Anti Counterfeit Packaging Technologies Market Size and Growth

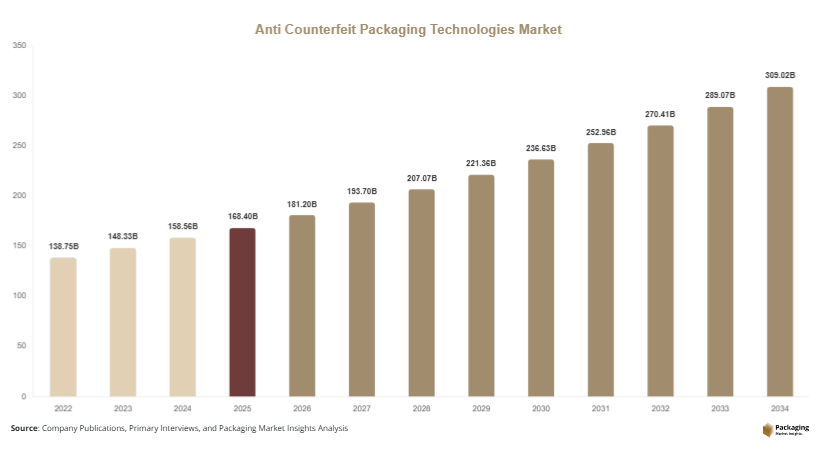

The global anti counterfeit packaging technologies market size was valued at USD 168.4 billion in 2025 and is projected to reach USD 181.2 billion in 2026. By 2034, the market is forecasted to reach USD 329.8 billion, expanding at a CAGR of 6.9% during 2025–2034. Rising incidents of counterfeit products, especially in healthcare and consumer goods industries, are encouraging manufacturers to adopt advanced anti-counterfeit packaging solutions to protect brand reputation and ensure regulatory compliance. The anti counterfeit packaging technologies market is experiencing substantial growth due to increasing concerns regarding product authenticity, supply chain transparency, and consumer safety across industries such as pharmaceuticals, food & beverages, cosmetics, electronics, and luxury goods.

Anti-counterfeit packaging technologies include holograms, RFID tags, tamper-evident labels, barcodes, QR codes, forensic markers, serialization systems, and smart tracking technologies. These solutions help manufacturers verify product authenticity, improve supply chain visibility, and reduce revenue losses caused by counterfeit trade. Growing digitalization in logistics and retail distribution is also increasing the integration of connected packaging technologies that enable real-time product tracking and authentication.

Key Highlights

- Asia Pacific dominated the market with a 36.8% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.5%.

- Authentication technologies led the type segment with a 33.7% share.

- Plastic-based packaging materials dominated with a 46.5% share

- Pharmaceutical applications led the end-use segment with 41.2% share.

- The US remained the dominant country with a market size of USD 39.4 billion in 2025 and USD 42.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Smart Authentication Technologies

The integration of smart authentication technologies is becoming a major trend in the anti counterfeit packaging technologies market. Companies are increasingly using NFC tags, QR codes, RFID-enabled labels, and blockchain-based verification systems to improve product traceability and prevent unauthorized duplication. Consumers can now scan packaging through smartphones to confirm product authenticity, access manufacturing information, and track supply chain movement.

For example, pharmaceutical manufacturers are implementing serialization systems that assign unique digital identities to medicine packages. Luxury cosmetics brands are also introducing NFC-enabled packaging to combat counterfeit beauty products sold through online marketplaces. These technologies improve brand transparency while helping regulators monitor product distribution more efficiently. Future adoption of artificial intelligence and cloud-connected packaging systems is expected to further enhance authentication accuracy and real-time monitoring capabilities. Smart authentication technologies are likely to become standard across high-value consumer products during the forecast period.

Increasing Use of Sustainable Secure Packaging

Sustainability is emerging as an important trend in anti-counterfeit packaging as brands seek environmentally responsible security solutions. Packaging companies are developing recyclable tamper-evident labels, paper-based authentication materials, and biodegradable security seals to align with global sustainability goals. Manufacturers are increasingly balancing product protection with environmental compliance as governments tighten regulations regarding packaging waste and plastic usage.

For instance, beverage manufacturers are adopting recyclable QR-enabled paper labels that provide authentication features without increasing plastic consumption. Similarly, pharmaceutical companies are investing in lightweight packaging formats integrated with invisible inks and security printing technologies. This trend is expected to accelerate as consumers become more conscious about sustainable packaging practices. The combination of eco-friendly materials and digital authentication features is likely to reshape packaging innovation strategies across the anti-counterfeit packaging industry.

Market Drivers

Growing Counterfeit Product Incidents Across Industries

The increasing circulation of counterfeit products is one of the primary factors driving the anti counterfeit packaging technologies market. Counterfeit medicines, fake cosmetics, imitation electronics, and unauthorized luxury products continue to create financial losses and safety risks for manufacturers and consumers. As a result, companies are investing heavily in packaging security technologies to strengthen product authentication and protect brand integrity.

Pharmaceutical companies are particularly vulnerable to counterfeit drug distribution, which has increased demand for serialization labels, tamper-proof seals, and traceability systems. For example, several healthcare manufacturers now use holographic labels and encrypted QR codes to reduce medicine duplication risks. Luxury fashion and electronics companies are also adopting RFID-enabled packaging to verify genuine products throughout the supply chain. Growing global trade and expansion of e-commerce platforms are expected to further increase demand for anti-counterfeit packaging technologies.

Government Regulations Supporting Product Traceability

Strict government regulations regarding product safety and traceability are significantly accelerating market growth. Regulatory agencies across North America, Europe, and Asia Pacific are implementing serialization mandates and track-and-trace requirements to combat counterfeit goods and improve supply chain transparency. Compliance with these regulations requires manufacturers to adopt secure packaging technologies and advanced labeling systems.

For example, pharmaceutical serialization laws in the United States and Europe require companies to assign unique identification codes to drug packaging for supply chain monitoring. Food and beverage companies are also adopting authentication labels to improve traceability and consumer trust. These regulations are encouraging packaging manufacturers to invest in digital printing technologies, forensic markers, and connected packaging solutions. The continued expansion of regulatory frameworks is expected to support long-term growth opportunities for anti-counterfeit packaging providers worldwide.

Market Restraint

High Implementation Costs and Technology Integration Challenges

The high cost of implementing advanced anti-counterfeit packaging technologies remains a major restraint for market growth. Small and medium-sized manufacturers often face financial challenges when adopting RFID systems, blockchain authentication platforms, forensic inks, and serialization equipment. Initial installation costs, software integration expenses, and employee training requirements can significantly increase operational expenditures.

In addition, integrating anti-counterfeit systems into existing supply chains and packaging lines can be technically complex. Companies operating in developing regions may lack adequate digital infrastructure to support real-time authentication and data management systems. For example, smaller food packaging manufacturers may struggle to justify investments in RFID-enabled tracking systems due to limited production volumes and budget constraints. The lack of standardized global regulations and interoperability between authentication systems can also create compatibility issues for multinational manufacturers. These challenges may slow technology adoption in cost-sensitive markets despite increasing demand for secure packaging solutions.

Market Opportunities

Expansion of Blockchain-Based Packaging Authentication

The growing use of blockchain technology presents a significant opportunity for the anti counterfeit packaging technologies market. Blockchain systems provide secure digital records that improve product traceability, authentication, and supply chain transparency. Manufacturers can use blockchain-enabled packaging to store production data, logistics records, and ownership history that cannot be easily altered or duplicated.

Luxury goods manufacturers and pharmaceutical companies are increasingly exploring blockchain authentication systems to combat counterfeit distribution. For example, premium beverage companies are using blockchain-connected QR labels that allow consumers to verify product origin and distribution details. This technology is expected to gain broader adoption as supply chains become more digitized. Blockchain-based packaging solutions may also improve consumer trust and reduce fraud-related losses across global retail channels.

Rising Demand for Secure E-Commerce Packaging

The rapid expansion of e-commerce platforms is creating strong opportunities for anti-counterfeit packaging providers. Online retail channels increase the risk of counterfeit product distribution because consumers often cannot verify authenticity before purchase. As a result, brands are adopting secure packaging systems designed specifically for digital commerce and direct-to-consumer delivery models.

Tamper-evident seals, serialized labels, and smartphone-scannable authentication features are increasingly used for cosmetics, supplements, electronics, and luxury products sold online. For example, skincare brands are integrating QR-enabled packaging that verifies authenticity through mobile applications. Growth in cross-border online trade and global marketplace platforms is expected to further increase demand for intelligent packaging technologies. Companies investing in connected packaging systems and digital verification solutions are likely to benefit from long-term growth opportunities in the expanding e-commerce sector.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 168.4 Billion |

| Market Size in 2026 | USD 181.2 Billion |

| Market Size in 2034 | USD 329.8 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Authentication technologies dominated the type segment and accounted for 33.7% of the market share in 2024. This category includes holograms, security inks, RFID tags, QR codes, and barcode verification systems widely used across pharmaceutical, food, electronics, and cosmetics industries. Companies increasingly rely on authentication technologies because they provide visible and digital verification methods that help consumers identify genuine products. Holographic labels remain popular in pharmaceutical packaging due to their difficulty to replicate and cost efficiency. QR-enabled packaging solutions are also witnessing significant demand because consumers can verify product authenticity through smartphones. Major packaging manufacturers are investing in advanced digital printing and encryption technologies to improve security performance. The increasing expansion of e-commerce and global trade continues to strengthen adoption of authentication technologies across high-value consumer goods industries.

Smart packaging technologies are projected to witness the fastest CAGR of 7.8% during the forecast period. Smart packaging includes NFC-enabled labels, blockchain-connected packaging, sensor-based tracking systems, and intelligent serialization platforms. Rising demand for real-time supply chain visibility and digital consumer engagement is accelerating adoption of connected packaging technologies. Manufacturers are increasingly integrating cloud-based tracking solutions and smartphone authentication features into product packaging to combat counterfeit distribution. For example, luxury fashion brands and pharmaceutical companies are using NFC-enabled labels that provide real-time product verification and logistics monitoring. Future growth is expected to be supported by artificial intelligence integration, IoT-enabled packaging systems, and expansion of digital retail ecosystems.

By Material

Plastic-based packaging materials dominated the anti counterfeit packaging technologies market with a 46.5% share in 2024 due to their flexibility, durability, and compatibility with advanced security technologies. Plastic packaging supports tamper-evident closures, embedded RFID tags, holographic labels, and printed authentication systems used across pharmaceutical and consumer goods industries. PET and HDPE materials are commonly used because they provide lightweight packaging solutions while maintaining product protection and security integration. Flexible plastic packaging is also widely adopted in food and cosmetics industries because it supports digital printing and variable data labeling technologies. Packaging manufacturers continue developing recyclable plastic materials integrated with anti-counterfeit features to improve sustainability performance while maintaining authentication efficiency.

Paper & paperboard materials are expected to grow at the fastest CAGR of 7.1% during the forecast period. Rising sustainability concerns and increasing regulatory pressure regarding plastic waste are encouraging manufacturers to adopt paper-based authentication packaging solutions. QR-enabled paper labels, tamper-proof cartons, and recyclable security packaging formats are becoming more common across luxury goods and premium food products. Technological advancements in digital printing and invisible security inks are improving the functionality of paper-based anti-counterfeit packaging systems. For example, beverage and cosmetics companies are increasingly adopting serialized paper labels integrated with blockchain authentication systems. Continued investment in eco-friendly packaging innovations is expected to support rapid growth in this segment.

By End-Use

Pharmaceutical applications dominated the end-use segment and accounted for 41.2% of the market share in 2024. The pharmaceutical industry faces significant risks associated with counterfeit medicines, making advanced packaging authentication systems essential for product safety and regulatory compliance. Serialization labels, tamper-evident seals, RFID tracking systems, and holographic packaging are widely used to improve medicine traceability and reduce counterfeit drug circulation. Government regulations across North America, Europe, and Asia Pacific continue to accelerate adoption of secure pharmaceutical packaging technologies. The growing expansion of biologics, specialty drugs, and online pharmacy distribution is also increasing demand for intelligent pharmaceutical packaging systems. Major healthcare manufacturers are investing heavily in digital traceability platforms and connected packaging technologies to strengthen supply chain security.

Cosmetics & personal care applications are projected to grow at the fastest CAGR of 7.3% during the forecast period. Rising counterfeit beauty product circulation through online retail channels is encouraging brands to adopt authentication packaging technologies. Premium skincare and cosmetic companies increasingly use QR-enabled labels, NFC tags, and tamper-proof packaging to improve product verification and brand protection. Consumer demand for transparency and genuine luxury beauty products is driving investment in smart packaging systems. For example, premium skincare brands are integrating mobile-based authentication tools that provide ingredient verification and product origin details. Continued expansion of global e-commerce beauty sales is expected to accelerate demand for secure cosmetics packaging solutions.

Anti Counterfeit Packaging Technologies Market Segmentations

By Type

- Authentication Technologies

- Track & Trace Technologies

- Tamper-Evident Technologies

- Holograms & Security Inks

- RFID & NFC Solutions

- Barcode & QR Code Systems

By Material

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Flexible Packaging Materials

By End-User

- Pharmaceuticals

- Food & Beverage

- Consumer Electronics

- Personal Care & Cosmetics

- Automotive

- Industrial Goods

Regional Analysis

North America

North America accounted for 31.2% of the anti counterfeit packaging technologies market share in 2025 and is projected to grow at a CAGR of 6.1% during the forecast period. The region benefits from advanced packaging infrastructure, strong pharmaceutical manufacturing capabilities, and strict regulatory frameworks regarding product authentication. High counterfeit risks in healthcare, electronics, and luxury goods industries continue to support demand for RFID labels, serialization systems, and tamper-evident packaging technologies. E-commerce expansion and rising consumer awareness regarding product authenticity are further accelerating market growth. Companies across the United States and Canada are increasingly investing in connected packaging technologies to improve supply chain visibility and customer engagement.

The United States dominated the regional market due to stringent pharmaceutical traceability regulations and strong adoption of digital authentication technologies. One major growth driver is the increasing use of smart packaging systems integrated with mobile verification applications. For example, several pharmaceutical manufacturers now use serialized QR-enabled medicine packaging that allows real-time authentication and tracking. The cosmetics and premium beverage sectors are also adopting NFC-enabled packaging to reduce counterfeit product circulation. Continuous investment in artificial intelligence-based supply chain monitoring systems is expected to strengthen the U.S. market during the forecast period.

Europe

Europe represented 26.4% of the global anti counterfeit packaging technologies market share in 2025 and is forecasted to expand at a CAGR of 6.0% through 2034. The region is supported by strict anti-counterfeit regulations, advanced manufacturing standards, and growing emphasis on consumer protection. Pharmaceutical serialization laws and food traceability regulations are encouraging widespread adoption of secure packaging technologies. Demand for sustainable authentication materials and recyclable smart labels is also increasing across Europe. Luxury goods manufacturers in France, Italy, and Germany are heavily investing in advanced packaging security features to protect premium brands from imitation products and unauthorized distribution.

Germany remained the dominant country within the European market due to strong industrial manufacturing and pharmaceutical packaging capabilities. One important growth driver is the rapid adoption of Industry 4.0 technologies across packaging and logistics operations. German companies are integrating RFID systems, digital watermarks, and automated traceability platforms into production lines to improve authentication accuracy. For example, several automotive and electronics manufacturers use secure serialized labels to prevent counterfeit spare parts distribution. Rising investment in sustainable anti-counterfeit packaging solutions is also contributing to long-term regional market growth.

Asia Pacific

Asia Pacific dominated the anti counterfeit packaging technologies market with a 36.8% share in 2025 and is projected to grow at a CAGR of 7.4% during the forecast period. Rapid industrialization, expanding e-commerce activity, and increasing counterfeit product incidents are driving strong demand for secure packaging technologies across the region. Countries such as China, India, Japan, and South Korea are witnessing increasing adoption of holograms, QR authentication labels, and RFID tracking systems. Growth in pharmaceutical manufacturing and cross-border trade is also supporting market expansion. Rising government efforts to strengthen intellectual property protection and product traceability are accelerating technology adoption throughout Asia Pacific.

China remained the leading country in the regional market due to its large manufacturing sector and extensive export activities. One unique growth driver is the government’s increasing focus on combating counterfeit consumer goods and pharmaceutical products. Chinese manufacturers are rapidly integrating digital traceability technologies into packaging operations to improve export compliance and supply chain transparency. For example, several electronics and luxury product companies now use blockchain-enabled authentication systems to reduce counterfeit distribution risks. India is also emerging as a major growth market because of increasing pharmaceutical exports and growing adoption of serialization technologies.

Middle East & Africa

The Middle East & Africa anti counterfeit packaging technologies market accounted for 3.8% of global revenue in 2025 and is projected to expand at a CAGR of 5.6% during the forecast period. Rising awareness regarding counterfeit medicines, cosmetics, and consumer products is supporting demand for authentication packaging technologies across the region. Governments are strengthening import monitoring systems and healthcare regulations to improve product safety standards. Pharmaceutical packaging demand is increasing for tamper-evident labels, secure closures, and serialized tracking systems. Expansion of organized retail and digital commerce channels is also contributing to growing adoption of anti-counterfeit packaging solutions.

Saudi Arabia dominated the regional market due to increasing investment in healthcare infrastructure and product safety initiatives. One important growth driver is the expansion of pharmaceutical manufacturing and retail pharmacy chains across the country. For example, healthcare companies are implementing secure labeling technologies to comply with evolving drug traceability regulations. Luxury cosmetics and imported food products are also driving demand for authentication packaging solutions. Rising consumer awareness regarding counterfeit risks is expected to support further market development throughout the Middle East and Africa.

Latin America

Latin America held 1.8% of the anti counterfeit packaging technologies market share in 2025 and is expected to register the fastest CAGR of 7.5% during the forecast period. Growing counterfeit trade and increasing online retail activity are creating strong demand for product authentication solutions across the region. Governments are gradually strengthening packaging regulations and customs monitoring systems to reduce illegal product distribution. Food & beverage, pharmaceutical, and personal care industries are increasingly adopting tamper-evident packaging and barcode authentication systems. Growth in regional manufacturing and export activities is also encouraging investment in secure packaging technologies.

Brazil emerged as the dominant country in the Latin American market due to rapid growth in pharmaceutical production and rising consumer goods demand. One major growth driver is the increasing use of serialized packaging technologies in healthcare supply chains. For example, pharmaceutical companies in Brazil are investing in track-and-trace systems to improve medicine distribution transparency and reduce counterfeit risks. Rising e-commerce penetration and cross-border trade activities are expected to further accelerate adoption of anti-counterfeit packaging solutions across the region.

Competitive Landscape

The anti counterfeit packaging technologies market is highly competitive, with major companies focusing on digital authentication innovation, strategic partnerships, and sustainable packaging technologies. Avery Dennison Corporation remains one of the leading companies due to its strong RFID solutions portfolio, global presence, and advanced intelligent labeling technologies. The company continues expanding its smart packaging and connected product authentication capabilities across healthcare and retail industries.

CCL Industries Inc. is strengthening its position through advanced holographic labels, security printing technologies, and track-and-trace solutions. Zebra Technologies Corporation focuses on digital supply chain visibility systems and barcode authentication technologies for industrial applications. SICPA Holding SA continues investing in forensic security inks and government-grade authentication systems. AlpVision SA specializes in invisible anti-counterfeit technologies integrated directly into product packaging materials.

Companies are increasingly developing cloud-based authentication platforms and smartphone-enabled verification tools to improve consumer engagement and supply chain monitoring. Strategic collaborations between packaging providers, pharmaceutical manufacturers, and e-commerce companies are expected to intensify competition during the forecast period.

Key Players List

- Avery Dennison Corporation

- CCL Industries Inc.

- Zebra Technologies Corporation

- SICPA Holding SA

- AlpVision SA

- Authentix Inc.

- SATO Holdings Corporation

- 3M Company

- DuPont de Nemours Inc.

- UPM Raflatac

- Brady Corporation

- Honeywell International Inc.

- Impinj Inc.

- De La Rue plc

- Optel Group