Automotive Thermoformed Plastic Parts Packaging Market Size and Growth

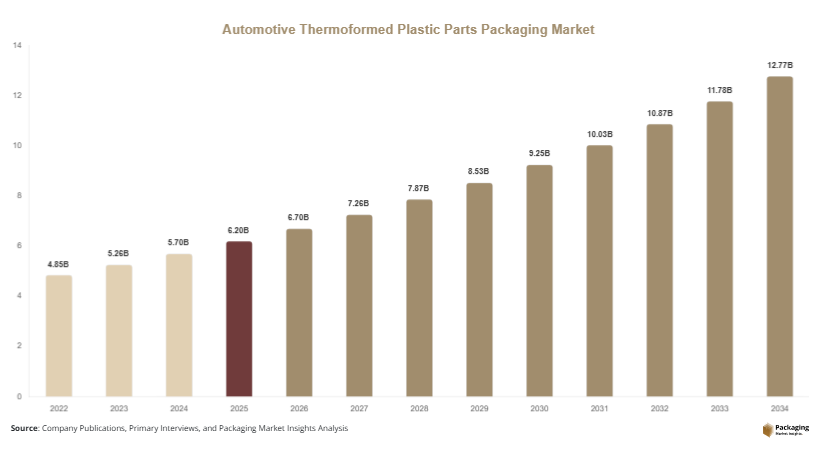

The global automotive thermoformed plastic parts packaging market is estimated at USD 6.2 billion in 2025, and it is projected to reach USD 6.7 billion in 2026. By 2034, the market is expected to reach approximately USD 12.9 billion, registering a CAGR of 8.4% (2025–2034). Growth is primarily driven by increasing automotive manufacturing volumes, expansion of electric vehicle (EV) production, and rising demand for customized packaging solutions in global supply chains.

The automotive thermoformed plastic parts packaging market is a specialized segment within the automotive packaging industry, focused on protective, lightweight, and precision-molded packaging solutions used for transporting and storing automotive components. These thermoformed plastic packaging solutions are widely used for engine parts, electronic control units, interior components, fasteners, sensors, and other precision automotive assemblies. The market is gaining traction due to increasing automotive production, rising demand for lightweight logistics solutions, and the growing need for damage-free transportation of high-value automotive parts across global supply chains.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Thermoformed trays led the type segment with a 33.8% share.

- Polypropylene (PP) based packaging dominated with a 52.1% share.

- Automotive OEMs led the segment with 45.7% share.

- The US remained the dominant country with a market size of USD 2.3 billion in 2025 and USD 2.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Returnable and Reusable Packaging Systems

A major trend in the automotive thermoformed plastic parts packaging market is the shift toward returnable and reusable packaging systems. Automotive manufacturers are increasingly adopting closed-loop packaging solutions that reduce waste and improve cost efficiency over multiple logistics cycles. For example, major automotive OEMs in Germany and Japan are implementing reusable thermoformed trays for engine components and transmission parts, which are collected, cleaned, and reused across supply chains. This approach not only reduces packaging waste but also lowers long-term procurement costs. In the future, digital tracking systems such as RFID-enabled reusable packaging will further enhance efficiency by enabling real-time monitoring of packaging assets across global automotive supply chains.

Rising Use of Anti-Static and Precision-Molded Packaging for EV Components

Another key trend is the increasing demand for anti-static and precision-molded thermoformed packaging solutions, particularly driven by electric vehicle manufacturing. EV components such as battery cells, control modules, and electronic sensors require high-precision packaging to prevent electrostatic discharge and mechanical damage. For instance, EV manufacturers in China and the United States are using custom thermoformed trays with conductive materials to ensure safe handling of sensitive parts. As EV production continues to expand globally, demand for specialized protective packaging solutions will increase, driving innovation in material science and design engineering within the thermoforming industry.

Market Drivers

Expansion of Automotive Production and Global Supply Chains

The continuous expansion of global automotive production is a major driver of the automotive thermoformed plastic parts packaging market. Increasing vehicle manufacturing volumes in Asia Pacific, Europe, and North America are creating strong demand for efficient logistics and packaging systems. Automotive parts often move across multiple countries before final assembly, requiring durable packaging that ensures product safety during transportation. For example, Tier 1 suppliers in Mexico export engine components to the United States, relying heavily on thermoformed plastic trays for protection and organization. This growing cross-border automotive supply chain is significantly boosting market demand.

Growth of Electric Vehicle Manufacturing

Another key driver is the rapid expansion of electric vehicle production worldwide. EVs require specialized components that are more sensitive than traditional automotive parts, increasing the need for advanced protective packaging. For instance, lithium-ion battery modules require anti-static and shock-resistant thermoformed packaging solutions to prevent damage during transport. Automotive companies in Europe and China are investing heavily in EV production facilities, leading to increased demand for customized packaging solutions. As EV adoption accelerates globally, packaging manufacturers are developing innovative materials and designs tailored to EV-specific requirements.

Market Restraint

High Dependency on Plastic Raw Materials and Environmental Regulations

One of the major restraints in the automotive thermoformed plastic parts packaging market is its dependency on plastic-based raw materials, which are subject to price volatility and environmental scrutiny. Fluctuations in petrochemical prices directly impact production costs, affecting profitability for packaging manufacturers. Additionally, increasing environmental regulations in Europe and North America are restricting the use of non-recyclable plastics. Automotive companies are under pressure to reduce plastic waste, which limits the adoption of conventional thermoformed packaging solutions. For example, several European OEMs are transitioning to recyclable or bio-based alternatives, increasing compliance costs and requiring reengineering of packaging systems.

Market Opportunities

Development of Sustainable and Bio-Based Thermoformed Packaging Materials

The growing focus on sustainability presents a significant opportunity for the automotive thermoformed plastic parts packaging market. Manufacturers are increasingly investing in bio-based and recyclable thermoformed materials to reduce environmental impact. For example, packaging companies in Europe are developing plant-based plastic alternatives for automotive trays and protective packaging systems. These materials offer similar durability and performance while reducing carbon emissions. In the future, regulatory pressure and corporate sustainability goals are expected to accelerate the adoption of eco-friendly thermoformed packaging across global automotive supply chains.

Expansion of Aftermarket Automotive Parts Distribution

The rapid growth of the automotive aftermarket industry presents another major opportunity for thermoformed packaging solutions. Replacement parts such as filters, brake components, and electronic modules require secure packaging for distribution across retail and service networks. For instance, aftermarket suppliers in the United States and India are increasingly using customized thermoformed trays to ensure product protection during long-distance shipping. As global vehicle fleets expand and maintenance demand rises, the need for efficient aftermarket packaging solutions is expected to grow significantly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.2 Billion |

| Market Size in 2026 | USD 6.7 Billion |

| Market Size in 2034 | USD 12.9 Billion |

| CAGR | 8.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Thermoformed trays dominated with a 33.8% share in 2024, due to their widespread use in organizing and protecting automotive components during transport. These trays are extensively used for engine parts, fasteners, and electronic modules. Automotive OEMs prefer trays for their customization flexibility and durability.

Multi-layer protective packaging is the fastest-growing segment with a CAGR of 6.9%, driven by increasing demand for enhanced protection of high-value EV components. These systems offer shock resistance and anti-static properties, making them ideal for sensitive electronics.

By Material

Polypropylene (PP) dominated with a 52.1% share in 2024, due to its durability, cost efficiency, and recyclability. It is widely used in automotive logistics for reusable packaging systems.

Bio-based thermoformed plastics are the fastest-growing segment with a CAGR of 6.5%, driven by sustainability initiatives and regulatory pressure. Automotive companies are increasingly adopting eco-friendly materials to reduce environmental impact.

By End-Use

Automotive OEMs dominated with a 45.7% share in 2024, due to their large-scale production and complex supply chain requirements. OEMs require customized packaging for assembly line efficiency.

EV component packaging is the fastest-growing segment with a CAGR of 7.4%, driven by rapid EV production and the need for specialized protective packaging for battery systems and electronics.

Automotive Thermoformed Plastic Parts Packaging Market Segmentations

By Type

- Thermoformed Trays

- Clamshell Packaging

- Blister Packaging

- Multi-Layer Protective Packaging

- Returnable Packaging Systems

By Material

- Polypropylene (PP)

- Polyethylene (PE)

- Polystyrene (PS)

- Bio-Based Thermoplastics

- Recycled Plastic Materials

By End-Use

- Automotive OEMs

- Tier 1 & Tier 2 Suppliers

- Electric Vehicle Manufacturers

- Aftermarket Parts Suppliers

- Logistics & Warehousing Providers

Regional Analysis

North America

North America accounted for 28.6% market share in 2025, with a CAGR of 7.9%. The region benefits from strong automotive manufacturing infrastructure, high EV adoption, and advanced logistics systems. Demand for thermoformed packaging is driven by OEMs and Tier 1 suppliers requiring precision packaging solutions.

The United States dominates the region due to its large automotive production and supply chain network. A key growth driver is the expansion of EV manufacturing hubs in states like Michigan and Texas. For example, U.S.-based EV manufacturers are increasingly using anti-static thermoformed trays for battery component logistics.

Europe

Europe held 24.8% market share in 2025, with a CAGR of 7.6%. The region is driven by strong automotive engineering capabilities, sustainability regulations, and high-quality packaging standards. Demand for reusable and recyclable packaging is increasing.

Germany leads the region due to its strong automotive manufacturing base. A key driver is the adoption of closed-loop packaging systems used by automotive OEMs. For instance, German automakers use returnable thermoformed trays for cross-border component shipments within the EU.

Asia Pacific

Asia Pacific dominated with 37.4% market share in 2025, and is projected to grow at a CAGR of 9.2%. Rapid automotive production, EV expansion, and large-scale manufacturing infrastructure are key drivers.

China remains the dominant country due to its massive automotive and EV production ecosystem. A key driver is the integration of thermoformed packaging in large-scale EV battery manufacturing facilities, ensuring safe logistics across domestic and export markets.

Middle East & Africa

The region accounted for 5.7% market share in 2025, with a CAGR of 6.8%. Growth is driven by increasing automotive imports, expansion of assembly plants, and rising demand for aftermarket services.

The UAE dominates the region due to its logistics and re-export capabilities. A key driver is the growing automotive spare parts distribution hub in Dubai, where thermoformed packaging is widely used for regional shipments.

Latin America

Latin America held 3.5% market share in 2025, with a CAGR of 6.2%, the fastest globally. Growth is driven by expanding automotive assembly plants and rising vehicle demand.

Brazil leads the region due to its strong automotive manufacturing sector. A key driver is the increasing localization of automotive component production, requiring standardized thermoformed packaging solutions for domestic and export logistics.

Competitive Landscape

The automotive thermoformed plastic parts packaging market is moderately consolidated, with key players focusing on customization, sustainability, and lightweight packaging innovation. Major companies include DS Smith Plc, Sonoco Products Company, Huhtamaki Oyj, Pactiv Evergreen Inc., and Amcor plc. Among these, DS Smith Plc leads due to its strong presence in automotive packaging solutions and closed-loop logistics systems.

Companies are investing in recyclable materials, automated thermoforming technologies, and digital packaging tracking systems. Strategic collaborations with automotive OEMs and EV manufacturers are increasing to develop customized packaging solutions that improve supply chain efficiency.

Key Players List

- DS Smith Plc

- Sonoco Products Company

- Huhtamaki Oyj

- Pactiv Evergreen Inc.

- Amcor plc

- Sealed Air Corporation

- Berry Global Inc.

- Smurfit Kappa Group

- Mondi Group

- Tekni-Plex Inc.

- Universal Protective Packaging Inc.

- Dordan Manufacturing Company

- Placon Corporation

- Nelipak Healthcare Packaging

- Encore Packaging LLC