by the continued growth of the global beer industry and increasing preference for premium and sustainable packaging formats.

One of the primary growth factors is the rising demand for premium and craft beers, where glass bottles and containers are widely used to enhance brand perception and consumer experience. Another important factor is the increasing emphasis on sustainable and recyclable packaging, as glass is fully recyclable and aligns with environmental goals. In addition, the growth of on-trade and off-trade consumption channels, including bars, restaurants, and retail stores, is driving demand for durable and visually appealing packaging formats.

Key Highlights

- Asia Pacific dominated the market with a 36.9% share in 2025, while Latin America is projected to grow at the fastest CAGR of 5.8%.

- Amber glass led the type segment with a 48.5% share, while flint glass is expected to grow at a CAGR of 5.6%.

- Bottles dominated the product segment with a 72.3% share, while glass cans are forecasted to grow at a CAGR of 5.9%.

- Alcoholic beverage applications led the segment with 91.4% share, while non-alcoholic variants are expected to grow at a CAGR of 5.2%.

- China remained the dominant country with a market size of USD 6.2 billion in 2025 and USD 6.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing preference for premium and aesthetically appealing glass packaging

The beer glass packaging market is witnessing a notable shift toward premium packaging designs that enhance brand identity and consumer appeal. Manufacturers are focusing on unique bottle shapes, embossed designs, and customized labeling to differentiate their products in a competitive market. This trend is particularly prominent in the craft beer segment, where packaging plays a crucial role in attracting consumers. Glass packaging offers superior clarity and visual appeal, allowing brands to showcase product quality. The demand for premium packaging is also driven by changing consumer preferences, as buyers increasingly associate glass containers with quality and authenticity. This trend is expected to continue as brands invest in innovative packaging solutions.

Growing adoption of lightweight and sustainable glass packaging solutions

Sustainability and cost efficiency are influencing the development of lightweight glass packaging in the beer glass packaging market. Manufacturers are reducing the weight of glass bottles without compromising strength, resulting in lower raw material usage and reduced transportation costs. Lightweight glass packaging also supports environmental goals by decreasing carbon emissions during production and distribution. Additionally, the recyclability of glass makes it an attractive option for companies aiming to meet sustainability targets. This trend is gaining traction across regions, as both consumers and regulatory bodies emphasize environmentally responsible packaging solutions.

Market Drivers

Expansion of the global beer industry and rising consumption

The growth of the global beer industry is a major factor driving the beer glass packaging market. Increasing consumer demand for beer, particularly in emerging economies, is boosting the need for reliable packaging solutions. Glass containers are widely used due to their ability to maintain product quality and prevent contamination. The rise in disposable income and changing lifestyle patterns are contributing to higher beer consumption, especially among younger demographics. Additionally, the growth of social and recreational activities is supporting demand for packaged beer products. As the beer industry continues to expand, the demand for glass packaging is expected to increase.

Increasing demand for sustainable and recyclable packaging materials

Sustainability is becoming a key consideration in packaging decisions, driving the adoption of glass containers in the beer industry. Glass is fully recyclable and can be reused multiple times without losing quality, making it an environmentally friendly option. Governments and regulatory bodies are encouraging the use of sustainable materials, further supporting market growth. Companies are investing in recycling infrastructure and promoting circular economy practices to reduce environmental impact. This shift toward sustainable packaging is expected to drive the demand for glass containers in the beer industry.

Market Restraint

High production and transportation costs associated with glass packaging

The beer glass packaging market faces challenges related to the high cost of production and transportation of glass containers. Glass manufacturing requires significant energy consumption, which increases production costs. Additionally, the weight of glass bottles contributes to higher transportation expenses compared to alternative packaging materials such as aluminum and plastic. These cost factors can impact profit margins for manufacturers and limit the adoption of glass packaging in certain markets. For example, small and medium-sized breweries may find it difficult to manage the higher costs associated with glass packaging, leading them to consider alternative materials. This restraint may affect market growth, particularly in price-sensitive regions.

Market Opportunities

Growth of craft breweries and premium beer segments

The increasing number of craft breweries presents significant opportunities for the beer glass packaging market. Craft beer producers often emphasize product quality and brand identity, making glass packaging an ideal choice. These breweries are experimenting with unique packaging designs to attract consumers and differentiate their products. The growing popularity of craft beer is driving demand for customized glass bottles and containers. As the craft beer segment continues to expand, it is expected to create new growth opportunities for glass packaging manufacturers.

Advancements in glass manufacturing technologies

Technological advancements in glass manufacturing are creating opportunities for innovation in the beer glass packaging market. Developments such as lightweight glass, improved durability, and enhanced design capabilities are making glass packaging more efficient and cost-effective. These innovations are helping manufacturers address challenges related to production costs and transportation. Additionally, advancements in decoration and labeling techniques are enabling brands to create visually appealing packaging solutions. As technology continues to evolve, it is expected to drive the adoption of glass packaging in the beer industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.4 Billion |

| Market Size in 2026 | USD 29.9 Billion |

| Market Size in 2034 | USD 44.7 Billion |

| CAGR | 5.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Glass Type

Amber glass dominated the beer glass packaging market in 2024, accounting for approximately 48.5% of the total share. This type of glass is widely used due to its ability to protect beer from ultraviolet light, which can affect flavor and quality. Amber glass bottles are commonly used for packaging various types of beer, making them a preferred choice among manufacturers.

Flint glass is expected to grow at the fastest CAGR of 5.6%. This type of glass offers high clarity and is used for premium beer packaging. The increasing demand for visually appealing packaging is driving the growth of this segment.

By Product Type

Glass bottles accounted for the largest market share in 2024, representing 72.3% of the total market. These bottles are widely used due to their durability and ability to preserve product quality. Glass bottles are available in various shapes and sizes, making them suitable for different beer products.

Glass cans are expected to grow at the fastest CAGR of 5.9%. These containers offer a unique combination of aesthetics and functionality, making them an emerging trend in the market.

By Application

Alcoholic beverage packaging dominated the market in 2024, accounting for 91.4% of the total share. The high consumption of beer and other alcoholic beverages is driving demand for glass packaging solutions.

Non-alcoholic variants are expected to grow at the fastest CAGR of 5.2%. The increasing popularity of alcohol-free beer is supporting the growth of this segment.

Beer Glass Packaging Market Segmentations

By Glass Type

- Amber Glass

- Flint Glass

- Green Glass

By Product Type

- Glass Bottles

- Glass Cans

- Specialty Containers

By Application

- Alcoholic Beverages

- Non-Alcoholic Beverages

Regional Analysis

North America

North America accounted for approximately 22.8% of the beer glass packaging market in 2025 and is expected to grow at a CAGR of 4.9% during the forecast period. The region’s mature beer industry and strong presence of craft breweries are key factors driving market growth. Increasing demand for premium beer products is also supporting the adoption of glass packaging.

The United States dominates the regional market due to its large consumer base and well-established beverage industry. A unique growth factor is the rising number of microbreweries, which are driving demand for customized and high-quality glass packaging solutions.

Europe

Europe held a market share of around 24.6% in 2025 and is projected to grow at a CAGR of 5.0%. The region’s long-standing beer culture and strong focus on sustainability are influencing the demand for glass packaging. Regulatory initiatives promoting recyclable materials are also supporting market growth.

Germany leads the European market due to its strong beer production and consumption. A unique growth factor is the widespread use of returnable glass bottles, which supports recycling and reduces environmental impact.

Asia Pacific

Asia Pacific dominated the beer glass packaging market in 2025 with a 36.9% share and is expected to grow at a CAGR of 5.4%. Rapid urbanization, population growth, and increasing disposable incomes are driving demand for beer products in the region.

China is the dominant country, supported by a large consumer base and expanding beer industry. A unique growth factor is the increasing demand for premium beer products, which drives the adoption of glass packaging.

Middle East & Africa

The Middle East & Africa region accounted for 7.1% of the market share in 2025 and is expected to grow at a CAGR of 4.8%. The growing hospitality sector and increasing tourism are driving demand for beer packaging solutions.

South Africa is a key market in the region, supported by a well-developed beverage industry. A unique growth factor is the expansion of tourism, which boosts demand for packaged beverages.

Latin America

Latin America held a market share of 8.6% in 2025 and is projected to grow at the fastest CAGR of 5.8%. The region’s growing middle class and increasing beer consumption are key drivers of market growth.

Brazil dominates the regional market due to its large population and strong beer industry. A unique growth factor is the rising popularity of local beer brands, which increases demand for glass packaging.

Competitive Landscape

The beer glass packaging market is characterized by the presence of several global and regional players focusing on innovation, sustainability, and product differentiation. Leading companies include Ardagh Group, Owens-Illinois Inc., Verallia, Vidrala S.A., and Vetropack Holding Ltd. Among these, Owens-Illinois Inc. is recognized as a leading player due to its extensive product portfolio and global presence.

Companies are investing in advanced manufacturing technologies and sustainable practices to enhance their competitive position. Recent developments include the introduction of lightweight glass bottles and expansion of production capacities.

Key Players List

- Ardagh Group

- Owens-Illinois Inc.

- Verallia

- Vidrala S.A.

- Vetropack Holding Ltd.

- BA Glass

- Gerresheimer AG

- Heinz-Glas GmbH

- Hindusthan National Glass & Industries Ltd.

- Saverglass Group

- Wiegand-Glas

- Zignago Vetro

- Stoelzle Glass Group

- AGI Glasspack Ltd.

- Piramal Glass Pvt. Ltd.