Anti Rust Packaging Products Market Size and Growth

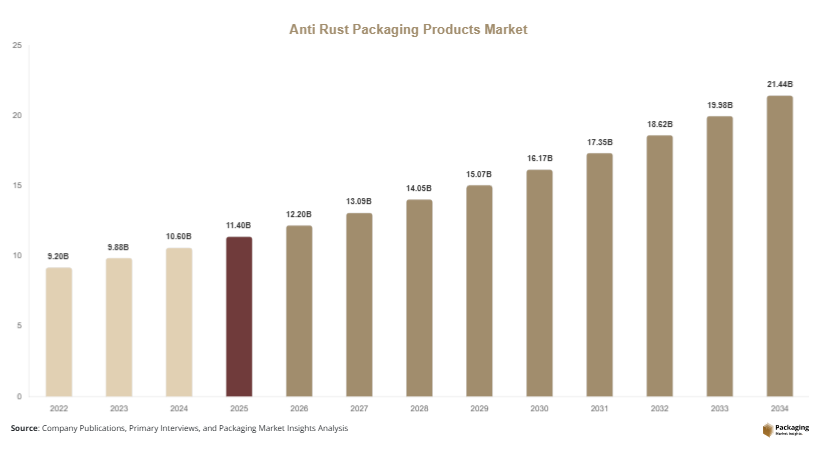

The global anti rust packaging products market was valued at USD 11.4 billion in 2025 and is projected to reach USD 12.2 billion in 2026. By 2034, the market is expected to reach USD 22.1 billion, growing at a CAGR of 7.3% during 2025–2034.

The market’s growth is being driven by increasing exports of industrial metal goods, rising adoption of preservation packaging in automotive and machinery logistics, and growing replacement of oil-based rust prevention methods with clean packaging-integrated protective systems. One major growth factor is the expansion of global industrial equipment supply chains, which require durable anti-rust packaging for long transit durations. A second growth factor is the increasing demand for protective storage systems in spare parts warehousing, where rust prevention is critical for maintaining product integrity over extended inventory cycles. A third factor is rising use of environmentally compliant inhibitor packaging that meets industrial sustainability standards.

Key Highlights

- Asia Pacific dominated the market with a 37.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.9%.

- VCI bags led the type segment with a 30.8% share.

- Polyethylene-based protective packaging dominated the material segment with a 44.9% share.

- Automotive & industrial machinery applications led the end-use segment with 29.4% share.

- The US remained the dominant country with a market size of USD 2.3 billion in 2025 and USD 2.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Clean and Dry Rust Prevention Packaging Systems

A key trend shaping the anti rust packaging products market is the increasing transition toward clean and dry packaging-based rust prevention systems that replace oil-coated, wax-treated, or grease-based metal preservation practices. Traditional rust prevention methods often involve messy application processes, cleaning requirements before component installation, and higher labor costs during packaging and unpacking. Modern anti-rust packaging solutions such as VCI bags, anti-rust wraps, and inhibitor paper systems eliminate many of these operational challenges by providing passive protection inside sealed packaging environments. Automotive transmission components, industrial bearings, and fabricated machine parts are increasingly shipped in dry-pack anti-rust packaging systems. This trend is expected to continue as manufacturers seek cleaner packaging workflows, reduced maintenance preparation, and lower lifecycle preservation costs across industrial logistics operations.

Growth in High-Barrier Hybrid Packaging Solutions

Another major trend is the rapid development of hybrid anti-rust packaging products that combine corrosion inhibition, moisture management, and contamination protection into a single packaging format. Manufacturers are introducing multilayer packaging systems that integrate VCI chemistry with desiccants, oxygen absorbers, anti-static properties, and high-barrier film technology. These hybrid systems are particularly valuable for aerospace assemblies, defense storage systems, electronics equipment, and marine industrial parts exposed to severe storage conditions. For example, heavy equipment exporters increasingly use reinforced hybrid anti-rust packaging for steel-intensive assemblies shipped across humid ocean freight routes. Future market growth is likely to favor advanced packaging systems that provide multi-layer protective functionality while improving sustainability through recyclable material formats.

Market Drivers

Rising Global Trade in Metal Components and Industrial Equipment

One of the strongest drivers for the anti rust packaging products market is the rapid increase in international trade of fabricated steel products, machinery components, automotive assemblies, industrial spare parts, and engineered equipment. Long-distance shipping exposes metal surfaces to moisture condensation, marine salt exposure, and fluctuating storage temperatures that significantly increase rust risk. Manufacturers are therefore adopting anti-rust packaging as a protective supply chain standard rather than an optional packaging layer. Bearings, shafts, fabricated tools, automotive driveline systems, and machine assemblies increasingly rely on protective packaging to ensure product quality at delivery. As cross-border industrial sourcing expands, demand for scalable anti-rust packaging solutions continues to increase globally.

Expansion of Long-Term Industrial Storage and Inventory Preservation

Growth in long-duration industrial inventory storage is another major market driver. Industrial spare parts, defense hardware, mining equipment components, heavy machinery assemblies, and infrastructure replacement parts are frequently warehoused for months or years before use. Exposure to humidity, trapped condensation, and temperature cycling creates significant rust risks over long storage periods. Anti-rust packaging products provide cost-efficient preservation by maintaining controlled protective environments around packaged components. Warehousing operators are increasingly integrating rust-prevention packaging into inventory protection strategies, especially for high-value replacement parts and precision-engineered assemblies that require corrosion-free operational readiness.

Market Restraint

Product Performance Dependence on Packaging Integrity

A significant restraint in the anti rust packaging products market is that product performance depends heavily on packaging integrity, environmental sealing quality, and proper usage conditions. Anti-rust packaging systems are most effective when the protective atmosphere remains contained within a properly enclosed packaging environment. Damage to packaging seals, punctures in protective films, poor wrapping practices, or prolonged exposure to external humidity can reduce inhibitor effectiveness and compromise rust prevention performance.

This challenge becomes more complex in oversized industrial shipments where large fabricated equipment requires custom protective wrapping. Uneven enclosure quality can create weak protection zones. Mixed-metal assemblies also create compatibility challenges because inhibitor chemistry optimized for steel may not provide equal protection for copper or aluminum surfaces. In high-humidity marine transport routes, standard packaging may require multilayer reinforcement to maintain reliable protection.

Industrial buyers often require packaging qualification trials before scaling adoption, which increases implementation time. Smaller manufacturers may also underutilize premium anti-rust packaging due to cost sensitivity, especially in price-competitive industrial supply chains. Packaging suppliers therefore must focus on technical support, climate-specific packaging engineering, and user education to ensure real-world performance consistency.

Market Opportunities

Expansion in Electronics and Electrical Equipment Protection

The rapid expansion of electronics manufacturing and electrical equipment logistics presents a major opportunity for anti-rust packaging suppliers. Connectors, terminals, conductive assemblies, electrical switchgear, industrial sensors, and power system components often contain exposed metal surfaces vulnerable to oxidation and micro-rust formation during storage and shipment. Anti-rust packaging integrated with anti-static and moisture-control features is becoming increasingly important in electronics supply chains. Manufacturers are demanding packaging systems that protect conductive surfaces while preventing contamination and humidity damage. This creates high-value market opportunities for hybrid anti-rust packaging tailored to precision electrical applications.

Growth in Sustainable Anti-Rust Packaging Solutions

Sustainability-driven packaging innovation offers another major growth opportunity. Industrial customers are increasingly seeking recyclable anti-rust films, biodegradable inhibitor paper systems, reusable protective wraps, and environmentally safer inhibitor chemistry that reduces hazardous packaging waste. Packaging producers developing mono-material recyclable anti-rust systems are seeing growing demand in regulated industrial markets. Future growth is likely to accelerate as global manufacturers integrate sustainability metrics into procurement strategies for industrial packaging, creating premium demand for green anti-rust preservation solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.4 Billion |

| Market Size in 2026 | USD 12.2 Billion |

| Market Size in 2034 | USD 22.1 Billion |

| CAGR | 7.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

VCI bags dominated the anti rust packaging products market in 2024 with a 30.8% market share, supported by their packaging flexibility, effective vapor-phase rust prevention, and suitability for enclosed industrial packaging environments. VCI bags release protective inhibitor molecules that create an invisible barrier over exposed metal surfaces, reducing oxidation without requiring direct chemical coating on parts. These products are widely used for bearings, fabricated steel components, automotive driveline parts, tools, marine assemblies, and industrial replacement parts. Their ease of use and clean unpacking profile make them attractive compared with oil-based preservation methods. Industrial exporters also favor VCI bags because they simplify packaging operations while supporting scalable rust prevention across varying shipment sizes. Growth in recyclable VCI bag technology is further strengthening segment dominance.

Anti-rust emitters are projected to be the fastest-growing type segment, expanding at a CAGR of 8.3% through 2034. These products are increasingly used in enclosed equipment housings, export crates, defense storage systems, and machine cabinets where passive vapor-phase rust protection can reach internal cavities and hidden surfaces. Growth is being supported by rising long-duration equipment storage, defense preservation programs, and industrial warehousing modernization. Future innovation in controlled-release inhibitor technology and long-life emitter systems is expected to expand their adoption in aerospace, marine, and heavy industrial equipment storage applications.

By Material

Polyethylene-based protective packaging led the material segment in 2024 with a 44.9% market share, driven by its durability, strong sealing capability, puncture resistance, and compatibility with rust inhibitor chemistry. Polyethylene anti-rust films and wraps are widely used across industrial packaging because they provide moisture protection while supporting vapor-phase inhibitor functionality in enclosed systems. Heavy machinery exporters often use reinforced polyethylene anti-rust wraps for fabricated steel structures and machine assemblies exposed to long shipping cycles. Specialty static-safe polyethylene protective packaging is also increasingly used in electrical component preservation. Cost efficiency, packaging flexibility, and manufacturing scalability continue to support widespread adoption across industrial packaging applications.

Recyclable moisture-barrier laminates are forecast to be the fastest-growing material segment at a CAGR of 8.1%, supported by sustainability initiatives and increasing demand for advanced long-duration packaging protection. These materials combine strong moisture resistance, oxygen barrier properties, and compatibility with inhibitor chemistry while improving recyclability compared with traditional multilayer industrial packaging systems. Industrial exporters increasingly use these laminates for sensitive fabricated equipment, precision assemblies, and climate-sensitive industrial shipments. Future innovation in mono-material high-barrier anti-rust packaging is expected to accelerate segment growth in sustainability-focused industrial markets.

By End-Use

Automotive & industrial machinery dominated the end-use segment in 2024 with a 29.4% market share, driven by rising shipment volumes of metal-intensive components requiring rust prevention during logistics and warehousing. Engines, fabricated transmission systems, bearings, shafts, machine frames, hydraulic assemblies, and replacement industrial parts are all vulnerable to oxidation during long storage cycles. Anti-rust packaging provides cost-efficient preservation while reducing maintenance preparation and warranty claims. Global machinery exports and growing aftermarket replacement part distribution are strengthening packaging demand across this segment. Industrial automation equipment expansion is also increasing adoption of specialized rust prevention packaging for fabricated metal assemblies.

Electronics & electrical equipment is projected to be the fastest-growing end-use segment, expanding at a CAGR of 8.0% through 2034. Connectors, conductive assemblies, switchgear components, terminals, sensors, and industrial control systems often contain exposed metal surfaces vulnerable to oxidation and micro-rust formation. Anti-rust packaging integrated with moisture control and anti-static functionality is increasingly used to protect these components during transit and storage. As electronics manufacturing expands globally, specialty rust prevention packaging for conductive assemblies is expected to become a high-growth niche market.

Anti Rust Packaging Products Market Segmentations

By Product Type

- VCI Bags

- Anti-Rust Films

- Rust Preventive Papers

- Anti-Rust Emitters

- Protective Foams & Wraps

- Desiccant Integrated Packaging

- Barrier Laminates

By Material

- Polyethylene-Based Packaging

- Polypropylene-Based Packaging

- Paper-Based Packaging

- Recyclable Moisture-Barrier Laminates

- Hybrid Composite Packaging Materials

By Application

- Automotive & Industrial Machinery

- Electronics & Electrical Equipment

- Aerospace & Defense

- Marine Equipment

- Heavy Industrial Components

- Industrial Spare Parts

- Oil & Gas Equipment

Regional Analysis

North America

North America accounted for 24.1% of the anti rust packaging products market share in 2025 and is projected to grow at a CAGR of 6.5% through 2034. Regional demand is supported by strong industrial manufacturing output, expansion in aerospace component logistics, and growing use of protective packaging in aftermarket machinery parts distribution. Automotive assembly plants and industrial equipment suppliers increasingly rely on anti-rust films, VCI bags, and moisture-barrier wraps to protect fabricated metal parts during storage and long-distance shipping. Warehousing modernization across the U.S. and Canada is also supporting broader adoption of long-duration rust prevention packaging systems. Growth is further supported by stricter industrial quality standards requiring corrosion-free delivery of precision-engineered products.

The United States dominates the regional market due to its large industrial export base, advanced packaging ecosystem, and defense logistics infrastructure. A unique growth driver in the U.S. is the increasing shipment of aerospace replacement components that require long-term corrosion-free preservation. Aircraft engine assemblies, landing gear systems, and fabricated aerospace structures increasingly use monitored anti-rust packaging systems with humidity indicators and advanced barrier layers. Industrial packaging companies are also introducing reusable protective packaging for closed-loop industrial logistics applications.

Europe

Europe held 25.7% of the global anti rust packaging products market in 2025 and is expected to register a CAGR of 6.8% during 2025–2034. The market is driven by strong automotive exports, industrial machinery manufacturing, marine engineering activity, and increasing regulatory pressure for sustainable packaging systems. Demand is rising for recyclable anti-rust wraps, biodegradable inhibitor papers, and advanced barrier packaging used in fabricated equipment exports. European industrial exporters increasingly require protective packaging solutions that combine rust prevention with recyclability and improved packaging efficiency. Expansion in electric vehicle component manufacturing is also contributing to packaging demand for conductive metal assemblies and fabricated structural components vulnerable to oxidation during transit.

Germany remains the dominant country in Europe due to its strong engineering manufacturing sector and export-oriented machinery industry. A unique growth driver in Germany is rising exports of precision machine tools and industrial systems that require climate-stable anti-rust packaging for long-distance logistics. Packaging manufacturers are developing customized rust prevention systems for fabricated steel assemblies, alloy components, and multi-metal equipment modules. Smart packaging labels that monitor storage exposure conditions are also gaining traction in industrial export packaging systems.

Asia Pacific

Asia Pacific dominated the anti rust packaging products market with a 37.2% share in 2025 and is projected to grow at a CAGR of 7.7% through 2034. The region benefits from rapid industrialization, large-scale automotive production, strong steel exports, expansion in electronics manufacturing, and increasing machinery exports. Demand is increasing for anti-rust bags, VCI films, rust inhibitor papers, and moisture-controlled protective packaging systems used across regional industrial supply chains. Warehousing growth in manufacturing hubs is increasing demand for long-duration rust prevention packaging for inventory preservation. Rising infrastructure spending and increasing exports of fabricated metal systems are also strengthening regional packaging demand.

China remains the dominant country in Asia Pacific because of its broad manufacturing base, strong export competitiveness, and integrated industrial packaging supply chains. A unique growth driver in China is the rapid growth of industrial electronics and machinery exports requiring contamination-free anti-rust packaging for conductive and fabricated metal assemblies. Domestic packaging manufacturers are expanding recyclable anti-rust material production while improving packaging performance for severe export logistics conditions, strengthening local adoption and export competitiveness.

Middle East & Africa

The Middle East & Africa represented 7.8% of the anti rust packaging products market in 2025 and is forecast to expand at a CAGR of 7.0% through 2034. Demand is being supported by industrial diversification, large-scale oilfield equipment imports, marine logistics expansion, and increasing warehousing investments. Corrosion risk is especially high in humid coastal environments and desert climates with large temperature variation, creating strong demand for reinforced anti-rust packaging systems. High-barrier protective wraps, desiccant-integrated rust prevention packaging, and long-duration inhibitor systems are increasingly used for industrial equipment storage and marine component logistics. Packaging demand is also increasing across heavy industrial replacement part supply chains.

Saudi Arabia dominates the regional market due to industrial infrastructure expansion and large-scale equipment preservation needs in oil & gas and petrochemical sectors. A unique growth driver is the rising storage of fabricated industrial systems in climate-challenging environments where moisture condensation and airborne salts increase rust exposure. Industrial packaging suppliers are therefore offering marine-grade anti-rust barrier systems tailored for harsh storage conditions, improving long-duration preservation reliability.

Latin America

Latin America accounted for 5.2% of the anti rust packaging products market share in 2025 and is projected to record the fastest CAGR of 7.9% through 2034. The market is benefiting from growth in agricultural machinery exports, mining equipment logistics, regional industrialization, and warehousing expansion. Industrial exporters increasingly require reliable anti-rust packaging for long-distance ocean freight and tropical climate exposure. Cost-effective rust inhibitor paper systems, reinforced anti-rust wraps, and hybrid moisture-barrier packaging are gaining wider commercial use. Regional port infrastructure upgrades and trade corridor expansion are also supporting demand for industrial preservation packaging products.

Brazil remains the dominant country in Latin America due to its broad machinery manufacturing base and growing fabricated equipment export sector. A unique growth driver in Brazil is expansion in agricultural machinery exports, where large steel-intensive equipment components require rust prevention packaging during extended shipment cycles. Packaging companies are increasingly supplying customized reinforced anti-rust systems for oversized industrial assemblies, supporting export quality protection.

Competitive Landscape

The anti rust packaging products market is moderately fragmented, with competition focused on inhibitor chemistry innovation, packaging sustainability, industrial customization, and global supply chain reach. Cortec Corporation remains the market leader due to its broad portfolio of anti-rust packaging solutions, strong VCI technology capabilities, and deep penetration across automotive, defense, heavy machinery, and industrial export packaging sectors.

Daubert Cromwell continues strengthening its market position through advanced rust prevention films, engineered industrial packaging systems, and tailored packaging solutions for fabricated metal exports. Armor Protective Packaging is actively expanding in customized VCI protective packaging and industrial logistics preservation systems. Zerust Excor remains a key player through corrosion prevention chemistry innovation and specialty industrial packaging offerings. Northern Technologies International Corporation (NTIC) continues investing in environmentally compliant rust prevention packaging technologies and recyclable packaging formats.

Key competitive strategies include recyclable VCI material development, smart humidity-monitoring packaging integration, industry-specific packaging customization, and regional manufacturing expansion to support faster industrial supply responsiveness.

Key Players List

- Cortec Corporation

- Daubert Cromwell

- Armor Protective Packaging

- Zerust Excor

- Northern Technologies International Corporation (NTIC)

- Branopac India Pvt. Ltd.

- Aicello Corporation

- MetPro Group

- Green Packaging Inc.

- Protective Packaging Corporation

- Smurfit Kappa Industrial

- Intertape Polymer Group

- OJI F-Tex Co., Ltd.

- RustX USA

- Polyplus Packaging

- Safepack Industries Ltd.

- Shenyang Rustproof Packaging Materials Co., Ltd.