Bag In Box Packaging Market Size and Growth

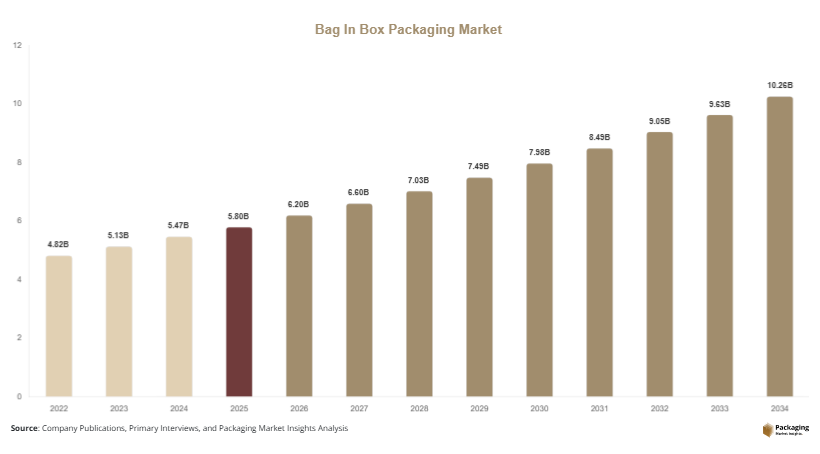

The global bag in box packaging market market was valued at approximately USD 5.8 billion in 2025 and is projected to reach USD 6.2 billion in 2026. By 2034, the market is expected to attain nearly USD 10.9 billion, registering a CAGR of 6.5% during 2025–2034. Bag-in-box packaging systems consist of a flexible inner bag placed within a rigid outer box, providing lightweight, durable, and space-efficient packaging for liquid and semi-liquid products. These packaging systems are widely used across food & beverage, chemicals, household products, dairy, edible oils, and industrial applications. The bag in box packaging market is experiencing steady expansion due to rising demand for cost-efficient bulk packaging, increasing adoption in beverage applications, and growing preference for sustainable packaging solutions.

One of the major growth factors supporting the bag in box packaging market is the rising demand for sustainable and recyclable packaging formats. Bag-in-box solutions reduce plastic consumption compared to rigid containers and offer better transportation efficiency due to their lightweight structure. Another significant growth driver is the expanding consumption of beverages such as wine, fruit juices, dairy products, and liquid concentrates. Beverage manufacturers increasingly prefer bag-in-box packaging because it extends shelf life, minimizes contamination risks, and improves dispensing convenience. In addition, the growing foodservice industry is creating strong demand for bulk liquid packaging systems for syrups, sauces, and beverage concentrates.

Key Highlights

- Europe dominated the market with a 34.2% share in 2025,.

- Latin America is projected to grow at the fastest CAGR of 7.4%.

- Standard bag-in-box systems led the type segment with a 46.5% share.

- Plastic materials dominated the market with a 57.1% share.

- Food & beverage applications led the segment with 61.3% share.

- The US remained the dominant country with a market size of USD 1.4 billion in 2025 and USD 1.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Aseptic Bag-In-Box Packaging Solutions

The increasing demand for extended shelf-life products is accelerating the adoption of aseptic bag-in-box packaging systems across dairy, beverage, and liquid food industries. Manufacturers are investing in advanced aseptic filling technologies that reduce contamination risks while preserving product quality without refrigeration. Beverage companies are increasingly using aseptic bag-in-box systems for juices, wine, and liquid concentrates due to their ability to maintain freshness during transportation and storage. For example, foodservice operators are adopting aseptic syrup dispensers and beverage concentrate systems to improve hygiene and operational efficiency. Future growth is expected to be supported by increasing demand for preservative-free liquid products and the expansion of cold-chain independent distribution systems in emerging markets.

Development of Recyclable and Mono-Material Packaging Structures

Sustainability concerns are encouraging manufacturers to develop recyclable and mono-material bag-in-box packaging formats. Traditional multilayer plastic films can be difficult to recycle, leading packaging producers to introduce simplified structures with improved recyclability. Several packaging companies are replacing mixed-material barrier layers with polyethylene-based mono-material films compatible with existing recycling systems. For instance, wine and edible oil producers are increasingly adopting recyclable bag-in-box packaging to reduce packaging waste and meet sustainability targets. Future market growth is likely to benefit from innovations in barrier coatings and bio-based polymers that improve recyclability while maintaining product protection. These developments are expected to strengthen the environmental profile of bag-in-box packaging solutions globally.

Market Drivers

Increasing Demand for Cost-Efficient Bulk Liquid Packaging

The growing need for economical and lightweight packaging solutions is a major factor driving the bag in box packaging market. Compared to rigid plastic or metal containers, bag-in-box systems reduce transportation costs, storage space requirements, and packaging waste. Foodservice providers, beverage manufacturers, and industrial chemical suppliers are increasingly using bag-in-box packaging for bulk liquid distribution. For example, restaurants and cafés commonly use syrup and beverage concentrate dispensers in bag-in-box formats to improve handling efficiency and reduce operational costs. This cost advantage is encouraging wider adoption across commercial and industrial sectors, particularly among companies seeking optimized logistics and reduced packaging material consumption.

Expansion of Beverage and Dairy Industries

Rapid growth in global beverage and dairy consumption is significantly contributing to demand for bag-in-box packaging solutions. Wine, fruit juice, flavored milk, liquid eggs, and dairy concentrate manufacturers are increasingly adopting bag-in-box systems because they improve product preservation and dispensing convenience. The packaging format also minimizes oxygen exposure, helping maintain product quality after opening. For example, wineries in Europe and North America are increasingly offering premium wines in bag-in-box packaging for retail and hospitality applications. The expanding foodservice and quick-service restaurant industries are further increasing demand for large-volume beverage dispensing systems, supporting sustained market growth.

Market Restraint

Limited Consumer Perception for Premium Product Packaging

One of the primary restraints affecting the bag in box packaging market is the limited consumer perception of bag-in-box packaging as a premium packaging format. While the packaging system provides functional and economic benefits, some consumers continue associating it with low-cost or lower-quality products, particularly in wine and specialty beverage categories. Premium beverage brands may hesitate to adopt bag-in-box formats due to concerns regarding brand positioning and shelf appeal. In addition, certain multilayer film structures used in bag-in-box packaging remain difficult to recycle in regions lacking advanced waste management infrastructure. For example, luxury beverage manufacturers often prefer glass bottles despite higher transportation costs because they are perceived as more premium by consumers. These perception-related challenges could limit adoption in certain high-end retail applications.

Market Opportunities

Growth of E-Commerce and Home Beverage Dispensing Systems

The expansion of e-commerce grocery delivery and home beverage dispensing solutions is creating strong opportunities for the bag in box packaging market. Consumers are increasingly purchasing bulk liquid products such as juices, cocktails, dairy products, and cleaning solutions through online retail channels. Bag-in-box packaging provides lightweight transportation, leak resistance, and efficient storage, making it highly suitable for direct-to-consumer delivery systems. Several beverage companies are also introducing compact home dispensing units compatible with bag-in-box packaging formats. Future opportunities are expected to emerge from smart dispensing systems integrated with automated refill technologies and digital inventory tracking for commercial and residential applications.

Increasing Adoption in Industrial and Chemical Applications

Industrial and chemical sectors are creating new growth opportunities for bag-in-box packaging manufacturers. The packaging format is increasingly used for lubricants, cleaning agents, paints, and liquid chemicals because it reduces contamination risks and improves transportation efficiency. Manufacturers are developing high-barrier liners and chemical-resistant dispensing systems designed for industrial liquid handling applications. For example, automotive lubricant suppliers are increasingly adopting bag-in-box packaging to reduce packaging waste and improve storage convenience. Future growth opportunities are expected to emerge from industrial automation systems that integrate bulk liquid dispensing with smart packaging technologies. Rising demand for safe and efficient industrial packaging solutions is likely to support broader adoption across manufacturing sectors.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.8 Billion |

| Market Size in 2026 | USD 6.2 Billion |

| Market Size in 2034 | USD 10.9 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Standard bag-in-box systems dominated the market in 2024, accounting for approximately 46.5% of the global market share. These packaging systems are widely used across beverages, edible oils, syrups, and household liquid products due to their affordability and operational simplicity. Standard bag-in-box solutions provide efficient dispensing, reduced product wastage, and lightweight transportation compared to rigid containers. Foodservice operators and beverage companies prefer these systems because they improve storage efficiency while lowering logistics costs. In addition, manufacturers are improving tap dispensing technologies and multilayer film barriers to enhance shelf life and reduce leakage risks. The broad commercial adoption of standard bag-in-box packaging across retail and industrial applications continues to support segment dominance globally.

Aseptic bag-in-box systems are projected to be the fastest-growing subsegment, registering a CAGR of 7.8% during the forecast period. Aseptic packaging technologies are increasingly used for dairy products, liquid eggs, fruit concentrates, and pharmaceutical liquids because they extend product shelf life without refrigeration. Manufacturers are investing in sterile filling systems and high-barrier packaging films to improve contamination protection and product quality. Several food processing companies are adopting aseptic bag-in-box solutions to support long-distance transportation and export operations. Future growth opportunities are expected to emerge from plant-based beverage packaging and temperature-sensitive healthcare applications. Rising demand for preservative-free liquid products is anticipated to strengthen adoption of aseptic packaging technologies worldwide.

By Material

Plastic materials held the dominant market share of 57.1% in 2024 due to their durability, flexibility, and barrier protection capabilities. Polyethylene and multilayer plastic films are widely used in bag-in-box packaging because they provide strong oxygen and moisture resistance while maintaining lightweight properties. Beverage manufacturers and industrial liquid suppliers rely on plastic liners to preserve product quality and prevent leakage during transportation. In addition, advancements in recyclable plastic film technologies are supporting broader adoption of sustainable plastic packaging formats. Manufacturers are increasingly introducing mono-material polyethylene liners compatible with recycling systems to improve environmental performance. These developments continue supporting strong demand for plastic-based bag-in-box packaging across global commercial and industrial sectors.

Paperboard materials are expected to witness the fastest growth, expanding at a CAGR of 7.2% during the forecast period. Corrugated paperboard outer boxes are gaining popularity because they improve packaging sustainability and provide strong structural protection during shipping and storage. Foodservice providers and beverage companies are increasingly adopting recyclable paperboard packaging to reduce plastic consumption and improve brand sustainability image. Several packaging manufacturers are also introducing lightweight paperboard structures designed for automated filling and dispensing systems. Future market growth is expected to benefit from increasing investments in renewable fiber packaging technologies and recyclable packaging innovations. Rising environmental regulations regarding packaging waste are likely to accelerate demand for paperboard-based packaging systems globally.

By End-Use

Food & beverage dominated the end-use segment in 2024, accounting for approximately 61.3% of the global bag in box packaging market share. The segment benefits from widespread use of bag-in-box packaging for wine, dairy products, fruit juices, sauces, and beverage syrups. Foodservice companies and beverage manufacturers prefer the packaging format because it improves dispensing convenience, extends product freshness, and reduces transportation costs. In addition, rapid growth in online grocery retail and institutional catering operations is increasing demand for bulk liquid packaging systems. Beverage dispensing systems used in restaurants, cinemas, and cafés are further supporting segment growth. Continuous innovation in aseptic packaging and recyclable barrier films is expected to strengthen adoption across the food & beverage industry.

Pharmaceutical applications are anticipated to be the fastest-growing end-use segment, registering a CAGR of 7.6% during the forecast period. Pharmaceutical manufacturers are increasingly using aseptic bag-in-box systems for liquid medicines, chemical intermediates, and sterile healthcare products. These packaging formats help reduce contamination risks while improving transportation efficiency and storage performance. Several healthcare packaging companies are developing high-barrier dispensing systems designed for sensitive pharmaceutical liquids and temperature-controlled products. Future opportunities are expected to emerge from biotechnology applications and hospital liquid dispensing systems. The growing focus on efficient healthcare supply chains and sustainable medical packaging solutions is likely to support broader adoption of bag-in-box packaging within pharmaceutical industries.

Bag In Box Packaging Market Segmentations

By Type

- Standard Bag-In-Box Systems

- Aseptic Bag-In-Box Systems

- Tap Dispensing Systems

- Custom Industrial Bag-In-Box Packaging

By Material

- Plastic

- Paperboard

- Aluminum Barrier Films

- Composite Materials

By End-User

- Food & Beverage

- Pharmaceuticals

- Household Products

- Industrial Liquids

- Chemicals & Lubricants

Regional Analysis

North America

North America accounted for approximately 26.8% of the global bag in box packaging market share in 2025 and is projected to expand at a CAGR of 6.1% during the forecast period. The region benefits from strong demand for beverage dispensing systems, advanced foodservice infrastructure, and increasing adoption of sustainable bulk packaging formats. Beverage producers, restaurants, and dairy companies across the United States and Canada are increasingly using bag-in-box systems to reduce packaging waste and improve transportation efficiency. Growth in institutional foodservice operations and rising demand for liquid concentrate packaging are also supporting market expansion. In addition, packaging manufacturers are investing in recyclable liners and automated filling systems to improve sustainability performance and operational efficiency across commercial applications.

The United States dominates the North American market due to its large beverage and foodservice industries. One unique growth driver is the increasing adoption of bag-in-box packaging within quick-service restaurant chains and cinema beverage dispensing systems. Several restaurant operators are transitioning toward large-capacity beverage syrup dispensers to reduce labor costs and improve operational efficiency. In addition, the expansion of home beverage systems and direct-to-consumer liquid product subscriptions is supporting demand for compact bag-in-box packaging formats. These trends are expected to strengthen market growth across the country during the forecast period.

Europe

Europe held the largest regional market share of 34.2% in 2025 and is expected to grow at a CAGR of 6.4% through 2034. The region has a well-established wine industry and strong demand for sustainable packaging solutions, making bag-in-box packaging widely accepted across beverage applications. Food manufacturers and beverage companies are increasingly adopting recyclable and lightweight packaging formats to comply with environmental regulations and reduce carbon emissions from transportation. The hospitality sector and retail beverage distribution networks are also contributing to growing demand for bag-in-box systems. Furthermore, technological advancements in aseptic filling and barrier film production are improving packaging performance across dairy and liquid food applications.

France remains the dominant country within the European market due to its strong wine production and export industries. A distinctive growth factor is the increasing use of premium bag-in-box wine packaging for retail and hospitality distribution. French wineries are adopting advanced oxygen-barrier bag technologies that improve wine preservation and shelf life while reducing transportation costs compared to glass bottles. Several supermarket chains are also expanding private-label wine products packaged in bag-in-box formats. These developments are expected to support sustained demand across France and neighboring European markets.

Asia Pacific

Asia Pacific represented approximately 29.7% of the global bag in box packaging market share in 2025 and is projected to register a CAGR of 7.1% through 2034. Rapid urbanization, rising consumption of packaged beverages, and expansion of foodservice industries are supporting regional market growth. Countries such as China, India, Japan, and South Korea are witnessing increasing demand for efficient bulk liquid packaging systems across dairy, edible oils, and beverage applications. The rise of modern retail channels and e-commerce grocery platforms is also increasing demand for lightweight and space-efficient packaging formats. In addition, packaging manufacturers are investing in regional production facilities to support growing demand for aseptic and recyclable bag-in-box solutions.

China dominates the Asia Pacific market due to its large food processing sector and expanding beverage industry. One unique growth driver is the rapid growth of tea concentrate and ready-to-drink beverage distribution systems. Beverage companies in China are increasingly adopting bag-in-box packaging for cafés, bubble tea chains, and institutional foodservice operations because it improves storage efficiency and dispensing convenience. The country is also witnessing rising adoption of aseptic liquid packaging systems for dairy and plant-based beverages. These trends are expected to sustain strong regional market growth during the forecast period.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.1% of the global bag in box packaging market share in 2025 and is anticipated to expand at a CAGR of 5.8% through 2034. Growing hospitality industries, increasing tourism activity, and rising demand for bulk beverage dispensing systems are supporting regional market growth. Hotels, restaurants, and catering businesses across Gulf countries are increasingly adopting bag-in-box packaging for juices, syrups, and liquid food concentrates. In addition, rising investments in food processing and industrial manufacturing are contributing to growing demand for liquid packaging systems. Packaging suppliers are also introducing heat-resistant and durable bag-in-box solutions designed for high-temperature transportation conditions within the region.

Saudi Arabia remains the dominant country within the Middle East & Africa market due to expanding foodservice and hospitality infrastructure. A key growth factor is the increasing use of bag-in-box packaging for large-scale catering and institutional beverage operations. Hotels and event management companies are increasingly adopting bulk beverage dispensing systems to reduce packaging waste and improve operational efficiency. Several dairy manufacturers are also using aseptic bag-in-box packaging for long shelf-life milk and liquid dairy products. These developments are expected to strengthen regional demand during the forecast period.

Latin America

Latin America represented approximately 5.2% of the global bag in box packaging market share in 2025 and is projected to register the fastest CAGR of 7.4% during the forecast period. Rising packaged beverage consumption, expanding wine production, and increasing adoption of sustainable packaging are supporting regional market growth. Countries such as Brazil, Argentina, and Chile are witnessing growing demand for bag-in-box systems across wine, edible oils, and fruit juice applications. The region’s food export industry is also increasing the use of lightweight liquid packaging formats to improve logistics efficiency and reduce shipping costs. Furthermore, retail expansion and urbanization are supporting broader adoption of packaged food and beverage products.

Brazil dominates the Latin American market due to its large beverage processing industry and expanding retail sector. One unique growth driver is the increasing use of bag-in-box packaging for tropical fruit juice distribution and institutional beverage supply chains. Beverage companies are adopting high-capacity dispensing systems for hotels, schools, and restaurants to improve operational convenience and reduce packaging waste. In addition, the expansion of supermarket private-label beverage brands is increasing demand for affordable and sustainable liquid packaging solutions. These factors are expected to support continued market growth across Brazil and neighboring countries.

Competitive Landscape

The bag in box packaging market is moderately competitive, with companies focusing on sustainable material innovation, aseptic packaging technologies, and strategic partnerships to strengthen market presence. Smurfit Kappa Group remains one of the leading players due to its extensive product portfolio and strong presence across beverage and industrial packaging applications. The company recently expanded its recyclable bag-in-box packaging solutions designed for wine and foodservice industries.

Other major companies operating in the market include DS Smith Plc, Scholle IPN, Liquibox, and Amcor plc. These companies are investing in advanced dispensing systems, barrier film technologies, and sustainable packaging materials to meet evolving industry requirements. Strategic collaborations with beverage manufacturers, foodservice operators, and industrial liquid suppliers are becoming increasingly common. Packaging companies are also expanding automated filling infrastructure and regional production facilities to strengthen supply chain efficiency. Growing demand for sustainable and lightweight liquid packaging solutions is expected to intensify competition across the global market during the forecast period.

Key Players List

- Smurfit Kappa Group

- DS Smith Plc

- Scholle IPN

- Liquibox

- Amcor plc

- CDF Corporation

- Arlington Packaging

- Parish Manufacturing Inc.

- Optopack Ltd

- TPS Rental Systems Ltd

- Vine Valley Ventures LLC

- Central Package & Display

- Accurate Box Company

- IC Packaging

- Arlington Packaging Ltd