Beer Cans Market Size and Growth

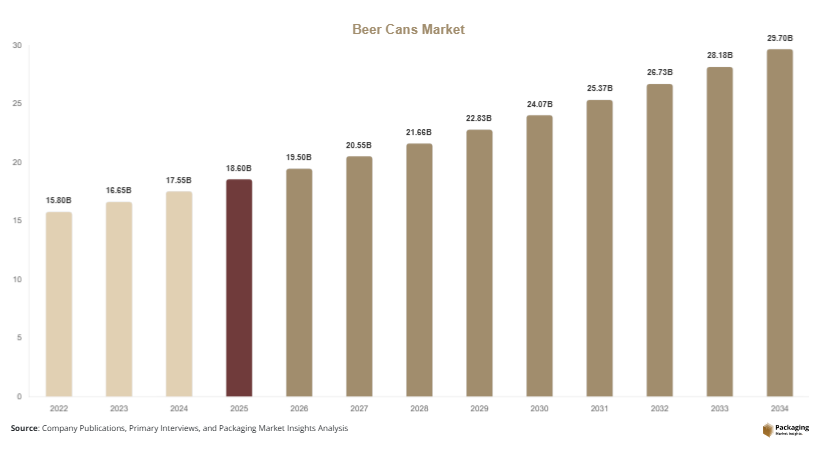

The global beer cans market was valued at approximately USD 18.6 billion in 2025 and is estimated to reach USD 19.5 billion in 2026. The market is projected to grow at a CAGR of 5.4% from 2025 to 2034, reaching nearly USD 31.2 billion by the end of the forecast period. The increasing consumption of canned alcoholic beverages, expansion of craft beer production, and growing preference for sustainable packaging solutions are supporting the steady growth of the market across major economies.

Beer cans have become a preferred packaging format for breweries because they provide longer shelf life, lightweight transportation, and superior protection against light and oxygen exposure. Aluminum cans are increasingly replacing glass bottles in several markets due to their recyclability and lower logistics costs. In addition, changing consumer lifestyles and rising demand for portable beverage packaging are encouraging breweries to expand canned beer product lines.

Key Highlights

- Asia Pacific dominated the market with a 36.9% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.1%.

- Two-piece beer cans led the type segment with a 68.4% share.

- Aluminum material dominated with a 79.2% share.

- Alcoholic beverage applications led the segment with 84.6% share.

- The US remained the dominant country with a market size of USD 4.2 billion in 2025 and USD 4.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable Aluminum Packaging

Sustainability has become a major trend influencing the beer cans market as breweries and beverage manufacturers increasingly focus on recyclable packaging solutions. Aluminum cans are gaining wider acceptance because they can be recycled repeatedly without losing quality. Governments across Europe and North America are introducing stricter regulations related to packaging waste reduction, encouraging breweries to transition from glass and plastic packaging toward aluminum cans.

Several multinational brewing companies have announced targets to increase recycled aluminum usage in beverage cans. Craft breweries are also using sustainability-focused branding strategies to attract environmentally conscious consumers. Lightweight can designs are helping reduce transportation emissions and logistics costs. Over the long term, demand for low-carbon packaging materials and closed-loop recycling systems is expected to strengthen investment in recycled aluminum production and energy-efficient can manufacturing technologies.

Growth of Premium and Customized Can Designs

Premiumization is becoming an important trend in the beer cans market as breweries seek to improve product differentiation and consumer engagement. Beverage companies are increasingly adopting digitally printed cans, matte textures, embossed graphics, and limited-edition packaging designs to strengthen shelf visibility. Customized cans are particularly popular among craft beer manufacturers that rely on branding and visual identity to compete in crowded retail environments.

For example, regional breweries in the United States and Europe frequently launch seasonal beer collections using high-definition printed cans with unique artwork and promotional content. Smart packaging technologies such as QR codes are also being integrated into beer cans to support digital marketing campaigns and customer interaction. In the coming years, advancements in digital printing and automated decoration technologies are expected to improve production flexibility and encourage greater adoption of customized packaging formats.

Market Drivers

Expansion of Craft Breweries and Premium Beer Consumption

The rapid expansion of craft breweries is a major driver supporting the growth of the beer cans market. Independent beer producers are increasingly choosing can packaging because it provides lower transportation costs, improved durability, and better product preservation compared to glass bottles. Beer cans also allow breweries to experiment with creative branding and limited-edition product launches.

Consumer demand for premium beer varieties, flavored beverages, and seasonal alcoholic drinks is increasing across North America, Europe, and Asia Pacific. Craft beer producers are introducing visually attractive can packaging to strengthen product visibility in retail stores and online beverage platforms. For example, several microbreweries in the United States are using slim aluminum cans with digitally printed graphics to target younger consumers. The continued growth of artisanal and specialty beer categories is expected to support long-term demand for innovative can packaging solutions.

Increasing Demand for Convenient and Portable Beverage Packaging

The growing preference for convenient beverage packaging is another key driver influencing the beer cans market. Consumers increasingly favor lightweight, portable, and durable beverage containers for outdoor activities, travel, sports events, and social gatherings. Beer cans are easier to transport and store compared to glass bottles, making them highly suitable for modern retail and e-commerce distribution channels.

The hospitality and entertainment sectors are also contributing to rising demand for canned beer products. Stadiums, music festivals, airlines, and recreational venues frequently prefer cans because they reduce breakage risks and simplify waste management. Beverage manufacturers are responding by introducing multipack can formats and resealable can technologies to improve convenience. This shift toward portable beverage consumption patterns is expected to continue supporting market growth during the forecast period.

Market Restraint

Volatility in Aluminum Prices and Supply Chain Challenges

Volatility in aluminum prices remains a major restraint affecting the beer cans market. Aluminum is the primary raw material used in beer can production, and fluctuations in metal prices significantly impact manufacturing costs. Changes in global energy prices, mining activities, trade regulations, and geopolitical conditions often create instability in aluminum supply chains.

Breweries and packaging manufacturers may face margin pressure during periods of raw material inflation, particularly smaller craft beer companies with limited purchasing power. Transportation disruptions and energy-intensive smelting operations can also increase production expenses. For example, supply chain disruptions in Europe and North America have periodically increased aluminum procurement costs for beverage can manufacturers.

Another challenge involves balancing sustainability goals with rising production costs. Although recycled aluminum reduces environmental impact, limited recycling infrastructure in some developing economies restricts material availability. Packaging companies are investing in lightweight can designs and alternative sourcing strategies to reduce cost pressure, but these investments often require substantial capital expenditure. These factors may limit rapid market expansion in cost-sensitive regions.

Market Opportunities

Expansion of Ready-to-Drink Alcoholic Beverage Categories

The growing popularity of ready-to-drink alcoholic beverages presents significant opportunities for the beer cans market. Consumers are increasingly purchasing flavored malt beverages, canned cocktails, hard seltzers, and low-alcohol drinks due to convenience and portability. Beer cans are widely preferred for these products because they offer durability, lightweight transportation, and attractive branding opportunities.

Major beverage companies are launching mixed alcoholic beverage products in slim and sleek can formats to target younger consumer groups. Retailers are also allocating additional shelf space for canned ready-to-drink beverages due to rising consumer demand. Future opportunities are expected to emerge from premium canned beverage products, low-calorie alcoholic drinks, and functional beer beverages with natural ingredients. Increasing demand from urban populations and convenience retail stores is likely to strengthen market expansion.

Growth of Sustainable and Recycled Aluminum Packaging

The increasing focus on sustainable packaging is creating long-term opportunities for the beer cans market. Governments, beverage companies, and consumers are encouraging the use of recyclable packaging materials to reduce environmental impact and landfill waste. Recycled aluminum cans require significantly lower energy consumption during manufacturing compared to primary aluminum production, making them attractive for sustainability-focused breweries.

Packaging manufacturers are investing in closed-loop recycling systems and advanced sorting technologies to improve aluminum recovery rates. Beverage companies are also promoting sustainability campaigns that highlight the recyclability of beer cans. In emerging economies, improvements in recycling infrastructure and waste collection systems are expected to increase the availability of recycled aluminum materials. These developments are likely to encourage wider adoption of eco-friendly beer can packaging solutions across global markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.5 Billion |

| Market Size in 2034 | USD 31.2 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Two-piece beer cans dominated the market and accounted for approximately 68.4% of the global market share in 2024. Their dominance is primarily attributed to cost efficiency, lightweight construction, and large-scale adoption by beverage manufacturers. Two-piece cans are widely used because they require fewer raw materials and provide better production efficiency compared to traditional multi-piece can structures. Major breweries prefer these cans for lagers, ales, flavored beers, and ready-to-drink alcoholic beverages due to their durability and compatibility with high-speed filling systems. Beverage manufacturers also benefit from improved branding flexibility through advanced printing and decoration technologies. The growing use of aluminum two-piece cans in supermarkets, convenience stores, and e-commerce beverage distribution channels continues to support segment growth. Packaging companies are investing in lightweight can walls and improved sealing technologies to reduce production costs and improve sustainability performance.

Slim cans are projected to register the fastest CAGR of 6.5% during the forecast period due to rising demand for premium and convenience-oriented beverage packaging. Slim cans are increasingly used for craft beer, hard seltzers, flavored alcoholic beverages, and energy-infused beer products because they provide a modern appearance and enhanced portability. Beverage companies are targeting younger consumers through sleek can designs and digitally printed graphics that improve shelf differentiation. Slim cans also support portion control and premium pricing strategies, making them attractive for specialty beverage categories. Packaging manufacturers are introducing recyclable slim can formats with lightweight aluminum structures to align with sustainability goals. Future growth is expected to be driven by the expansion of ready-to-drink beverages and increasing demand for visually distinctive packaging across urban retail markets.

By Material

Aluminum dominated the beer cans market with a 79.2% share in 2024 because of its high recyclability, lightweight structure, and superior protection against oxygen and light exposure. Aluminum cans are widely preferred by breweries because they help preserve beverage freshness and extend shelf life. In addition, the material offers strong compatibility with high-speed manufacturing systems and advanced printing technologies. Major beer manufacturers are increasingly adopting lightweight aluminum can designs to reduce logistics costs and improve environmental performance. Beverage companies also benefit from the ability to produce visually attractive packaging using embossing, matte coatings, and digital graphics. The rapid growth of canned craft beer and ready-to-drink alcoholic beverages is further supporting the dominance of aluminum packaging across global markets.

Recycled aluminum is expected to witness the fastest CAGR of 6.8% during the forecast period due to increasing sustainability initiatives and government regulations related to packaging waste reduction. Beverage manufacturers are increasingly incorporating recycled aluminum into can production to reduce carbon emissions and energy consumption. Several breweries in Europe and North America have announced commitments to increase recycled material content in beverage packaging over the next decade. Recycled aluminum also supports circular economy strategies because it can be reused multiple times without significant quality degradation. Packaging suppliers are investing in advanced recycling technologies and closed-loop material recovery systems to improve production efficiency. Emerging economies are expected to witness stronger growth in recycled aluminum demand as investments in waste management and recycling infrastructure continue to expand.

By End-Use

Alcoholic beverage applications accounted for nearly 84.6% of the global beer cans market in 2024, making it the dominant end-use segment. The segment benefits from rising global beer consumption, expansion of premium alcoholic beverage categories, and increasing demand for portable beverage packaging. Beer cans are extensively used for lagers, pilsners, wheat beers, flavored beer products, and low-alcohol beverages because they offer durability and improved product protection. Beverage companies are increasingly launching limited-edition canned products with customized graphics to strengthen brand visibility and attract younger consumers. Supermarkets, bars, sports venues, and convenience stores continue to drive high sales volumes for canned alcoholic beverages. In addition, the expansion of e-commerce beverage delivery services is encouraging breweries to adopt durable packaging formats that withstand transportation and storage conditions.

Craft beer packaging is expected to register the fastest CAGR of 6.7% through 2034 due to increasing consumer interest in artisanal and specialty alcoholic beverages. Independent breweries are increasingly using cans because they provide lower transportation costs, improved branding flexibility, and reduced breakage risks compared to glass bottles. Craft beer companies are investing heavily in premium can decoration technologies, including digital printing and embossed graphics, to improve shelf differentiation. Growth in local brewery tourism and specialty beverage festivals is also supporting segment expansion. Future demand is expected to rise as breweries introduce organic beer products, fruit-infused beverages, and low-calorie craft beer variants in sustainable aluminum packaging. Emerging economies are witnessing increasing adoption of craft beer culture, creating additional opportunities for innovative can packaging solutions.

Beer Cans Market Segmentations

By Type

- Two-Piece Beer Cans

- Three-Piece Beer Cans

- Slim Cans

- Standard Cans

By Material

- Aluminum

- Recycled Aluminum

- Steel

By End-User

- Alcoholic Beverages

- Craft Beer Packaging

- Non-Alcoholic Malt Beverages

- Ready-to-Drink Alcoholic Beverages

Regional Analysis

North America

North America accounted for approximately 28.4% of the global beer cans market in 2025 and is projected to expand at a CAGR of 5.0% through 2034. The region benefits from strong beer consumption, a mature beverage packaging industry, and widespread adoption of canned alcoholic beverages. Beer cans are extensively used across supermarkets, convenience stores, stadiums, and entertainment venues because they provide portability and improved product preservation. The rapid growth of craft breweries across the United States and Canada is further strengthening demand for customized can packaging. Beverage manufacturers are also increasing investments in lightweight aluminum can technologies to reduce transportation costs and support sustainability initiatives.

The United States remains the dominant country within the regional market due to its extensive craft beer industry and high consumption of canned beverages. One unique growth driver in the region is the expansion of hard seltzer and flavored malt beverage categories. Beverage companies are increasingly launching alcoholic ready-to-drink products in sleek aluminum cans targeted at younger consumers. Several breweries are adopting digital can printing technologies to support seasonal packaging campaigns and regional product launches. Canada is also witnessing increasing demand for recyclable beverage packaging due to environmental awareness and strong recycling programs.

Europe

Europe represented nearly 24.1% of the global beer cans market in 2025 and is anticipated to register a CAGR of 5.2% during the forecast period. The region benefits from strong beer production, established brewing traditions, and increasing demand for recyclable beverage packaging. European consumers are gradually shifting toward aluminum cans because of their convenience and lower environmental footprint compared to alternative packaging formats. The growth of premium and craft beer categories across Western Europe is further increasing demand for decorative and customized can designs.

Germany remains the leading country in the European market due to its large brewing industry and advanced beverage packaging infrastructure. One important growth driver is the increasing export of canned beer products across European trade markets. Breweries are expanding production of canned lagers, wheat beers, and specialty alcoholic beverages to support export demand and convenience retail growth. In addition, breweries in countries such as the United Kingdom and Belgium are adopting recycled aluminum packaging to align with sustainability regulations. Investments in energy-efficient can manufacturing and closed-loop recycling systems are expected to support regional market growth.

Asia Pacific

Asia Pacific dominated the global beer cans market with a 36.9% share in 2025 and is projected to register a CAGR of 5.9% through 2034. Rising urbanization, increasing disposable income, and expanding retail distribution networks are major factors supporting regional market growth. Countries such as China, India, Japan, South Korea, and Vietnam are witnessing increasing consumption of canned alcoholic beverages among younger consumers. Beer cans are becoming increasingly popular because they are lightweight, affordable, and suitable for convenience retail formats.

China remains the dominant country in the regional market due to its large beer production capacity and extensive beverage manufacturing industry. One unique growth driver is the expansion of modern retail and online beverage delivery platforms. Consumers in major urban centers are increasingly purchasing canned beer through digital grocery applications and convenience stores. Japanese breweries are investing in premium aluminum can technologies with improved sealing and freshness preservation features. India is also emerging as a growing market due to rising demand for premium and flavored beer products among urban consumers. Regional governments are encouraging investments in aluminum recycling infrastructure to support sustainable packaging industries.

Middle East & Africa

The Middle East & Africa accounted for approximately 5.8% of the global beer cans market in 2025 and is expected to grow at a CAGR of 5.5% through 2034. The market is supported by increasing urban populations, growth in hospitality industries, and rising demand for non-alcoholic canned malt beverages in several countries. Beverage manufacturers are expanding can production facilities to address growing retail demand and improve product shelf life in warm climatic conditions.

South Africa remains the dominant country in the regional market because of its established brewing industry and growing packaged beverage consumption. One unique growth driver is the expansion of tourism and hospitality sectors, which is increasing demand for portable beverage packaging at hotels, sporting venues, and entertainment centers. Breweries are also introducing premium canned beverage products to attract younger consumers and tourists. In Gulf countries, the demand for non-alcoholic malt beverages packaged in cans is increasing due to changing retail trends and convenience-focused consumption patterns. Investments in regional can manufacturing facilities are expected to support long-term market growth.

Latin America

Latin America held nearly 4.8% of the global beer cans market in 2025 and is projected to expand at the fastest CAGR of 6.1% during the forecast period. Increasing beer consumption, expanding retail infrastructure, and growing adoption of recyclable packaging solutions are supporting regional market expansion. Beverage manufacturers are increasingly shifting toward aluminum cans because they reduce transportation costs and improve product preservation in tropical climates. The growth of convenience stores and supermarket chains is also contributing to rising canned beverage sales.

Brazil remains the leading country in the Latin American market due to its large beer industry and strong consumer demand for affordable alcoholic beverages. One major growth driver is the increasing popularity of outdoor social events, sports tournaments, and music festivals that favor portable can packaging. Breweries are launching flavored beer variants and limited-edition canned beverages to strengthen brand differentiation. Mexico is also emerging as a major export hub for canned beer products supplied to North America. Investments in aluminum recycling infrastructure and local can manufacturing facilities are expected to support long-term regional growth.

Competitive Landscape

The beer cans market is highly competitive, with global packaging manufacturers focusing on lightweight can technologies, sustainability initiatives, and advanced printing capabilities to strengthen market presence. Companies are increasing investments in recyclable aluminum production, digital decoration technologies, and regional manufacturing expansion to address growing beverage packaging demand.

Ball Corporation remains one of the leading companies in the market due to its extensive global production network and strong focus on sustainable aluminum packaging solutions. The company has expanded its lightweight can manufacturing capabilities and invested in recycled aluminum technologies to support beverage industry sustainability targets.

Crown Holdings, Ardagh Group, CANPACK, and Toyo Seikan Group are also major market participants. These companies are focusing on capacity expansion projects, strategic partnerships with breweries, and advanced can decoration technologies to strengthen competitive positioning. Beverage can manufacturers are increasingly introducing slim cans, resealable can formats, and digitally printed packaging solutions for premium alcoholic beverage brands.

Regional manufacturers are also expanding operations in Asia Pacific and Latin America to support rising beer consumption and growing retail distribution networks. Collaborations between breweries and packaging suppliers are increasing as companies seek customized packaging solutions with improved sustainability performance and enhanced branding capabilities.

Key Players List

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group

- CANPACK Group

- Toyo Seikan Group Holdings Ltd.

- Orora Packaging Australia Pty Ltd.

- Nampak Ltd.

- CPMC Holdings Limited

- Baosteel Packaging Co., Ltd.

- Kian Joo Can Factory Berhad

- Showa Aluminum Can Corporation

- Envases Group

- Massilly Holding SAS

- Silgan Holdings Inc.

- Daiwa Can Company

- Universal Can Corporation

- GZI Industries Limited