Automotive Labeling Market Size and Growth

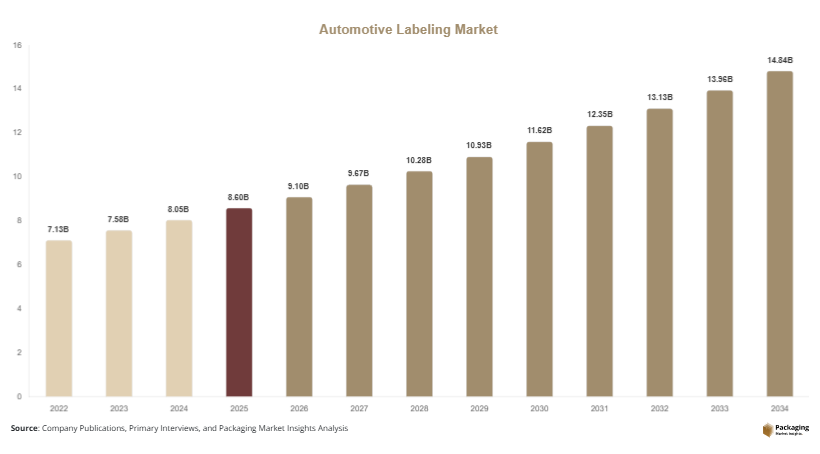

The global automotive labeling market size was valued at approximately USD 8.6 billion in 2025 and is projected to reach USD 9.1 billion in 2026. The market is forecasted to expand significantly and reach nearly USD 14.8 billion by 2034, registering a CAGR of 6.3% during 2025–2034. Rising adoption of electric vehicles, increasing automotive exports, and advancements in smart labeling technologies are major factors driving market expansion globally. Automakers are increasingly using durable labels and RFID-enabled tracking systems to improve production efficiency and vehicle lifecycle management.

The global automotive labeling market is experiencing steady growth due to rising vehicle production, increasing integration of electronic components, and growing regulatory requirements related to vehicle safety and traceability. Automotive labels are widely used across passenger vehicles, commercial vehicles, and electric vehicles for branding, warning instructions, component identification, barcode tracking, and compliance labeling. These labels are designed to withstand harsh environmental conditions including heat, moisture, chemicals, abrasion, and UV exposure, making them critical for long-term vehicle performance and regulatory adherence.

Key Highlights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.9%.

- Warning and safety labels led the type segment with a 33.8% share.

- Plastic-based labels dominated with a 54.2% share.

- Passenger vehicles led the end-use segment with 61.4% share.

- The US remained the dominant country with a market size of USD 1.9 billion in 2025 and USD 2.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of RFID and Smart Labels

One of the major trends shaping the automotive labeling market is the increasing use of RFID-enabled and smart labeling technologies across vehicle manufacturing operations. Automotive companies are integrating RFID tags and QR-based labels to improve inventory management, component tracking, and production line automation. These labels enable real-time monitoring of automotive parts throughout the supply chain and simplify vehicle maintenance and aftermarket services. For example, several automotive manufacturers in North America and Europe are using RFID labels for battery tracking and warehouse automation. Smart labels also improve anti-counterfeit protection for spare parts and critical electronic components. Future demand for connected manufacturing systems and Industry 4.0 technologies is expected to accelerate adoption of intelligent automotive labeling solutions globally.

Rising Demand for Sustainable Labeling Materials

Another important trend influencing the market is the growing demand for sustainable and recyclable labeling materials. Automotive manufacturers are increasingly focusing on reducing production waste and improving sustainability across vehicle manufacturing processes. Label suppliers are developing recyclable polyester films, solvent-free adhesives, and low-emission printing technologies to align with environmental targets. For instance, several European automotive companies are adopting eco-friendly labeling systems for electric vehicles and interior automotive applications. Sustainable labels also support lightweight vehicle manufacturing by reducing material consumption and improving recyclability. Increasing pressure from environmental regulations and sustainability initiatives is expected to encourage wider adoption of green labeling solutions across the automotive industry.

Market Drivers

Expansion of Electric Vehicle Manufacturing

The rapid growth of electric vehicle production is one of the primary drivers supporting the automotive labeling market. EVs require specialized labels for battery packs, charging ports, high-voltage systems, and electronic control units. These labels must withstand high temperatures, moisture exposure, and chemical interactions over long operating periods. As governments encourage electric mobility adoption through incentives and emissions regulations, automakers are significantly increasing EV production capacities. For example, automotive manufacturers in China, Germany, and the United States are expanding EV assembly facilities and battery manufacturing plants, increasing demand for durable industrial labeling solutions. Rising investment in battery technology and charging infrastructure is expected to further strengthen market demand for automotive labels globally.

Increasing Regulatory Requirements for Vehicle Safety

Strict government regulations related to vehicle safety and traceability are also driving strong market growth. Automotive labels play a critical role in communicating safety warnings, compliance instructions, airbag information, tire specifications, and emissions details. Regulatory authorities across North America, Europe, and Asia Pacific require manufacturers to maintain standardized labeling systems for safety certification and product identification. Automotive companies are increasingly adopting durable thermal-transfer labels and tamper-evident solutions to ensure long-term compliance. For instance, vehicle identification number labels and under-the-hood safety labels have become mandatory across several automotive markets. Continued expansion of global automotive trade and regulatory harmonization is expected to support higher demand for compliant labeling technologies.

Market Restraint

High Raw Material Costs and Adhesive Performance Challenges

One of the key restraints affecting the automotive labeling market is the rising cost of raw materials and performance limitations associated with adhesive technologies. Automotive labels require high-performance materials capable of resisting heat, chemicals, oil exposure, moisture, and abrasion throughout the vehicle lifecycle. Fluctuations in the prices of polyester films, specialty plastics, inks, and industrial adhesives can increase manufacturing costs for labeling suppliers. In addition, some labeling materials may experience adhesion failure under extreme environmental conditions such as engine heat or prolonged UV exposure. For example, labels used in electric vehicle battery systems require specialized adhesives that maintain durability despite high thermal stress. Developing long-lasting labeling solutions while controlling production costs remains a major challenge for manufacturers. Small and regional labeling suppliers may face difficulties investing in advanced material technologies and regulatory testing processes, potentially limiting market competitiveness and innovation.

Market Opportunities

Growth of Autonomous and Connected Vehicles

The increasing development of autonomous and connected vehicles presents major opportunities for the automotive labeling market. Modern vehicles incorporate advanced sensors, cameras, electronic modules, and communication systems that require detailed identification and tracking labels. Automotive manufacturers are implementing smart labels and digital tracking technologies to improve diagnostics, maintenance, and software management. Connected vehicle platforms also require durable labels for electronic systems and data management infrastructure. Countries including the United States, Japan, and South Korea are investing heavily in autonomous vehicle testing and smart mobility technologies. Future expansion of self-driving vehicle ecosystems is expected to create strong demand for high-performance automotive labeling solutions.

Expansion of Automotive Manufacturing in Emerging Economies

The rapid expansion of automotive production in emerging economies offers another significant opportunity for market growth. Countries such as India, Mexico, Thailand, and Brazil are attracting investments in vehicle assembly plants and automotive component manufacturing facilities. Rising disposable income and increasing vehicle ownership are supporting higher automotive production across these regions. Label manufacturers are establishing local production units to serve growing demand for component identification and safety labeling solutions. Increasing exports of passenger vehicles and commercial vehicles from emerging economies are also driving adoption of international labeling standards. Continued industrialization and supply chain expansion are expected to strengthen long-term opportunities for automotive labeling suppliers globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.6 Billion |

| Market Size in 2026 | USD 9.1 Billion |

| Market Size in 2034 | USD 14.8 Billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

RFID smart labels are projected to be the fastest-growing segment, registering a CAGR of 7.8% during the forecast period. Automotive manufacturers are increasingly integrating RFID-enabled labels to improve inventory tracking, production automation, and aftermarket services. These labels support real-time monitoring of vehicle components and simplify logistics management across automotive supply chains. EV battery manufacturers are particularly adopting smart labels for tracking battery modules and thermal systems during production and transportation. Countries including China, Germany, and the United States are witnessing growing deployment of smart manufacturing technologies within automotive facilities. Future expansion of Industry 4.0 systems is expected to strengthen demand for RFID automotive labels.

By Material

Plastic-based labels dominated the market in 2024 with approximately 54.2% share because of their durability, flexibility, and resistance to chemicals and heat exposure. Materials such as polyester, polypropylene, and vinyl are commonly used in automotive labels due to their ability to withstand harsh operating conditions. Plastic labels are widely utilized in engine compartments, battery systems, and under-the-hood applications where exposure to oil, moisture, and temperature fluctuations is common. Automotive manufacturers also prefer plastic-based labels because they are compatible with thermal transfer printing and high-speed production systems. Continued growth in electric vehicle manufacturing and automotive electronics is expected to maintain strong demand for durable plastic labeling materials globally.

Recyclable polyester labels are expected to emerge as the fastest-growing material segment with a CAGR of 7.1% during the forecast period. Increasing sustainability initiatives and environmental regulations are encouraging automotive manufacturers to adopt eco-friendly labeling solutions. Recyclable polyester materials provide high durability while improving recyclability and reducing industrial waste. Automotive suppliers are developing low-emission adhesives and solvent-free coatings to enhance sustainability across vehicle manufacturing operations. European automotive manufacturers are particularly investing in recyclable labels for electric vehicles and lightweight automotive systems. Rising demand for green manufacturing solutions and sustainable automotive components is expected to support long-term segment growth.

By End-Use

Passenger vehicles dominated the market in 2024 with approximately 61.4% share due to high global vehicle production and increasing integration of electronic systems. Automotive labels are extensively used across passenger vehicles for branding, compliance, component identification, and safety instructions. Rising consumer demand for connected vehicles and advanced driver assistance systems is increasing the number of labels required per vehicle. Automotive manufacturers are also implementing QR-based service labels and anti-counterfeit tracking systems for aftermarket components. Growth in vehicle ownership across emerging economies and expansion of premium passenger vehicle production are supporting continued dominance of the segment.

Electric vehicles are projected to be the fastest-growing end-use segment with a CAGR of 8.4% during the forecast period. EVs require specialized labels for battery packs, charging systems, cooling modules, and high-voltage electrical components. These labels must withstand chemical exposure, extreme temperatures, and long operational cycles. Governments worldwide are encouraging EV adoption through incentives and emissions regulations, resulting in rapid expansion of battery manufacturing facilities and EV assembly plants. Automotive labeling suppliers are increasingly developing thermal-resistant and flame-retardant label solutions for EV applications. Continued advancements in battery technology and electric mobility infrastructure are expected to drive long-term growth in the segment.

Automotive Labeling Market Segmentations

By Type

- Pressure-Sensitive Labels

- Shrink Sleeve Labels

- In-Mold Labels

- RFID Labels

- Heat Transfer Labels

By Material

- Plastic

- Paper

- Metal

- Polypropylene

- Polyester

By End-User

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Automotive Components & Spare Parts

- Logistics & Transportation

Regional Analysis

North America

North America accounted for approximately 26.8% of the global market share in 2025 and is projected to grow at a CAGR of 5.9% during the forecast period. The region benefits from strong automotive manufacturing capabilities, advanced supply chain infrastructure, and rising adoption of electric vehicles. Automotive manufacturers across the United States and Canada are increasingly using RFID-enabled labels and smart tracking systems to improve production efficiency and inventory management. Growth in electric vehicle assembly and battery manufacturing is also supporting higher demand for thermal-resistant automotive labels. In addition, strict vehicle safety regulations and product traceability requirements are encouraging adoption of durable warning and compliance labels across the automotive sector.

The United States dominates the North American market due to its advanced automotive manufacturing industry and rapid EV expansion. A unique growth driver in the country is the increasing investment in battery production and connected vehicle technologies. Automotive companies are implementing specialized labeling systems for EV battery modules, charging systems, and autonomous driving components. Several manufacturers are also integrating digital QR-based labels for vehicle maintenance and aftermarket tracking. Rising demand for connected mobility solutions and expansion of automotive software integration are expected to strengthen future market growth in the United States.

Europe

Europe represented nearly 24.9% of the market share in 2025 and is expected to expand at a CAGR of 5.8% through 2034. Strong environmental regulations, growing electric vehicle production, and advanced automotive engineering are major factors supporting regional market growth. Automotive manufacturers across Germany, France, Italy, and the United Kingdom are increasingly adopting sustainable labeling materials and digital printing technologies. The region is also witnessing rising demand for high-durability labels used in advanced driver assistance systems and electronic control modules. Growth in premium automotive manufacturing and vehicle exports continues to create demand for specialized automotive identification and compliance labels.

Germany remains the dominant country in the European automotive labeling market due to its large automotive production base and strong export activities. A unique growth driver in Germany is the rapid adoption of Industry 4.0 technologies across automotive assembly plants. Vehicle manufacturers are increasingly using automated labeling systems and RFID-enabled tracking solutions to improve manufacturing accuracy and supply chain visibility. German automotive companies are also investing in sustainable labeling materials to align with carbon reduction targets. Continued innovation in electric mobility and connected manufacturing is expected to support long-term market growth in Germany.

Asia Pacific

Asia Pacific held approximately 39.1% share of the global automotive labeling market in 2025 and is forecasted to register the fastest CAGR of 6.8% during the forecast period. Rapid expansion of automotive manufacturing in China, India, Japan, and South Korea is a major factor driving regional market growth. Rising vehicle ownership, increasing exports, and expansion of electric vehicle production are creating strong demand for durable automotive labeling solutions. Automotive component suppliers across the region are adopting advanced barcode and RFID labels to improve inventory management and supply chain efficiency. In addition, increasing investments in automotive electronics and battery manufacturing are supporting higher demand for thermal-resistant and chemical-resistant labels.

China dominates the Asia Pacific market because of its large-scale automotive production and strong electric vehicle ecosystem. A unique growth driver in China is the rapid expansion of domestic EV battery manufacturing and smart mobility infrastructure. Automotive manufacturers are increasingly implementing high-performance labeling systems for battery packs, charging systems, and autonomous driving modules. The country is also witnessing rising adoption of smart factory systems that require automated labeling technologies for component tracking and quality management. Continued investment in electric mobility and vehicle exports is expected to support strong future demand for automotive labeling solutions in China.

Middle East & Africa

The Middle East & Africa region accounted for approximately 4.8% market share in 2025 and is projected to expand at a CAGR of 6.1% during the forecast period. Growing automotive imports, rising industrialization, and increasing vehicle assembly activities are supporting demand for automotive labeling products across the region. Governments are investing in transportation infrastructure and industrial diversification programs to strengthen domestic manufacturing sectors. Automotive distributors and assembly plants are increasingly adopting standardized labeling systems for safety compliance and inventory management. Demand for durable labels capable of withstanding high temperatures and harsh desert environments is also increasing throughout the region.

Saudi Arabia dominates the Middle East & Africa market due to rising investments in automotive assembly and industrial manufacturing. A unique growth driver in the country is the expansion of domestic automotive production under economic diversification initiatives. Automotive companies are establishing new assembly facilities and component manufacturing plants, increasing demand for industrial labeling solutions. The country is also witnessing growth in commercial vehicle imports and logistics infrastructure development. Rising industrial automation and expansion of local automotive supply chains are expected to support future market demand across Saudi Arabia.

Latin America

Latin America accounted for nearly 4.4% market share in 2025 and is expected to register a CAGR of 6.9% through 2034. Increasing vehicle production, expansion of automotive component manufacturing, and rising commercial vehicle demand are supporting regional market growth. Countries such as Brazil and Mexico are strengthening automotive exports and attracting foreign investment in vehicle assembly operations. Automotive labeling demand is rising due to growing adoption of safety compliance labels, barcode tracking systems, and branding labels for vehicle components. In addition, expansion of automotive aftermarket services and spare parts distribution networks is supporting demand for durable labeling technologies across the region.

Brazil remains the dominant country in the Latin American market because of its strong automotive manufacturing sector and expanding commercial vehicle production. A unique growth driver in Brazil is the increasing localization of automotive component manufacturing. Automotive suppliers are investing in regional production facilities to reduce import dependency and improve supply chain efficiency. This trend is increasing demand for standardized industrial labels and inventory management systems across automotive manufacturing operations. Continued industrial expansion and rising vehicle exports are expected to strengthen future market growth in Brazil.

Competitive Landscape

The global automotive labeling market is moderately fragmented, with major players focusing on smart labeling technologies, durable material innovation, and sustainability initiatives. Companies are investing in RFID-enabled solutions, high-temperature resistant materials, and automated printing systems to strengthen market competitiveness. Growing adoption of electric vehicles and connected manufacturing systems is encouraging labeling manufacturers to develop advanced tracking and compliance solutions.

3M Company remains one of the leading players in the market due to its strong portfolio of industrial adhesives, automotive labeling products, and global manufacturing network. Other major companies including Avery Dennison Corporation, CCL Industries, Brady Corporation, and UPM Raflatac are focusing on digital labeling innovation and sustainable material development. Automotive labeling suppliers are also expanding regional production facilities and collaborating with automotive OEMs to support growing vehicle manufacturing demand. Continued investment in smart factory technologies and eco-friendly label materials is expected to intensify market competition over the forecast period.

Key Players List

- 3M Company

- Avery Dennison Corporation

- CCL Industries Inc.

- Brady Corporation

- UPM Raflatac

- tesa SE

- Henkel AG & Co. KGaA

- SATO Holdings Corporation

- Multi-Color Corporation

- Dunmore Corporation

- Resource Label Group

- Fuji Seal International, Inc.

- Lintec Corporation

- Schreiner Group GmbH & Co. KG

- HID Global Corporation