Barrier Films Packaging Market Size and Growth

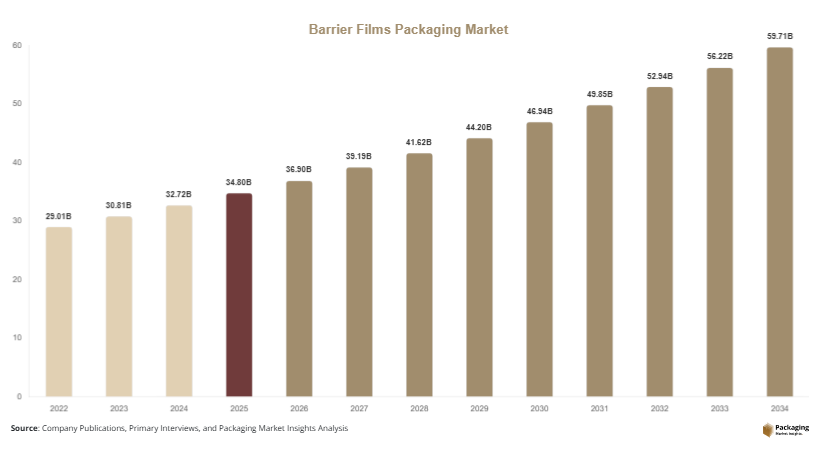

The global barrier films packaging market was valued at USD 34.8 billion in 2025 and is estimated to reach USD 36.9 billion in 2026. The market is projected to attain USD 59.7 billion by 2034, registering a CAGR of 6.2% during the forecast period from 2025 to 2034. The global barrier films packaging market is witnessing strong growth due to increasing demand for high-performance packaging solutions across food and beverage, pharmaceuticals, healthcare, personal care, agriculture, and industrial sectors. Barrier films are widely used to protect products from moisture, oxygen, light, aroma transfer, and contamination, helping extend shelf life and maintain product quality during transportation and storage.

The expansion of packaged food consumption is one of the primary growth factors driving the barrier films packaging market. Consumers are increasingly preferring convenient and ready-to-eat food products that require advanced packaging systems capable of preserving freshness and preventing spoilage. Food manufacturers are adopting multilayer barrier films for meat, dairy, frozen food, snacks, and beverage packaging to improve shelf stability and reduce food waste. Growth in modern retail and e-commerce grocery platforms is further increasing demand for protective flexible packaging solutions.

Key Market Insights

- Asia Pacific dominated the market with a 38.4% share.

- Latin America is projected to grow at the fastest CAGR of 6.8%.

- High-barrier films led the type segment with a 35.7% share.

- Plastic-based materials dominated with a 57.9% share.

- Food and beverage applications led the end-use segment with 46.2% share.

- The US remained the dominant country with a market size of USD 6.3 billion in 2025 and USD 6.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Recyclable Barrier Films

Sustainability has become a major trend shaping the barrier films packaging market as governments, consumers, and packaging manufacturers focus on reducing plastic waste and improving recyclability. Companies are increasingly developing mono-material barrier films and recyclable multilayer packaging structures that maintain product protection while simplifying recycling processes. Food and beverage brands are replacing conventional mixed-material laminates with recyclable polyethylene and polypropylene-based barrier solutions to comply with environmental regulations.

Packaging companies are also investing in compostable barrier films and bio-based coatings derived from renewable resources. For example, snack and frozen food manufacturers are introducing recyclable pouch packaging with oxygen and moisture barrier properties to improve sustainability performance. This trend is expected to accelerate over the forecast period as consumer preference for eco-friendly packaging continues to rise and regulatory authorities strengthen restrictions on non-recyclable flexible packaging products.

Growth of Smart and Functional Packaging Technologies

The integration of smart and functional packaging technologies is becoming increasingly important in the barrier films packaging market. Packaging manufacturers are introducing advanced films with antimicrobial properties, freshness indicators, and active barrier technologies designed to improve food safety and shelf-life management. Functional packaging solutions are gaining popularity in pharmaceutical and food applications where product integrity and traceability are critical.

Companies are also adopting digital printing and QR-enabled smart packaging systems that allow consumers to access product information, authentication data, and supply chain tracking details. For instance, pharmaceutical companies are implementing high-barrier blister packaging integrated with anti-counterfeiting features and tamper-evident technologies. Future advancements in intelligent packaging systems and active barrier materials are expected to create new growth opportunities across healthcare, premium food, and personal care industries.

Market Drivers

Rising Demand for Packaged and Convenience Foods

The increasing consumption of packaged and convenience food products is a major driver supporting growth in the barrier films packaging market. Urban consumers are increasingly purchasing ready-to-eat meals, frozen foods, processed snacks, and packaged dairy products that require advanced protective packaging to maintain freshness and product quality. Barrier films provide strong resistance against oxygen, moisture, and contaminants, helping manufacturers extend product shelf life and reduce spoilage.

Food manufacturers are investing heavily in multilayer flexible packaging systems to improve transportation efficiency and preserve flavor and texture during storage. The growth of organized retail chains and e-commerce grocery platforms is also increasing demand for durable and lightweight packaging materials. As disposable incomes and urban lifestyles continue to evolve globally, packaged food consumption is expected to remain a significant growth driver for barrier film packaging solutions.

Expansion of Pharmaceutical and Healthcare Industries

The rapid growth of pharmaceutical manufacturing and healthcare product distribution is significantly contributing to the barrier films packaging market. Pharmaceutical products such as tablets, capsules, medical devices, and diagnostic kits require high-barrier packaging solutions that protect against moisture, oxygen, and microbial contamination. Rising healthcare expenditure and increasing pharmaceutical exports are creating strong demand for advanced barrier packaging materials.

Healthcare companies are increasingly adopting multilayer films with superior sealing and protective properties to ensure product safety and regulatory compliance. In addition, the expansion of biologics, specialty medicines, and temperature-sensitive pharmaceutical products is supporting demand for high-performance packaging solutions. Countries such as India, Germany, and the United States are witnessing rising pharmaceutical production, which is expected to sustain long-term market growth across the healthcare packaging segment.

Market Restraint

High Production Costs and Recycling Complexity

High manufacturing costs and recycling challenges remain significant restraints affecting the barrier films packaging market. Advanced barrier films often require multilayer structures, specialized coatings, and metallized materials to achieve high moisture and oxygen resistance. These complex manufacturing processes increase production costs and create pricing pressure for packaging suppliers operating in competitive markets.

Recycling multilayer flexible packaging products also remains a major industry challenge because different material layers can be difficult to separate during waste processing. Regulatory authorities in Europe and North America are increasing pressure on manufacturers to improve packaging recyclability and reduce landfill waste. For example, food companies using aluminum-based barrier laminates may face limitations in recycling infrastructure availability and higher waste management costs. Small packaging manufacturers may struggle to invest in sustainable material innovation due to high research and development expenses. These factors can limit adoption among cost-sensitive industries and slow market penetration in developing economies.

Market Opportunities

Expansion of Bio-Based and Compostable Barrier Packaging

The growing focus on sustainable packaging is creating substantial opportunities for the barrier films packaging market. Food and beverage companies are increasingly seeking compostable and bio-based barrier packaging materials capable of maintaining product freshness while reducing environmental impact. Packaging manufacturers are developing plant-based films, biodegradable coatings, and recyclable high-barrier structures to meet evolving sustainability goals.

Retailers and consumer goods brands are also investing in environmentally responsible packaging to strengthen brand reputation and comply with corporate sustainability commitments. Future opportunities are expected to emerge from advancements in biodegradable polymers, water-based coatings, and renewable packaging feedstocks. Government incentives supporting sustainable packaging innovation are likely to accelerate commercialization and adoption of eco-friendly barrier films across multiple industries.

Growth in E-Commerce and Flexible Packaging Applications

The rapid expansion of e-commerce retail and direct-to-consumer product distribution is creating new opportunities for the barrier films packaging market. Online grocery platforms, pharmaceutical delivery services, and personal care brands require durable and lightweight packaging solutions that protect products during shipping and handling. Barrier films offer advantages such as flexibility, puncture resistance, and reduced transportation weight compared to rigid packaging alternatives.

Manufacturers are increasingly introducing customized flexible packaging solutions designed for e-commerce logistics, including stand-up pouches, resealable bags, and protective film laminates. Growth in cross-border trade and packaged consumer goods exports is also increasing demand for high-performance packaging materials capable of maintaining product integrity across long-distance supply chains. Continued investment in digital retail infrastructure and smart packaging innovation is expected to create sustained growth opportunities over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 34.8 Billion |

| Market Size in 2026 | USD 36.9 Billion |

| Market Size in 2034 | USD 59.7 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

High-barrier films accounted for the largest share of the barrier films packaging market in 2024, representing approximately 35.7% of total revenue. These films are widely used across food, pharmaceutical, and industrial packaging applications because they provide superior protection against oxygen, moisture, aroma transfer, and contamination. Food manufacturers increasingly prefer high-barrier multilayer films for meat, cheese, frozen foods, coffee, and snack packaging to extend shelf life and reduce spoilage. Pharmaceutical companies also rely on high-barrier blister films and medical packaging materials to maintain product integrity and regulatory compliance. The dominance of this segment is further supported by rising demand for lightweight flexible packaging alternatives capable of replacing rigid containers in multiple applications. Packaging manufacturers continue investing in advanced coating technologies and metallized film structures to improve performance and durability.

Biodegradable barrier films are projected to emerge as the fastest-growing type segment, registering a CAGR of 7.6% during the forecast period. Environmental concerns and regulatory restrictions on conventional plastic packaging are encouraging manufacturers to develop compostable and plant-based barrier solutions. Food and beverage companies are increasingly adopting biodegradable packaging films for snacks, bakery products, and ready-to-eat meals to improve sustainability performance and strengthen consumer trust. Packaging suppliers are investing in renewable raw materials, water-based coatings, and compostable multilayer technologies capable of maintaining oxygen and moisture resistance. Future growth is expected to be driven by stricter environmental regulations, increasing consumer preference for eco-friendly packaging, and expansion of industrial composting infrastructure across developed economies.

By Material

Plastic-based materials dominated the barrier films packaging market in 2024 with a revenue share of approximately 57.9%. Polyethylene, polypropylene, polyethylene terephthalate, and polyamide materials remain highly preferred because they provide excellent flexibility, durability, sealability, and barrier performance at competitive production costs. Plastic barrier films are widely used in food packaging, pharmaceutical blister packs, and personal care products due to their lightweight structure and compatibility with advanced printing and lamination technologies. Manufacturers favor plastic-based materials because they support high-speed packaging operations and enable development of customized multilayer packaging systems. The increasing demand for flexible packaging solutions in e-commerce and retail distribution channels is further strengthening segment dominance. Packaging companies are also introducing recyclable polyethylene-based barrier structures to improve sustainability while maintaining packaging efficiency.

Bio-based materials are expected to witness the fastest growth during the forecast period, expanding at a CAGR of 7.3% through 2034. Rising consumer awareness regarding environmental sustainability and increasing regulations targeting plastic waste are encouraging adoption of renewable packaging materials. Bio-based barrier films derived from starch, cellulose, polylactic acid, and other renewable feedstocks are gaining popularity across foodservice and consumer goods packaging applications. Packaging manufacturers are investing heavily in advanced biodegradable coatings and renewable barrier technologies to improve product performance and shelf-life protection. Future innovation in compostable polymers and recyclable bio-based laminates is expected to accelerate commercial adoption and create new growth opportunities across global packaging industries.

By End-Use

Food and beverage applications represented the dominant end-use segment in the barrier films packaging market in 2024, accounting for approximately 46.2% of overall revenue. The segment relies heavily on barrier packaging solutions for snacks, dairy products, meat, frozen foods, confectionery, and beverage packaging. Food manufacturers increasingly use multilayer barrier films to preserve freshness, extend shelf life, and prevent moisture or oxygen exposure during storage and transportation. Rising global consumption of packaged convenience foods and growth in supermarket retail distribution networks are supporting demand for advanced flexible packaging materials. Beverage companies are also adopting barrier films for liquid pouches and single-serve drink packaging to improve portability and reduce transportation costs. Increasing food exports and expansion of cold-chain logistics are expected to sustain segment growth.

Pharmaceutical packaging is expected to register the fastest CAGR of 7.1% during the forecast period. Pharmaceutical companies require high-performance barrier films for blister packs, medical pouches, and sterile healthcare packaging applications where contamination prevention is critical. Rising production of specialty medicines, biologics, and temperature-sensitive pharmaceutical products is increasing demand for advanced barrier packaging systems with superior sealing and protective properties. Packaging manufacturers are investing in multilayer medical films, child-resistant packaging technologies, and anti-counterfeiting features to meet evolving healthcare regulations. Continued growth in global pharmaceutical exports and rising healthcare expenditure are expected to create long-term growth opportunities for barrier film packaging manufacturers.

Barrier Films Packaging Market Segmentations

By Type

- High-Barrier Films

- Medium-Barrier Films

- Metallized Films

- Biodegradable Barrier Films

- Transparent Barrier Films

By Material

- Plastic-Based Materials

- Aluminum Foil

- Paper-Based Materials

- Bio-Based Materials

By End-User

- Food and Beverage

- Pharmaceuticals

- Personal Care and Cosmetics

- Agriculture

- Industrial Packaging

Regional Analysis

North America

North America accounted for approximately 23.7% of the global barrier films packaging market share in 2025 and is projected to expand at a CAGR of 5.8% during the forecast period. The regional market benefits from strong demand across packaged food, pharmaceuticals, healthcare, and personal care industries. Consumers in the United States and Canada increasingly prefer packaged convenience foods and ready-to-consume products, which is supporting demand for high-performance protective packaging solutions. Regulatory requirements related to food safety and pharmaceutical packaging standards are encouraging adoption of advanced multilayer barrier films. Growth in e-commerce grocery delivery and healthcare product distribution is also contributing to regional market expansion.

The United States remains the dominant country in North America due to its large food processing and pharmaceutical manufacturing sectors. A key growth driver in the country is the rising demand for sustainable flexible packaging solutions among consumer goods companies and retail chains. Major food brands are investing in recyclable barrier pouches and mono-material packaging systems to improve sustainability performance and reduce packaging waste. Pharmaceutical companies are also increasing the use of high-barrier blister films and medical packaging solutions to meet stricter safety standards. Ongoing investment in packaging innovation and advanced manufacturing technologies is expected to support long-term market growth.

Europe

Europe represented nearly 25.8% of the global barrier films packaging market in 2025 and is forecasted to register a CAGR of 5.9% through 2034. The regional market is driven by stringent environmental regulations, strong recycling infrastructure, and rising demand for sustainable packaging materials. Countries including Germany, France, Italy, and the United Kingdom are witnessing increased adoption of recyclable flexible packaging solutions across food and healthcare industries. Food manufacturers are increasingly using high-barrier films to extend product shelf life and reduce food waste across retail distribution networks.

Germany dominates the European market due to its advanced packaging manufacturing capabilities and strong pharmaceutical industry presence. One unique growth driver in the country is the rapid adoption of circular economy practices in flexible packaging production. Packaging companies are investing in recyclable mono-material barrier structures and solvent-free coating technologies to improve sustainability performance. In addition, Germany’s growing exports of processed food products and pharmaceutical formulations are increasing demand for high-performance barrier packaging solutions. Continued investment in sustainable materials and packaging automation is expected to strengthen regional market growth.

Asia Pacific

Asia Pacific held the largest share of the barrier films packaging market at 38.4% in 2025 and is expected to register a CAGR of 6.6% during the forecast period. Rapid urbanization, rising packaged food consumption, and expansion of pharmaceutical manufacturing are major factors supporting market growth across the region. Countries such as China, India, Japan, South Korea, and Indonesia are witnessing increasing demand for flexible packaging solutions used in snacks, dairy products, frozen foods, and healthcare products. The growth of organized retail and e-commerce grocery platforms is also increasing adoption of advanced barrier film packaging.

China remains the dominant country in Asia Pacific due to its large-scale packaging manufacturing industry and expanding consumer goods sector. A major growth driver in the country is the rapid expansion of packaged food exports and convenience food consumption among urban consumers. Packaging manufacturers are investing in high-speed film production lines, recyclable multilayer technologies, and lightweight flexible packaging systems to improve operational efficiency and export competitiveness. India is also emerging as a strong market due to rising pharmaceutical production and increasing adoption of packaged food products. Continued industrialization and retail modernization are expected to sustain long-term regional demand.

Middle East & Africa

The Middle East & Africa accounted for approximately 6.3% of the global barrier films packaging market share in 2025 and is projected to grow at a CAGR of 6.0% during the forecast period. Expanding food imports, pharmaceutical distribution networks, and retail modernization are supporting demand for advanced packaging materials across the region. Gulf countries are witnessing increasing consumption of packaged food and beverage products, driving adoption of moisture-resistant and oxygen-barrier packaging films. The healthcare sector is also contributing to demand for pharmaceutical blister packaging and sterile medical packaging materials.

Saudi Arabia dominates the regional market due to the rapid expansion of food processing industries and healthcare investments. One unique growth driver is the increasing establishment of local packaged food manufacturing facilities aimed at reducing dependence on imported consumer goods. Packaging suppliers are benefiting from rising demand for flexible packaging solutions capable of preserving food quality under high-temperature transportation conditions. In Africa, South Africa is witnessing increasing adoption of barrier packaging for dairy products, snacks, and healthcare products. Investments in cold-chain logistics and modern retail infrastructure are expected to support continued regional market growth.

Latin America

Latin America represented approximately 5.8% of the global barrier films packaging market in 2025 and is expected to witness the fastest CAGR of 6.8% during the forecast period. The regional market is benefiting from rising consumption of packaged foods, expansion of retail chains, and increasing pharmaceutical distribution activities. Countries such as Brazil, Mexico, and Argentina are experiencing growth in processed food manufacturing and convenience food sales, increasing demand for protective flexible packaging solutions. The expansion of e-commerce retail and supermarket networks is also contributing to higher usage of multilayer barrier films.

Brazil remains the dominant country in Latin America due to its large food processing industry and growing packaged consumer goods market. One important growth driver is the increasing demand for flexible packaging solutions used in frozen foods, snacks, and beverage products. Packaging manufacturers are expanding regional production facilities and investing in sustainable film technologies to improve service capabilities for food and healthcare companies. Mexico is also witnessing rising adoption of pharmaceutical blister packaging due to increasing healthcare investments. Continued retail modernization and urbanization are expected to support long-term market expansion across Latin America.

Competitive Landscape

The barrier films packaging market is highly competitive, with global manufacturers focusing on material innovation, sustainability initiatives, and strategic capacity expansion to strengthen market presence. Leading companies are investing in recyclable multilayer structures, bio-based packaging materials, and high-performance coating technologies to meet evolving regulatory standards and consumer preferences. Product differentiation through improved oxygen and moisture barrier performance remains a key competitive strategy across food, pharmaceutical, and industrial applications.

Amcor plc is recognized as a leading company in the market due to its broad flexible packaging portfolio, global manufacturing footprint, and strong investment in sustainable packaging innovation. The company continues to develop recyclable barrier films and lightweight flexible packaging systems aimed at reducing environmental impact while maintaining product protection. Other major players are expanding manufacturing facilities in Asia Pacific and Latin America to capitalize on rising packaged food and pharmaceutical demand.

Several companies are also focusing on smart packaging technologies integrated with freshness indicators, antimicrobial coatings, and digital printing capabilities. Strategic partnerships with food manufacturers, healthcare companies, and retail brands are helping packaging suppliers strengthen long-term customer relationships and improve product development capabilities. Sustainability-focused investments and advanced material research are expected to remain central competitive priorities throughout the forecast period.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Mondi Group

- Huhtamaki Oyj

- Coveris Holdings S.A.

- Winpak Ltd.

- Constantia Flexibles

- UFlex Limited

- Toray Industries Inc.

- Jindal Poly Films Ltd.

- Toppan Holdings Inc.

- Cosmo Films Ltd.

- Mitsubishi Chemical Group Corporation

- Dupont de Nemours Inc.

- ProAmpac LLC