Aseptic Carton Packaging Market Size and Growth

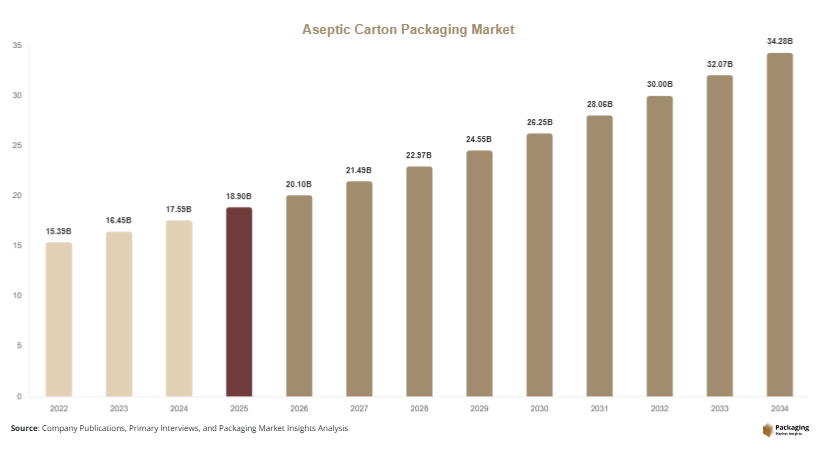

The global Aseptic Carton Packaging Market size was valued at approximately USD 18.9 billion in 2025 and is projected to reach USD 20.1 billion in 2026. By 2034, the market is forecasted to reach nearly USD 36.8 billion, expanding at a CAGR of 6.9% during 2025–2034. Rising urbanization, increasing consumption of packaged beverages, and growing demand for preservative-free food products are major contributors to market growth.

One of the primary growth factors is the rising preference for long shelf-life packaging among consumers and retailers. Aseptic cartons help reduce spoilage while improving transportation efficiency, especially in regions with limited cold-chain infrastructure. Another key growth factor is the increasing adoption of sustainable paper-based packaging solutions as governments implement regulations against single-use plastics. In addition, technological advancements in multilayer barrier coatings and lightweight carton structures are enhancing product protection and reducing overall packaging costs.

Key Highlights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.2%.

- Brick-shaped aseptic cartons led the type segment with a 36.4% share.

- Paperboard-based materials dominated the market with a 58.2% share.

- Food & beverage applications led the segment with 68.3% share.

- The US remained the dominant country with a market size of USD 4.6 billion in 2025 and USD 4.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Recyclable Carton Structures

A major trend shaping the Aseptic Carton Packaging Market is the growing transition toward recyclable and renewable packaging materials. Packaging manufacturers are reducing the use of aluminum and fossil-based plastics while increasing paperboard content in aseptic cartons. Governments across Europe and North America are implementing sustainability regulations that encourage low-carbon packaging solutions. Beverage companies are responding by introducing cartons made from certified renewable paper fibers and plant-based caps. For example, dairy and juice manufacturers in Sweden and Canada have expanded the use of bio-based carton packaging for shelf-stable beverages. This trend is expected to strengthen over the forecast period as brands focus on circular economy goals and environmentally responsible packaging systems.

Rising Demand for Convenient On-the-Go Beverage Packaging

Another important trend is the increasing demand for portable and single-serve beverage packaging formats. Urban consumers are purchasing ready-to-drink coffee, flavored milk, nutritional drinks, and fruit beverages in compact aseptic cartons with resealable caps and ergonomic designs. Manufacturers are developing slim cartons and lightweight packaging formats to improve portability and reduce transportation costs. For instance, beverage producers in Japan and South Korea are introducing small-capacity aseptic cartons for convenience stores and vending machine distribution. This trend is expected to create opportunities for innovative packaging designs and customized branding solutions across the beverage sector during the forecast period.

Market Drivers

Growing Demand for Shelf-Stable Food and Beverage Products

The increasing consumption of shelf-stable packaged food and beverages is a major driver for the Aseptic Carton Packaging Market. Consumers are seeking products with longer shelf life, minimal preservatives, and convenient storage requirements. Aseptic cartons preserve product quality without refrigeration, making them highly suitable for dairy products, juices, soups, and nutritional beverages. This packaging format also reduces supply chain costs and food waste. For example, milk producers in India and Brazil are increasingly using aseptic cartons to distribute products in regions with limited cold storage infrastructure. As consumer preference for convenient packaged products continues to rise, demand for aseptic carton packaging is expected to increase significantly.

Expansion of Global Dairy Alternative and Functional Beverage Industries

The rapid growth of plant-based beverages and functional drinks is another important market driver. Products such as almond milk, oat milk, protein beverages, and probiotic drinks require packaging solutions that maintain freshness and nutritional quality over extended periods. Aseptic cartons provide excellent barrier protection and lightweight transportation advantages. In North America and Europe, plant-based beverage brands are increasingly adopting carton packaging to align with sustainability goals and consumer preferences for eco-friendly packaging. As health-conscious consumption patterns continue to expand globally, aseptic carton demand is projected to rise across premium beverage categories.

Market Restraint

High Initial Investment and Complex Manufacturing Requirements

One of the major restraints affecting the Aseptic Carton Packaging Market is the high capital investment required for aseptic filling systems and multilayer packaging production. Manufacturing aseptic cartons involves sophisticated sterilization equipment, advanced barrier materials, and precision filling technologies that increase operational costs. Small and medium-sized food manufacturers often face challenges in adopting aseptic packaging due to expensive machinery installation and maintenance requirements. For example, regional beverage producers in developing economies may continue using conventional plastic bottles because aseptic processing infrastructure requires substantial investment. In addition, fluctuations in raw material prices for paperboard, polymers, and aluminum layers can further increase production costs. These factors may limit market penetration among smaller companies and price-sensitive industries, particularly in emerging markets where packaging cost efficiency remains a major purchasing factor.

Market Opportunities

Expansion of Pharmaceutical Liquid Packaging Applications

The increasing use of aseptic packaging in pharmaceutical and healthcare applications presents a strong opportunity for market growth. Liquid medicines, nutritional supplements, pediatric formulations, and medical nutrition products require contamination-free packaging with extended shelf life. Aseptic cartons provide secure storage conditions while reducing the need for preservatives. Pharmaceutical manufacturers in Germany and the United States are increasingly exploring carton-based aseptic packaging for oral nutritional products and hospital-use liquid formulations. As healthcare spending rises globally and demand for sterile liquid packaging expands, the pharmaceutical sector is expected to create long-term growth opportunities for aseptic carton manufacturers.

Growth Potential in Emerging Economies and Rural Distribution Networks

Emerging economies across Asia Pacific, Africa, and Latin America offer substantial opportunities for the Aseptic Carton Packaging Market due to improving retail infrastructure and rising packaged food demand. Rural distribution networks in countries such as India, Indonesia, and Mexico are increasingly adopting shelf-stable beverage products because refrigeration infrastructure remains limited in many regions. Aseptic cartons help manufacturers distribute products efficiently without cold-chain dependence. Food processing companies are investing in localized packaging plants and affordable carton formats to serve growing middle-class populations. This trend is expected to support long-term market expansion across developing economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.9 Billion |

| Market Size in 2026 | USD 20.1 Billion |

| Market Size in 2034 | USD 36.8 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Brick-shaped aseptic cartons dominated the market in 2024 with a market share of approximately 36.4%. These cartons are widely used for milk, juices, soups, and dairy alternatives because they provide efficient storage, transportation, and shelf utilization. Their rectangular structure allows manufacturers and retailers to optimize warehouse and retail shelf space. Large dairy and beverage companies across Europe and Asia prefer brick cartons due to lower logistics costs and high compatibility with automated filling systems. In addition, these cartons support multilayer barrier protection that helps preserve freshness and nutritional quality. Growing demand for family-sized beverage packaging and long shelf-life dairy products continues to strengthen the dominance of this segment in the global market.

Slim carton formats are projected to be the fastest-growing type segment, registering a CAGR of 7.5% during the forecast period. These cartons are increasingly used for single-serve beverages such as ready-to-drink coffee, flavored milk, energy drinks, and nutritional products. Urban consumers prefer lightweight and portable packaging formats that are convenient for travel and on-the-go consumption. Beverage brands in Japan, South Korea, and the United States are launching premium slim cartons with resealable caps and attractive digital printing designs. Manufacturers are also introducing recyclable lightweight materials to improve sustainability performance. Increasing demand for convenience beverages and personalized serving sizes is expected to accelerate future growth in this segment.

By Material

Paperboard-based materials dominated the market in 2024 with a share of nearly 58.2%. Paperboard remains the preferred material because it provides structural strength, printability, and sustainability advantages. Most aseptic cartons use multilayer paperboard structures combined with thin polymer and aluminum barrier layers to protect products from moisture, oxygen, and light exposure. Food and beverage manufacturers are increasingly using renewable fiber-based materials to meet sustainability goals and reduce plastic dependency. Large packaging suppliers are investing in certified paperboard sourcing and low-carbon manufacturing technologies. In addition, governments in Europe and North America are encouraging the use of recyclable fiber-based packaging systems, further supporting segment growth.

Bio-based polymer coatings are expected to emerge as the fastest-growing material segment with a projected CAGR of 7.1%. Traditional aseptic cartons rely on petroleum-based polymer coatings for moisture protection, but manufacturers are increasingly shifting toward plant-based alternatives. Packaging companies are developing sugarcane-derived polyethylene coatings and biodegradable barrier layers to reduce environmental impact. Beverage brands focused on sustainability are adopting cartons with renewable caps and bio-based materials to improve brand positioning. Countries such as Sweden, Germany, and Canada are witnessing increasing commercial adoption of these advanced packaging solutions. Rising consumer awareness regarding eco-friendly packaging and stricter environmental regulations are expected to drive long-term growth for this segment.

By End-Use

The food & beverage segment dominated the global market in 2024 with approximately 68.3% share. Aseptic cartons are extensively used for dairy products, juices, soups, sauces, and plant-based beverages because they extend shelf life without refrigeration. Food manufacturers benefit from lower storage costs and improved transportation efficiency compared to glass and metal packaging. Increasing consumption of packaged milk and ready-to-drink beverages across Asia Pacific and Latin America continues to support segment dominance. Major beverage brands are also introducing premium carton designs with improved dispensing features and sustainable materials. The rise of organized retail and online grocery delivery services is further increasing demand for durable and lightweight carton packaging across the food and beverage industry.

Pharmaceutical liquid packaging is projected to be the fastest-growing end-use segment, registering a CAGR of 7.3% during the forecast period. Healthcare companies are increasingly adopting aseptic cartons for nutritional supplements, pediatric nutrition products, and sterile liquid formulations. These cartons provide contamination resistance, lightweight handling, and extended product stability. Pharmaceutical manufacturers are investing in advanced aseptic filling systems to improve production efficiency and meet strict hygiene standards. Growing healthcare expenditure, aging populations, and rising demand for liquid nutritional products are expected to support market expansion. In addition, the increasing need for sustainable healthcare packaging solutions is encouraging innovation in recyclable aseptic carton materials and barrier technologies.

Aseptic Carton Packaging Market Segmentations

By Type

- Brick-Shaped Cartons

- Gable Top Cartons

- Slim Cartons

- Pillow Packs

By Material

- Paperboard

- Aluminum Foil

- Polyethylene

- Bio-Based Polymer Coatings

By End-User

- Food & Beverages

- Dairy Products

- Pharmaceutical Liquids

- Nutritional Supplements

- Household Products

Regional Analysis

North America

North America accounted for approximately 24.6% of the global market share in 2025 and is projected to expand at a CAGR of 6.1% during the forecast period. The region benefits from high consumption of packaged dairy products, nutritional beverages, and ready-to-drink coffee products. Demand for recyclable packaging and sustainable beverage containers is increasing across the United States and Canada. Food manufacturers are also investing in advanced aseptic filling technologies to improve operational efficiency and product shelf life. Growing retail penetration of plant-based beverages and increasing demand for preservative-free packaged food products are contributing to regional growth. The rise of e-commerce grocery delivery services is further increasing demand for lightweight and durable carton packaging.

The United States dominates the North American market due to strong beverage production infrastructure and high consumer preference for shelf-stable packaged products. A unique growth driver in the country is the rapid expansion of protein drinks and meal replacement beverages packaged in aseptic cartons. Beverage companies are launching portable carton formats for fitness and health-conscious consumers. Major supermarkets and convenience stores are increasing shelf space for carton-packaged dairy alternatives and nutritional beverages. Investments in sustainable packaging technologies and recycling partnerships are further strengthening the U.S. market position.

Europe

Europe represented nearly 22.1% market share in 2025 and is expected to grow at a CAGR of 5.8% through 2034. Strict environmental regulations and increasing focus on recyclable packaging solutions are supporting market growth across the region. European food and beverage companies are transitioning toward fiber-based packaging materials to reduce carbon emissions and meet sustainability targets. Demand for long shelf-life dairy products and organic beverages continues to rise across Germany, France, and the Nordic countries. In addition, technological advancements in low-carbon carton manufacturing and renewable barrier coatings are driving innovation in the regional packaging industry.

Germany remains the dominant country within Europe due to its advanced food processing sector and strong dairy export industry. A unique growth factor in the German market is the increasing use of aseptic cartons for organic milk and premium juice products. Consumers are showing preference for environmentally friendly packaging with recyclable paperboard structures. Beverage manufacturers are also adopting digital printing technologies to improve product differentiation and branding. Growing demand for sustainable packaging among retailers and food service companies is expected to support continued market expansion.

Asia Pacific

Asia Pacific dominated the global Aseptic Carton Packaging Market with a 39.1% share in 2025 and is projected to register a CAGR of 7.4% during the forecast period. Rapid urbanization, rising disposable income, and growing packaged food consumption are major growth factors in the region. Countries including China, India, Japan, and Indonesia are witnessing increasing demand for shelf-stable milk, flavored beverages, and ready-to-drink tea products. Expanding retail infrastructure and rising investments in food processing facilities are further driving aseptic carton adoption. In addition, the region benefits from a large consumer base and increasing awareness regarding food safety and hygiene standards.

China is the leading country in the Asia Pacific market due to its large dairy and beverage manufacturing sector. A unique growth driver in China is the strong demand for school nutrition beverages and packaged dairy drinks in urban and semi-urban regions. Beverage manufacturers are introducing smaller and affordable carton formats to target middle-income consumers. The country is also investing heavily in automated aseptic filling lines and domestic carton recycling initiatives. Increasing exports of packaged beverages across Southeast Asia are further contributing to market growth.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.8% of the global market share in 2025 and is expected to grow at a CAGR of 6.5% through 2034. Rising demand for packaged dairy products, juices, and nutritional beverages is supporting market expansion. Population growth, urban retail development, and improving food distribution systems are increasing the adoption of shelf-stable packaging solutions. The region’s warm climate also creates strong demand for packaging formats that preserve product quality without continuous refrigeration. Governments are encouraging investments in domestic food processing and packaging industries to strengthen food security.

Saudi Arabia dominates the regional market due to high consumption of packaged milk and juice products. A key growth driver is the expansion of modern retail chains and convenience stores across urban centers. Food companies are increasingly introducing long shelf-life dairy products packaged in aseptic cartons to improve distribution efficiency. The country is also investing in local beverage manufacturing and sustainable packaging technologies. Growing demand for imported premium beverages and nutritional products is expected to support long-term market growth.

Latin America

Latin America held around 6.4% market share in 2025 and is forecasted to expand at a CAGR of 7.2%, making it one of the fastest-growing regional markets. Increasing packaged beverage consumption, improving retail penetration, and rising dairy production are supporting regional demand for aseptic cartons. Consumers are increasingly purchasing shelf-stable juices, flavored milk, and nutritional drinks due to convenience and affordability. Packaging manufacturers are also expanding production facilities in Brazil and Mexico to meet growing regional demand. Government initiatives supporting sustainable packaging adoption are further contributing to market growth.

Brazil remains the dominant country in Latin America due to its strong dairy industry and expanding beverage sector. A unique growth factor in Brazil is the increasing export of packaged fruit juices and dairy beverages to neighboring countries. Beverage manufacturers are adopting lightweight aseptic cartons to reduce transportation costs and improve product shelf life during long-distance shipping. Rising investment in recyclable carton packaging and modern food processing infrastructure is expected to support future market expansion across the country.

Competitive Landscape

The global Aseptic Carton Packaging Market is moderately consolidated, with leading companies focusing on sustainable packaging innovation, geographic expansion, and advanced aseptic filling technologies. Major market participants are investing in recyclable carton structures, lightweight materials, and renewable barrier coatings to strengthen their market position. Strategic collaborations with food and beverage manufacturers are also becoming increasingly common as companies seek long-term supply agreements and customized packaging solutions.

Tetra Pak remains the market leader due to its extensive global manufacturing network, advanced aseptic processing systems, and strong sustainability initiatives. The company continues to invest in bio-based packaging materials and low-carbon carton technologies. SIG Group and Elopak are also expanding their product portfolios with recyclable carton solutions and digital packaging innovations. Companies are increasingly integrating smart labeling, QR-based traceability systems, and high-speed filling technologies to improve operational efficiency and brand differentiation.

Key Players List

- Tetra Pak International S.A.

- SIG Group AG

- Elopak AS

- Greatview Aseptic Packaging Co., Ltd.

- Nippon Paper Industries Co., Ltd.

- Mondi Group

- Smurfit Kappa Group

- Stora Enso Oyj

- Ecolean AB

- UFlex Limited

- Billerud AB

- Refresco Group

- Amcor plc

- Sealed Air Corporation

- Evergreen Packaging LLC