Anti Corrosion Packaging Products Market Size and Growth

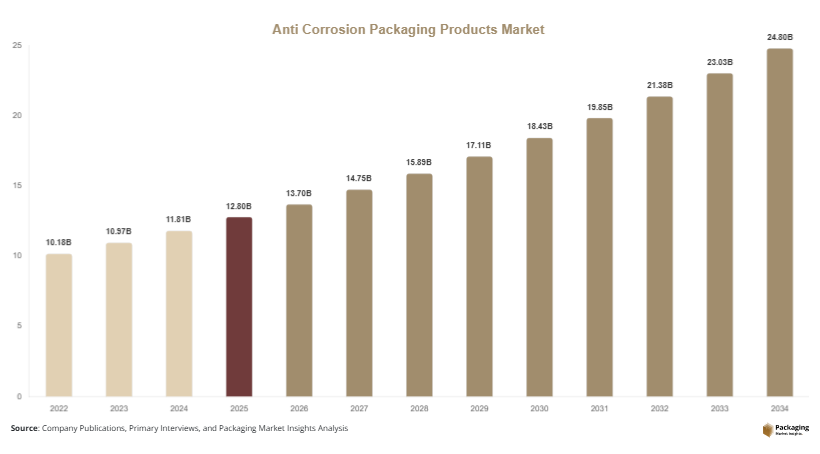

The global anti corrosion packaging products market was valued at USD 12.8 billion in 2025 and is projected to reach USD 13.7 billion in 2026. By 2034, the market is forecast to grow to USD 24.9 billion, registering a CAGR of 7.7% during 2025–2034.

The market’s growth trajectory is being driven by rising industrial exports, increasing demand for long-duration packaging protection, and broader adoption of specialized corrosion prevention systems in manufacturing supply chains. One major growth factor is expansion in automotive parts trade, where steel and aluminum components require protective packaging for overseas shipment. Another strong driver is increasing investment in defense and aerospace logistics, where high-value metal assemblies require corrosion-resistant packaging for long storage periods. A third growth factor is the rapid adoption of advanced moisture-barrier and VCI-based packaging in electronics and industrial equipment distribution.

Key Highlights

- Asia Pacific dominated the market with a 36.8% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 8.1%.

- VCI films led the type segment with a 32.4% share.

- Polyethylene-based packaging dominated the material segment with a 46.7% share.

- Automotive applications led the end-use segment with 27.9% share.

- The US remained the dominant country with a market size of USD 2.6 billion in 2025 and USD 2.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable Corrosion Protection Packaging

A major trend in the anti corrosion packaging products market is the increasing shift toward sustainable corrosion protection solutions that reduce environmental impact while maintaining protective performance. Packaging manufacturers are developing recyclable VCI films, water-based corrosion inhibitor coatings, compostable barrier wraps, and reusable anti-corrosion packaging systems for industrial clients. Automotive and machinery manufacturers are actively replacing conventional multilayer plastic packaging with recyclable mono-material anti-corrosion films to align with sustainability commitments. Industrial exporters are also adopting reusable corrosion-protection packaging for closed-loop logistics systems involving repeat shipments of machinery components. This trend is expected to accelerate innovation in green inhibitor chemistry, recyclable barrier materials, and low-emission packaging manufacturing processes, creating a broader sustainable packaging category within industrial protective packaging.

Integration of Smart Monitoring Features in Protective Packaging

Another emerging trend is the integration of smart packaging features into anti-corrosion packaging systems. Manufacturers are increasingly combining humidity indicators, oxygen sensors, digital condition tags, and corrosion exposure monitoring labels with protective packaging formats. These features provide logistics managers and industrial buyers with real-time condition visibility during storage and transportation. For example, aerospace component suppliers are using monitored corrosion-protection packaging for long-distance shipment of sensitive metal assemblies. Electronics manufacturers are also integrating environmental exposure indicators into protective wraps for precision components. In the future, smart anti-corrosion packaging may integrate RFID-enabled environmental monitoring systems, improving traceability, reducing product damage risk, and supporting predictive packaging quality management.

Market Drivers

Expansion of Global Industrial Component Trade

One of the strongest drivers of the anti corrosion packaging products market is the expansion of global trade in industrial metal components, machinery parts, fabricated equipment, and engineered assemblies. International shipping exposes metal products to humidity, salt air, condensation, and temperature fluctuations that increase corrosion risk. As global industrial sourcing becomes more geographically diversified, packaging protection requirements are increasing. Automotive transmission parts, fabricated steel assemblies, industrial bearings, marine equipment, and precision tools all require reliable anti-corrosion packaging during transit and warehousing. Manufacturers are therefore investing in VCI films, inhibitor papers, moisture barriers, and desiccant-integrated packaging systems to reduce damage rates and protect asset value across global supply chains.

Increasing Need for Long-Term Storage Protection

The growing need for long-term industrial storage protection is another major market driver. Defense equipment, replacement machinery parts, oilfield components, electrical assemblies, and aerospace parts are often stored for extended periods before deployment or use. Without protective packaging, these components are exposed to oxidation, moisture attack, and micro-surface corrosion that can reduce performance or increase maintenance requirements. Anti-corrosion packaging provides a controlled preservation environment that extends storage life while reducing preservation costs compared to repeated maintenance treatments. Warehousing expansion across industrial economies is increasing use of long-duration corrosion protection systems, particularly for high-value inventory management.

Market Restraint

Performance Variability Across Environmental Conditions

A major restraint in the anti corrosion packaging products market is the variability in packaging performance across different environmental and storage conditions. Corrosion protection effectiveness can vary depending on humidity levels, exposure duration, salt content in the air, packaging sealing quality, temperature variation, and the type of metal being protected. VCI packaging systems, for example, require appropriate enclosure design and correct dosage concentration to create an effective protective atmosphere. If packaging is damaged or improperly sealed, corrosion protection may weaken significantly.

Mixed-metal packaging applications present additional complexity because inhibitor chemistry suitable for steel may not perform equally well for copper, aluminum, or alloy systems. Heavy marine transport environments also create extreme conditions where standard protective packaging may require reinforcement through multilayer barriers or hybrid packaging systems. Industrial buyers often require product testing and customization before large-scale adoption, increasing qualification time and packaging system complexity.

In emerging markets, inconsistent packaging handling standards and lower awareness of corrosion science can reduce real-world performance outcomes. This creates hesitation among some industrial buyers regarding product reliability. Manufacturers must therefore invest heavily in technical education, packaging customization, and climate-specific formulation development to maintain market confidence.

Market Opportunities

Growth in Electronics and Precision Equipment Packaging

The rapid expansion of electronics manufacturing and precision industrial equipment packaging presents a major growth opportunity for anti-corrosion packaging suppliers. Precision connectors, conductive metal components, semiconductor equipment parts, sensors, and advanced electrical systems are increasingly vulnerable to oxidation and micro-corrosion during logistics and warehousing. Anti-corrosion films, static-safe VCI packaging, and hybrid moisture-control systems are gaining wider use in electronics packaging ecosystems. As precision manufacturing expands globally, demand for contamination-free corrosion protection packaging solutions is expected to increase significantly, creating higher-value specialty packaging opportunities.

Rising Demand in Defense and Offshore Equipment Logistics

Defense logistics and offshore industrial operations offer another major opportunity. Naval systems, defense machinery, ammunition storage hardware, aerospace components, offshore drilling equipment, and marine industrial assemblies require long-term corrosion prevention under severe environmental conditions. Anti-corrosion packaging designed for salt-rich atmospheres, humidity extremes, and extended warehousing is becoming essential in these sectors. Governments are increasing defense storage modernization, while offshore energy projects continue to expand specialized equipment logistics. This creates long-term demand for premium protective packaging systems with enhanced barrier performance and multi-year preservation capability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.8 Billion |

| Market Size in 2026 | USD 13.7 Billion |

| Market Size in 2034 | USD 24.9 Billion |

| CAGR | 7.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

VCI films dominated the anti corrosion packaging products market in 2024 with a 32.4% market share, primarily due to their broad industrial usability, flexible packaging formats, and reliable vapor-phase corrosion protection across enclosed packaging environments. These films release corrosion inhibitors that form a protective molecular layer on exposed metal surfaces, helping prevent oxidation without direct coating application. VCI films are widely used for automotive components, fabricated steel parts, bearings, marine assemblies, tools, and industrial replacement components. Their transparency also allows visual inspection without opening packages, improving logistics efficiency. Manufacturers increasingly prefer VCI films because they reduce secondary preservation steps, lower labor requirements, and support multi-metal packaging systems when formulated correctly. New recyclable VCI film formulations are also strengthening segment dominance in environmentally regulated markets.

Anti-corrosion emitters are projected to be the fastest-growing type segment, expanding at a CAGR of 8.5% through 2034. These products provide concentrated vapor-phase corrosion protection in enclosed storage spaces such as machinery cabinets, electrical housings, defense storage crates, and export containers. Their growth is being driven by increasing long-duration equipment storage, military logistics modernization, and expansion of industrial warehousing systems. Emitters are especially valuable for hard-to-reach internal cavities in machinery where direct packaging films may provide incomplete protection. Future innovation in programmable inhibitor release systems and long-life emitter cartridges is expected to expand applications in aerospace storage, marine equipment preservation, and precision industrial machinery packaging.

By Material

Polyethylene-based packaging materials led the material segment in 2024 with a 46.7% share, driven by their durability, flexibility, moisture resistance, processing efficiency, and compatibility with VCI chemistry. Polyethylene films and wraps are widely used in industrial packaging due to strong sealing performance, puncture resistance, and adaptability across custom packaging sizes. Heavy machinery exporters often use reinforced polyethylene anti-corrosion films for wrapping fabricated steel structures and sensitive equipment components. Electronics manufacturers also favor specialty polyethylene protective packaging because static-safe and barrier-enhanced formulations can be developed for combined corrosion and contamination protection. In addition, polyethylene packaging remains cost-effective at industrial scale, making it widely accessible across large-volume protective packaging applications.

Recyclable barrier laminates are forecast to be the fastest-growing material segment at a CAGR of 8.2%, supported by sustainability goals and rising demand for long-duration high-performance packaging systems. These advanced laminates combine moisture resistance, oxygen barrier protection, and corrosion inhibitor compatibility while improving recyclability compared with traditional multilayer protective packaging. Industrial exporters are increasingly adopting recyclable barrier laminates for sensitive machine assemblies, aerospace parts, and high-value engineered equipment shipped across long transit cycles. Future development in mono-material high-barrier packaging systems will likely accelerate adoption further, particularly in Europe and North America where circular packaging regulations continue to tighten.

By End-Use

Automotive dominated the end-use segment in 2024 with a 27.9% market share, supported by rising exports of engines, transmissions, chassis systems, fabricated components, and aftermarket replacement parts requiring corrosion protection during transport and warehousing. Metal-intensive automotive parts are highly vulnerable to moisture exposure, especially during ocean shipping and long-term inventory storage. Anti-corrosion packaging systems such as VCI films, moisture barrier bags, and inhibitor papers are widely used to preserve component quality and reduce warranty losses linked to oxidation damage. EV component supply chains are also increasing demand for protective packaging for battery housings, conductive metal systems, and precision electrical assemblies. Automotive’s global production scale and complex logistics needs continue to support segment leadership.

Electronics packaging is projected to be the fastest-growing end-use segment, expanding at a CAGR of 8.4% through 2034. Growth is being driven by rising exports of precision electrical assemblies, semiconductor equipment, conductive components, and advanced industrial electronics vulnerable to micro-corrosion and oxidation. Static-safe anti-corrosion packaging is increasingly used for connectors, sensors, control systems, and precision conductive assemblies. Hybrid packaging systems that combine corrosion protection, moisture control, and contamination prevention are gaining traction in electronics manufacturing ecosystems. With global electronics supply chains expanding rapidly, specialty anti-corrosion packaging designed for precision assemblies is expected to become a high-value growth segment.

Anti Corrosion Packaging Products Market Segmentations

By Type

- VCI Films

- VCI Papers

- Anti-Corrosion Bags

- Anti-Corrosion Emitters

- Foams & Wraps

- Desiccant Integrated Packaging

- Barrier Laminates

By Material

- Polyethylene-Based Packaging

- Polypropylene-Based Packaging

- Paper-Based Protective Packaging

- Recyclable Barrier Laminates

- Hybrid Composite Packaging Materials

By End-User

- Automotive

- Electronics

- Aerospace & Defense

- Heavy Machinery

- Marine Equipment

- Industrial Spare Parts

- Oil & Gas Equipment

Regional Analysis

North America

North America accounted for 24.6% of the anti corrosion packaging products market share in 2025 and is projected to grow at a CAGR of 6.8% through 2034. The regional market is supported by strong aerospace manufacturing, defense logistics modernization, automotive component exports, and industrial warehousing expansion. Demand is increasing for VCI films, corrosion inhibitor papers, and multilayer barrier wraps used in machinery packaging, fabricated metal parts, and industrial spare component preservation. Rising industrial automation equipment shipments are also increasing packaging protection requirements. Growth is further supported by stricter quality assurance standards for long-distance industrial shipping, especially in sectors handling precision metal assemblies and high-value replacement parts.

The United States dominates the regional market due to its extensive industrial exports, defense storage infrastructure, and advanced packaging technology ecosystem. A unique growth driver in the U.S. is the expansion of aerospace component logistics networks, where anti-corrosion packaging is increasingly used for high-precision turbine components, landing gear systems, and aircraft spare assemblies stored for extended periods. Packaging suppliers are developing aerospace-grade monitored corrosion protection systems that combine humidity control, barrier films, and real-time exposure indicators, improving long-duration preservation reliability.

Europe

Europe held 26.1% of the global anti corrosion packaging products market in 2025 and is expected to register a CAGR of 7.0% during 2025–2034. The market benefits from strong automotive exports, industrial equipment manufacturing, marine engineering, and expanding circular packaging initiatives. Demand is growing for recyclable VCI papers, reusable anti-corrosion wraps, and moisture-controlled protective packaging designed for industrial exports. Machinery manufacturers across Europe are increasingly adopting high-barrier protective packaging for global shipment of fabricated steel equipment and engineered assemblies. Sustainability regulations are also encouraging adoption of environmentally compliant inhibitor chemistry, creating opportunities for next-generation green corrosion packaging products.

Germany remains the dominant country in Europe due to its strong industrial manufacturing base and export-driven machinery sector. A unique growth driver in Germany is the increasing export of high-value precision engineering systems that require climate-stable anti-corrosion packaging during long-distance shipment. German packaging suppliers are integrating multilayer recyclable barrier systems with tailored inhibitor chemistry for steel, copper, and alloy component protection. Industrial digitization is also encouraging adoption of smart packaging indicators that monitor exposure conditions during transport and warehousing.

Asia Pacific

Asia Pacific dominated the anti corrosion packaging products market with a 36.8% share in 2025 and is projected to grow at a CAGR of 8.0% through 2034. The region benefits from rapid industrialization, strong electronics manufacturing, expansion in automotive production, and rising exports of fabricated metal products. Packaging demand is increasing for VCI films, anti-corrosion bags, desiccant packaging systems, and multilayer moisture barriers used in machinery parts, industrial electronics, and automotive components. Warehousing modernization across regional manufacturing hubs is also increasing adoption of long-duration protective packaging systems. Growth is further supported by rising infrastructure investment and expanding marine industrial supply chains.

China remains the dominant country in Asia Pacific due to its large manufacturing output, broad export base, and integrated industrial supply chain ecosystem. A unique growth driver in China is the rapid growth in electronics and industrial component exports requiring contamination-free corrosion prevention packaging. Manufacturers are increasingly using static-safe VCI packaging and advanced moisture barrier laminates for connectors, precision assemblies, and electrical systems. Domestic packaging producers are also scaling production of recyclable corrosion-protection materials to meet both industrial demand and sustainability targets.

Middle East & Africa

The Middle East & Africa accounted for 7.4% of the anti corrosion packaging products market in 2025 and is forecast to expand at a CAGR of 7.3% during the forecast period. Demand is increasing due to oil & gas equipment logistics, marine infrastructure development, industrial diversification programs, and growth in regional heavy equipment imports. Corrosion exposure risk is especially high in coastal and humid industrial environments, increasing demand for high-performance barrier packaging, long-duration inhibitor systems, and desiccant-integrated protective wraps. Industrial warehousing expansion in Gulf economies is further increasing consumption of corrosion-prevention packaging for stored machinery components and replacement industrial parts.

Saudi Arabia dominates the region due to large industrial infrastructure investment and strong demand for equipment preservation in oilfield logistics chains. A unique growth driver is expansion in offshore and petrochemical equipment storage, where metal-intensive systems require specialized packaging that protects against salt-rich humidity and extreme temperature fluctuations. Packaging suppliers are introducing multilayer marine-grade anti-corrosion barrier systems specifically designed for long-term equipment storage in harsh climatic conditions.

Latin America

Latin America held 5.1% of the anti corrosion packaging products market share in 2025 and is expected to record the fastest CAGR of 8.1% through 2034. Market growth is being supported by expansion in mining equipment logistics, agricultural machinery trade, industrial warehousing, and rising automotive component manufacturing. Export-oriented industrial sectors increasingly require reliable corrosion-prevention packaging for long shipping routes and variable climatic exposure. Packaging suppliers are also introducing cost-effective anti-corrosion paper systems and hybrid desiccant packaging products suited for regional industrial clients. Growth in port infrastructure and regional trade integration is further strengthening packaging demand.

Brazil remains the dominant country in Latin America due to its large industrial economy and growing machinery export base. A unique growth driver in Brazil is the expansion of agricultural equipment exports, where large steel-intensive machinery components require moisture-resistant and corrosion-protective packaging during ocean freight. Packaging providers are increasingly supplying reinforced VCI wraps and custom industrial protective systems designed for oversized machinery parts, supporting long-distance logistics reliability.

Competitive Landscape

The anti corrosion packaging products market is moderately fragmented, with competition centered on inhibitor chemistry innovation, sustainable packaging design, customized industrial solutions, and global supply capability. Cortec Corporation remains the market leader due to its broad anti-corrosion packaging portfolio, extensive VCI technology expertise, and strong global industrial customer base spanning automotive, defense, marine, and heavy machinery sectors.

Daubert Cromwell continues expanding through high-performance corrosion protection films and industrial export packaging systems tailored to metal-intensive supply chains. Armor Protective Packaging focuses on VCI packaging innovation for industrial components and global equipment logistics. Branopac India Pvt. Ltd. is strengthening regional penetration through specialized anti-corrosion paper systems and moisture-control packaging technologies. NTIC (Northern Technologies International Corporation) remains active in environmentally compliant corrosion inhibitor chemistry and specialty protective packaging systems.

Competitive strategies include development of recyclable VCI materials, smart monitoring packaging integration, industry-specific packaging customization, and expansion into emerging industrial logistics markets. Companies are also investing in climate-specific packaging formulations designed for marine, desert, and high-humidity industrial environments.

Key Players List

- Cortec Corporation

- Daubert Cromwell

- Armor Protective Packaging

- Northern Technologies International Corporation (NTIC)

- Branopac India Pvt. Ltd.

- Zerust Excor

- MetPro Group

- Aicello Corporation

- Green Packaging Inc.

- Protective Packaging Corporation

- OJI F-Tex Co., Ltd.

- Smurfit Kappa Industrial

- Transcendia Inc.

- Intertape Polymer Group

- RustX USA

- Shenyang Rustproof Packaging Materials Co., Ltd.

- Polyplus Packaging

- Safepack Industries Ltd.